Download presentation

Presentation is loading. Please wait.

1

Risk and Term Structure of Interest Rates Chapter 6

2

Learning Objectives Relate the risk of a security to its yield. Identify the three largest credit rating agencies. Explain flight to quality. Define the term structure of interest rates. Describe the yield curve. Outline the theories of term structure.

3

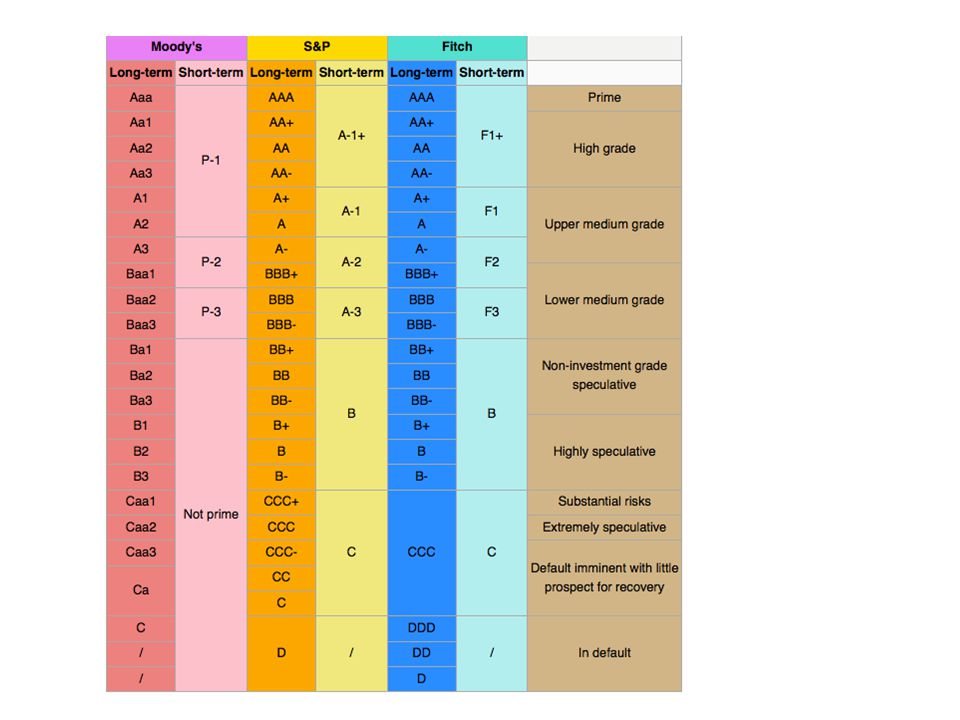

Bond Ratings Grades assigned to bonds indicating the likelihood of default.

4

“Big three” nationally recognized ratings organizations 1.Moody’s Investor Services 2.Standard and Poors 3.Fitch Ratings

6

Rating on U.S. Treasury Securities August 6, 2011

7

Risk Structure of Interest Rates 7

8

Credit Risk Spread Difference between a low risk and high risk security. In recessions the credit risk spread widens.

9

Flight to quality Demand for high quality bonds goes up Demand for low quality bonds goes down

11

Maturity Structure of Interest Rates 11

12

The Yield Curve http://stockcharts.com/freecharts/yieldcurve.h tml

13

Why does the “normal” yield curve slope upward? Long term securities carry more interest rate risk so require high yields to compensate.

14

Why might the yield curve flatten or even become inverted Investors think that interest rates will drop so want to lock into high long term rates. If interest rates do drop their long-term bonds will appreciate.

15

Expectations Hypothesis: part of the story The long rate is the average of future short rates. So if one year rates for the next three years are 3%, 4%, 5%, the expectations hypothesis says that the three year rate is 4% (the average.)

.")

Similar presentations

: A plot of the interest rates of Treasury Bills and Treasury Bonds versus their maturities.>")