Download presentation

Presentation is loading. Please wait.

1

UASFAA Fall Conference April 18, 2013 Yes…Another Presentation on Default Prevention

2

Bio Rose Amador, Call Center Supervisor 7 Years Experience in Loan Servicing, Default Prevention and Default Collections Joined UHEAA in 2006 to establish in-house servicing Direct Experience – Collector to Supervisor Primary Experience: Default Prevention Part of UHEAA’s Default Prevention Team that helped UHEAA reach the #1 cohort default rate in the nation Part of UHEAA’s Default Prevention Team that helped UHEAA reach a 1.9% cohort default rate

3

U.S. Department of Education Fact Sheet, September 2011 “HBCUs have deployed innovative approaches towards default management and reduction. Such strategies include implementation of a default management plan that engages stakeholders, identifies approaches to reducing default rates, and tracks measureable goals. These schools have increased borrower awareness of obligations through incorporating borrower topics at orientation sessions and providing enhanced entrance and exit counseling. Other best practices include borrower tracking, increased contact with delinquent borrowers…and partnering with other stakeholders to optimize default prevention, resolution, and reduction.” [Fact Sheet September 12, 2011.]

4

NY Times Editorial Columnist, Gail Collins “…Don’t you think there should be someone in charge of calling [students] once a week and yelling: ‘$800 a month until you’re 51 years old’?” [New York Times, “The Lows of Higher Ed”, September 14, 2012 ]

![NY Times Editorial Columnist, Gail Collins …Don’t you think there should be someone in charge of calling [students] once a week and yelling: ‘$800 a month until you’re 51 years old’ [New York Times, The Lows of Higher Ed , September 14, 2012 ]](http://images.slideplayer.com/12/3459620/slides/slide_4.jpg "NY Times Editorial Columnist, Gail Collins …Don’t you think there should be someone in charge of calling [students] once a week and yelling: ‘$800 a month until you’re 51 years old’ [New York Times, The Lows of Higher Ed , September 14, 2012 ]")

5

Presentation Objective #1 Make the case that we have a motivation problem, not an information problem. Presentation Objective #2 Present our recommended strategy for preventing delinquent students from becoming defaulted students.

6

Keep in mind… CDR calculations based on # not $ Compare: 1 st -year student with $2,500 in debt vs. a graduating senior with $25,000. Who is most likely to default? Who is most difficult to help?

7

Keep in mind… Highest risk of default: Dropouts Most Critical Risk Indicator: Completion Most Important Success Indicator: Completion Average debt of 1 st year dropouts -- $4,500 Monthly payment over 10 years: $52

8

Keep in mind… Average debt of college seniors: $25,250* Monthly payment over 10 years: $291 *The Project on Student Debt, www.projectonstudentdebt.org

9

Keep in mind… The desired action is contact with the servicer Why? Only the servicer can solve the problem.

10

Consider this… A successful default prevention program must be strong enough to influence the behavior of the most difficult students. The students most likely to default are the most difficult students to influence. We have a motivation problem, not an information problem.

11

Debtor Psychology Two Obstacles Avoidance: “I don’t want to deal with this…” Ignorance: “I don’t know what to do about this…” First Obstacle is much harder to overcome than the second

12

Debtor Psychology Three Causes of Avoidance: Fear Confrontation Negative treatment Personal embarrassment

13

Debtor Psychology Second Cause of Avoidance: Procrastination “It’s only a student loan…” “It’s a government loan – it will take someone a long time to come after me.” “What are they going to do, repossess my brain?”

14

Debtor Psychology Third Cause of Avoidance: Feelings of Being Overwhelmed or Helpless “I cannot afford the past due amount…” “I have so many other problems…” “There is nothing I can do right now…”

15

Debtor Psychology How do we overcome avoidance? Borrower Communication that is: Persistent… Relentless… Sustained…

16

Debtor Psychology Second Obstacle: Ignorance Lack of Information about options & resources. Confusion about who to call.

17

Debtor Psychology How do we overcome ignorance? Information vs. Recommendations Recommendations are more important than information Giving information is not enough. We must tell them what to do and how to do it. “Contact your servicer” “Ask About…” “Here are links, resources, contact points…”

18

Debtor Psychology Our Objective: Motivate the borrower to contact the servicer

19

Our Recommendations Communication Strategy: Call Center Emails Text Messages Web Resources Skip Tracing Targeted Mailings Persistent, relentless and sustained communication of options, resources, and suggestions.

20

Our Recommendations Implement the Department’s Plan Engage Campus-Wide Stakeholders Identify Your Unique Borrower Profiles Set & Track Goals Implement Borrower Awareness Programs Strengthen & Enhance Orientations Strengthen Entrance & Exit Counseling Track Riskiest Borrowers Partnerships

21

Our Recommendations Collaborate with Federal Servicers Servicer’s School Representatives Servicer Website Servicer Ombudsman Office

22

Our Recommendations Sponsor or Link to Online Resources In-House Resources U.S. Department of Education Resources Commercial Resources

23

Our Recommendations Use NSLDS Reports Portfolio Reports Delinquency Reports Other Databases

24

Our Recommendations Timing of Borrower Communication Begin 90-Days Delinquent - Why? 90-Days Delinquent = 4 Payments Due Average 1 st Year Student Owes: $200 Average Senior Owes: $1,000 Avoidance in full swing…

25

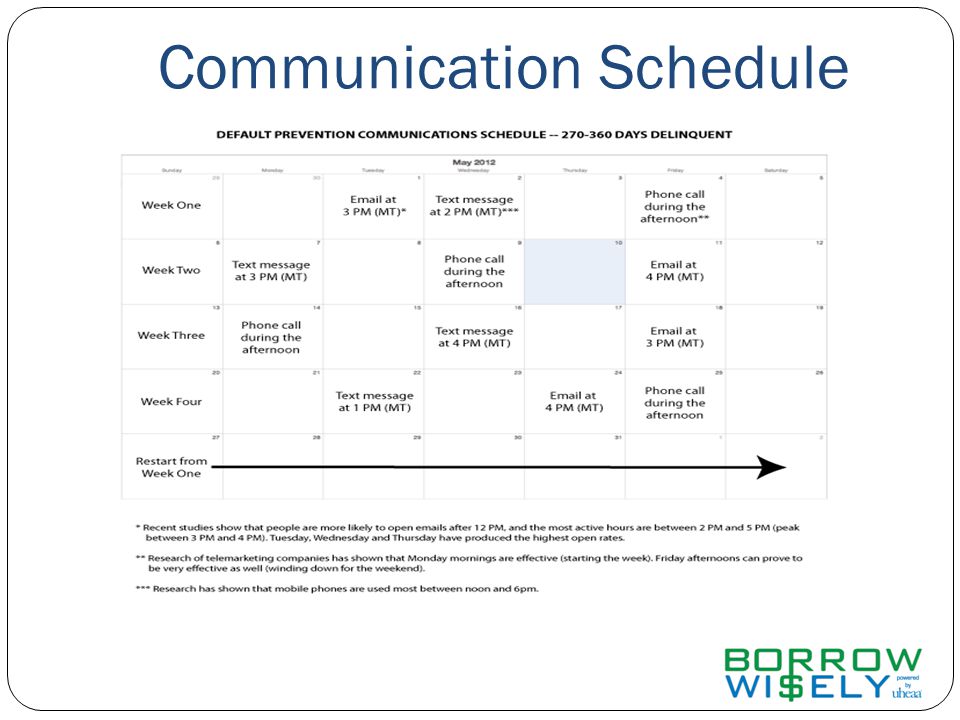

Communication Schedule

27

Results – How Do You Know? Follow delinquency This month’s 90-day delinquency is next month’s 120-day delinquency. You want the month-to-month historical trend lines to aim downward.

28

Results Don’t stop… Questions?

Similar presentations

AND.>")

On Campus 6 FAFSA Workshops (January & February)>")