Download presentation

Presentation is loading. Please wait.

1

Do XBRL Filings Take Longer Hui Du Kean Wu University of Houston – Clear Lake

2

“interactive data has the potential to increase the speed, accuracy and usability of financial disclosure, and eventually reduce costs” (SEC, 2009)

")

3

Timeliness of filing financial report Investor response to SEC filings, and the response is stronger around a 10-K date than a 10-Q date (Griffin, 2003) 10-Q allows investor to better assess the integrity of reported earnings (Balsam, Bartov, and Marguardt; 2002) Financial statement user utilize footnote information to make adjustments at the 10-K dates (Franco, Wong and Zhou, 2011)

10-Q allows investor to better assess the integrity of reported earnings (Balsam, Bartov, and Marguardt; 2002) Financial statement user utilize footnote information to make adjustments at the 10-K dates (Franco, Wong and Zhou, 2011)")

4

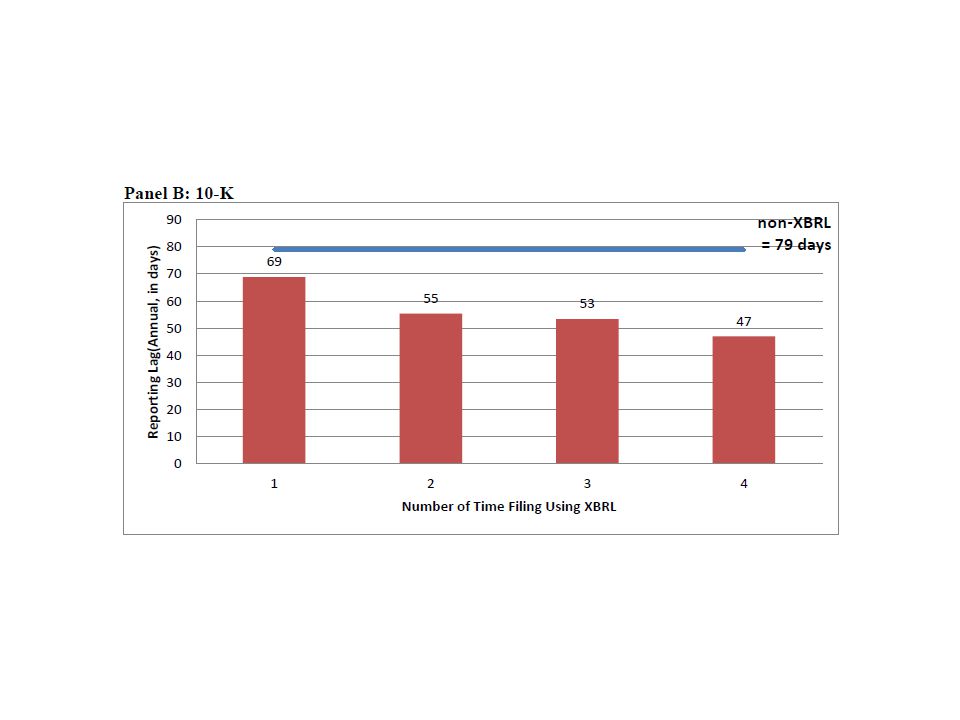

Main Findings Preview The time lags between fiscal year end and SEC filing date decrease for 76 days to 60 days for 10-K filings, and from 40 day to 36 days for 10- Q filing. These decreases in reporting lag only manifest for on-time filer, not for extension filer. In a 4 year window, reporting lags decrease from 69 days to 47 days for 10-K filings, from 38 days to 33 days for 10-Q filings.

5

Hypothesis Development Li, Lin, and Ni (2012) find XBRL adoption results in a significant reduction in cost of equity capital. Information system are able to process large and complex routings and tasks effectively and efficiently (Polites and Karahanna, 2013). Company using XBRL was moving 30% of its bookkeeping staff to different positions, and was able to decrease the reporting time (Pinsker and Li, 2008).

. Company using XBRL was moving 30% of its bookkeeping staff to different positions, and was able to decrease the reporting time (Pinsker and Li, 2008)..")

6

“Bunching” - a Disclosure Timing Theory Dye (2010) “the SEC’s recent initiatives regarding XBRL-tagging of financial data have been motivated in part to enhance the timeliness of financial reporting information.” Prediction: Information acquisition and disclosure at a single point in time.

the SEC’s recent initiatives regarding XBRL-tagging of financial data have been motivated in part to enhance the timeliness of financial reporting information. Prediction: Information acquisition and disclosure at a single point in time.")

7

Bunching under XBRL Acquire Disclose AcquireProcessDisclose Jan 1 Mar 1

8

H1: Financial statement filings using XBRL takes shorter time than financial statement filings without using XBRL.

11

Distribution of Reporting Lags(10-Q) Pre-XBRL Post-XBRL

Pre-XBRL Post-XBRL")

12

10-Ks Pre-XBRL Post-XBRL

13

Regression Model Reporting Lag = 0 + 1 XBRL+ 2 lnS + 3 INV + 4 GS5 + 5 lnA + 6 ROA + 7 Loss + 8 LEV + 9 AR + 10 IA + 11 GOOD +

16

TABLE 4 Comparison of Average Reporting Lags by Fiscal Year Fiscal10-Q Filings 10-K Filings Year XBRL non-XBRL XBRL non-XBRL Reporting Lag N N N N 1996 -4313,056 - 87 3,682 1997 -4314,704 - 87 3,848 1998 -4314,968 - 88 3,624 1999 -4415,032 - 88 3,627 2000 -4315,429 - 88 3,733 2001 -4315,850 - 87 3,664 2002 -4314,843 - 86 4,952 2003 -4214,503 - 79 5,219 2004 -4015,068 - 80 5,136 2005 -3914,857 - 77 5,045 2006 -3914,410 - 75 4,910 2007 -3913,902 - 73 4,806 2008 -3914,954 591 73 5,026 2009348153913,929 54438 73 4,528 2010342,9963911,299 551,298 75 3,507 2011379,670404,276 694,194 77 456 20123812,803 42692 61953 86 69

21

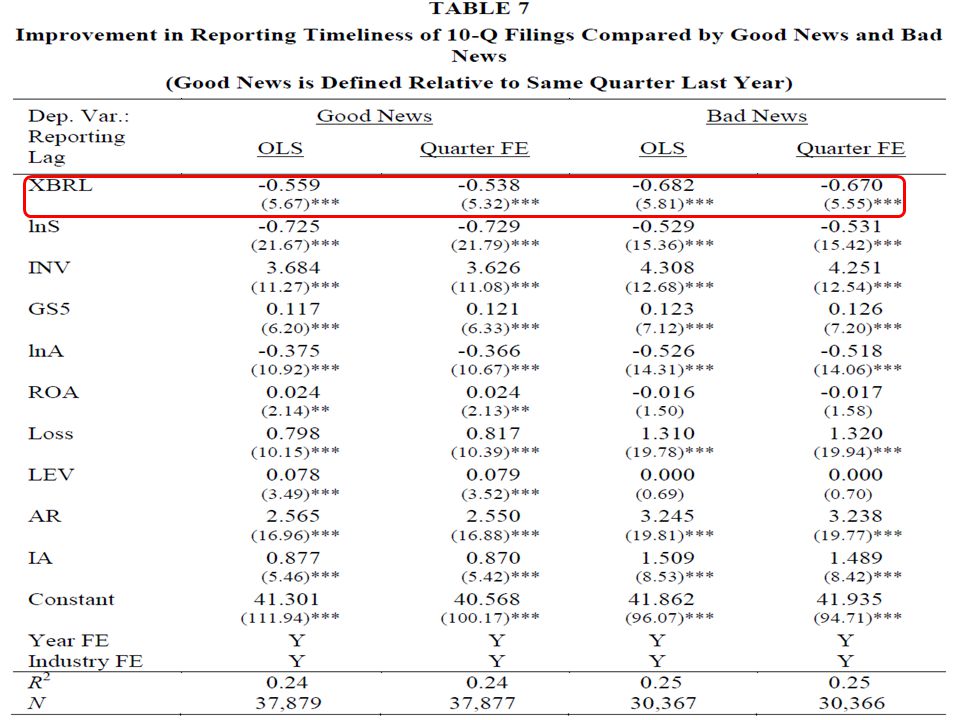

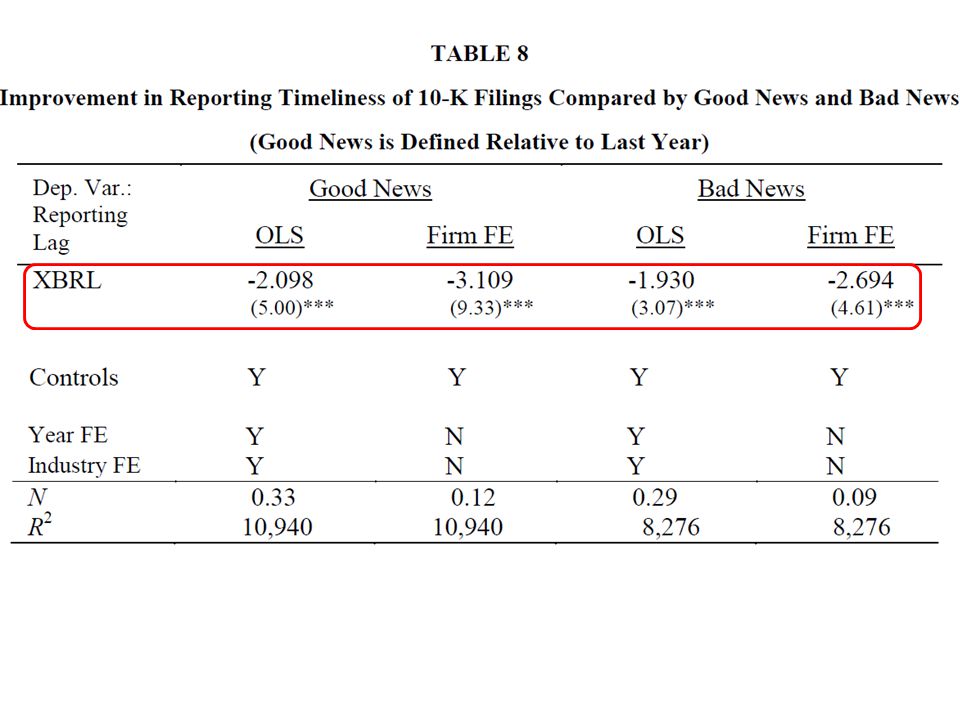

In disclosure “bunching” theory, one of the necessary conditions is that the presence of effective real-time reporting requirement. H2: The timely XBRL financial reporting is only among companies that make their filings in time, but not among companies that file extensions.

28

Concluding Remarks XBRL reduces reporting lag for both 10-Q and 10-K filings. We also document a decreasing trend of reporting lag after adoption of XBRL, suggesting a significant learning curve in the filing process. The improvement is more pronounced for on-time filers, but not for filers that requested filing extensions. Accounting information system improve reporting efficiency. This paper may also draw policy implication that XBRL mandate improves business information processing and reporting efficiency.

Similar presentations

XBRL: eXtensible Business Reporting Language PowerPoint Presentations.>")

platform for the analysis, exchange, and reporting of financial information with the purpose.>")

Maureen Mascha (University of Wisconsin – Oshkosh)>")