Download presentation

Presentation is loading. Please wait.

1

Financial reporting Oskar Otsus January 2013 Moldova

2

Topics: Eligible and ineligible costs Funding rates Overheads Form C Personnel costs Changes in budget Audits Most frequent errors in FP7 AND 2 EXERCISES!

3

Eligible vs non-eligible costs Funding rates

4

The forms of EC contribution of costs: Reimbursement of eligible costs – the statement of actual eligible costs, made during the project Flat rate (including scale of unit costs) – Flat rate can be: 1) scale of unit costs (for example one researcher in Marie Curie actions) 2) indirect costs / direct costs x 100% Lump-sum – fixed amount There is a possibility to combine the funding schemes within the project. For example: travel costs as lump sum, research activities as reimbursement of costs For International Cooperation Partner Countries (ICPC) the Commission proposes simplified method –flat rate lump-sum amounts. They have been defined on the basis of World Bank data on cross national income levels in different countries. The partners from ICPC can still request the standard reimbursement of eligible costs.

the Commission proposes simplified method –flat rate lump-sum amounts. They have been defined on the basis of World Bank data on cross national income levels in different countries. The partners from ICPC can still request the standard reimbursement of eligible costs..")

5

Reimbursement of eligible costs Cost Eligible DirectIndirect Non- eligible

6

Eligible costs of the project In order to be considered eligible the costs must be: (FP7 Grant Agreement – Annex II.14.): Actual Incurred by the beneficiary Incurred during the duration of the project Determined in accordance with the usual accounting and management principles and practices of the beneficiary Used for the sole purpose of achieving the objectives of the project Recorded in the accounts of the beneficiary

: Actual Incurred by the beneficiary Incurred during the duration of the project Determined in accordance with the usual accounting and management principles and practices of the beneficiary Used for the sole purpose of achieving the objectives of the project Recorded in the accounts of the beneficiary")

7

Non-eligible costs The following costs are considered as non-eligible: Identifiable indirect taxes including value added tax, Duties, Interest owed, Provisions for possible future losses or charges, Exchange losses, cost related to return on capital, Costs declared or incurred, or reimbursed in respect of another Community project Debt and debt service charges, excessive or reckless expenditure

8

Funding rates Depending on the type of the organisation Reasearch and development activities – 50% - 75%* Demonstration activities – up to 50% Project management activities – up to 100% Other activities – up to 100% Coordination and support actions - up to 100% * Higher education establishments, SME-s, non-profit public bodies, research organisations

9

Indirect costs Indirect costs are those eligible costs which cannot be identified as being directly attributed to the project but which is in direct relationship with the eligible direct costs and can be identified by its accounting system (phone and mobile phone costs, postal charges, bank fees, other office costs) 1.Real indirect cost method 2.Flat-rate (% of total direct eligible costs) Flat-rate’s: a) 20 % b) 60 % ( Higher education establishments, SME-s, non-profit public bodies, research organisations ) c) 7 % for coordination and support actions Indirect costs = (direct costs - subcontracting) x flat-rate

1.Real indirect cost method 2.Flat-rate (% of total direct eligible costs) Flat-rate’s: a) 20 % b) 60 % ( Higher education establishments, SME-s, non-profit public bodies, research organisations ) c) 7 % for coordination and support actions Indirect costs = (direct costs - subcontracting) x flat-rate")

10

How to calculate indirect costs? A university participates in an FP7 project: They use 60% flat-rate for calulating indirect costs They have only RTD tasks in the project (funded 75% by the EC) Costs of the university: Direct costs 100,000.- EUR Indirect costs (60%) 60,000.- EUR ------------------------------------------------- Total costs 160,000.- EUR EC contribution: (160,000x75%) 120,000.- EUR

Costs of the university: Direct costs 100,000.- EUR Indirect costs (60%) 60,000.- EUR Total costs 160,000.- EUR EC contribution: (160,000x75%) 120,000.- EUR.")

11

What did we talk about? Non-eligible costs Eligible costs Indirect costs flat-rate 60% Direct costs RTD 75% Other 100% Personnel Durables Equipment Travel Office costs Electricity …

12

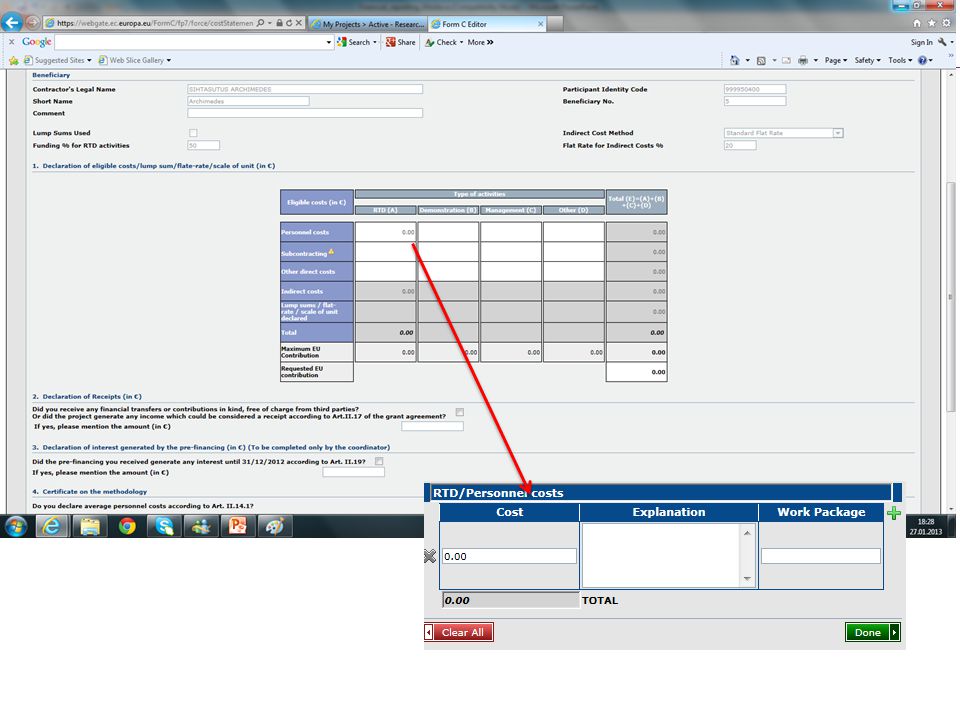

Form C – the financial report in FP7 75% 50%100%

13

Submitting the financial report Report on the costs of 1 period 1. Partner fills in the Form C electronically and submits to the coordinator 2. Coordinator collects and checks all the form C-s and send them to the Commission 3. Partner prints the form C, stamps, authorized representative signs 2 copys, send to the coordinator 4. Coordinator Collects the paper form C-s, checks them and send to the project officer New projects (starting 2013) will sign form C-s electronically Ongoing projects can choose to use electronic signature as well Amendments have to be sent separately

will sign form C-s electronically Ongoing projects can choose to use electronic signature as well Amendments have to be sent separately.")

18

Personnel costs

19

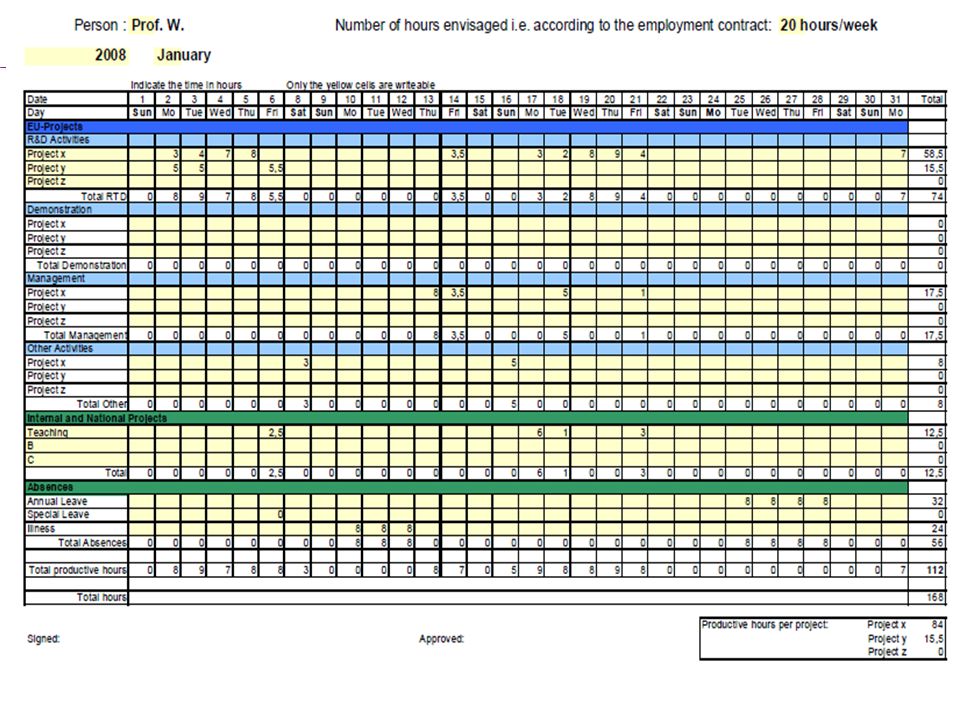

You must know the value of your person month Person month = salary + social charges + regular bonuses Example: Your person month rate is 2500 € Researcher works 6 month for the project (50% of his time) Personnel costs = 2 500 * 6/2 = 7 500 In FP7 you have to keep timesheets, unless you have a better system of proving your dedicated working time. Timesheets must be filled in with one day accuracy. Standard productive hours = 1680 hours/per year = 140 hours/per month This means: 1 person month = 140 hours

20

Productive hours Question: How many hours is 1 person month? You need to know the number of your productive hours European Commission calculation for standard productive hours: Days/year: 365 Weekends: 104 Vacation: 21 National holidays: 15 Average days on sick leave: 15 Working days in year: 365-104-21-15-15 = 210 Hours per one working day: 8 hours Productive hours per year: 210 x 8 = 1680 Productive hours per month: 1680/12 = 140

21

Time contributed to the project Timesheets are mandatory in FP7 projects, unless you have a better time recording system. Even people working full time for the project are recommended to use timesheets. Minimum recuirements for timesheets: Beneficiary name Name and signature of the employee Project name Number of hours worked (daily) Name and signature of the superior Timesheets must comply with sick leaves, holidays and travels Additional recommendations for timesheets Hours devided by work packages Explanation of work done

Name and signature of the superior Timesheets must comply with sick leaves, holidays and travels Additional recommendations for timesheets Hours devided by work packages Explanation of work done.")

26

Holiday fees Holiday allowances are eligible in FP7 projects Holiday allowances payd from the project budget must be in proportion with your time dedicated to the project. Your vacation must take place during the lifetime of the project You don’t need to fill in your days spent on holidays in the timesheets

27

Changes in budget During the lifetime of the project you can change the budget, but the entire work described in the Description of Work must be done All changes must be approved by the coordinator If there is a need to change activities foreseen in the Description of Work it must be approved by the project officer It is possible to change the allocation of budget between project partners, but the EC contribution always remains the same. Person months are not very strict. If you declare that your person month rate is 3000 €, it does not mean you have to pay all your employees 3000 €. The total budget for personnel costs is constant and average salaries should not differ much from the person month rate. The European Commission is always happy if you show you have contributed more to the project than foreseen :)

.")

28

Subcontracting A subcontractor is a type of third party : a legal entity which is not a beneficiary of the ECGA, and is not a signatory to it. subcontracting between beneficiaries in the same ECGA is not to be accepted Subcontracting can not be a core part of the work Subcontracting costs have to be identified in the Annex I of the grant agreement Minor subcontracting does not have to be identified in the annex 1 (The criteria to decide whether a subcontract concerns minor tasks are qualitative and not quantitative)

.")

29

Audits Audit of the Methology is neccessary for beneficiaries using the real indirect costs to be performed once in the lifetime of FP7. It can be used for all FP7 Grant Agreements. Audit of the Financial Statement is obligatory only in the case of reimbursement of real costs, when EC contribution is over 375 000.-EUR. The EC may, at any time during the project and up to 5 years after the end of the project, arrange for financial, systemic and technical audits to be carried out by external auditors or by the EC staff including European Anti-Fraud Office (OLAF).

..")

30

Most Frequent errors in FP7 1. Costs claimed that are not substantiated or are not linked to the project 2. Third parties and sub-contracting 3. Depreciation 4. Indirect cost models 5. Indirect costs - Ineligible costs included in the pool of indirect costs 6. Personnel costs - Calculation of productive hours 7. Personnel costs - charging of hours worked on the project 8. Personnel costs - Use of average personnel costs 9. Payment of salaries to owner/managers of SMEs 10. VAT

31

What did we talk about? 1.Eligible vs ineligible costs 2.Funding rates 3.Submitting the form C 4.Personnel costs and timesheets 5.Subcontracting 6.Audits 7.Errors in FP7 Oskar Otsus Estonian Research Council tel: +372 7 317 350 e-mail: oskar.otsus@etag.ee

Similar presentations

is co-funded by the European Community's ICT Programme under FP7 6 - Resource Allocation and Budgeting.>")

Grant Agreement / between EC and VITO / relevant for all partners B) Consortium Agreement / between partners / relevant for EC.>")