Download presentation

Presentation is loading. Please wait.

1

Women in the Global Corporate Elite: Evidence from the 2006 Global Fortune 500 Clifford L. Staples Heather Jackson Department of Sociology University of North Dakota, USA

2

Purpose of Research Study the rise of the Transnational Capitalist Class or Global Corporate Elite Explore the role of women in the Global Corporate Elite Specifically, explain variation in the presence, or absence, of women on FG500 boards

3

Previous Research Most work has been descriptive and/or normative No studies specifically of the FG500 Need to understand and explain diversity in the global power elite and its consequences

4

Data Fortune Global 500 (498) for 2006 Director names from company web-sites collected in late 2006-early 2007 Sex coded from name, photos, press coverage, web-searches, etc.

for 2006 Director names from company web-sites collected in late 2006-early 2007 Sex coded from name, photos, press coverage, web-searches, etc.")

5

Descriptive Findings 6,633 directors, 5,743 individuals Consistent with previous research on top corporate boards, we find only a small minority are female. Of the 5,743 individual directors 584, or 10.2% are women There are, however, differences by the country in which the corporation is headquartered

6

Country Men Women Number of companies Norway 60.87% 39.13% 2 Sweden 75.61% 24.39% 6 Australia 77.89% 22.11% 8 Denmark 79.31% 20.69% 2 United States 83.31% 16.69% 171 Finland 85.00% 15.00% 2 Canada 85.43% 14.57% 14 United Kingdom 88.03% 11.97% 39 Netherlands 90.12% 9.88% 14 France 90.27% 9.73% 35 Brazil 90.32%. 9.68% 1 Germany 90.44% 9.56% 12 Switzerland 90.45% 9.55% 38 Ireland 90.91% 9.09% 4 Hong Kong 92.86% 7.14% 1 Thailand 92.86% 7.14% 1 Turkey 93.75% 6.25% 5 Belgium 94.05% 5.95% 5 Russia 94.55% 5.45% 1 China 94.57% 5.43% 5 Spain 97.28% 2.72% 21 South Korea 97.46% 2.54% 9 Mexico 97.67% 2.33% 12 Italy 97.97% 2.03% 10 India 98.61% 1.39% 6 Japan 98.96% 1.04% 69 Malaysia 100.00% 0.00% 1 Venezuela 100.00% 0.00% 1 Saudi Arabia 100.00% 0.00% 1 Austria 100.00% 0.00% 1 Taiwan 100.00% 0.00% 1

7

Descriptive Findings

8

On average, there are 1.38 women per board as compared to 11.94 men per board Proportionally, women represent from 0% to 50%, with an average of 10.55% per board.

9

Royal AholdNetherlands50.00 StatoilNorway46.15 La PosteFrance42.85 Albertson'sUnited States42.85 Nordea BankSweden36.36 SyscoUnited States36.36 Sara LeeUnited States36.36 AT&TUnited States35.29 CFEMexico33.33 AetnaUnited States33.33 J.C. PenneyUnited States33.33 Merrill LynchUnited States33.33 XeroxUnited States33.33 McKessonUnited States33.33 Office DepotUnited States33.33 WellpointUnited States31.25 ElectroluxSweden30.76 Johnson & JohnsonUnited States30.76 Washington MutualUnited States30.76 TIAA-CREFUnited States30.76 Norsk HydroNorway30.00 U.S. Postal ServiceUnited States30.00 CignaUnited States30.00 3MUnited States30.00 AccentureUnited States30.00 UnitedHealth GroupUnited States30.00 Coles MyerAustralia30.00

10

Descriptive Findings The correlation between number of women on the board and proportion of women on the board is quite high (.908), suggesting that the boards that do include women are replacing men rather than simply adding women and increasing board size Consistent with this interpretation, the correlation between board size and proportion of women is relatively low (.190)

, suggesting that the boards that do include women are replacing men rather than simply adding women and increasing board size Consistent with this interpretation, the correlation between board size and proportion of women is relatively low (.190)")

11

Accounting for Women on FG500 Boards While in the aggregate the proportion of women in the Global Corporate Elite is quite low (10- 15%), there is considerable variation in the proportion of women on FG500 boards How can we explain this variation? How might the Global Corporate Elite become less male-dominated?

12

Accounting for Women on FG500 Boards Proponents of increasing the number of women on corporate boards stress the importance of “networking,” but there is little empirical research on how, or if, social networks might play a role. While we do not have data on personal networks, because of director interlocks we do have network data for the corporations and directors of the FG500 (ex. Anne Mulcahy)

.")

14

Accounting for Women on FG500 Boards Corporate boards are interested in minimizing uncertainty and discomfort and maximizing comfort and predictability (Kantor) Women in the heretofore all-male world of the corporate elite are seen as a threatening and potentially disruptive to this world Given that women on corporate boards are few and far between many boards and most male directors have little or no experience with female colleagues on boards

Women in the heretofore all-male world of the corporate elite are seen as a threatening and potentially disruptive to this world Given that women on corporate boards are few and far between many boards and most male directors have little or no experience with female colleagues on boards")

15

Accounting for Women on FG500 Boards Thus, knowledge of what it is like to serve on a diverse board is a bit of social capital that is unevenly distributed across this community Given that possession of this knowledge will tend to reduce uncertainty, we would suggest that the inclusion of women on corporate boards within the community will generally follow the diffusion of such knowledge

16

Accounting for Women on FG500 Boards And given that the diffusion of such knowledge is likely to be transmitted via both formal and informal connections, we would predict that, other things equal, the most connected firms– the firms with the most ties to other firms—will be more likely to have any women directors as well as a greater proportion of female directors.

17

Accounting for Women on FG500 Boards First we treat both independent and dependent variables as dichotomous (interlocks/no interlocks by women/no women)

")

18

Chi-Square 90.71, 1df, sig..000

19

Accounting for Women on FG500 Boards Shifting to measuring the dependent variable as the proportion of women on the board, and controlling for the size of the company– a variable thought to be important by some– the results are substantively the same, with a substantively and statistically significant effect (.313) for having any connections. Though smaller (.216), the effect when using the number of links as the independent variable holds up.

, the effect when using the number of links as the independent variable holds up..")

21

Accounting for Women on FG500 Boards The extent to which firms with women are connected, and to each other in particular, can be seen from two contrasting network diagrams The first diagram shows the connections, or lack of connections, between firms that no women on the board. Of the 155 firms without women, only 57 have a tie to another firm, the majority (63.2%) are “isolates.” And as is evident, the network is very fragmented.

are isolates. And as is evident, the network is very fragmented..")

22

Companies with no women on Board

23

Accounting for Women on FG500 Boards The second diagram shows the network produced by corporations who have women on board. Of the 343 firms with women, all but 49 are connected to another firm, and, in fact, 291, or 84.8%, are connected in one network. Thus, it is not only the case that connected firms are more likely to have a woman on the board; most of the firms with women on board are connected to each other.

24

Companies with women on Board

25

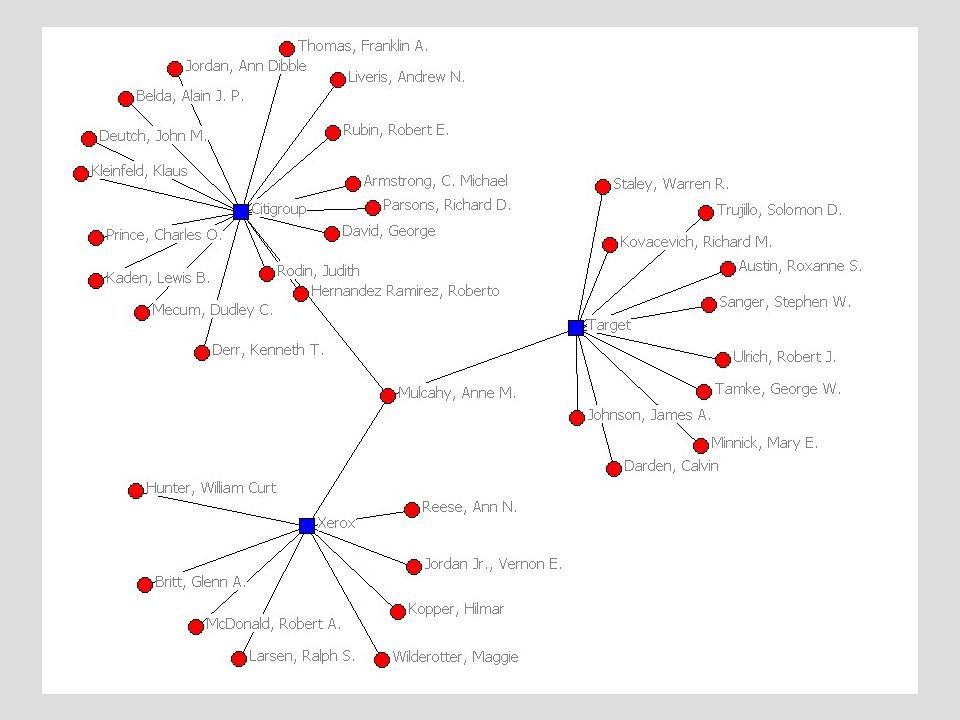

Interlocks and Networks An interlock occurs when an individual corporate director serves on the boards of two or more companies Such an interlock connects the companies and individuals involved into a network. Anne Mulcahy, for example, as of 2006 served on the boards of Target, Xerox, and Citigroup

26

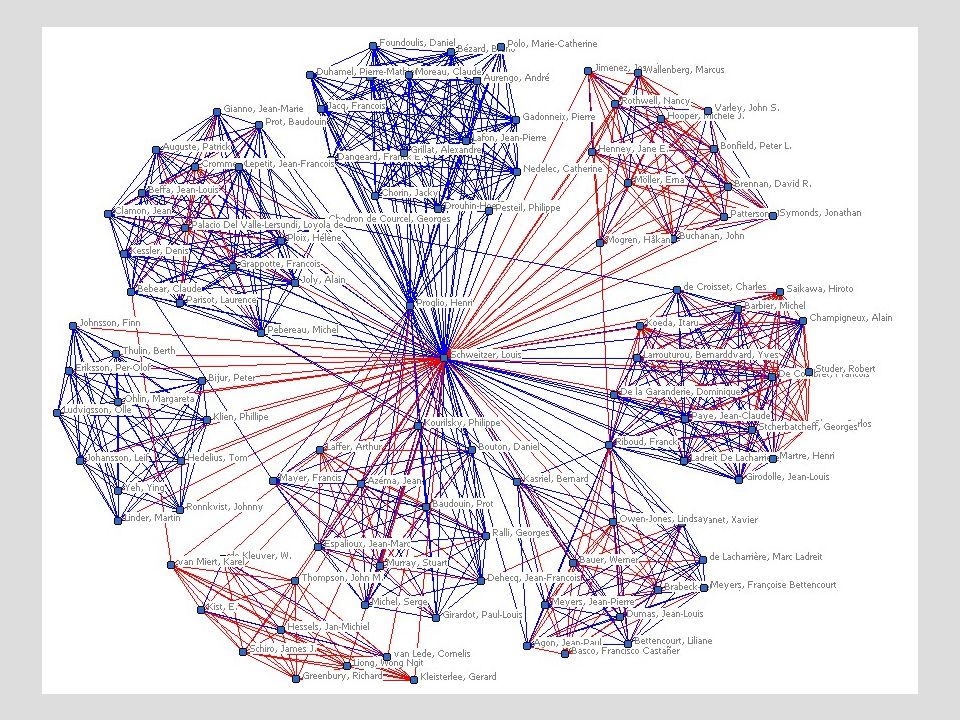

Interlocks and Networks Probably the most connected corporate director in the world is a Frenchman by the name of Louis Schweitzer. He serves on the boards of 8 different corporations from 4 different countries.

28

Two Kinds of Networks From corporation by director networks you can create corporation-corporation networks and director-director networks Both kinds of networks are of interest to researchers

29

FG500 corporate network 2006

30

FG500 directors 2006

31

Women in the FG500 Also consistent with previous studies, we find that women constitute a very small proportion of CEOs There are just 8 women CEOs out of 505 (some companies have dual CEOs).

.")

32

Women CEOs of FG500 2006 NameNationality Hayashi, FumikoJapanDaiei Lund, HelgeNorwayStatoil Sammons, Mary F.U.S.Rite Aid Woertz, Patricia A.U.S. Archer Daniels Midland Barnes, Brenda C.U.S.StaplesSara Lee Idrac, Anne-MarieFranceDexia GroupSNCF Mulcahy, Anne M.U.S.CitigroupTargetXerox Lauvergeon, AnneFranceSuezTotalVodafoneAREVA

33

Women in the FG500 On the other hand, women are just as likely to serve on multiple boards as are men (men 1.15 boards on average; women 1.18 boards on average) Just as likely to serve on a foreign board (men 11.4%, women 10.8%) And just as likely to link two boards from different countries (men 3.0%, women 3.3%)

Just as likely to serve on a foreign board (men 11.4%, women 10.8%) And just as likely to link two boards from different countries (men 3.0%, women 3.3%)")

34

Women in the FG500 The emergence of a transnational corporate network, or community, that transcends both company and country is a notable feature of globalization We are not aware of any studies, however, that explore the position of women within the transnational corporate director network A critical question is whether the women who have made it into the network have access to each other and to positions of power within it.

36

A Man’s World As the two previous graphs show, the women are largely superfluous to the network– most men are connected to other men in the network whether or not the women are present. In contrast, only some women are connected to each other without “going through” men. Their network is much more fragmented, and many women are cut off completely from the other women in the network. In short, in the world of the global corporate elite, women need men far more than men need women.

38

A Man’s World This is also evident in the “brokerage” scores for the men and the women Brokerage (number of pairs not directly connected). The idea of brokerage is that ego is the "go-between" for pairs of other actors. In an ego network, ego is connected to every other actor (by definition). If these others are not connected directly to one another, ego may be a "broker" if ego falls on a the paths between the others. One item of interest is simply how much potential for brokerage there is for each actor (how many times pairs of neighbors in ego's network are not directly connected). In our example, actor number 5, who is connected to almost everyone, is in a position to broker many connections. Brokerage scores Sex of IndividualMeanNStd. Deviation male 349.08 584618.118 Female 230.21 81201.204 In contrast, only some women are connected to each other without “going through” men. Their network is much more fragmented, and many women are cut off completely from the other women in the network.

. If these others are not connected directly to one another, ego may be a broker if ego falls on a the paths between the others. One item of interest is simply how much potential for brokerage there is for each actor (how many times pairs of neighbors in ego s network are not directly connected). In our example, actor number 5, who is connected to almost everyone, is in a position to broker many connections. Brokerage scores Sex of IndividualMeanNStd. Deviation male Female In contrast, only some women are connected to each other without going through men. Their network is much more fragmented, and many women are cut off completely from the other women in the network..")

39

Power in Networks Power is based on the possession or control of resources In networks, information is a resource, and so whoever has access to information has power relative to other actors in the network In networks, not all actors have equal access to other actors, creating inequality in resources and thus inequalities in power. Independent of the number of women in the network, are they positioned in a way that gives them less power than men?

40

Sisterhood Since women are In networks, information is a resource, and so whoever has access to information has power relative to other actors in the network In networks, not all actors have equal access to other actors, creating inequality in resources and thus inequalities in power. Independent of the number of women in the network, are they positioned in a way that gives them less power than men?

41

Brokerage in Networks B is acting as a “coordinator” between actor’s A and C, because all three actors belong to the same group.

42

Brokerage in Networks B is acting as a “consultant” between actor’s A and C, because B does not belong to the same group as A and C.

Similar presentations