Download presentation

Presentation is loading. Please wait.

1

Presentation to the IESBA

13 January 2015 Jeff Kaye & Peter van Veen Transparency International UK

2

Jeff Kaye, FCMA, CGMA – Trustee, Transparency International - UK

Peter van Veen – Director, Business Integrity Programme, Transparency International - UK

3

Transparency International

Founded in 1993 Chapters in over 100 countries Specialist anti-corruption NGO Transparency International’s Approach: Zero tolerance Corruption has victims Any bribery embeds corruption in the system Fighting corruption often requires collective action to achieve systemic change

4

Corruption and Bribery

What is corruption? “The abuse of entrusted power for private gain” What is bribery? “The offering, promising, giving, accepting or soliciting of an advantage as an inducement for an action which is illegal, unethical or a breach of trust.”

5

How Does Bribe Paying Happen?

Bribery Grand Corruption (Large bribes) Facilitation payments Gifts Hospitality Political donations Charitable donations Agents Enhanced commissions In-kind help & support Education & Training Projects Employing of Relatives Benefits & Perks to Relatives Offsets Firstly, a bribe doesn't have to be about money in a brown envelope. It is anything at all that might be of value to the person you are bribing. The thing of value can be disguised as a gift or hospitality, or it can be a payment to an intermediary - these are two red-flag areas for bribery, as you will see later in this module. 'Improper performance' is a breach of a person's proper role or function. It may involve actions, such as an award of a contract or a permit, or it may simply involve inaction, i.e. someone turning a blind eye to something they are supposed to do. In the UK and many other jurisdictions, the legislation now applies this definition in the widest possible sense. For instance, a UK company can be prosecuted for paying bribes anywhere in the world. Copyright Transparency International UK 2011 5

Facilitation. payments. Gifts. Hospitality. Political donations. Charitable donations. Agents. Enhanced. commissions. In-kind help & support. Education & Training Projects. Employing of Relatives. Benefits & Perks to Relatives. Offsets. Firstly, a bribe doesn t have to be about money in a brown envelope. It is anything at all that might be of value to the person you are bribing. The thing of value can be disguised as a gift or hospitality, or it can be a payment to an intermediary - these are two red-flag areas for bribery, as you will see later in this module. Improper performance is a breach of a person s proper role or function. It may involve actions, such as an award of a contract or a permit, or it may simply involve inaction, i.e. someone turning a blind eye to something they are supposed to do. In the UK and many other jurisdictions, the legislation now applies this definition in the widest possible sense. For instance, a UK company can be prosecuted for paying bribes anywhere in the world. Copyright Transparency International UK")

6

Corruption is a Global Problem

Corruption Perception Index (CPI) 2013

")

9

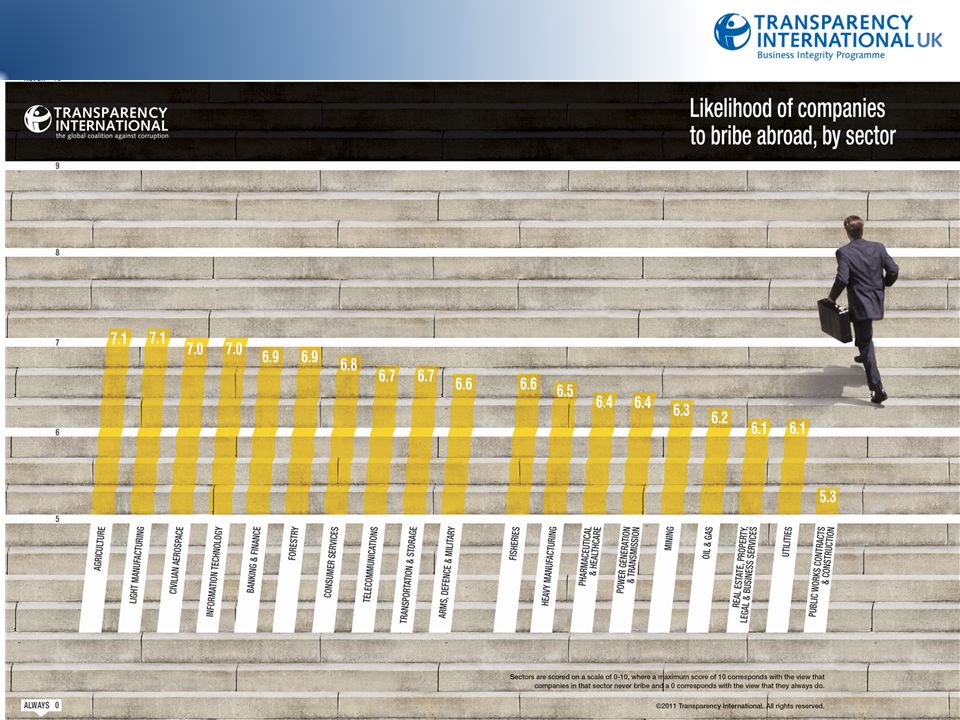

What do those in business think of each other?

Bribe Payers Index 2011

11

Corruption links to many other ethical issues…

12

The tightening net

13

Legislation and Regulation increasing

14

UNCAC Anti-corruption Laws

Signatories encouraged to criminalise: Passive bribery of all public officials Illicit enrichment Abuse of function Trading in influence Private sector bribery and embezzlement Money laundering and concealment of assets Whistleblower reporting and protection measures [OPTIONAL] See Reference document R1 for explanations of terminology. These are the practices encourage, but not required, to make criminal offences. Passive bribery (demand side/receiving the bribe) includes: denial of goods or services, access to utilities, access to licences, legal sanctions and lost opportunities. UNCAC also addressed whistleblower protection: Article 8: Codes of Conduct for public officials to facilitate the reporting by public officials of acts of corruption to appropriate authorities Article 13: Reporting channels - take appropriate measures to ensure that the relevant anti-corruption bodies are known to the public and provide access for the reporting, including anonymously, of any incidents. Article 33: Protection of reporting persons against any unjustified treatment for any person who reports in good faith.

includes: denial of goods or services, access to utilities, access to licences, legal sanctions and lost opportunities. UNCAC also addressed whistleblower protection: Article 8: Codes of Conduct for public officials to facilitate the reporting by public officials of acts of corruption to appropriate authorities. Article 13: Reporting channels - take appropriate measures to ensure that the relevant anti-corruption bodies are known to the public and provide access for the reporting, including anonymously, of any incidents. Article 33: Protection of reporting persons against any unjustified treatment for any person who reports in good faith.")

15

Common features of anti-bribery laws

They seek to punish bribe givers and takers Extra-territoriality Criminal offence Foreign public officials Penalties for individuals and organisations Corporate liability As new bribery laws get drafted and old ones are updated, a set of common themes is emerging. These are based on what the OECD considers a good anti-bribery law to be, the key principles in UNCAC and the FCPA. Punish bribe givers and takers – hence reference to both active and passive bribery in UNCAC. Extra-territoriality - If you were to get involved in bribery, you could be prosecuted in a jurisdiction other than your home country for bribes paid anywhere in the world, eg in the US. Criminal offence - international pressure has strongly increased to make bribery a criminal offence and to encourage prosecution of offenders. Previously a civil offence. Foreign public officials - most laws make a special reference to bribes paid to overseas public officials as transactions involving such public officials are regarded as high-risk. But bribery in the private sector is increasing and recent anti-bribery laws reflect this. Included in this category are: Civil servants, local government officials. government ministers, health officials, judges, MPs. Penalties for individuals and organisation - range from heavy fines to imprisonment and even the death sentence Corporate liability – companies are increasingly being held liable for bribes paid by their employees and agents – and the fines and associated costs are growing. Duress or extortion – if the payment is genuinely the result of a threat to the person’s security, it is unlikely to be deemed as bribery. PAUSE FOR DISCUSSION Pause here to check in and allow learners a break from the slides. Ask the group to share any thoughts on what we have shared so far before we take a look at the UK Bribery Act. For example, are there any surprises? How does this impact on their work, eg extra-territoriality rules, penalties for individuals. Allow 3-4 minutes discussion then move on to look at the UK Act.

16

Managing Risks

17

Adequate Procedures High-level commitment Risk assessment

Policies and Procedures Implementation (e.g. training, communication) Due diligence assessment of partners, agents and contractors Monitoring and evaluation We can respond in a positive way – by adopting zero-tolerance as a starting point. This leaves no room for doubt. Needs to be communicated effectively. In real life, it will still happen. But less likely if you commit to ZT. Introduce the 7 principles (refer to WB11): Commitment – tone needs to permeate all levels Risk assessment – do this regularly as the risks vary over time, where you operate, sectors etc Procedures – purposefully designed to suit the risks facing your organisation, as highlighted by the risk assessment Due diligence of 3rd parties - agents, procurement, local partners. Need contracts and certification. We don’t have control over their processes but have to make it clear what you expect – they must operate to the same standards. Communication - employees need to know what to expect so train what it means for ZT, the situations they will face and how to deal with them. Provide support and guidance. Monitoring – check that your policies are working, then learn and adapt if needed. Collective action – this is about working externally and we will address that this afternoon. Reference: the BOND/TIUK/mango Principles document. Next, CAROUSEL ACTIVITY, SEE FN4.

Due diligence assessment of partners, agents and contractors. Monitoring and evaluation. We can respond in a positive way – by adopting zero-tolerance as a starting point. This leaves no room for doubt. Needs to be communicated effectively. In real life, it will still happen. But less likely if you commit to ZT. Introduce the 7 principles (refer to WB11): Commitment – tone needs to permeate all levels. Risk assessment – do this regularly as the risks vary over time, where you operate, sectors etc. Procedures – purposefully designed to suit the risks facing your organisation, as highlighted by the risk assessment. Due diligence of 3rd parties - agents, procurement, local partners. Need contracts and certification. We don’t have control over their processes but have to make it clear what you expect – they must operate to the same standards. Communication - employees need to know what to expect so train what it means for ZT, the situations they will face and how to deal with them. Provide support and guidance. Monitoring – check that your policies are working, then learn and adapt if needed. Collective action – this is about working externally and we will address that this afternoon. Reference: the BOND/TIUK/mango Principles document. Next, CAROUSEL ACTIVITY, SEE FN4.")

18

Risks Legal Organisational Reputational Prosecution

Fines and imprisonment Large legal and compliance costs. Organisational Loss of focus – takes up management time Huge internal disruption Reputational Brand reputation damage Loss of Key Customers Loss of staff + decrease in morale

19

The Challenge of for accountants

20

Inducements: when does a gift become a liability?

Gifts and hospitality are common in many parts of the world in business Reciprocity is often (but not always) expected In some cultures, the size of the gift is directly correlated to the perceived importance of the business relationship Refusing gifts in many cultural contexts can be fatal for the business relationship Different cultures/ industries have different expectations and traditions in terms of size of gifts and hospitality Some companies ban the receipt and giving of gifts

expected. In some cultures, the size of the gift is directly correlated to the perceived importance of the business relationship. Refusing gifts in many cultural contexts can be fatal for the business relationship. Different cultures/ industries have different expectations and traditions in terms of size of gifts and hospitality. Some companies ban the receipt and giving of gifts.")

21

The Role of Accountants relating to Corruption

Uncover & Report Corruption/ Whistleblower Unwitting participant in corruption Hoodwinked Negligence Witting participant in corruption Willful Blindness Connivance Willing participant in corruption Collusion Instigator Illegal vs unethical…..

22

What can Accountants do?

Be familiar with the law Do not participate in Bribery Understand where the risk of bribery/ corruption is in their organisation/ industry/ country Understand the impact of a bribery incident to their organisation Know what to look for in relation to Bribery Ensure proper policies and procedures Create an environment where they are comfortable to ask questions and push back Be comfortable raising/ reporting concerns to senior management / compliance function or externally if need be

23

Ethics codes – codes within codes

Governance Industry A Industry B Industry C Industry D Location PAIBs Other “drivers”* * Education, training, business size, externalities, implementation, sanctions

24

Transparency International Resources

26

Extra slides

27

Some illustrative case studies

28

Case Study 1 You are in the process of issuing a tender for a new IT System. This is a significant project running into several hundred thousand Euros. Bill works for Datax who have done IT work for you over the last few years and you have got to know him very well often meeting for lunch and occasionally playing golf or tennis on the weekend. You consider him a good friend – certainly more a friend than than a supplier –as his last project finished over 9 months ago. You are due to meet Bill for lunch for a regular catch up and a chance to chat about your mutual interest: mountaineering. Bill has just called you that he understands that there may be a tender coming up and that this is excellent news. In fact his boss has told him it is OK to put the lunch on expenses and go somewhere a lot nicer than the café you were planning. Bill jokingly finishes off: “of course we can get the business end done quickly and focus on talking about the real business of our plan to climb K2 !” What do you do?

29

Case Study 2 After a well deserved Christmas break you come back to the office to find 5 boxes on you desk. When you open them up you find the following: A bottle of vintage champagne from a consultant to celebrate the completion of a major assignment A Swarovski crystal plaque from one of your clients with an inscription celebrating 10 years of working together A couple of good bottles of Bordeaux wine from a supplier A small gold looking statue of an Eagle as a thank you from a delegation from the Gulf that visited you the previous year on behalf of Brunel Energy A couple of tickets to a musical from a stagiaire thanking you for the opportunity to gain experience What do you do with these gifts? Do you accept them?

30

Case Study 3 Some months ago you asked a distributor for a neighbouring country that you oversee to show a key customer, travelling in that country, around over a weekend. After a long delay, he's finally submitted an invoice for the expense. It is for 6,000 dollars and the transaction is described as "recharge of Distributor's sales promotion expenses". No further details are given. He's calling to chase it up. How would you respond to him? Olaf: "Hi, did you get my invoice? Could you get it paid soon? We've been out of pocket for many months.” Could you give me a breakdown of your costs? Yes, I've got the invoice. I'll get accounts payable to process it asap. Certainly, I'll get it paid today. You did well. We've done some more business with that customer. I'll keep you in mind if something like this comes up again. This is a large cost just for showing a person around and may look like a bribe. So, at a minimum, you must ask for details of expenditure in case you are asked.

31

Tell the distributor to leave the invoice as is to mask the problem.

Olaf: "Sure. I can resubmit the invoice with a detailed breakdown and payment receipts. I know the cost is high, but I thought you wanted me to take good care of him. I took him out to the most expensive restaurant and bought some pearls for his partner." The distributor is recounting items that include rather lavish entertainment and gifts. What would you do now? Inform your senior management or legal department about the incident and get advice as to how to proceed. Tell the distributor to leave the invoice as is to mask the problem. Tell the distributor that he overstepped his mandate and must bear some of these costs himself. If you detect problems with costs (e.g. cash payments, lavish entertaining, unusual hotel bookings, large gifts), you should report them internally through the correct channels – such as your legal or compliance department. Remedies may include asking the customer for reimbursement and instructing, controlling and monitoring intermediaries more carefully in the future. This may include putting in place processes for pre-approval of certain expenses.

, you should report them internally through the correct channels – such as your legal or compliance department. Remedies may include asking the customer for reimbursement and instructing, controlling and monitoring intermediaries more carefully in the future. This may include putting in place processes for pre-approval of certain expenses.")

Similar presentations

European Commission Training.>")

defines bribery as the.>")

Bribery and Facilitation Payments Training Module – March 2014.>")