Download presentation

Presentation is loading. Please wait.

1

EFFECTIVE AND EFFICIENT MANAGEMENT OF THE EXTERNAL AUDIT PROCESS Government Finance Officers Association of Arizona August 2012

2

Effective and Efficient Management Understanding (and performing)

")

3

Objectives After this afternoon’s session we be better able to answer these questions – What is an audit? What are the client’s responsibilities? What are the auditor’s responsibilities? What are the outcomes? What are some of the significant new and proposed accounting and auditing changes?

4

Financial Statement Audits An INDEPENDENT person: Supports Corroborates Validates Provides Assurance Adds Credibility to what MANAGEMENT says about its own finances. What’s an Audit?

5

Financial Statement Audits Audits provide Reasonable Assurance. A clean audit report does NOT mean a ‘clean bill of health’. Financial statement audits do not endorse the entity’s: Policy decisions Use of resources Internal controls What’s an Audit?

6

Financial Statement Audit Rule Makers AICPA American Institute of Certified Public Accountants Clients Governments Not-for-Profits Non-Issuers GAO Government Accountability Office Clients Governments PCAOB Public Company Accounting Oversight Board Clients Large Companies with Publically Traded Stock (Issuers) Also makes the rules for federal compliance audits (A-133 Single Audits) What’s an Audit?

Also makes the rules for federal compliance audits (A-133 Single Audits) What’s an Audit")

7

Financial Audit Process Perform tests of controls Perform substantive tests Evaluate audit findings Conclude Design further audit procedures for assertion level risks Develop overall response for financial statement level risks Assess the risk of material misstatement Perform risk assessment and other procedures Gain an understanding of the entity Start What’s an Audit?

8

Financial Audit Process Gather Information Assess Risk of Material Misstatement Perform Control and Validation Procedures Evaluate Findings and Reassess Risk What’s an Audit?

9

Financial Audit Procedures What do you do? How do you do it? Corroboration increases the value of the information. Inquiry An auditor watches you perform something. Only valid for the watched performance. Observation Evidence can be found on physical/electronic documents. 3 rd party documents are more valuable than internal docs. Inspection of Documents Auditor develops an expectation. Reported information is compared to the expectation. Analytical Procedures Here’s where we get our fingers dirty scrutinizing stuff. May involve sampling. Tests of Details What’s an Audit?

10

Audit Responsibilities CLIENT Responsible for the financial statements Develop sound accounting policies and establish and maintain internal controls AUDITOR Responsible for reporting on the accuracy and reliability of the financial statements Perform tests and report results of procedures What’s an Audit?

11

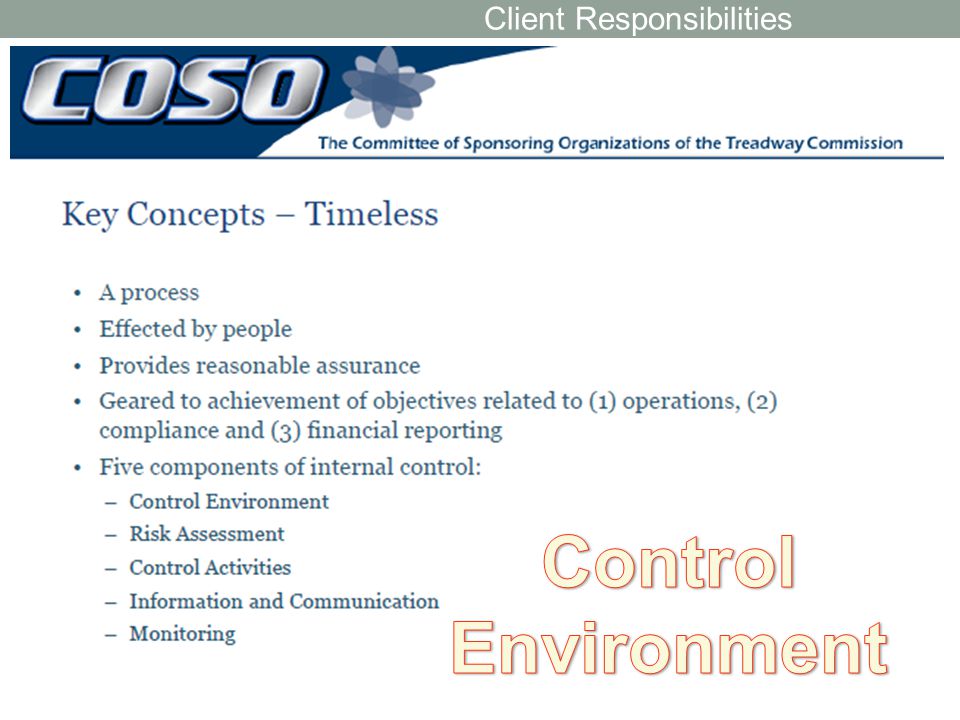

CLIENT RESPONSIBILITIES

12

Two Types of Internal Controls Detective Let’s find the problem before it grows Cash counts and bank reconciliations Reviewing payroll reports Monitoring expenditures against budgeted amounts Preventive Let’s stop an unwanted outcome Understanding policy Review and approval of purchase orders Passwords Client Responsibilities

20

The Role of the Governing Body Set a proper “tone at the top” Ensure open communication and proper allocation of resources Stress that the audit is important and that staff will be held accountable An audit committee will help the governing body fulfill its responsibility Client Responsibilities

21

Governing Body Review of Findings The governing body should review audit findings, hold management responsible, and assist management with ways to correct deficiencies and prevent them from occurring again. It should also consider meeting with the auditors to discuss the findings. Client Responsibilities

22

Consider Forming an Audit Committee The creation of an audit committee is a method for the governing body to fulfill its oversight responsibility. There is an increasing emphasis on the importance of audit committees. Guidance is available for the development of audit committees. Client Responsibilities

23

Audit Committees - Responsibilities Evaluate the request for proposal for annual financial audit Recommend the selection of the financial auditor Attend the entrance and exit conferences for annual and special audits Be accessible to the external financial auditors as requested to facilitate communication with the board Review and address audit findings Client Responsibilities

24

Management and Other’s Roles Providing written policies and procedures Telling us about your procedures Demonstrating how controls function Providing supporting documents Answering questions about financial activity Client Responsibilities

25

AUDITOR RESPONSIBILITIES

26

Auditor Responsibilities Financial report reliabilityEffective internal control Compliance with laws and regulations What Auditors Do

27

Inquiries of management, staff, and governing body members Review a sample of transactions Provide reasonable assurance that the financial statements are materially accurate. Report deficiencies noted during the audit What Auditors Do

28

Routine Audit Services Routine audit services pertain directly to the audit and include: Providing advice related to an accounting matter Researching and responding to an audited entity’s technical questions Providing advice on routine business matters Educating the audited entity on technical matters Other services not directly related to the audit are considered nonaudit services What Auditors Do

29

Nonaudit Services Services that are considered nonaudit services include: Financial statement preparation Bookkeeping services Cash to accrual conversions (a form of bookkeeping) Other services not directly related to the audit Unless specifically prohibited, nonaudit services MAY be permissible but should be documented In relation to the conceptual framework In relation to the auditor’s assessment of management’s skill, knowledge or experience What Auditors Do

Other services not directly related to the audit Unless specifically prohibited, nonaudit services MAY be permissible but should be documented In relation to the conceptual framework In relation to the auditor’s assessment of management’s skill, knowledge or experience What Auditors Do")

30

2011 Yellow Book Conceptual Framework for Independence

31

Categories of Independence Threats Management Participation Threat Self Review Threat Bias Threat Familiarity Threat Undue influence Threat Self Interest Threat Structural Threat What Auditors Do

32

What Auditors Don’t Do Verify every financial statement figure Provide an opinion on the internal controls of an Organization Examine every single transaction of the Organization. Judge the appropriateness of management decisions/strategies Replace or fulfill the responsibilities of management/TCG What Auditors DON’T Do

33

Yellow Book Prohibitions Set policies or evaluate recommendations Internal Audit Design, develop, modify, operate or supervise a system subject to audit IT Design, implement, or monitor system of internal control Internal Control If material or significantly subjective Valuation Services What Auditors DON’T Do

34

AUDIT OUTCOMES

35

Audit Outcomes Financial statement opinion Report on Compliance and Internal Control Other compliance and internal control communication Other communication Audit Outcomes

36

Management Evaluation of Audit Findings There should not be an expectation of no audit findings Cost/benefit considerations of internal controls must be considered The Good… Help management address issues May identify problem areas Indication of value received for audit services The Bad… Critical, technical language used in audit findings Expectation of no audit findings Evaluation of the effort of management and staff Audit Outcomes

37

FEDERAL COMPLIANCE AUDITS A-133 Single Audits

38

The Single Audit Act Gives the Director of the Office of Management and Budget (U.S. Presidential Office) authority to establish audit guidelines and policy for a uniform system of auditing states, local governments and non-profits that spend federal awards. OMB Circular A-133 Audits of States, Local Governments, and Non-Profit Organizations A-133 Compliance Supplement Single Audits

authority to establish audit guidelines and policy for a uniform system of auditing states, local governments and non-profits that spend federal awards. OMB Circular A-133 Audits of States, Local Governments, and Non-Profit Organizations A-133 Compliance Supplement Single Audits.")

39

The Single Audit Act Expend Any Federal Awards Identify all federal awards received and expended, by program, in the accounting records Know the grantor, pass- through grantor and the Catalog of Federal Domestic Assistance Numbers for all federal programs Maintain internal control over federal programs that ensures compliance with federal requirements Comply with laws, regulations, and the provisions of grants and contracts related to federal programs Single Audit Changes

40

A-133 Single Audit Expend > $500k in Fed Awards = Single Audit Financial Statement Audit in Accordance with Government Auditing Standards Prepare a Schedule of Expenditures of Federal Awards (SEFA) Larger and Riskier Federal Programs Audited and Internal Control Evaluated Single Audit Changes

Larger and Riskier Federal Programs Audited and Internal Control Evaluated Single Audit Changes")

41

A-133 Single Audit Outputs Schedule of Expenditures of Federal Awards “in relation to” opinion on SEFA Opinion on compliance Report on Internal Control over Compliance Schedule of Findings and Questioned Costs Summary Schedule of Prior Audit Findings Data Collection Form Single Audits

42

EVALUATING THE PERFORMANCE AND EFFECTIVENESS OF THE EXTERNAL AUDITORS

43

Factors to Consider Was the auditor responsive to inquiries of management and the governing body throughout the audit process? Did the auditor inform the governing body (or audit committee) of any risks of which it was previously not aware? Did the auditor adequately discuss issues of the quality of financial reporting, including applicable new and significant auditing principles? Evaluating Auditors

of any risks of which it was previously not aware. Did the auditor adequately discuss issues of the quality of financial reporting, including applicable new and significant auditing principles. Evaluating Auditors.")

44

Factors to Consider Did the auditor communicate issues freely with the governing body or audit committee? Does it appear that the independent auditors are reluctant or hesitant to raise issues that would negatively affect management? Is the governing body or audit committee satisfied with the planning and conduct of the audit, including the financial statements and internal control over financial reporting? Evaluating Auditors

45

Factors to Consider Is the audit committee satisfied with its relationship with the auditor? Was the engagement partner involved at all? Was the auditor frank? Were services delivered in a timely manner? Was the audit fee fair and reasonable based on the services provided and in relation to fees of other auditors? Did the independent auditor provide constructive observations, implications, and recommendations in areas needing improvement, particularly with respect to the organization’s internal control system over financial reporting? Evaluating Auditors

46

Factors to Consider What were the results of the audit organization’s peer review? Does the audit organization have a quality control system for monitoring compliance with independence requirements? Does the audit organization have a quality control system for monitoring compliance with continuing professional education requirements? Evaluating Auditors

47

ACCOUNTING UPDATE

48

The Accounting Lineup Effective for f/y ended June 30, 2013 Service Concession Arrangements (GASB 60) Financial Reporting Entity Omnibus (GASB 61) Codification of Pre-1989 FASB and AICPA Pronouncements (GASB 62) Financial Reporting of Deferred Outflows of Resources, Deferred Inflows of Resources, and Net Position (GASB 63) Accounting Update

Financial Reporting Entity Omnibus (GASB 61) Codification of Pre-1989 FASB and AICPA Pronouncements (GASB 62) Financial Reporting of Deferred Outflows of Resources, Deferred Inflows of Resources, and Net Position (GASB 63) Accounting Update")

49

The Accounting Lineup Effective for f/y ended June 30, 2014 Statement 65—Items Previously Reported as Assets and Liabilities Statement 66—Technical Corrections— 2012, an amendment of GASB Statements No. 10 and No. 62 Statement 67— Financial Reporting for Pension Plans Accounting Update

50

The Accounting Lineup Effective for f/y ended June 30, 2015 Statement 68— Accounting for Pensions by State and Local Governmental Employers Accounting Update

51

Proposed Standards for Public Comment Recognition of Elements of Financial Statements and Measurement Approaches (PV Comment Deadline: Sept 30, 2011) Economic Condition Reporting: Financial Projections (PV Comment Deadline: March 16, 2012 ) Government Combinations and Disposals of Government Operations (ED Comment Deadline: June 15, 2012) Accounting and Financial Reporting for Nonexchange Financial Guarantee Transactions (ED Comment Deadline: September 28, 2012) Accounting Update

Economic Condition Reporting: Financial Projections (PV Comment Deadline: March 16, 2012 ) Government Combinations and Disposals of Government Operations (ED Comment Deadline: June 15, 2012) Accounting and Financial Reporting for Nonexchange Financial Guarantee Transactions (ED Comment Deadline: September 28, 2012) Accounting Update")

52

REPORTING PENSION LIABILITIES

53

Pension Accounting and Reporting Basics Defined benefit pensions originate from exchanges between the employer and employees of salaries and benefits for employee services and are part of the total compensation for employee services Obligations for pensions meet the definition of a liability in Concepts Statement No. 4 Compensation expense should be recognized in the period employee services are provided Pension – Employer Reporting

54

Pension Accounting and Reporting Basic 3 Step Measurement Approa ch 25 40 6280 1) Project Benefit Payments now This period 2) Discount Future Payments 3) Allocate to Service Periods 42% (16/38) of the PV of the Future Payments should have been expensed at this point. Pension – Employer Reporting

55

Pension Accounting and Reporting Pension – Employer Reporting

56

Pension Accounting and Reporting Cost-Sharing Employers Sole-employer plans Multiple- employer agent plans Multiple- employer cost-sharing plans Pension – Employer Reporting

57

AUDITING UPDATE

58

Clarity Background Discussion paper issued March 2007 ASB considered comments received and approved direction forward August 2007 Goals Address concerns over length and complexity of standards Make standards easier to read, understand and implement Lead to enhancements in audit quality Clarity - Background

59

Clarity Project 58 AU sections 3 withdrawn 37 redrafted to corresponding SAS 7 combined into 1 new SAS 11 combined/split into 9 SASs Replaced by 47 new SASs AU section numbers will be changed to converge with ISA numbering Effective for audits of periods ending on or after 12/15/2012 Clarity - Background

60

Clarity Drafting Conventions Introduction Objectives Definitions Requirements Application Material Appendices and Exhibits Clarity – Overall Objectives

61

OPENING BALANCE-INITIAL AUDIT ENGAGEMENTS AU-C510

62

Opening Balances—Initial Audit Engagements Obtain sufficient appropriate evidence about whether beginning balances contain material misstatements Reviewing predecessor auditor helps determine auditor scope, but is not sole basis for sufficient appropriate evidence AU-C 510 62 1.Whether prior period closing balances brought forward correctly 2. Whether opening balances reflect appropriate application of accounting principles 3. Evaluating evidence about opening balances from current period audit procedures and one or both: a.Review predecessor auditor’s work b.Perform specific procedures about opening balances

63

GROUP AUDITS AU-C600

64

Group Audits Component GASB 14, 39, 61 Component Unit Group Audits

65

a group has - at least two components management financial statements group-wide controls consolidation process group audit group auditor group audit team group materiality Component A Component B Component C Component D components have- management financial information component evidence component auditor component materiality components of their own component –an activity or entity for which financial information is prepared that is needed for the group financial statements

66

Group Audits Component A Component B Component C Component D group team responsibilities overall audit strategy and plan understand group – UEE and RMM and group-wide controls and consolidation process understand components understand component auditor refer or make reference? group materiality component materiality response to RMM consolidation process subsequent events communication – CA, MGMT, TCG

67

QUESTIONS? Thanks for your participation!!!

68

About the Auditor General’s Office The Office of the Auditor General serves as an independent source of impartial information and provides specific recommendations to improve the operations of the state and local governments. To fulfill its statutory duties, the Office must – ascertain whether public entities are making wise use of their resources determine compliance with applicable laws, regulations, and governmental accounting standards define standards and establish procedures for accounting and budgeting; and provide technical assistance

69

About the Auditor General’s Office The Joint Legislative Audit Committee, which oversees all audit functions of the Arizona Legislature, provides direction for the Auditor General’s Office. Subject to approval by a majority vote of both legislative houses, the Committee also appoints the Auditor General for a 5-year renewable term.

70

About the Auditor General’s Office The Auditor General is assisted in fulfilling office responsibilities by a Deputy and nearly 200 employees organized into four operating divisions: Financial Audit, Performance Audit, Accounting Services, and School Audits. These divisions are supported by a general counsel and administrative, information technology services, and quality control groups.

71

About the Auditor General’s Office The Office has audit responsibility for state agencies, counties, universities, community college districts, and school districts. The Office also completes highly specific research and investigative projects in response to legislative requests.

Similar presentations