Download presentation

Presentation is loading. Please wait.

1

Brief Note November 24, 2014

3

Regarding the merger process, all the information and financial data therein is to be approved by the governmental agencies such as CMB, EMRA and Borsa Istanbul. Without their consent the merger process shall not be completed.

5

On September 1st, 2014, Park Elektrik announced a plan by the BOD to merge with Silopi Elektrik, the sister company which is engaged in electricity production in Silopi, in its 135 MW thermal power plant. 95% of Silopi Elektrik’s investments to triple its capacity to 405 MW has been completed already. The merger has rationale of product diversification, managerial and financial scales of economies and the Group’s perspective to have a bigger entity in the capital markets.

6

Increasing Market Cap Product Diversification Managerial and Financial Scale of Economics

7

Scale of Economics Product Diversification Creating Value Neighbouring locations shall help to optimize scale of economics. To be a player in the developing energy sector as well as commodity markets. The value created by the merger shall be projected in the market value of the company.

8

1 Sep 2014 12 Sep 2014 15 Sep 2014 16 Sep 2014 1 Oct 2014 13 Oct 2014 12 Nov 2014 21 Nov 2014 Board of directors decisions declared of both companies. They included exit price of TL 4.20. Expert report was declared. Merger ratio was determine d as 0,186914. Merger agreement and merger report of the Board of Directors was signed. CMB and EMRA applica- tions accomp- lished. Silopi Elektrik applied to the BIST to be listed. Board decision was announced by Silopi Elektrik on dividend distribution policy and it included in the merger agreement. Borsa Istanbul approved listing of Silopi Elektrik shares subsequent to forthco- ming merger. Capital Market Board approved merger of Park and Silopi with an exit right of TL4.20.

9

Approval from Energy Market Regulatory Agency. Approvals of the merger in the general meetings of the both companies. Exit rights will be executed maximum six days after the general meeting. It will be lasted min. 10 and max 20 days. Stockholders who did not prefer to use exit right will change their shares with new company’s shares. Central Registry Agency registration will take place. Commencing transactions in Borsa Istanbul.

10

It is planned to have general meetings of both companies through the end of the 2014 to finalize the merger process.

11

Silopi Elektrik (Transferee) Park Elektrik (Transferor) Total Value SH’s Equity DCFComparable Transaction Value Base Value SH’s EquityDCFMarket Value Base Value 73,2053,518,8852,451,7462,402,893469,1021,402,196674,487924,494 3,327,387 20%40% %10020%40% %100 * Expert institution is Eren Bağımsız Denetim YMM A.Ş., a member of Grant Thornton International Limited.

Park Elektrik (Transferor) Total Value SH’s Equity DCFComparable Transaction Value Base Value SH’s EquityDCFMarket Value Base Value 73,2053,518,8852,451,7462,402,893469,1021,402,196674,487924,494 3,327,387 20%40% %10020%40% %100 * Expert institution is Eren Bağımsız Denetim YMM A.Ş., a member of Grant Thornton International Limited.")

12

Silopi Elektrik Paid Capital: 80.000.000 TL Park Elektrik Paid Capital: 148.867.243 TL Merger Ratio=2,402,893 3,327,387 =%72.22 Post Merger Capital=80,000 0.7222 =110,779 Amount of Capital Increase =110,779 -80,000=30,779 Exchange Ratio=30,779 148,867,243 =0.206757

14

It is located in Şırnak/Silopi, southeast of Turkey. Electricity production license, dated 23.03.2004 was issued by EMRA. The license duration is 20 years. Electricity production started in 2009 with one unit. Established capacity is 135 MW currently. It will triple its capacity in the beginning of 2015 by adding two more units that each has 135MW capacity. Total capacity of the company will be 405MW starting from 2015.

15

95% of the investment of two new units has been completed already. Total investment value of the three units is estimated as US$500mn in today’s prices. After completion of the two generation units at the end of 2014, the company’s established capacity will reach 405 MW. With this capacity the Company aims to produce 1% of total electricity production of the country. Currently the company sells %50 of the production to the group companies. Remaining is to be sold in the free market.

16

Consumes asphaltite, a kind of hydrocarbon as fuel. The technology is called fluidised bed. Owns the operational rights in the asphaltite mine until 2033. Calorific value of the asphaltite is between 5.500-5.800 kcal/kg. Silopi Electrik benefits guaranteed supply and low cost for the fuel. The electricity is sold via bilateral agreements or PMUM.

17

Gross Production 2011 201220132014/06 Capacity (annual) (KWh) 1,182,600,000 586,305,000 Production (annual) (KWh) 816,911,424849,468,384 731,715,744516,539,520 CUR (annual) 70%71.8%61.87%88.10%

(KWh) 1,182,600, ,305,000 Production (annual) (KWh) 816,911,424849,468, ,715,744516,539,520 CUR (annual) 70%71.8%61.87%88.10%")

18

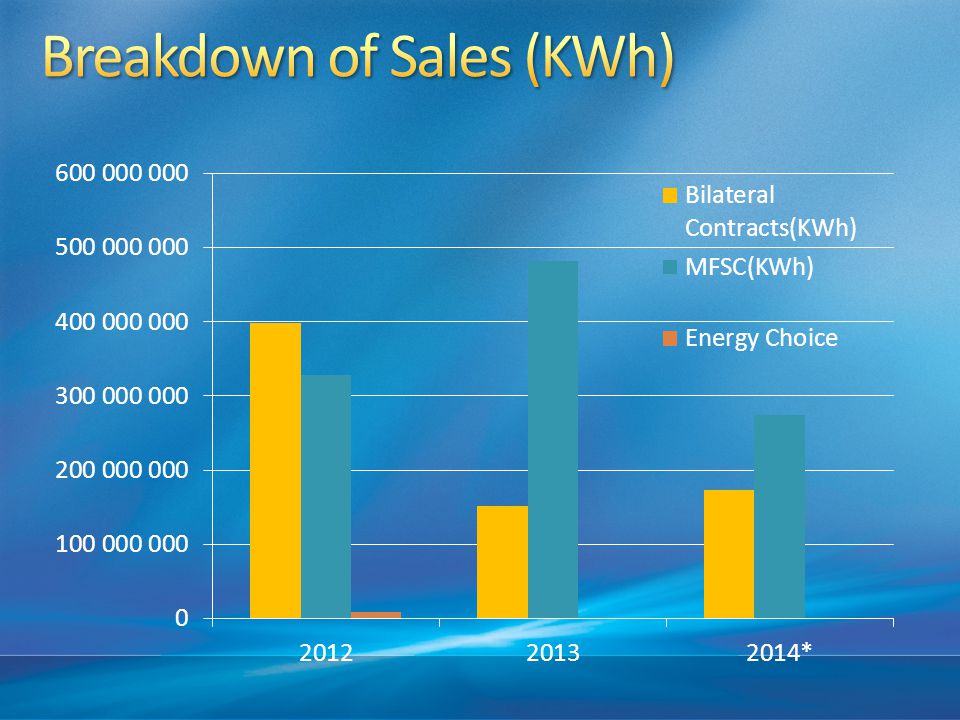

Sales201220132013/062014/06 Sales Amount (mn, kw/h) 735634333*470 Sales Revenues (mn TL) 1129651*73 * In 2013, maintenance works caused the production to be realized at low levels which was deteriorated the revenues. With the completion of the new plants, we do not expect to suffer from substantial production losses.

22

TL2011201220131H131H014 Sales97.377.269111.789.78596.386.86650.668.61573.136.601 COGS-73.490.313-94.119.783-88.171.97047.225.84856.804.865 Gross Profit23.886.95617.670.0028.214.8963.442.76716.331.736 Margin25%16%9%7%22% GM Expenses-2.838.152-3.039.365-2.066.6801.025.9071.218.537 Other Income233.732406.053164.67293.8294.772.706 Other Expenses-444.830-243.600-44.99168.4001.337.730 Operating Income20.837.70614.793.0906.267.8972.442.28918.548.175 Margin21%13%7%5%25% Income From Invesment05.518-31.7486.5290 Financial Income013.010.61009.595.653 Financial Expenses-47.859.425-6.445.417-66.157.32025.476.3520 Income Before Tax-27.021.71921.363.801-59.921.171-23.027.53428.143.828 Tax Income/(Loss)5.125.557-4.569.39311.813.745-4.555.2555.414.209 Net Income/Loss-21.896.16216.794.408-48.107.426-18.472.27922.729.619 Margin-15%--31%

Net Income/Loss Margin-15%--31%")

23

TL2011201220131H131H14 Sales97.377.269111.789.78596.386.86650.668.61573.136.601 Gross Profit23.886.95617.670.0028.214.8963.442.76716.331.736 Gross Margin25%16%9%7%22% EBITDA32.523.52826.574.41318.168.2188.353.45130.580.387 EBITDA Margin33%24%19%16%42% Net Earnings-21.896.16216.794.408-48.107.426-18.472.27922.729.619 Net Margin-15%--31%

Similar presentations

1 This chapter describes the importance of managing your business finances.>")

Geometry (29%)>")