Download presentation

Presentation is loading. Please wait.

1

David McKenzie, World Bank (with Gustavo Henrique de Andrade and Miriam Bruhn ) CIC impact BBL, April 2, 2013

CIC impact BBL, April 2, 2013")

2

De Soto/Doing Business -> a decade+ of governments trying to extend helping hand to make it easier for firms to formalize ◦ 75% of countries adopted at least one reform to make it easier to start a business ◦ Reforms make it cheaper and less steps But: majority of firms in many developing countries still informal, and much of response to these reforms comes from entry of new firms, not existing firms formalizing. Much less effort given to issue of raising cost of staying informal ◦ Using long arm of the law to increase enforcement of existing regulations ◦ Not clear whether this causes firms to register, or shut down,

3

Period of simplification of firm registration SIMPLES introduced in 1996, consolidates multiple tax payments and contributions into single payment, lowers tax burden on small firms Minas Facil program in state started in 2005 to reduce number of procedures and time to start a business Yet despite these efforts survey data from 2009 reveal that 72% of firms still informal.

4

Field experiment with State Government of Minas Gerais to test four different actions to formalize firms: Carrots ◦ Information about how to register and dedicated hotline ◦ Removal of registration fees + year of free accounting services Sticks ◦ Municipal inspector randomly assigned to visit a firm ◦ Municipal inspector randomly assigned to visit a neighboring firm.

5

Descomplicar, a unit within the state government of Minas Gerais which has the mandate to simplify relations between citizens, firms and the state, wanted to test various mechanisms that could be used to induce more firms to formalize under the existing system in place. Focus: target firms that fell under the eligibility criteria for SIMPLES, which at the time of design was for either revenues in the range R$36,000 to R$240,000, or having two or more workers if revenues were below this

7

Communication: -18 page brochure - info on advantages of formalizing -On disadvantages of being informal -Opportunities in business procurement with state govt. -Opportunities for lines of credit through state development bank -10 steps needed to register + hotline number

8

Free Cost Treatment ◦ Brochure + waiving the JUCEMG registration fee and municipal license fees, as well as paying the first year’s sanitary tax and municipal inspection fee that are due within 30 days of registering. The fees waived thus amounted to between R$366 and R$504 (US$183-250) depending on the type of firm ◦ arrangement was made with the local accountant’s association, whereby 50 accountants would be available to provide one year of free accounting services to these firms, which has an effective value of R$3,600 given the prevailing cost of accounting services ◦ Only cost to firms who formalize in first year would then be SIMPLES taxes

depending on the type of firm ◦ arrangement was made with the local accountant’s association, whereby 50 accountants would be available to provide one year of free accounting services to these firms, which has an effective value of R$3,600 given the prevailing cost of accounting services ◦ Only cost to firms who formalize in first year would then be SIMPLES taxes.")

9

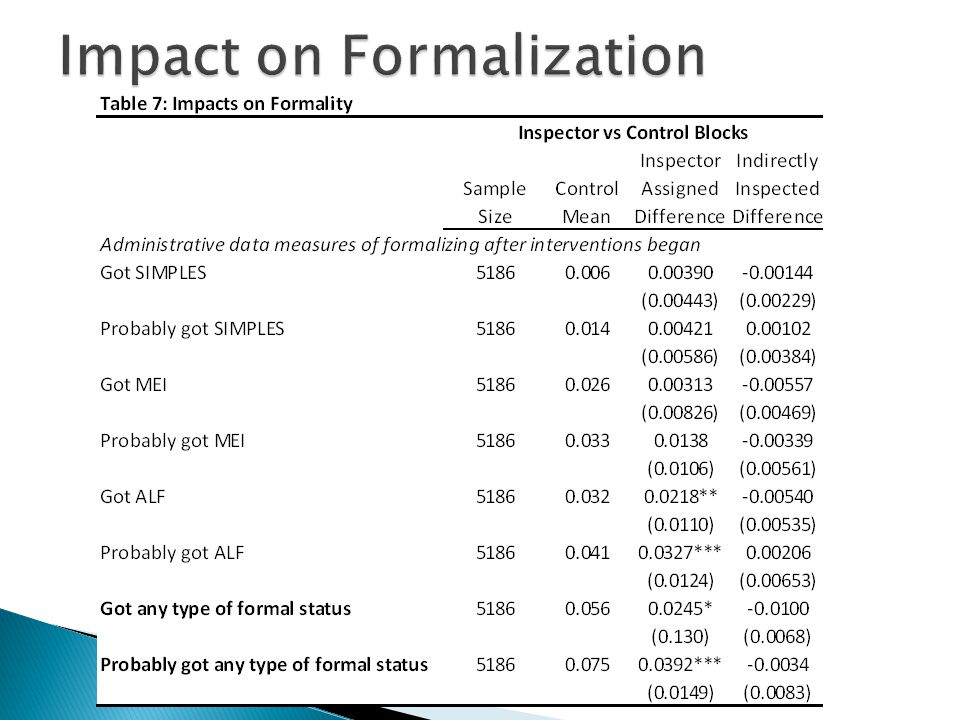

Inspector Treatment: ◦ Prefeitura Belo Horizonte (PBH) is the authority in charge of municipal inspections within the city of Belo Horizonte ◦ gave inspectors a list of selected firms to receive an inspection ◦ Inspectors then follow their usual procedure with these firms: visit them and request proof that they have a current municipal license (ALF), which expires every five years Firms lacking ALF given notification and given 30-45 days to formalize Then if not formalized, inspector comes back, fines firm, and closes firm If firm proves they are in the process of formalizing, get more time. Inspectors can’t fine firms for not being registered with State or Federal – but if firm applies for municipal license should technically register with these too.

10

Indirect Inspector Treatment ◦ Firm itself is not assigned to be inspected, but a nearby firm is => aim is to measure spillover impacts of inspections on formalization decisions of neighboring firms

12

Visit each firm operating out of a fixed building in the census block Enumerators recorded basic information about the firm that could be observed without talking to the firm owner – the full street address, the business sector, the “fantasy name” of the firm (the name on a sign outside the firm if they had one), whether or not the business had a sign, the approximate area in square meters of the premises, and the approximate number of employees in the business 10,000 + firms listed ◦ Then match to databases of firms registered with municipal and state governments – drop firms which appear on both lists

, whether or not the business had a sign, the approximate area in square meters of the premises, and the approximate number of employees in the business 10,000 + firms listed ◦ Then match to databases of firms registered with municipal and state governments – drop firms which appear on both lists")

15

Free Cost ◦ offer was delivered to 255 out of the 328 firms assigned to this treatment (78%). ◦ Take-up of the offer was incredibly low: one month after the offer our partner government agency and hotline had received just 5 calls and 2 visits; and three months after the offer, only 10 to 15 people had called and one had started the formalization process. ◦ Ultimately only one firm in this treatment group took-up the offer to formalize and use one of the free accountants.

19

Findings suggest sticks rather than carrots have more impact on getting firms to formalize – or at least that simplifying and informing firms is not enough of a carrot Process of registering in Belo Horizonte still requires more steps and complications than in a number of other countries that have pursued entry reforms. Moreover, in addition to facing taxes, firms which do register face a relatively large cost in terms of the need to hire an accountant. Faced with these costs of being formal, it appears few informal firms want to formalize unless they are forced to do so by enforcement.

20

1. Reconsider which types of firms worth bringing into the formal sector – tiniest firms likely not worth it, but firms in our sample seem to be in terms of fiscal revenues at least. 2. Make it easier to formalize, remove accountant requirement 3. Improve enforcement ◦ Challenge for researchers to think about how to evaluate more enforcement.

Similar presentations

Why procuring PPPs? Can you get what you want? Minimum.>")