Download presentation

Presentation is loading. Please wait.

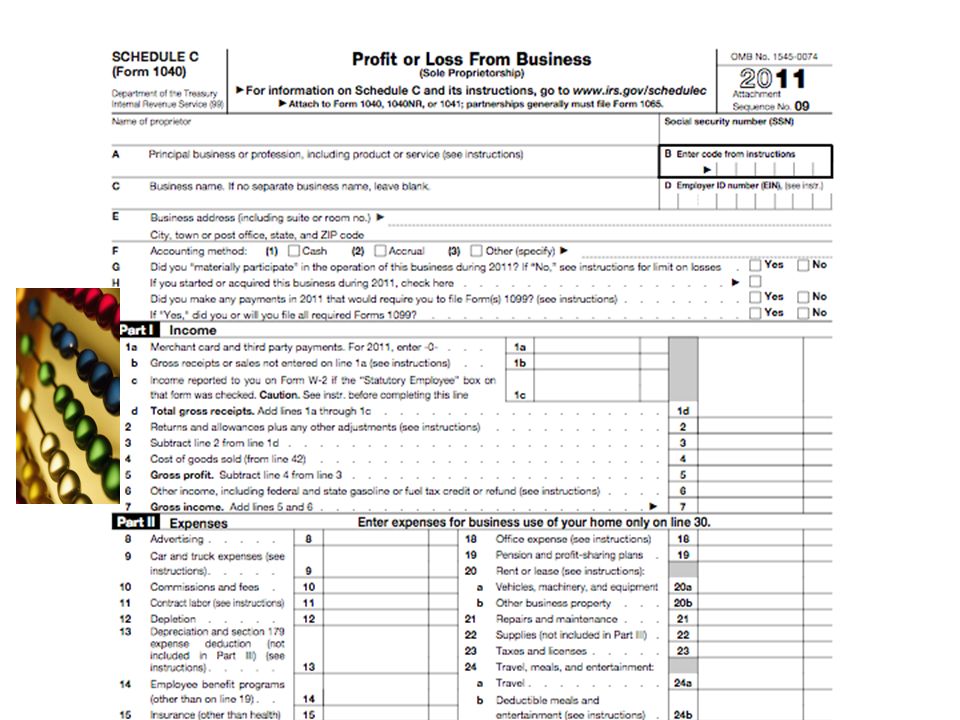

1

2011 Schedule C-1 Big change is in the header lines I and J –Self employed may have to issue a 1099 to any sub-contr. whom they pay $600 or more during the year. This is the case only where the Sch C represents a major part of their income. –If they answer yes to line I, then THE RETURN IS OUT OF SCOPE FOR TCE –Similarly for Sch C-EZ question F

2

Schedule C-2 Next change is in Part I lines 1a-1d –Note that for line 1a, instruction is to enter 0 for 2011. IRS is delaying using this entry for 1 yr. –Thus, ignore Merchant card and 3rd party payments which are reported on the new form 1099-K

3

Schedule C-3 Report all income from 1099s, cash, check and merchant cards or 3rd party on line 1b If a W-2 is received and statutory employee box is checked, report that income on line 1c If both Statutory employee income and normal self employment income are received, then 2 Schedule Cs are required

5

Calculate the SE tax which is 13.3% for income of $106,800 or less. Previous percentage was 15.3% If over $106,800 then only Medicare 2.9% factor multiplies line 4, then add $11,107.20 per instructions. [(4.2 + 10.4)% * 106,800] Self employment deduction for Form 1040 line 27 is calculated on line 6. This factor previously was 0.5. For 2011 it is 0.5751 or the ratio of 7.65/13.30 which is the [employers rate/(employers rate +employees rate)] Schedule SE lines 5 and 6

% * 106,800] Self employment deduction for Form 1040 line 27 is calculated on line 6. This factor previously was 0.5. For 2011 it is or the ratio of 7.65/13.30 which is the [employers rate/(employers rate +employees rate)] Schedule SE lines 5 and 6.")

Similar presentations

Publication 969 (Health Savings Accounts and Other Tax-Favored Health.>")

>")