Download presentation

Presentation is loading. Please wait.

1

Core Acceleration HP Competitive Update DO NOT DISPLAY

2

Agenda Michael Rau Ross Fowler Dean Eyers 07.07.2011

3

Dean Eyers Lessons Learned Taking the Fight to HP FlexNetwork Organizational Changes

4

HP Announced Significant Management Changes on June 13 th, 2011 Positioning: Allow HP to better capitalize on strategic market opportunities Executive Moves: Ann Livermore (EVP Head of Enterprise Business) Leaving day to day HP Enterprise Management Position, Elected to Board Dave Donatelli Will report directly to HP CEO Leo Apothekar Peter Bocian (Chief Admin Officer) and Randy Mott (Chief Information Officer) Both depart HP, roles consolidated into Chief Information Officer role – TBH Follows Early June announcement: Marius Haas (Head of Enterprise Networking) and Michael Mendenhall (CMO) both departing HP

Leaving day to day HP Enterprise Management Position, Elected to Board Dave Donatelli Will report directly to HP CEO Leo Apothekar Peter Bocian (Chief Admin Officer) and Randy Mott (Chief Information Officer) Both depart HP, roles consolidated into Chief Information Officer role – TBH Follows Early June announcement: Marius Haas (Head of Enterprise Networking) and Michael Mendenhall (CMO) both departing HP")

5

HP suing Oracle over the hire of former CEO, Mark Hurd HP suing Oracle over decision to cease supporting Intel's Itanium architecture HP knows Intel plans to end-of-life the Itanium microprocessor. “Knowing this, HP issued numerous public statements in an attempt to mislead and deceive their customers and shareholders into believing that these plans to end-of-life Itanium do not exist.” quote from Jon Stokes, ars technica

6

FlexNetwork Architecture solutions include: FlexFabric – Data center converged compute, storage, and storage solution FlexCampus – High performance, secure solution for media ready campus FlexBranch – Simplified, secure, best of breed branch solution FlexManagement – Consolidated, single-pane of glass management solution FlexNetwork locks customers into HP… …exposes them to HP high margin services New FlexNetwork Architectures announced May, 2011 Claim FlexNetwork is open to 3 rd parties - ONE

7

HP originally claimed a lack of overlap and said “we will keep all products for as long as customers will buy them” This was short lived… Initial EoS announcements focused on individual switches, recent on switch families So far, since the acquisition of 3Com, HP has announced EoS of 38 E Series switches Feb 2011: E6400 (ProCurve) E4200-12G E4210-16-PoE E5500G Series March 2011: E5500 Series April 2011: E4210 Series E4210G Series E4500 Series E4500G Series June 2011: V1405 Series A3100 SI – Two slot models (H3C)

E G E PoE E5500G Series March 2011: E5500 Series April 2011: E4210 Series E4210G Series E4500 Series E4500G Series June 2011: V1405 Series A3100 SI – Two slot models (H3C)")

8

Confidential and Proprietary Information of Bleu Marketing Solutions Inc and its Clients © 2011 Objectives: –Promote Cisco leadership in the Las Vegas airport to incoming participants of the HP Discover 2011 event Reach: –HP’s largest user conference event - 10,000+ attendees for Discover 2011 –Las Vegas Airport - 110,000 passengers daily; 7th U.S., 11th World Placements: –Banners in A & B walkways –Exit signage –Video walls in baggage claim –Baggage carousels in baggage claim Thanks to Jen Robinson and CMO BN Solutions Marketing

13

Why We Win Strength of Customer Relationship Architectural understanding Customer Pre-investment with Cisco Reliance on Cisco products/support Technical Advantages and Education EnergyWise / Medianet / TrustSec Ease of use – i.e. Auto Smartports Lunch and learn Highlighting HP technical deficiencies Why We Lose Price HP focus TCO discussions on CapEx Aggressive discounting (>75%) in lighthouse accounts Relationship HP “buying the business” Disconnected account teams “Anyone But Cisco” attitude Bad technical experience issues Single Issue Technical Features 10G switches with vPC-like features and physical size requirements Lack of Competitive Readiness

in lighthouse accounts Relationship HP buying the business Disconnected account teams Anyone But Cisco attitude Bad technical experience issues Single Issue Technical Features 10G switches with vPC-like features and physical size requirements Lack of Competitive Readiness.")

14

Ross Fowler Beyond TCO Network TCO Architectural TCO Key Insights

16

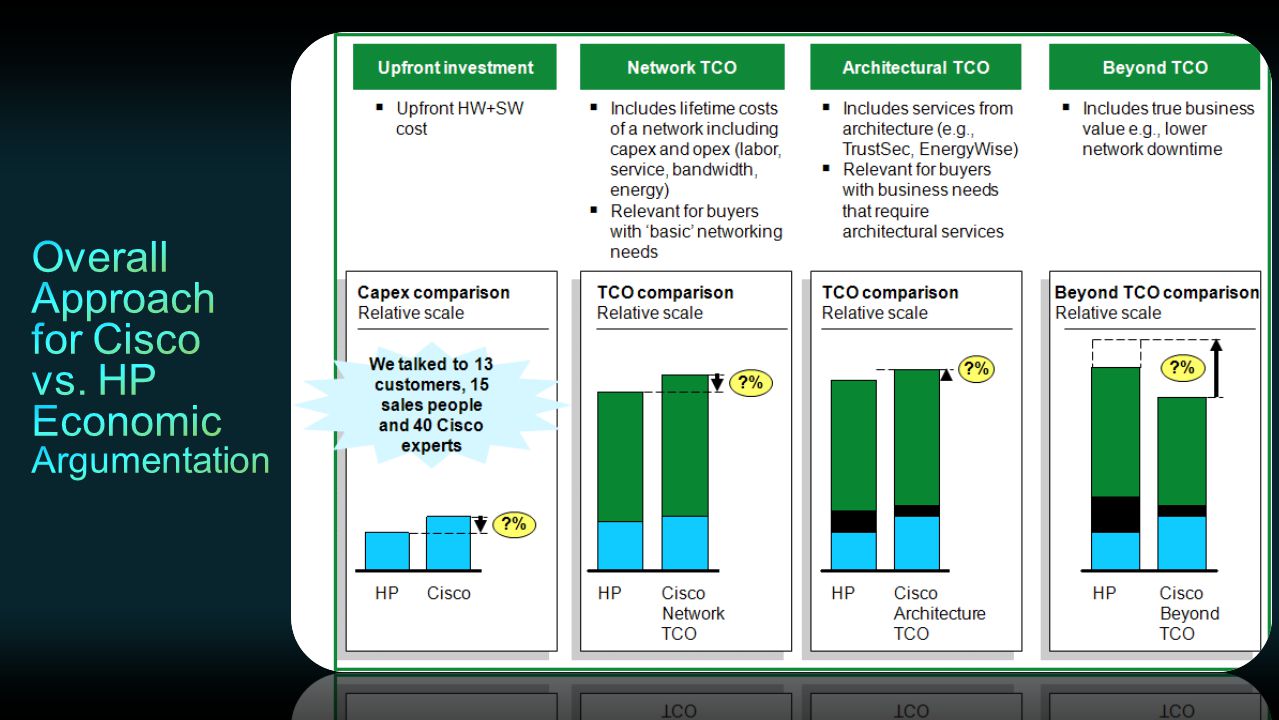

TCO is a better metric than CapEx to assess network cost because it considers the full impact on IT spend, including CapEx, services, labor, bandwidth, and energy Cisco BN architecture is at 4% premium over HP on TCO, making a more compelling case than 30-50% CapEx difference claimed by HP Even on an economy network, Cisco is at 7% TCO premium over HP, confirming a compelling economic argument for all customer segments Labor savings is the single biggest advantage Cisco has over HP; labor constitutes 50% of TCO and Cisco delivers 5-10% labor savings driven by unified wired and wireless, embedded security A quality network drives benefits beyond TCO, including Customer-specific benefits such as longer hardware refresh cycle, EnergyWise savings on endpoints and building energy Business benefits such as improved network uptime, higher user productivity and lower threat of security breach 1 2 3 4 5

19

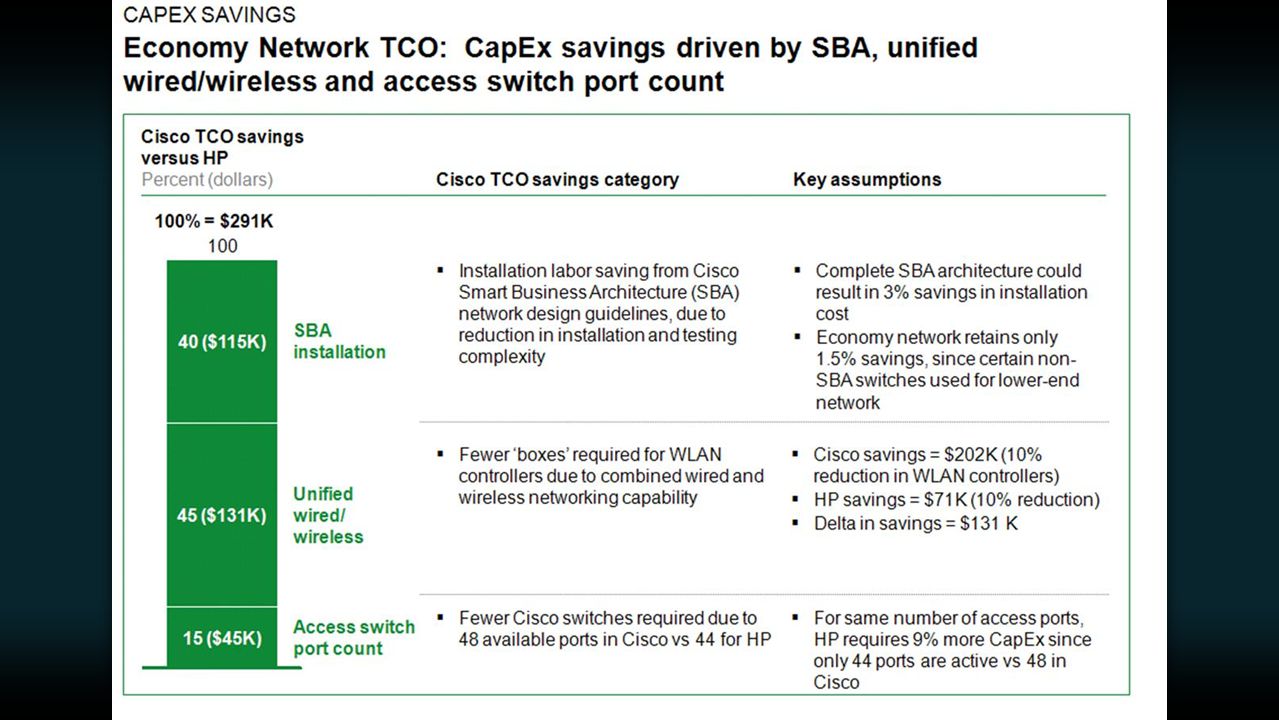

Hardware refresh Endpoint energy management Building energy management Cisco benefitEconomic impact Cisco vs. HP comparisons not included in TCO calculations, dependent on specific customer situations 6-8 year lifecycle for Cisco access and distribution switches and aggregation routers versus potential refresh by year 5 for HP ~5% increase in HP TCO Network based energy management for laptops, VDI, IP phones and other endpoints Integration of EnergyWise with building energy controls ~9% decrease in Cisco TCO ~3% decrease in Cisco TCO Could make Cisco up to 13% less expensive than HP!

21

1 additional security threat avoided per year compared to competing solutions Network downtime decreased by ~1 minute per year Productivity increased by ~1 hour per employee per year through mobility, higher video QoS and application optimization 1%, 4% or 7% premium for Cisco justified if… What does this look like for your company? Your sales force does not lose access to their quoting tool You are not waiting several minutes for each access to the ERP system You don't spend video conference time discussing video quality but rather discuss the decisions to be made in the meeting Mobile employees access data securely from any device, anytime What must you believe? You do not spend several days to detect, notify and respond to security threats, or lose business as a result OR

22

Is the customer an architectural buyer? Focus for today’s discussion Architectural TCO “Yes” to >=4 of the 8 questions “No” to at least 3 of the 8 questions Does customer rely on high network performance? Network TCO Product sale Yes No Can the customer envision becoming an architectural buyer? Yes No Does the network buyer’s job depend on a certain level of network uptime or SLAs? Has the customer been targeted for a cyber security attack in the past year? Does a large portion of the customer’s employee productivity depend on wireless and video? Does the customer have a predominantly Cisco network? Does the customer use infrastructure for full lifecycle (not refresh in 4-5 years even if equipment is functional)? Does the customer wish to enable corporate data access through consumer devices? Does the customer have large information databases or regulatory requirements? Does the customer expect >30% of traffic to be video in the next 18-24 months? Does the customer have >30% mobile workforce e.g., sales? Does the customer run high-performance applications in-house or from the Cloud? Does the customer emphasize energy management and sustainability?

. Does the customer wish to enable corporate data access through consumer devices. Does the customer have large information databases or regulatory requirements. Does the customer expect >30% of traffic to be video in the next months. Does the customer have >30% mobile workforce e.g., sales. Does the customer run high-performance applications in-house or from the Cloud. Does the customer emphasize energy management and sustainability .")

23

Ross Refer to TCO presentations and your video on Core Acceleration website. Next slide gives URL. DO NOT DISPLAY

24

Core Acceleration Website

25

Michael Rau Catalyst Switching BN Services Innovations HP vs Cisco BN Architecture

26

Architecture for Agile Delivery of the Borderless Experience BORDERLESS INFRASTRUCTURE Application Networking/ Optimization Switching SecurityRoutingWireless BORDERLESS NETWORK SYSTEMS BORDERLESS NETWORK SERVICES BORDERLESS END-POINT/ USER SERVICES Securely, Reliably, Seamlessly: AnyConnect Mobility: Motion App Performance: App Velocity Energy Management: EnergyWise Multimedia Optimization: Medianet Security: TrustSec Core Fabric Extended Cloud Extended Edge Unified Access POLICY MANAGEMENT SMART PROFESSIONAL AND TECHNICAL SERVICES: Realize the Value of Borderless Networks Faster APIs

27

A “Good Enough” Network Application and Endpoint Ignorant An Enterprise Next Generation Network Basic QoS Support through Basic Warranty Security as a Bolt On Acquisition Cost Standards Based Application Intelligence with Optimization, Endpoint Intelligence, Location & Policy Media Aware Control to Support Voice/Video Integration Warranty + Intelligent Services with Integrated Management Integrated Security from Premise to the Cloud Investment Protection & ROI Standards + Innovations Driving Standards Single Purpose Unified (Wired/Wireless/VPN, Building and Energy Control)

")

28

Context-Aware, Prioritized, High-Quality Voice and Video No Resource Reservation, Degraded Voice and Video CEO Meeting M&A Negotiation Sports Event GLOBAL BUSINESS, WORLDWIDE OFFICES Can My Network Deliver Real-Time Collaboration Experiences? CEO Meeting M&A Negotiation Sports Event

29

IPSLA VO (Video Operations) & MediaTrace Collaboration Manager Media Services Interface (MSI) ISRG2 Video DSP’s

& MediaTrace Collaboration Manager Media Services Interface (MSI) ISRG2 Video DSP’s")

30

Managed Nightly Shutdown $280,000 Additional Energy Policies $150,000 Annual Energy Costs $770,000 Am I Using My Network to Reduce My Energy Costs? Countywide Office Energy Management No Energy Management Total Savings $430,000 COUNTY OFFICES 10,000 PCs

31

EnergyWise IOS Software and API Interface Prime LMS Energywise Ecosystem of Partners for Energy Management “Light Bulb Moment: Lenovo and Cisco Help Businesses Manage Energy via Smarter PCs and Intelligent Networks” Universal POE (UPOE)

")

32

Flexible Centralized DIVERSE USERS, DEVICES, DATA Do I Have a Consistent Access Policy Architecture Across My Network for All Users and Devices? Inflexible Hard to Manage Wired Wireless VPN SimpleComplex, Multi-dimensional

33

Identity Services Engine (ISE) The best Security Product engineered by Cisco in 5 years to fit our Customer requirement on Identity and Policy enforcement on the Network – Recent CSE at Borderless Networks VT MACSec SGT’s and SGACL’s AnyConnect

The best Security Product engineered by Cisco in 5 years to fit our Customer requirement on Identity and Policy enforcement on the Network – Recent CSE at Borderless Networks VT MACSec SGT’s and SGACL’s AnyConnect")

34

Benefits Catalyst 2960-S Competitive feature set at compelling prices Reduced TCO with Smart Operations ENABLING THE BORDERLESS EXPERIENCE High Availability Catalyst 3K-XCatalyst 4K Traditional WorkspaceNext Generation Workspace Data Voice Any Device HD Video Lower TCO PoE Energywise Video Medianet Security TrustSec VDI

36

Dean & Ross: Close on Mike’s video. How to two tie together key point’s from Mike’s video and the TCO discussion to make business sense to the CFO? “It’s not for less, it’s not Cisco.” DO NOT DISPLAY

37

Dean Eyers Switching Market Share Taking the Fight to HP UCS Market Momentum New HP SI Agreement

38

Replace the HP Transitional Systems Integrator Agreement with a contract that reflects the evolving relationship between Cisco and HP Provide HP the ability to continue to sell Cisco products and services, recognizing that many existing HP customers will continue to want to purchase Cisco products and services through HP Provide HP with pricing and access to Cisco information that reflects HP’s status as a competitive partner Empower Cisco account teams to decide whether or not to grant HP additional discount through the DSA process Monitor HP’s resale and service entitlement activities for any violations of the agreement No longer able to directly sell ATP products after August 1 st, and reducing the standard discount on outsource/managed service accounts to 32% on August 22 nd

39

Campaign to maximize impact of Cisco achieving #3 in WW x86 Blade Servers validated Cisco’s position in server market

40

Cisco received ITU-T award for outstanding Next Generation network contributions Cisco partner for customer success and interoperability: VMWare, Citrix, NetApp, Intel

41

41 Source: Dell’Oro, calendar quarters $B Nx5010 Nx7K-F132XP- 15 Nx2148 Cat2960-S Cat4500E Nx1010 Nx5548 Nx4000 Cat4948E Cat3750-X First Customer Ship ACE30 Multi-hop FCoE/Nx5000 Nx5596UP/ Nx5548UP

42

42 Source: Dell’Oro, calendar quarters $B HP Rev Share 9.9% 10.6% 10.5% 9.3% 10.5% 10.3% 10.5% 11.9% 21.3% 21.8% 22.5% 20.5% 19.9% 20.3% 20.9% HP Port Share

43

Bust the “Good Enough is Good Enough” Myth Medianet, TrustSec, EngergyWise, Fabric Path, UCS Bust the TCO Myth Bust the HP Innovation Catalyst 6500 –Sup2T Nexus Family ISR G2 CleanAir, TrustSec –Policy Control, Virtualisation, High Availability Gartner spoke favourably of Cisco DCV and UCS

44

Selling Competitively: http://iwe.cisco.com/web/competitive Core Acceleration http://wwwin.cisco.com/WWSales/csinitiatives/core_acceleration.sht ml Engage the HP War Room: http://wwwin.cisco.com/go/got Martin Cook Luna Chiu Fred Manicom

45

Questions and Answers

46

Seed Question How does the TCO model work in markets where the labor rates are lower? Next Slides are TCO Back-up Slides. DO NOT DISPLAY

47

Appendix

53

Thank you.

Similar presentations