Download presentation

Presentation is loading. Please wait.

1

Vepa Kamesam Former Deputy Governor, RBI Chairman, IDRBT/BRBNML

Technology – The Core Service Differentiator for The Cochin Roundtable on Technology for Banks Vepa Kamesam Former Deputy Governor, RBI Chairman, IDRBT/BRBNML

2

Technology and Banking

The Quintessence Nature of Banking harmonizes closely with Technology – Banking Technology Information Storage Processing Transmission Tasks Common to Both

3

Banking and Technology

Innovative Risk Management Complex Credit Calculations Banking and Technology Global Operations Pervasive Branch Network Mass Transaction & Items Processing

4

Many Benefits of Technology

Increased operational efficiency, profitability & productivity Superior customer service Multi-channel, real-time transaction processing Better cross-selling ability Improved management and accountability Efficient NPA and risk management Minimal transaction costs Improved financial analyses capabilities

5

Focus aspects of Commercial Banking now are:

Core Banking (CBS) MIS & Intranet ATMs Electronic Banking Card Management Corporate Network Any Branch Banking Document Management CRM Risk Management Resource Management

MIS & Intranet. ATMs. Electronic. Banking. Card. Management. Corporate. Network. Any Branch Banking. Document. Management. CRM. Risk. Management. Resource. Management.")

6

Financial Technology Infrastructure

Data Center to host servers for: CBS ATM/Financial Switch Internet Banking DW/DM/CRM/MIS etc. Back-office Application Servers, Internet Server, Enterprise-wide Network & Networking Equipment Security Systems Systems at Branches/RO/ZO/CO Depts. Supporting Systems Disaster Recovery Site & Business Continuity

7

Technology – A Differentiator

Technology is indeed a differentiator not only in terms of competitive advantage, but also in terms of administrative and back-end processes…. But…due to rapid technology deployment in Indian banking sector, the “haves” and “have-nots” gap is all set to narrow quickly.

8

Technology Differentiation Fades Gradually….

9

How Long a Differentiator?

Then….can technology be enough of a differentiator? Any new technology or technology-enabled process can act as a differentiator or a competitive edge for some level of time. After that time, the technology still has to be adopted as a “necessity” and as a cost of doing business Thanks to shortening technology life cycles, it would be short sighted to assume that technology would be a long term differentiator…

10

Elements of Technology as a Differentiator

For Long-Term Differentiation Elements of Technology as a Differentiator Scalability & Flexibility Efficient utilisation, mgmt Process enabling Utility to customer Support Skills

11

The Human Interface Technology means changes in skills and culture…

This means extensive changes for the employees… The Implication – Train existing people Get new people Technology change Processes change Skills required change People & culture change

12

But Change is not easy… Organisational structure and culture not dynamic Extensive job redesign & redeployment is tough….as bank machinery is slow Staff has 2 critical jobs to learn– How to operate new technology How to undertake the new tasks This is not easy, as average employee age is nearly 45

13

Elements in People Issues

Choosing the suitable people for the task Career emergence instead of career planning Recognising and rewarding the achievers Managers taking on the role of trainers Encouraging new ideas and concepts Adopting a multi-disciplinary, multi-functional approach Shift from individual to business unit Balancing – creativity & routine, change Inculcating business discipline Understanding the need and extent of continuous education Getting rid of myths

14

Issues with Customers Not only employees, there are problems for customers too when a new technology arrives… The major challenges – Comfort levels Security and trust issues Convenience factor Getting rid of myths Migration from existing to new systems Changing the habits

15

Technology Acquisition

Inappropriate technology purchases can be the root of all problems… The Bank management has to: Give thought to the utilization rate Avoid “knee-jerk” reactions (“they have done it…I should also do it”) Be impartial in technology decisions (“I like that technology…I want it”) Understand where the solution will fit AND where it won’t! Assess the strengths & weakness of solution And seek answer to “are we ready for it?”

Be impartial in technology decisions ( I like that technology…I want it ) Understand where the solution will fit AND where it won’t! Assess the strengths & weakness of solution. And seek answer to are we ready for it")

16

For Sustained Differentiation

Differentiation is attained not achieved just through technology, it is gained in the way the technology is selected, implemented and utilised Technology For Sustained Differentiation Goal definition Integrating business & technology goals Solution features Vendor selection Business process re-engineering Change management Efficient utilisation Customer utility Technology Management Support functions Maintenance Back-ups and Disaster Recovery Scalability & flexibility Learning & evolution

17

Why Central Banks are interested?

Technology and Central Banks The potential Technology offers to improve internal processes Technology has Affected every Core Central Banking Function Why Central Banks are interested?

18

Why Central Banks are Interested?

The widespread adoption of technology by the banking industry The impact of technology on every single core central banking function Supervision and Regulation Currency Management Monetary & Financial Stability The potential technology offers to central banks for rendering more effective its internal processes and functions

19

Regulation and Supervision – The Challenge

Challenge of Technology: New markets, products, services, delivery channels Opened up a market for “risks” – derivatives Challenge of financing tech firms & IT innovation all have implications for the stability of banks and of the economy The Opportunity Regulators have new tools Focus of all recent financial sector reforms Emergence of non-intrusive, focused supervision …with a view to prevent frauds and disturbances to financial stability

20

Technology and Banking Supervision

THE RBI RESPONSE Offsite Supervision & Monitoring OSMOS COSMOS (Non banking Financial Companies / Development Financial Institutions) UBD Soft Credit Information Bureau (A joint venture between Housing Development Finance Corporation Ltd., State Bank of India, Trans Union International Inc. & Dun & Bradstreet Information Services India Pvt. Ltd.)

UBD Soft. Credit Information Bureau (A joint venture between Housing Development Finance Corporation Ltd., State Bank of India, Trans Union International Inc. & Dun & Bradstreet Information Services India Pvt. Ltd.)")

21

Currency Management and Technology – Opportunities Galore

Currency Management - a formidable task in India given… the geographical size, the volume and value of notes and coins in circulation, preference for cash and currency handling practices ...but technology offers immense opportunities to improve performance RBI’s The Clean Note Policy (1999) Establishment of 2 state of the art currency presses Technology driven anti counterfeit measures 48 fully automated Currency Verification & Processing Systems 21 Shredding and Briquetting Machines

Establishment of 2 state of the art currency presses. Technology driven anti counterfeit measures. 48 fully automated Currency Verification & Processing Systems. 21 Shredding and Briquetting Machines.")

22

Technology & Monetary Systems

Technology has: transformed the conduct of the payment and settlement system set the stage for an unprecedented growth in financial activity across the globe Rendered more vulnerable the domestic payment system and financial stability to international “shocks” … making the conduct of monetary policy more complex and prone to implementation and operational risks

23

Technology & Monetary Systems

The Opportunities – The proliferation of IT has also set the stage for improving and managing risks in payment systems Electronic Trading Systems DVP/PVP RTGS Secured Netting Systems The growth of the Central Counterparty (CCP) Continuous Linked Settlement

Continuous Linked Settlement.")

24

IT and Payment and Settlement Systems

Demateria-lisation Of Securities Delivery Versus Payments Payment Continuous Linked Settlement Electronic Dealing Platforms Real Time Gross Central Counter party Secured Netting Systems

25

RBI INITIATIVES IN PAYMENT & SETTLEMENT SYSTEMS

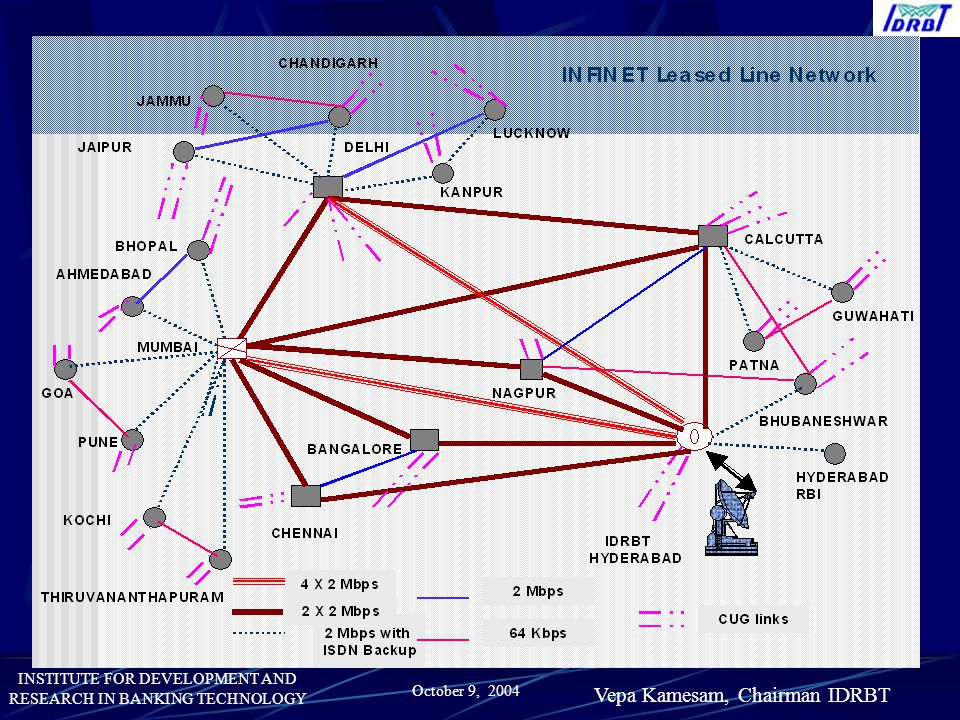

NFS/IBPG CFMS NEFT RTGS PKI-based Security RBI INITIATIVES IN PAYMENT & SETTLEMENT SYSTEMS SFMS PDO-NDS & SSS Compliance with BIS Core Principles INFINET Clearing Corporation of India IDRBT

26

RBI Initiatives in Payment and Settlement Systems (1)

The IDRBT Network Externalities The Indian Financial Network (INFINET) Messaging Solutions The Structured Financial Messaging System (SFMS) Security Public Key Infrastructure IDRBT CA National Financial Switch Inter Bank Payment Gateway

Messaging Solutions. The Structured Financial Messaging System (SFMS) Security. Public Key Infrastructure. IDRBT CA. National Financial Switch. Inter Bank Payment Gateway.")

28

Financial Networks SWIFT Reuters NSE Gateways and Integration with

Other Financial Network Services G1 - SWIFT Network G2 - Reuters Network G3 - Stock Exchange Network G4 - Inter Banks/FIs G5 - Shared ATMs G6 - Clearing Operations Network G7 - Internet Corporate Network Inter Banks/FIs Network Shared ATMs Network Clearing Operations Network SWIFT Reuters NSE G1 G2 G3 G4 G5 G6 G7 Internet INFINET

29

Structured Financial Messaging System

Bank-1 Gateway Bank-2 Gateway Bank-n Gateway Branch-2 Branch-n Branch-1 Central Server at IDRBT ………..…………….….. ………..…………….….…….. … …….…… Branch-1

30

PKI Hierarchy CCA IDRBT CA RA RA RA Subscriber Subscriber Subscriber

Repository IDRBT CA RA RA RA Subscriber Subscriber Subscriber Subscriber Subscriber Subscriber

31

IDRBT CA Physical Infrastructure

Iron gate with Biometric Access Access through Swipe Card Network Strong Room Key Ceremony Room Operational Room Tier 1 Tier 2 Tier 3 Tier 4 Tier 5 UPS Administration Room Media proof CA Private Key Storage Biometric Access

32

NFS CONNECTIVITY with Existing Consortiums & Individual Banks

ISDN National Financial Switch & E- Payment Gateway ISDN MITR Location: Chennai BANCS & Cashtree Location: Mumbai Leased Line Bank 2 INFINET Bank 1 Broad Band VSAT Bank N CashNet IP Address: Subnet Mask: Location: Mumbai Primary Link Backup Link

33

RBI Initiatives in Payment and Settlement Systems (2)

A Real Time Gross Settlement System Reduction of systemic risk in inter bank payment systems To be implemented by the year end The Centralised Funds Settlement System Facilitating effective liquidity management The Negotiated Dealing System A modern electronic dealing platform for gilts Enabling Straight Through Processing

34

IAS Real Time Gross Settlement CFMS Settlement Accounts Intra Day

Liquidity SSS IFTP Strip & Store Processes RBI Payments and Actg. Entry Interface INFINET NSS Participant’s Interface Participant’s Interface Participant’s Interface

35

RTGS Scenario 87 banks have implemented it

6 more to implement in a fortnight Customer transactions have already started Total volumes – Transactions on average Rs.20,000 crores per day

36

Centralised Funds Management System

Gateway for the participating banks DAD-1 Bank 1 DAD-2 Bank 2 CFMS Server Bank 3 DAD-16 Balance checks & funds transfer messages Bank n DAD-17

37

Centralised Funds Management System – Countrywide Spread

38

Negotiated Dealing System & the Securities Settlement System

Electronic dealing platform in government securities and money market instruments- Primary and Secondary markets Quicker Price Discovery Straight Through Processing- Settlement of transactions Delivery versus Payments Efficient Servicing Centralised Depository and Debt Servicing Wide Area Based Dealing System

39

RBI Initiatives in Payment and Settlement Systems (3)

The Securities Settlement System Providing centralized depository and settlement services Seamlessly integrated with the NDS and RTGS Systems The Clearing Corporation of India Secured netting services with central counterparty arrangements G-Sec and Forex segments Elimination of settlement risks with liquidity saving elements

40

The Clearing Corporation of India

Promoted by large banks & financial institutions Central Counterparty to trades in Government Securities Forex markets Secure netting system

41

Smart Cards – The Future

Multi-application Smart Card Channel of the future Pilot project started Pilot Project funded by MCIT, Govt. of India The project is in progress in partnership with IDRBT, IIT Bombay, and Banks in India

42

Goal of Payment and Settlement Systems

Establishment of a secure, efficient, modern payment and settlement system in the country Ensuring full compliance with the Core Principles for Systemically Important Payment Systems of the Bank for International Settlements

43

RBI itself uses Technology for differentiation

An integrated solution for each functional area Online analytical capabilities – The Integrated Foreign Exchange Management Solution, The Human Resource Information System, Integrated Monetary Policy Solution Online Decision Making – The Centralized Database Management System , The Enterprise Knowledge Management System Customer Service – RBI website, coin & note dispensing machines for public, Interactive voice response for banks & FIs, ECS/EFT, cheque truncation This is apart from technologies used for central banking functions

44

RBI and Customer Service…(1)

Dissemination of information The RBI website Multiple Delivery Channels Coin & Note Dispensing Machines For the general public Interactive Voice Response System For banks and financial institutions Web server For government customers On the anvil…. A secured web server SFMS/ based communication with customers

45

RBI and Customer Service...(2)

Improvements in payment and settlement systems MICR Clearing Enabling faster clearing of cheques Cheque Truncation & E-Cheques On the drawing board ECS/EFT Enabling T+2 settlement of our equities market National EFT Enabling T+0 settlement of all customer funds transfer transactions

46

Technology Vision of the RBI

Centralised Database Management System Enterprise Knowledge Integrated Accounting System Integrated Government Accounting System Currency Operations Desk Top Decision Making Capability Desk Top Analytical Capability Desk Top Transactional Capability Securities Settlement Integrated Establishment Offsite Supervisory Systems Integrated Forex Human Resource Information System

47

Issues in Implementation

“Less than 10% of failures are due to technical snags – most are due to poor management and implementation” Resistance to change Overlooking process reengineering Project management Dedicated project teams Change management Policies People Skills & Training Basic Infrastructure – telecom, power Security Privacy & confidentiality Legal and regulatory issues

48

Pre-requisites for Technology

Business Process Re-engineering Human Resource Empowerment Planning for Disasters

49

The pre-requisites for Technology

Planning for disasters Increased operational risk Business Continuity Planning Business Process Re-engineering Human Resource Empowerment

50

People represent the most precious asset

Getting Personal with Personnel People represent the most precious asset Large employee base – largely untrained. Training scope & methodology? VRS to balance costs. Break even? Down sizing? Bring in young blood Campus recruitment Re-defining & designing jobs. Career paths? Specialist Vs. Generalist Attrition of trained employees to IT industry / other banks. Competitive incentives? Re-location of personnel. Union issues? Retrained personnel. Morale of employees?

51

Need for Training All these developments call for extensive, continuous training Current and future technology implementations call for at least 20% of officers specialise in IT Hence need for specially skilled people – a mix of: System administrators Application managers (knowledgeable about both banking and technology) Technology managers (who form the core team of technology professionals).

Technology managers (who form the core team of technology professionals).")

52

Success is a journey not a destination.

- Arthur Ashe Thank You

53

Monetary Policy – The Challenge (1)

The proliferation of IT has… redefined the toolkit of economic indicators used in implementing monetary policy rendered more complex, the task of compiling statistical information rendered difficult the task of capturing the impact of IT on price levels raised issues in respect of the possible proliferation of digital money

54

Monetary Policy – The Challenge (2)

transformed the conduct of the payment and settlement system set the stage for an unprecedented growth in financial activity across the globe Rendered more vulnerable the domestic payment system and financial stability to international “shocks” … making the conduct of monetary policy more complex and prone to implementation and operational risks

55

Monetary Policy – The Opportunity

The proliferation of IT has also set the stage for improving and managing risks in payment systems Electronic Trading Systems DVP/PVP RTGS Secured Netting Systems The growth of the Central Counterparty (CCP) Continuous Linked Settlement

Continuous Linked Settlement.")

Similar presentations

: Nationwide electronic funds transfer (EFT) system that facilitates inter-bank clearing of debit and credit.>")