Download presentation

Presentation is loading. Please wait.

1

Dairy Market Update: May 2013 Dr. Craig Thomas Michigan State University Extension Dairy Farm Business Management & Milk Marketing Educator Sanilac, Huron, Tuscola, St. Clair, Lapeer, Saginaw, Genesee, Macomb, Oakland, Washtenaw, Wayne, & Monroe Counties

2

Benefactor ($200) Active Feed Co. Major Sponsor ($75-$100) Contributor ($50) Exchange State Bank Eastern Michigan Bank Thumb Veterinary Services Crop Production Services-Sandusky & Deckerville 2013 Sponsors Dairy Farmers of America- Steve Steely Graff Chevrolet/Buick, Inc. Sanilac Drain & Tile Co. Secher Site Specific LLC GreenStone FCS

Contributor ($50) Exchange State Bank Eastern Michigan Bank Thumb Veterinary Services Crop Production Services-Sandusky & Deckerville 2013 Sponsors Dairy Farmers of America- Steve Steely Graff Chevrolet/Buick, Inc. Sanilac Drain & Tile Co. Secher Site Specific LLC GreenStone FCS.")

3

+ $1.87 Class III vs. Apr 2012 ($14.68, +$2.91 vs. Apr average) April Milk Prices + $3.30 Class IV vs. Apr 2012 ($14.80, +$3.30 vs. Apr average) $18.10 +$0.35 $17.59 +$0.66 USDA Michigan Mailbox Jan 2013: $19.81 up $0.77

April Milk Prices + $3.30 Class IV vs. Apr 2012 ($14.80, +$3.30 vs. Apr average) $ $0.35 $ $0.66 USDA Michigan Mailbox Jan 2013: $19.81 up $0.77.")

4

+0.2% Nationally versus April 2012 U.S. Production 2012 +2.1% vs. 2011 2013 +0.1% vs. 2012 (99-12 ave. = +1.6%) +0.3% Top 23 States versus April 2012

+0.3% Top 23 States versus April")

5

+0.2% Nationally versus April 2012 U.S. Production 2012 +2.1% vs. 2011 2013 +0.1% vs. 2012 (99-12 ave. = +1.6%) Tenth time in past eleven months below trend increase. Record 200.324 billion lbs. for 2012!

Tenth time in past eleven months below trend increase. Record billion lbs. for 2012!.")

6

+0.2% Nationally versus April 2012 U.S. Production 2012 +2.1% vs. 2011 2013 +0.1% vs. 2012 (99-12 ave. = +1.6%) BUT… Q-1 2012 U.S. milk production was up 4.2% vs. 2011!

BUT… Q U.S. milk production was up 4.2% vs. 2011!.")

7

+0.2% Nationally versus April 2012 U.S. Production 2012 +2.1% vs. 2011 2013 +0.1% vs. 2012 (99-12 ave. = +1.6%) Michigan +1.3% versus April 2012.

Michigan +1.3% versus April")

8

+0.2% Nationally versus April 2012 U.S. Production 2012 +2.1% vs. 2011 2013 +0.1% vs. 2012 (99-12 ave. = +1.6%) Seqestration! Milk Production Report No cow numbers! No milk per cow! administrative data only

Seqestration. Milk Production Report No cow numbers. No milk per cow. administrative data only.")

9

+0.2% Nationally versus April 2012 U.S. Production 2012 +2.1% vs. 2011 2013 +0.1% vs. 2012 (99-12 ave. = +1.6%) M:F ratio <2.0 for 27 of past 29 months.

M:F ratio <2.0 for 27 of past 29 months..")

10

+0.2% Nationally versus April 2012 U.S. Production 2012 +2.1% vs. 2011 2013 +0.1% vs. 2012 (99-12 ave. = +1.6%) April Milk:Feed Price Ratio All-Milk: $19.30 (+0.20) Corn: $6.67 (-$0.46) Soybeans: $14.20 (-$0.40) Alfalfa Hay: $215 (-$4.00)

April Milk:Feed Price Ratio All-Milk: $19.30 (+0.20) Corn: $6.67 (-$0.46) Soybeans: $14.20 (-$0.40) Alfalfa Hay: $215 (-$4.00).")

11

+0.2% Nationally versus April 2012 U.S. Production 2012 +2.1% vs. 2011 2013 +0.1% vs. 2012 (99-12 ave. = +1.6%) Feed costs up 3.8% vs. April 2012 ($11.92 to $12.38).

Feed costs up 3.8% vs. April 2012 ($11.92 to $12.38)..")

12

+0.2% Nationally versus April 2012 U.S. Production 2012 +2.1% vs. 2011 2013 +0.1% vs. 2012 (99-12 ave. = +1.6%) USDA report on alfalfa hay and alfalfa hay mixtures: U.S.: -34% vs. last May 1 st Hay stocks declined by 50% or more in nine states vs. last year (MI, MN, NY, OH, VT, WI). Little indication 2013 crop will be large enough to replenish stocks. Hay acreage has fallen to second lowest level on record.

USDA report on alfalfa hay and alfalfa hay mixtures: U.S.: -34% vs. last May 1 st Hay stocks declined by 50% or more in nine states vs. last year (MI, MN, NY, OH, VT, WI). Little indication 2013 crop will be large enough to replenish stocks. Hay acreage has fallen to second lowest level on record..")

13

+0.2% Nationally versus April 2012 U.S. Production 2012 +2.1% vs. 2011 2013 +0.1% vs. 2012 (99-12 ave. = +1.6%) IOFC up 25.8% (+$1.74/cwt) vs. April 2012 ($8.51 to $6.77).

IOFC up 25.8% (+$1.74/cwt) vs. April 2012 ($8.51 to $6.77)..")

14

+0.2% Nationally versus April 2012 U.S. Production 2012 +2.1% vs. 2011 2013 +0.1% vs. 2012 (99-12 ave. = +1.6%) IOFC up 5.5% vs. March 2013 (+$0.47).

IOFC up 5.5% vs. March 2013 (+$0.47)..")

15

+0.2% Nationally versus April 2012 U.S. Production 2012 +2.1% vs. 2011 2013 +0.1% vs. 2012 (99-12 ave. = +1.6%) April all-milk price +$2.50/cwt vs. April 2012.

April all-milk price +$2.50/cwt vs. April")

16

Above Trend For Apr April: +11.9% vs. April 2012 +1.1% vs. March April +28,600 hd vs. April 2012 2012 +187,200 hd vs. 2011! YTD +56,200 hd (as of 4/30/13) Jan (296.9) highest monthly slaughter number since 1986; year of the whole-herd buyout.

Jan (296.9) highest monthly slaughter number since 1986; year of the whole-herd buyout..")

17

Cull Rate Above Long Term Average (29.0%) +4.1% California: ~100 dairy farms are closing their doors permanently each year.

+4.1% California: ~100 dairy farms are closing their doors permanently each year.")

18

Cull Rate Above Long Term Average (29.0%) +4.1% U.S. cull cow prices down 1.5% vs. March 2012 ($82.90 vs. $84.20).

..")

19

Cull Rate Above Long Term Average (29.0%) +4.1% What will the future hold?

+4.1% What will the future hold")

20

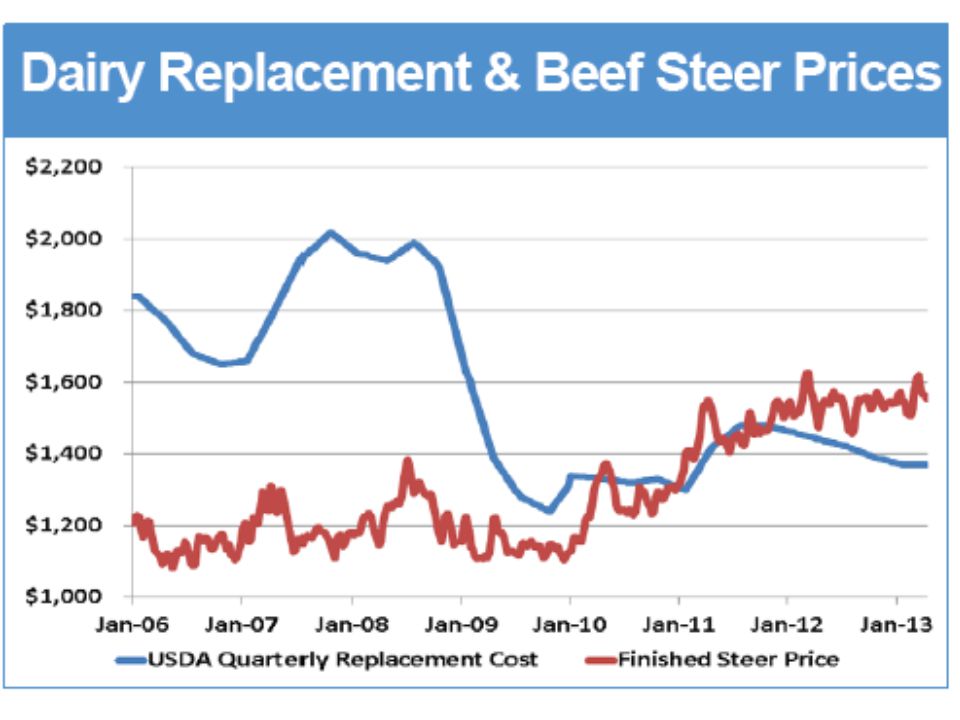

Cull Rate Above Long Term Average (29.0%) +4.1% Unusual circumstances moving forward: Steers >$ vs. replacement heifers xbred calf likely more value than purebred heifer Less sexed semen usage Holstein heifers being sold in lots destined for the feedlot Strong beef prices continue to fuel unprecedented dairy cull rates Beef industry will continue to pull dairy to beef Thus, dairy herd will eventually shrink and may be more difficult to grow in the future.

22

Going Strong…Better! No??!! 2012 vs. 2011 +1.7%; 2013 vs. 2012 +0.8% (1996-12 average = +1.6%) Cheese: 1996-12 average = +2.5% 2012 vs. 2011 +1.2%; 2013 vs. 2012 +0.1%

Cheese: average = +2.5% 2012 vs %; 2013 vs %.")

23

Going Strong…Better! No??!! 2012 vs. 2011 +1.7%; 2013 vs. 2012 +0.8% (1996-12 average = +1.6%) Cheese: 1996-12 average = +2.5% 2012 vs. 2011 +1.2%; 2013 vs. 2012 +0.1% Total commercial disappearance set all-time monthly record for Jan in Jan; but down 0.7% in Feb vs. Feb 2012!

Cheese: average = +2.5% 2012 vs %; 2013 vs % Total commercial disappearance set all-time monthly record for Jan in Jan; but down 0.7% in Feb vs. Feb 2012!.")

24

Going Strong…Better! No??!! 2012 vs. 2011 +1.7%; 2013 vs. 2012 +0.8% (1996-12 average = +1.6%) Cheese: 1996-12 average = +2.5% 2012 vs. 2011 +1.2%; 2013 vs. 2012 +0.1% 2013 vs. 2012 (YTD Jan-Feb) American Cheese: +1.8% (+2.3%) Other Cheese: +1.9% (+2.5%) Butter: +10.2% (+2.8%) NFDM: -18.7% (+5.3%) Fluid Milk: -4.4% (Feb)

Cheese: average = +2.5% 2012 vs %; 2013 vs % 2013 vs (YTD Jan-Feb) American Cheese: +1.8% (+2.3%) Other Cheese: +1.9% (+2.5%) Butter: +10.2% (+2.8%) NFDM: -18.7% (+5.3%) Fluid Milk: -4.4% (Feb).")

25

Going Strong…Better! No??!! 2012 vs. 2011 +1.7%; 2013 vs. 2012 +0.8% (1996-12 average = +1.6%) Cheese: 1996-12 average = +2.5% 2012 vs. 2011 +1.2%; 2013 vs. 2012 +0.1% March fluid milk 38 th consecutive month of declining sales versus same month last year.

Cheese: average = +2.5% 2012 vs %; 2013 vs % March fluid milk 38 th consecutive month of declining sales versus same month last year..")

26

American Cheese (+5.3% Apr vs. Apr 2012, +35.2 M lbs. vs. 5/1/12) Total Cheese (+4.5% Apr vs. Apr 2012, +48.1 M lbs. vs. 5/1/12) 5/28/13 Close = $1.7388 May 07-12 Average = $1.5505

Total Cheese (+4.5% Apr vs. Apr 2012, M lbs. vs. 5/1/12) 5/28/13 Close = $ May Average = $")

27

American Cheese (+5.3% Apr vs. Apr 2012, +35.2 M lbs. vs. 5/1/12) Total Cheese (+4.5% Apr vs. Apr 2012, +48.1 M lbs. vs. 5/1/12) May 07-12 Average = $1.5505 Total Cheese Inventory Above 1.0 billion pounds fifth consecutive month! 5/28/13 Close = $1.7388

Total Cheese (+4.5% Apr vs. Apr 2012, M lbs. vs. 5/1/12) May Average = $ Total Cheese Inventory Above 1.0 billion pounds fifth consecutive month. 5/28/13 Close = $")

28

American Cheese (+5.3% Apr vs. Apr 2012, +35.2 M lbs. vs. 5/1/12) Total Cheese (+4.5% Apr vs. Apr 2012, +48.1 M lbs. vs. 5/1/12) May 07-12 Average = $1.5505 Cheese Inventories All-time historical highs! 5/28/13 Close = $1.7388

Total Cheese (+4.5% Apr vs. Apr 2012, M lbs. vs. 5/1/12) May Average = $ Cheese Inventories All-time historical highs. 5/28/13 Close = $")

29

American Cheese (+5.3% Apr vs. Apr 2012, +35.2 M lbs. vs. 5/1/12) Total Cheese (+4.5% Apr vs. Apr 2012, +48.1 M lbs. vs. 5/1/12) May 07-12 Average = $1.5505 2013 cheese production (Jan-Mar): American cheese 2.7% (1.9%) Total cheese +1.7% (2.7%) vs. Jan-Mar 2012. 5/28/13 Close = $1.7388

Total Cheese (+4.5% Apr vs. Apr 2012, M lbs. vs. 5/1/12) May Average = $ cheese production (Jan-Mar): American cheese 2.7% (1.9%) Total cheese +1.7% (2.7%) vs. Jan-Mar /28/13 Close = $")

30

+22.2% versus Apr 2012 Butter May 07-12 Average = $1.5062 5/28/13 Close = $1.5450

31

+22.2% versus Apr 2012 Butter May 07-12 Average = $1.5062 Butter Inventory All-time historical high! 5/28/13 Close = $1.5450

32

+22.2% versus Apr 2012 Butter May 07-12 Average = $1.5062 2013 butter production (Jan-Mar) +4.4% (2.3%) vs. Jan-Mar 2012. 5/28/13 Close = $1.5450

33

Dairy Exports Dairy trade surpluses 37 consecutive months! FY-2013 (Oct-Mar): $918.1 M!

: $918.1 M!")

34

FY-2013: October-March U.S. dairy exports equaled: CY-2011, 13.3%; CY-2012, 13.2%. March 13.5% of total U.S. milk solids production! Jan-Mar 13.1% (12.9%)

.")

35

FY-2013: October-March U.S. dairy exports equaled: CY-2011, 13.3%; CY-2012, 13.2%. March 24 th time in past 25 months exports exceeded $400 million!

36

Dairy Exports CY-2013 (Jan-Mar) Exports as a % of total U.S. production: NFDM/SMP: 41% (44%) Cheese: 5.6% (5.3%) Butter: 5.9% (5.2%) Dry Whey: 46% (46%) Lactose: 72% (68%)

Cheese: 5.6% (5.3%) Butter: 5.9% (5.2%) Dry Whey: 46% (46%) Lactose: 72% (68%).")

37

Dairy Exports 2011-2012 One of every 8 tanker loads of raw milk was ultimately exported!

38

Dairy Exports 2013 Outlook Milk production growth in Oceania, EU, and U.S., unlikely to satisfy world dairy product demand. China expected to increase dairy imports by 14%. New Zealand milk prdn down >16% in Mar; -2.3% in Feb. YTD up 4.8% vs. 2012; Australia -1.6% vs. 2012 (drought driven). Offerings are tight…servicing existing accounts on the books and having little extra for other demand. EU milk prdn down every month vs. last year since July 2012; weak 2013 spring flush. Thus, no significant finished product stocks in EU or Oceania to buffer markets moving into remainder of 2013. U.S. dairy product prices remain below international prices. Higher international demand has softened demand (at least in the short term); however, look for stronger prices in second half of 2013.

. Offerings are tight…servicing existing accounts on the books and having little extra for other demand. EU milk prdn down every month vs. last year since July 2012; weak 2013 spring flush. Thus, no significant finished product stocks in EU or Oceania to buffer markets moving into remainder of U.S. dairy product prices remain below international prices. Higher international demand has softened demand (at least in the short term); however, look for stronger prices in second half of")

39

Dairy Exports Big 5 Dairy Exporters USDEC predicts will be down >1% in milk prdn for first half of 2013; a shortfall of 1.6 M tons of milk (~3.5 B lbs).

.")

40

Dairy Exports USD Strengthening!

41

Dairy Exports Tom Suber USDEC president Global economic signs are starting to move in a more positive direction, demand and consumption will continue rising, and world prices are expected to come more in line with U.S. prices.

42

Dairy Exports China will be a key player in determining the health of global dairy markets given its demand for an ever-growing share of dairy supplies. +8.1% GDP growth in 2013 (+7.5% in 2011) >5% annual growth in dairy consumption!

>5% annual growth in dairy consumption!.")

43

Dairy Exports World …there are currently no significant surplus stocks in the United States or the EU to buffer markets. Consequently global economic and population growth are expected to keep driving import demand which could put upward pressure on dairy prices particularly towards the second half of 2013.

44

Dairy Exports Long Term Outlook Bright, but loaded with risk. U.S. Dairy Export Council The United States cannot absorb back into the domestic market 13% of annual milk solids produced in this country. And as we produce more milk, most of it has to go to international customers because domestic consumption is growing slowly...

45

Retail Food Prices March Whole Milk CPI = +1.9% Price: -$0.068/gal Cheese CPI = -1.3% Price: -$0.109/lb (p) +$0.077/lb (n) Butter CPI = +1.0% Price: NA All-Food CPI = +1.5% Dairy CPI = -0.5% MPFE CPI = +1.2% Ice Cream CPI = +0.0% Price: -$0.001/half gal.

+$0.077/lb (n) Butter CPI = +1.0% Price: NA All-Food CPI = +1.5% Dairy CPI = -0.5% MPFE CPI = +1.2% Ice Cream CPI = +0.0% Price: -$0.001/half gal.")

46

Class III Current Class III futures prices are averaging +$1.93 (2013), +$1.86 (next 12 mos.), +$0.73 (2014) versus the 2007-2013 averages.

, +$1.86 (next 12 mos.), +$0.73 (2014) versus the averages.")

47

Class III / Cheese Next 12 mos: $18.55 ($18.06) (-$0.49) 4/29/13 2013: $18.13 ($18.52) (-$0.39) 2014: $16.93 ($16.85) (+$0.07)

(-$0.49) 4/29/ : $18.13 ($18.52) (-$0.39) 2014: $16.93 ($16.85) (+$0.07)")

48

Class III Current Class III futures prices are averaging +$1.93 (2013), +$1.86 (next 12 mos.), +$0.73 (2014) versus the 2007-2013 averages.

, +$1.86 (next 12 mos.), +$0.73 (2014) versus the averages.")

49

Wheres the Market Headed? Cheese prices. 5/29/13 Ave. $1.7388 4/29/13 $1.7663 block/barrel cheese price.

50

Wheres the Market Headed? Cheese prices. 5/29/13 Ave. $1.7388 Decrease of $0.0275

51

Wheres the Market Headed?

53

USDA Forecast May Milk production: 2013 201.8 B lbs. +0.7% Milk consumption: 195.0 B lbs. +0.9% 2013 prices: Class III: $17.80-$18.30 (-5¢) Class IV: $18.20-$18.80 (+10¢) All-Milk: $19.5-$20.00 (+5¢) Cheese: $1.745-$1.795 (+1¢) Butter: $1.570-$1.650 (+1¢) NFDM: $1.590-$1.630 (+0.5¢) Dry whey: $0.580-$0.610 (-2.5¢)

Class IV: $18.20-$18.80 (+10¢) All-Milk: $19.5-$20.00 (+5¢) Cheese: $1.745-$1.795 (+1¢) Butter: $1.570-$1.650 (+1¢) NFDM: $1.590-$1.630 (+0.5¢) Dry whey: $0.580-$0.610 (-2.5¢).")

54

Prices Spring flush ending soon; major heat in 2013? Domestic consumption weak, exports remain strong; push on to produce more milk, esp. w/lower feed $; will U.S. dairy herd shrink? Will higher prices and stronger USD limit upside? Cheese: flat then up? $2.00 by mid-summer? Butter: flat then up? $2.00 by mid-summer? Class III & IV: flat near term; ave. near or above USDA top? Will cow numbers fall; international demand remain strong? Wheres the Market Headed?

55

LGM-Dairy FY-2014 budget calls for increase in LGM subsidies from $20 M to $100 M. DSA likely component of new Farm Bill…but when? Wheres the Market Headed?

56

Long Range Weather Forecast Jun-Jul-Aug Temperature

57

Long Range Weather Forecast Aug-Sep-Oct Temperature

58

Long Range Weather Forecast Jun-Jul-Aug Precipitation

59

Long Range Weather Forecast Aug-Sep-Oct Precipitation

61

Prediction is very difficult, especially if it is about the future. -Neils Bohr Wheres the Market Headed?

62

It doesnt matter how smart you are unless you stop and think. -Thomas Sowell

63

Craig Thomas Web Site www.msu.edu/~thomasc

64

News Web Site msue.anr.msu.edu Agriculture Dairy

65

2013 Ag Market Updates Live over the Net! Send me your e-mail address to receive advance notification of live Ag Market Update webinars.

66

Craig Thomas thomasc@anr.msu.edu http://breeze.msu.edu/craigthomas

67

The End

Similar presentations