Download presentation

Presentation is loading. Please wait.

1

Trade Blocs and Monetary Unions Mauro F. Guillén

2

Multilateralism: The GATT Rounds (General Agreement on Tariffs and Trade) NameStartDurationCountriesSubjects coveredAchievements GenevaApr-477 mos.23Tariffs Signing of GATT, 45,000 tariff concessions affecting $10 billion of trade AnnecyApr-49513TariffsCountries exchanged some 5,000 tariff concessions TorquaySep-50838Tariffs Countries exchanged some 8,700 tariff concessions, cutting the 1948 tariff levels by 25% Geneva IIJan-56526Tariffs, admission of Japan$2.5 billion in tariff reductions DillonSep-601126TariffsTariff concessions worth $4.9 billion of world trade KennedyMay-643762Tariffs, Anti-dumpingTariff concessions worth $40 billion of world trade TokyoSep-7374102 Tariffs, non-tariff measures, "framework" agreements Tariff reductions worth more than $300 billion dollars achieved Uruguay* Sep-8687123 Tariffs, non-tariff measures, rules, services, intellectual property, dispute settlement, textiles, agriculture, creation of WTO, etc The round led to the creation of WTO, and extended the range of trade negotiations, leading to major reductions in tariffs (about 40%) and agricultural subsidies, an agreement to allow full access for textiles and clothing from developing countries, and an extension of intellectual property rights. Doha**Nov-01?141 Tariffs, non-tariff measures, agriculture, labor standards, environment, competition, investment, transparency, patents etc The round is not yet concluded. * Ended with the creation of the WTO. ** Started by the WTO.

3

The WTO Dark green: founding members in 1995. (Today there are 153.)

")

4

Types of Blocs A.A group of countries that agrees to one or more of the following: 1.Reduce tariffs for certain goods [preferential trade area]. 2.Remove internal trade barriers [free trade area]. 3.Coordinate external trade barriers [customs union]. 4.Allow for the free movement of capital 5.Allow for the free movement of labor 6.Coordinate indirect tax policy 7.Coordinate regulatory & competition policies 8.Coordinate macroeconomic policies [economic union]. 9.Introduce a common currency [monetary union]. 10.Merge treasuries and fiscal policies [fiscal union]. 11.Coordinate foreign & defense policies [political union]. B.The European Union meets criteria 2-7 & 9 (8?). C.The NAFTA meets criteria 2 and 4. D.The Mercosur/Mercosul meets criteria 1-4. [single market]. [common market].

![Types of Blocs A.A group of countries that agrees to one or more of the following: 1.Reduce tariffs for certain goods [preferential trade area].](http://images.slideplayer.com/5/1600714/slides/slide_4.jpg "2.Remove internal trade barriers [free trade area]. 3.Coordinate external trade barriers [customs union]. 4.Allow for the free movement of capital 5.Allow for the free movement of labor 6.Coordinate indirect tax policy 7.Coordinate regulatory & competition policies 8.Coordinate macroeconomic policies [economic union]. 9.Introduce a common currency [monetary union]. 10.Merge treasuries and fiscal policies [fiscal union]. 11.Coordinate foreign & defense policies [political union]. B.The European Union meets criteria 2-7 & 9 (8 ). C.The NAFTA meets criteria 2 and 4. D.The Mercosur/Mercosul meets criteria 1-4. [single market]. [common market]..")

5

Trade Blocs Tend to Include Countries: At similar levels of development. Geographically close or adjacent. With similar trade regimes. Sharing a desire to organize regionally.

6

How Common are They? 1834: Zollverein, first modern trade bloc. There are 219 trade blocs presently in force, and registered with the WTO http://rtais.wto.org/UI/PublicAllRTAList.aspx 1990s: Trend towards continental-size blocs.

7

Main Trade Blocs

8

What are Trade Blocs, Really? People are very excited about trade blocs. Officially, an attempt to enhance trade. In reality, trade blocs destroy, divert, and create trade in complex ways. They can be an attempt to privilege insiders relative to outsiders.

9

NAFTA Only large trade bloc that includes both rich & developing countries: –Mexico is so far away from God, and… … –Very controversial (social dumping). Its a free trade area + free capital flows: –Origin & content rules are necessary. –Various unintended consequences/effects. External trade policies are not coordinated. Some product & environmental regulations. Trucking issue: first Mexican truck crossed the border in October 2011.

11

Automobile Assembly in Mexico (thousand units) TimelineNAFTAPeakNadirMost Recent 1994200020042010 Chrysler239408156257 Ford22626571393 GM161436141559 Honda019215 Nissan194313277506 Renault00110 VW256426225434 Toyota00054 Total107718689032260 % exported64%82% Sources: Automotive News; Asociación Mexicana de la Industria Automotriz.

TimelineNAFTAPeakNadirMost Recent Chrysler Ford GM Honda Nissan Renault00110 VW Toyota00054 Total % exported64%82% Sources: Automotive News; Asociación Mexicana de la Industria Automotriz.")

13

A maquila worker inserts electronic components at an assembly line for video turners, Tuesday, Nov. 18, 1998 at the Samsung Electromechanics plant in Tijuana, Mexico. Sprawled across a hillside on Tijuana's outskirts, Samsung's state-of-the- art manufacturing complex is a hive of activity, except for the cavernous blue-and-beige building on the campus' eastern edge. Built as part of a planned $400 million expansion, the empty building now serves only as a reminder of the long reach of the Asian financial crisis.(AP Photo/Damian Dovarganes)

.")

14

FTAs: Origin and Content Rules For a good to be sold duty-free anywhere within the FTA, it must exceed a minimum level of local content. For instance, in the NAFTA, an automobile is deemed to be North American if the percentage of local (i.e. within bloc) value attributable to 69 key components (e.g., engines, transmissions, bumpers) exceeds 62.5%.

value attributable to 69 key components (e.g., engines, transmissions, bumpers) exceeds 62.5%..")

15

A Sudden Devaluation In late 1995 and early 1996, over a period of 5 weeks, the Mexican peso lost 45% of its value relative to the dollar. What was the consequence of this change for companies wishing to comply with the 62.5% local content rule? How could they adapt to the new situation?

16

Economic Controversies Competitive implications: –Economies of scale. –Improved terms of trade (through either bargaining power or specialization): Welfare implications: trade creation, diversion, and destruction, depending on the characteristics of the bloc (FTA vs. CU, level of external tariff(s), etc.). Source: Edward D. Mansfield and Helen V. Milner, The New Wave of Regionalism. International Organization 53(3) (Summer 1999):589-627. p is price, q is quantity. X is exports, M is imports. c is the current period. 0 is the base period. i is the product.

: Welfare implications: trade creation, diversion, and destruction, depending on the characteristics of the bloc (FTA vs. CU, level of external tariff(s), etc.). Source: Edward D. Mansfield and Helen V. Milner, The New Wave of Regionalism. International Organization 53(3) (Summer 1999): p is price, q is quantity. X is exports, M is imports. c is the current period. 0 is the base period. i is the product..")

17

Political Controversies Domestic: –Who is in favor, and who is against? Exporters (L vs. K-intensive), import-competitors, consumers, investors, etc. –Justification for unpopular adjustment policies. International: –Pressures towards democratization (e.g. Spain, Portugal, Paraguay, etc.). –Enhanced power in multilateral trade negotiations. –Improved global governance. –Extension of influence over weaker states. Sources: Edward D. Mansfield and Helen V. Milner, The New Wave of Regionalism. International Organization 53(3) (Summer 1999):589-627; Andrew G. Brown, and Robert M. Stern, Free Trade Agreements and the Governance of the Global Trading System. The World Economy (2011):331-354.

, import-competitors, consumers, investors, etc. –Justification for unpopular adjustment policies. International: –Pressures towards democratization (e.g. Spain, Portugal, Paraguay, etc.). –Enhanced power in multilateral trade negotiations. –Improved global governance. –Extension of influence over weaker states. Sources: Edward D. Mansfield and Helen V. Milner, The New Wave of Regionalism. International Organization 53(3) (Summer 1999): ; Andrew G. Brown, and Robert M. Stern, Free Trade Agreements and the Governance of the Global Trading System. The World Economy (2011):")

18

Local Content Formula

19

Problem Set #2 Please work individually. Due in one week from today.

20

The Euro Cliffhanger: An Avalanche of Thrills

21

National Currencies: The Post Bretton Woods World Source: Reuven Glick and Andrew K. Rose, Contagion and Trade. Why are Currency Crises Regional?Journal of International Money and Finance 18 (1999):603-617.

:")

22

Monetary Unions # Members GDP 2007 $bn Economic and Monetary Union (Eurozone)1712,225 Economic and Monetary Community of Central Africa659 West African Economic and Monetary Union858 Overseas Issuing Institute (French Polynesia, New Caledonia, Wallis and Fotuna) 314 Organisation of Eastern Caribbean States64

1712,225 Economic and Monetary Community of Central Africa659 West African Economic and Monetary Union858 Overseas Issuing Institute (French Polynesia, New Caledonia, Wallis and Fotuna) 314 Organisation of Eastern Caribbean States64")

23

Source: Roel Beetsma and Massimo Giuliodori, The Macroeconomic Costs and Benefits of EMU and Other Monetary Unions. Journal of Economic Literature 48 (September 2010):603-641. The Governing Council makes decisions by majority vote.

: The Governing Council makes decisions by majority vote..")

25

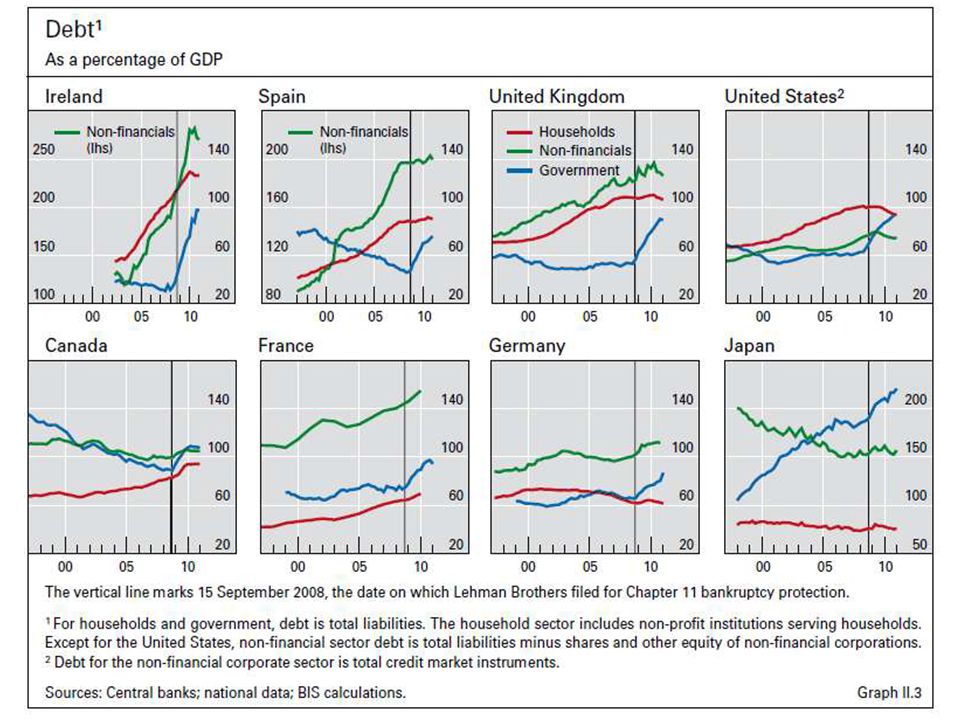

Consequences of Monetary Unions Member countries cannot print money to inflate their debt away. They cannot devalue the currency to regain competitiveness. In order for a monetary union to work: –Labor needs to be able & willing to move around in search of opportunities. –Fiscal union is advisable. Because members usually retain sovereignty, they usually do not get transfers to make up for revenue shortfalls or increased social spending during a crisis. Nota bene: Robert Mundell won the Nobel Prize for his work on optimal currency areas.

26

The Way it Was Supposed to Be The architects of the euro believed that a Greece-like problem would not occur because financial markets would have punished countries with excessive debt by raising the cost of borrowing. They didnt until the global financial crisis started. The European Central Bank (ECB): –Prohibits loaning money to service national debts. –Its no-bail-out clause discourages overspending. It did not. The Stability and Growth Pact should have prevented the situation from worsening: –Deficit/GDP 3% and Gross debt/GDP 60%. –It was not enforced, and in 2005 the rules were relaxed at the request of France and Germany. Source: Lorenzo Bini Smaghi, The Future of the Euro. Foreign Affairs (2010).

: –Prohibits loaning money to service national debts. –Its no-bail-out clause discourages overspending. It did not. The Stability and Growth Pact should have prevented the situation from worsening: –Deficit/GDP 3% and Gross debt/GDP 60%. –It was not enforced, and in 2005 the rules were relaxed at the request of France and Germany. Source: Lorenzo Bini Smaghi, The Future of the Euro. Foreign Affairs (2010)..")

27

CountryGDP Growth (%) Consumer Prices (%) Budget balance (% GDP) Debt stock (% GDP) Current account balance (% GDP) Unemployment (%) USA+1.6+3.9-9.1 62.3 -3.39.1 China+9.1+6.1-1.8 18.9 +4.06.1 Japan-1.1+0.2-8.3197.5+2.44.3 UK+0.6+5.2-8.876.1-2.08.1 Eurozone+1.6+3.0-4.2 … -0.510.0 Austria+3.5+3.8-3.6 71.0 +2.93.7 Belgium+2.3+3.6-3.8 100.9 +1.16.8 France+1.7+2.2-5.8 82.4 -2.59.9 Germany+2.8+2.6-1.7 83.2 +5.16.9 Greece-7.3+3.1-9.1 142.8 -9.616.5 Ireland+2.3+2.6-10.1 96.7 +0.614.3 Italy+0.8+3.1-3.7 119.1 -3.77.9 Holland+1.6+2.7-3.8 62.6 +7.45.6 Portugal-0.9+3.6-6.7 93.0 -8.412.1 Spain+0.7+3.1-6.5 60.1 -4.421.2

Consumer Prices (%) Budget balance (% GDP) Debt stock (% GDP) Current account balance (% GDP) Unemployment (%) USA China Japan UK Eurozone … Austria Belgium France Germany Greece Ireland Italy Holland Portugal Spain")

28

Labor Protections in the OECD Eurozone:199020002008Other OECD:199020002008 Austria 2.21 1.93 Australia 0.941.191.15 Belgium 3.152.18 Canada 0.75 Finland 2.332.091.96 Hungary 1.27 1.65 France 2.98 3.05 Japan 1.841.43 Germany 3.172.342.12 South Korea 2.742.031.90 Greece 3.50 2.73 Mexico 3.13 Ireland 0.931.11 Poland 1.40 1.90 Italy 3.572.511.89 Sweden 3.492.241.87 Netherlands 2.732.121.95 Switzerland 1.14 Portugal 4.103.673.15 Turkey 3.763.72 Slovakia …1.801.44 UK 0.600.680.75 Spain 3.822.932.98 USA 0.21 OECD average..2.001.94 Other countries: Brazil.. 2.75 Indonesia.. 3.68 Chile.. 2.65 Israel.. 1.37 China.. 2.65 Russia.. 1.92 India.. 2.77 South Africa.. 1.25 Note: The index is based on protections against dismissal for permanent employees, regulation of temporary employment, and requirements for collective dismissal. Source: OECD Employment Protection Legislation database.

30

Source: Adrian Blundell-Wignall and Patrick Slovik, The EU Stress Test and Sovereign Debt Exposures. (OECD, August 2010). EU Banks Exposure to Sovereign Debt

. EU Banks Exposure to Sovereign Debt.")

33

Counterparty Risk Nobody really knows how much because most instruments are traded over the counter. Estimates range between 4 and 100 or more billion of exposure to a Greek credit event. Hedging. CDSs. Naked CDSs.

34

Public Debt as % of GDP Note: Data after 2009 are projections. Source: IMF.

36

Net government lending (+) or net borrowing (-), % of GDP (Source: OECD) 199519961997199819992000200120022003200420052006200720082009 FranceCentral-5.28-4.09-3.54-2.91-2.09-1.67-1.69-3.29-4.15-3.48-2.77-2.15-2.33-2.89-7.28 Local-0.180.060.230.300.320.190.13 0.03-0.14-0.19-0.17-0.40-0.45-0.29 GermanyCentral-8.31-2.19-1.51-1.67-1.261.39-1.48-2.00-2.19-2.41-2.30-1.27-0.31-0.27-2.19 Länder-1.15-1.10-1.13-0.72-0.47-0.34-1.29-1.43-1.51-1.26-0.450.170.07-0.68 Local-0.21-0.030.010.220.270.26-0.05-0.23-0.33-0.11-0.010.120.400.31-0.17 GreeceCentral-9.14-6.70-5.95-3.88-3.19-3.73-4.58-4.83-5.75-7.28-5.30-5.94-6.66-9.57-15.46 Local0.070.050.060.050.090.000.140.000.04-0.14-0.05-0.11-0.05-0.03 HungaryCentral-8.87-4.75-5.52-7.15-5.14-2.75-4.19-8.07-7.06-6.12-7.40-8.57-4.90-3.77-3.99 Local0.140.38-0.02-0.300.00-0.270.11-0.87-0.16-0.28-0.55-0.81-0.110.07-0.37 IrelandCentral-2.24-0.291.262.212.454.911.430.040.111.291.412.720.24-7.03-14.23 Local0.190.18 0.060.16-0.13-0.48-0.340.300.110.240.23-0.22-0.27-0.15 ItalyCentral-7.48-6.56-2.49-2.83-1.19-0.72-2.82-2.20-3.09-2.57-3.52-2.34-1.33-2.35-4.88 Local0.06-0.40-0.19-0.24-0.59-0.14-0.28-0.81-0.45-0.99-0.85-0.15-0.33-0.37 JapanCentral-2.11-2.36-1.73-9.39-6.29-5.96-5.83-7.01-6.42-4.76-5.88-1.02-2.84-3.03 Local-2.86-2.51-2.24-2.43-1.60-0.89-0.90-1.31-1.28-0.72-0.270.01-0.10-0.01 MexicoCentral 0.030.360.420.110.06-2.41-0.90 State -0.070.25-0.050.11-0.51-0.19-0.28 Local 0.11-0.090.000.01-0.030.07-0.14 PolandCentral-3.40-3.75-3.57-3.29-1.43-2.62-4.81-4.58-5.81-5.48-3.94-3.38-1.93-3.50-6.20 Local-1.02-1.12-1.07-0.98-0.88-0.41-0.46-0.40-0.380.09-0.14-0.250.04-0.18-1.04 PortugalCentral-5.11-4.26-2.98-3.86-2.96-2.56-3.93-2.50-2.67-3.31-5.54-3.95-2.58-2.63-8.70 Local0.08-0.28-0.410.380.24-0.37-0.39-0.44-0.42-0.10-0.34-0.13-0.26-0.37-0.66 SpainCentral-5.82-4.22-3.09-2.86-1.25-0.580.020.130.50-0.291.311.982.43-2.04-8.56 CC.AA.-0.64-0.65-0.32-0.39-0.18-0.51-0.64-0.49 -0.07-0.29-0.04-0.22-1.62-1.98 Local-0.030.010.020.03-0.010.09-0.04-0.12-0.240.01-0.060.08-0.31-0.49-0.58 SwedenCentral-6.97-2.97-1.161.061.123.531.83-0.89-0.910.381.522.093.422.33-0.69 Local-0.35 -0.48-0.18-0.330.06-0.25-0.59-0.350.030.430.130.11-0.11-0.28 TurkeyCentral 1.01-0.76-1.10-5.94 Local -0.17-0.41-1.12-0.76 UKCentral-5.54-4.13-2.040.171.121.650.85-1.87-3.41-3.10-2.98-2.67-2.62-4.63-10.89 Local-0.38-0.13-0.14-0.27-0.20-0.30-0.27-0.110.10-0.27-0.360.02-0.06-0.26-0.40 USACentral-2.76-1.90-0.570.541.081.910.39-2.60-3.83-3.61-2.76-1.82-2.23-5.25-10.50 State-0.46-0.31-0.23-0.16-0.31-0.36-0.93-1.30-1.08-0.79-0.44-0.22-0.52-0.96-0.69

or net borrowing (-), % of GDP (Source: OECD) FranceCentral Local GermanyCentral Länder Local GreeceCentral Local HungaryCentral Local IrelandCentral Local ItalyCentral Local JapanCentral Local MexicoCentral State Local PolandCentral Local PortugalCentral Local SpainCentral CC.AA Local SwedenCentral Local TurkeyCentral Local UKCentral Local USACentral State")

37

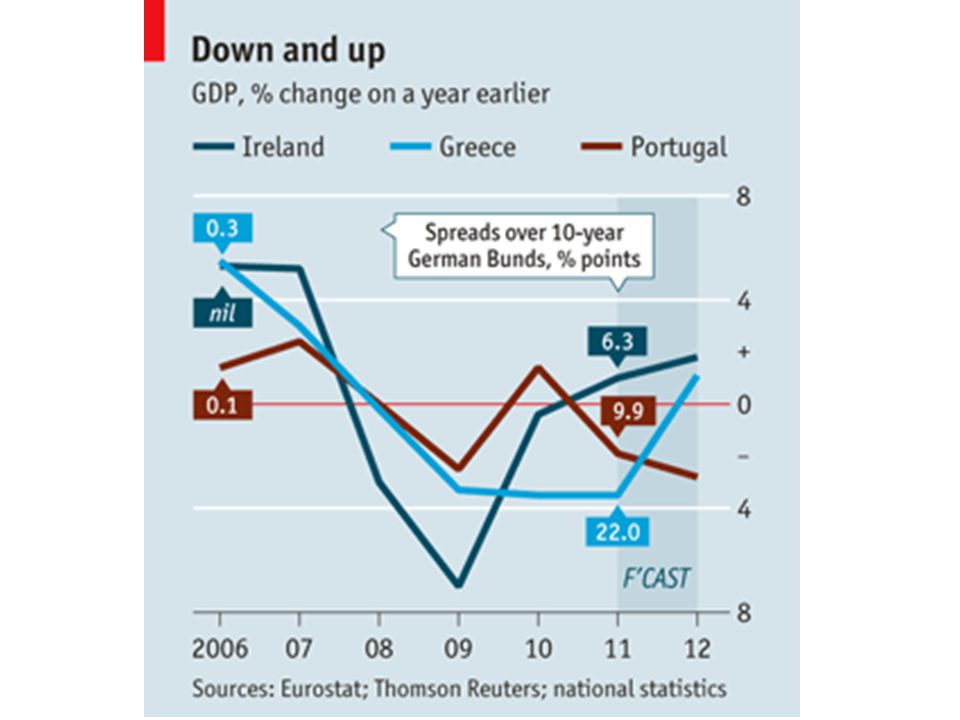

The PIIGS Source: IMF, World Economic Outlook (September 2011).

.")

38

Source: IMF, Global Financial Stability Report (September 2011).

.")

41

What Are Policymakers Doing? They are meeting…

42

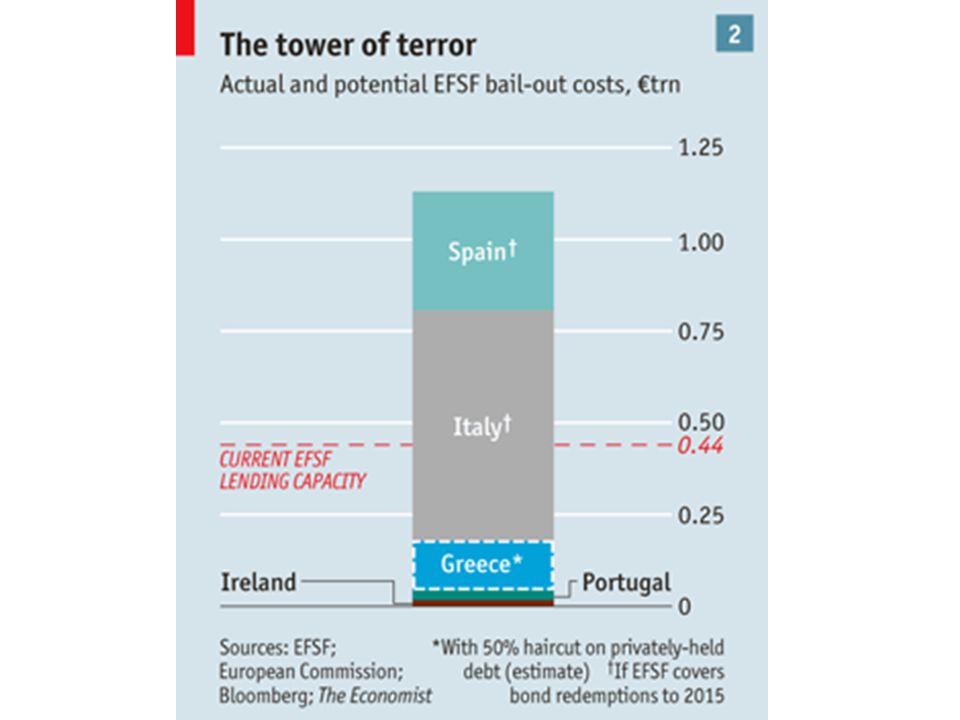

Only 440 in the fund. 100 IT+ES; 70 PIG. … and making some decisions…

45

The Euro Deal 27 October 2011 Greek debt: haircut of 50%. Bank recapitalization for 106 bn ($146 bn). Must reach 9% of tier 1 capital within 9 months. (But the calculations based on just 70 banks out of the 5,000 in the Euro Zone. Firewall: 1 trillion European Financial Stability Facility, but with just 20% equity. The rest to be raised through Special Purpose Vehicles issuing collateralized debt obligations (up to a ×5 leverage).

. Must reach 9% of tier 1 capital within 9 months. (But the calculations based on just 70 banks out of the 5,000 in the Euro Zone. Firewall: 1 trillion European Financial Stability Facility, but with just 20% equity. The rest to be raised through Special Purpose Vehicles issuing collateralized debt obligations (up to a ×5 leverage)..")

46

From The Economist, April 2-8, 2011. Europes Biggest Problem: Lack of Leadership

47

Claudio Barbaro (L), a member of the opposition FLI party, fought with Fabio Ranieri (R) from the Northern League in Italy's Parliament on 26 October 2011. Photo Reuters.

49

Is the Euro Good for Germany? Eurozone: 2/5 of German exports. The crisis in the periphery of the Eurozone has depressed the value of the euro. The DM would be overvalued nowadays. German firms benefited from the investment boom in the periphery. Large German firms in favor of bailouts; Mittelstand firms skeptical. The rate of inflation in Germany has been lower than with the DM. Reserves in > [DM + FFr + Guilders].

50

Is the Euro Good for Greece? Source: http://macrotragedy.blogspot.com/2011/10/greek-tradable-sector-odyssey.html

51

Greeces Exports Shipping services. Tourism. Apparel. Vegetables & fruit. Non-ferrous metals. Pharmaceuticals. Electrical equipment.

52

A White Knight?

54

Balance of Payments in 2010 (US$bn) ConceptFormula / NotationU.S.ChinaIndiaBrazil Gross Domestic ProductGDP14582587917292088 Trade balance in goods(Xg-Mg)-645.9+254.2-132.1+20.2 Trade balance in services(Xs-Ms)+145.8-22.1+41.2-30.8 Trade balance goods & services(X-M)-500.0+232.1-90.9-10.6 Net income from abroad(INF-IFF)+165.2+30.4-13.1-39.6 Net transfers from abroadZ-136.1+42.9+52.2+2.8 Current account(X-M) + (INF-IFF) + Z-470.9+305.4-51.9-47.4 Net capital transfers to/from abroadF-93.8+226.0+67.6+99.7 Net foreign loan (reserve change)SF-347.9 +471.7 +13.2+49.1 Capital accountF – SF+254.1-245.7+54.5+50.6 Statistical discrepancyAs reported by each government+216.8-59.7-2.6-3.2 Balance of payments(X-M) + (INF-IFF) + Z + F – SF = 00.0 Source: Re-calculated by M. Guillen with data reported by BEA, State Administration of Foreign Exchange, Central Bank of India, and Banco Central do Brasil.

55

Additional Slides on the Euro Cliffhanger

56

Source: Luc Laeven and Fabian Valencia, Systemic Banking Crises: A New Database. IMF WP 08/224. Frequency of Financial Crises Twin crisis = banking + currency. Triplet crisis = banking + currency + sovereign debt.

57

Source: Carmen M. Reinhardt and Kenneth S. Rogoff, This Times is Different. NBER WP 13882 (2008).

.")

58

G7 Sovereign Debt (% of GDP) Source: IMF, Long-Tern Trends in Public Finances in the G-7 Economies (2010).

Source: IMF, Long-Tern Trends in Public Finances in the G-7 Economies (2010).")

59

G7 Sovereign Debt (continued) Source: IMF, Long-Tern Trends in Public Finances in the G-7 Economies (2010).

Source: IMF, Long-Tern Trends in Public Finances in the G-7 Economies (2010).")

60

Bank Holdings of Sovereign Debt (Dec 2010)

")

61

Banks Capital Needs (adjusted for the impact of sovereign debt holdings, 2011)

")

62

Trust in the Banks

64

Were All Different… Italy is absolutely not in the same situation as Greece. Jean-Claude Trichet, head of the European Central Bank, April 9 What the Portuguese government wants the world to know is simpler: Portugal is not Greece. The Economist magazine, April 22 Portugal, Spain, Ireland or Italy are not in the same situation as Greece. And Belgium less yet. Guy Quaden, governor of the National Bank of Belgium, May 7 Ireland is no Greece confirms latest economic forecast. Ernst and Young, in its Economic Eye Summer Forecast, June 2010 "Greece is not Ireland; it doesnt have banking stability problems. George Papaconstantinou, finance minister of Greece, Nov. 8 Our economy is very different from that of Greece or Ireland because our financial sector has benefited by the supervision and regulation of the Bank of Spain, which was missing in Ireland. Elena Salgado, the Spanish finance minister in an interview in the British newspaper The Independent, Nov. 25 Bank failures in Ireland had nothing to do with Portugal. Ángel Gurría, secretary general of the OECD, in Bloomberg News, Nov. 22 Portugal does not need any help, it is in a very different situation to Ireland. Herman Van Rompuy, the president of the European Council, Nov. 23 Zapatero gets it and Spain is taking its medicine pre-emptively. Certainly, Spain faces serious economic growth and labor market challenges as it works its way through a devastating real estate collapse in the coming quarters. But it has neither the debt stock of Greece, the bust banks of Ireland or the complacent government of Portugal. Jacob Funk Kirkegaard, research fellow at the Peterson Institute of International Economics in a CNBC guest blog post, Nov. 24. Source: Landon Thomas, Jr., They are not like Ireland. Really. The New York Times (Nov. 27, 2010).

..")

65

… but Some Animals are More Different Than Others.

66

The Exorbitant Privilege of the Reserve Currency* * Term used by French Finance Minister Valéry Giscard dEstaing in the 1960s. Often misattributed to De Gaulle.

67

Balance of Payments in 2010 (US$bn) ConceptFormula / NotationU.S.ChinaIndiaBrazil Gross Domestic ProductGDP14582587917292088 Trade balance in goods(Xg-Mg)-645.9+254.2-132.1+20.2 Trade balance in services(Xs-Ms)+145.8-22.1+41.2-30.8 Trade balance goods & services(X-M)-500.0+232.1-90.9-10.6 Net income from abroad(INF-IFF)+165.2+30.4-13.1-39.6 Net transfers from abroadZ-136.1+42.9+52.2+2.8 Current account(X-M) + (INF-IFF) + Z-470.9+305.4-51.9-47.4 Net capital transfers to/from abroadF-93.8+226.0+67.6+99.7 Net foreign loan (reserve change)SF-347.9 +471.7 +13.2+49.1 Capital accountF – SF+254.1-245.7+54.5+50.6 Statistical discrepancyAs reported by each government+216.8-59.7-2.6-3.2 Balance of payments(X-M) + (INF-IFF) + Z + F – SF = 00.0 Source: Re-calculated by M. Guillen with data reported by BEA, State Administration of Foreign Exchange, Central Bank of India, and Banco Central do Brasil.

69

Currency Allocation of Reserves Upper: total Lower: emerging & developing countries Source: IMF.

70

Currency Allocation of Reserves (% of total) WorldDevelopedEmerging & Developing 19952011 Q219952011 Q219952011 Q2 USD59.060.254.263.671.956.5 Euro-26.7-24.9-28.7 Sterling2.14.22.12.62.15.9 DM15.8-16.1-14.8- FFr2.4-2.3-2.5- Guilders0.3- - - SFr0.30.10.2 0.70.1 Yen6.83.97.24.55.73.2 ECUs8.5-11.7-0.1- Source: IMF.

WorldDevelopedEmerging & Developing Q Q Q2 USD Euro Sterling DM FFr Guilders SFr Yen ECUs Source: IMF.")

71

Official Gold Holdings (10/2011) Source: World Gold Council. One ton of gold is worth about US$61 million. Gold Reserves Per Capita (2010):

:.")

72

Foreign Currency Reserves + Gold minus External Debt in 2010 Source: CIA Factbook (map from Wikipedia).

.")

73

Exchange Rates The nominal exchange rate. The real exchange rate = [/$] × [US inflation/EZ inflation]. The effective or trade-weighted exchange rate = weighted average of exchange rates of home and foreign currencies, with the weight for each foreign country equal to its share in bilateral trade.

74

Source: IMF, World Economic Outlook (September 2011). Index 2000=100, three-month moving average

. Index 2000=100, three-month moving average")

75

Source: http://macrotragedy.blogspot.com/2011/10/greek-tradable-sector-odyssey.html

76

Source: Multipolarity: The New Global Economy (The World Bank, 2011).

.")

77

Reserve Currency Store of value. Medium of exchange. Unit of account. Determinants: GDP, trade, price stability, and financial strength, both internal and external.

78

Benefits to the Issuing Country Convenience to its resident firms and individuals. Seigniorage (the exorbitant privilege): it allows running a large current account deficit and to accumulate debt at low interest rates. This is true during both boom and bust times. Geopolitical power, status, and prestige.

: it allows running a large current account deficit and to accumulate debt at low interest rates. This is true during both boom and bust times. Geopolitical power, status, and prestige..")

79

Costs to the Issuing Country The seigniorage effect makes the currency appreciate, which hurts exports. Vulnerability to the actions of foreign holders of assets denominated in the reserve currency. Burden of responsibility and leadership. Requires openness to capital flows.

80

Source: Multipolarity: The New Global Economy (The World Bank, 2011).

.")

81

Artist: Laura Gilbert. http://www.securitiesdocket.com/2008/10/04/the-zero-dollar-bill/

82

Source: Multipolarity: The New Global Economy (The World Bank, 2011).

.")

83

A Renminbi Currency Area?

84

Source: Multipolarity: The New Global Economy (The World Bank, 2011).

.")

88

Special Drawing Rights (SDRs) Supplementary foreign exchange reserve assets defined and maintained by the IMF. They represent a claim to currency held by IMF member countries. They are allocated to countries by the IMF. Created in 1969, initially at 1 SDR = $1. This week, 1 SDR = US$1.54. They are essentially a basket of currencies. There are 238.3 billion SDRs in existence, allotted to countries depending on their IMF quota.

89

More on SDRs They carry a weekly interest rate (a weighted average of short-term debt in the countries represented in the basket), but it is only paid to (from) a country if it holds more (less) than its allotted quota of SDRs. They are a unit of account used by many international agencies, including the IMF. Some countries peg their currencies to SDRs (nowadays only the Czech Rep. and Jordan). They can also be issued by private parties. China is interested in SDRs playing a more important role.

. They can also be issued by private parties. China is interested in SDRs playing a more important role..")

90

Value of 1 SDR Note: The basket of currencies that values the SDR could be re-evaluated sooner than 2015 if the IMF decides that the current basket no longer reflects "the relative importance of currencies in the worlds trading and financial systems.

91

Source: Multipolarity: The New Global Economy (The World Bank, 2011).

.")

Similar presentations

Grants Chapter 6.>")