Download presentation

Presentation is loading. Please wait.

1

GCC Macroeconomic Overview Click to continue

2

Founded in 1934, ISPI is one of the oldest and most prestigious international relations institutes in Italy, with its headquarters in Palazzo Clerici, Milan.Palazzo Clerici It is a private law association, granted the status of non-profit-making body in 1972, and operates under the supervision of the Ministry for Foreign Affairs. Where the management is concerned, it is under the control of the Ministry of Economy and Finance, and the State Auditors Court. ISPIs scientific output has always been distinguished by a sound pragmatic approach, based on monitoring the various geo-political areas and interpreting the major trends in progress on the global scene, so as to provide political and economic operators with reliable information and guidance. Its interdisciplinary nature is guaranteed by the close collaboration of specialists in economics, politics, law, history and strategic studies (from both academic and non-academic circles) and by partnerships with prestigious institutions and research centres all over the world. The Institutes activities branch out in four major directions: research (divided into Programs and Projects on specific geo-political areas or transversal themes), publications, career training and organization of events.research publicationscareer trainingorganization of events The public served is traditionally wide ranging: from students to representatives of the political and cultural world, from members of public administrations, international bodies and non-governmental organizations to the business community (who are still major interlocutors as well as important supporters of the Institute). In particular, ISPI has become the institute that makes the biggest contribution in Italy toforming tomorrows diplomats (over 20% of those admitted to the diplomatic career in the last 5 years are from ISPI) as well as young people wishing to work in international organizations, both governmental and non-governmental. ISPI stimulates debate on current affairs in the global scenario (every year over 1,600 students are involved in its training activities and 20,000 people take part in the events, organized especially in Milan, Turin and Rome). ISPI is moreover a major source of information and assistance for companies and institutions that intend to widen their horizons abroad, proposing material and organizing meetings on a specialist, ad hoc basis. In 2012 ISPI was included among the Best 100 Think Tanks worldwide (non-US) in "Global Go To Think Tanks Report" published by the University of Pennsylvania and scored a remarkable 34th place in the Best Policy Studies produced by a Think Tank category. "Global Go To Think Tanks Report" Click to continue

and by partnerships with prestigious institutions and research centres all over the world. The Institutes activities branch out in four major directions: research (divided into Programs and Projects on specific geo-political areas or transversal themes), publications, career training and organization of events.research publicationscareer trainingorganization of events The public served is traditionally wide ranging: from students to representatives of the political and cultural world, from members of public administrations, international bodies and non-governmental organizations to the business community (who are still major interlocutors as well as important supporters of the Institute). In particular, ISPI has become the institute that makes the biggest contribution in Italy toforming tomorrows diplomats (over 20% of those admitted to the diplomatic career in the last 5 years are from ISPI) as well as young people wishing to work in international organizations, both governmental and non-governmental. ISPI stimulates debate on current affairs in the global scenario (every year over 1,600 students are involved in its training activities and 20,000 people take part in the events, organized especially in Milan, Turin and Rome). ISPI is moreover a major source of information and assistance for companies and institutions that intend to widen their horizons abroad, proposing material and organizing meetings on a specialist, ad hoc basis. In 2012 ISPI was included among the Best 100 Think Tanks worldwide (non-US) in Global Go To Think Tanks Report published by the University of Pennsylvania and scored a remarkable 34th place in the Best Policy Studies produced by a Think Tank category. Global Go To Think Tanks Report Click to continue.")

3

GDP Growth The macroeconomic soundness of the GCC economies have been making them remarkably more resilient throughout the global economic crisis. In the last years, the Gulf monarchies have enjoyed high GDP growth rates, managed to control inflation, and boosted their fiscal policies and public current and investment spending. External Sector Thanks to the oil-prices peak of 2011 and 2012, the current account balance has showed record-high surplus, allowing the GCC states to further increase their foreign assets investment through their sovereign funds. Such external assets investment which should serve as a sufficient cushion to avoid an immediate breakdown of the fiscal balance in case of prolonged periods of weak oil prices Fiscal and Monetary Policy The monetary policy has remained expansionary, in line with the rates policy adopted by the currencies to which the Gulf currencies are pegged. This allowed banks to increase the local credit to the private sector, which has enjoyed good rates of growth. The remarkable increase of current public spending has added new long-term weights on the public budget and increased the breakeven prices. The decrease of the oil-prices witnessed during the first half of 2013 raises substantial uncertainties about the future sustainability of the GCC countries public budgets. Unemployment The growth rate of the non-oil private sector has proved insufficient to offset the growing number of young unemployed citizens, to whom entrepreneurs usually prefer cheaper and often better-qualified foreign workforce. Some Gulf monarchies have introduced organic programs – notably Saudi Nitiquaat programme – to increase the share of local workers in the private sector and further diversify their economies. Go to the Analysis

4

Overview In the last years, the GCC economies have been enjoying high growth rates. This effect has been facilitated by historically high oil prices and expanded oil production accompanied by expansionary fiscal policies. The main economic institutions predict a more limited growth for this year and the next, due to diminishing production after the peaks of 2011-2012 and decreasing oil prices. Nevertheless, the general outlook remains positive, although the persistent dependence on oil exports represents a significant risk for the macroeconomic stability of the Gulf monarchies. The real non-oil GDP is expected to drop from 7 percent in 2011 and from 6 percent in 2012 to 5,5 percent in 2013. The non-oil sector has witnessed remarkable rates of growth in the last years but has proven to be still too influenced by the oil-sector performances, especially in countries such as Saudi Arabia, Qatar and Kuwait, where the share of oil&gas exports still exceeds by 80 percent the total exports. Despite the prolonged expansionary fiscal policies and the record-low rates implemented in the GCC countries – in line with those applying to the anchor currencies for the regions exchange rate pegs – the inflation rates remain low due to the softening of food and real estate prices – the traditional inflation drivers in the region – with the food prices in most cases held down by increased subsidies and the real estate market still facing a supply overhang following the 2009 crisis. The budget expansionary policies implemented in the last years to offset the global economic crisis effects and the social turbulences sparked in 2011 by the Arab Spring have put pressure on the national budgets of the GCC countries, increasing the breakeven prices (the oil price level necessary to sustain the state expenditures without incurring in a budget deficit). The significant increase of current expenditure during the Arab Spring – mainly in the form of increased salaries, subsidies and public jobs – has limited the resources available for investment in economic diversification and in infrastructures projects. Furthermore, the increased expenditures may pose significant risks in case of prolonged stagnation of the global growth and the consequent additional drop of the oil prices under the red line of 100 dollar per barrel. In response to their exposure to oil prices uncertainties, in the past years the GCC countries have built up significant precautionary buffers in the form of huge amounts of external assets and low debt-on-GDP ratios. In 2012, the IMF estimated at about 1,6 trillion dollars the total external assets retained by the GCC countries in the world. Such buffers would easily sustain the national budgets in case of oil prices drop in the short and medium term, while may reveal insufficient in case of substantial and prolonged (a 30$ drop for more than a year) oil price fall, with some countries such as Saudi Arabia, Oman and Bahrain particularly exposed.

. The significant increase of current expenditure during the Arab Spring – mainly in the form of increased salaries, subsidies and public jobs – has limited the resources available for investment in economic diversification and in infrastructures projects. Furthermore, the increased expenditures may pose significant risks in case of prolonged stagnation of the global growth and the consequent additional drop of the oil prices under the red line of 100 dollar per barrel. In response to their exposure to oil prices uncertainties, in the past years the GCC countries have built up significant precautionary buffers in the form of huge amounts of external assets and low debt-on-GDP ratios. In 2012, the IMF estimated at about 1,6 trillion dollars the total external assets retained by the GCC countries in the world. Such buffers would easily sustain the national budgets in case of oil prices drop in the short and medium term, while may reveal insufficient in case of substantial and prolonged (a 30$ drop for more than a year) oil price fall, with some countries such as Saudi Arabia, Oman and Bahrain particularly exposed..")

5

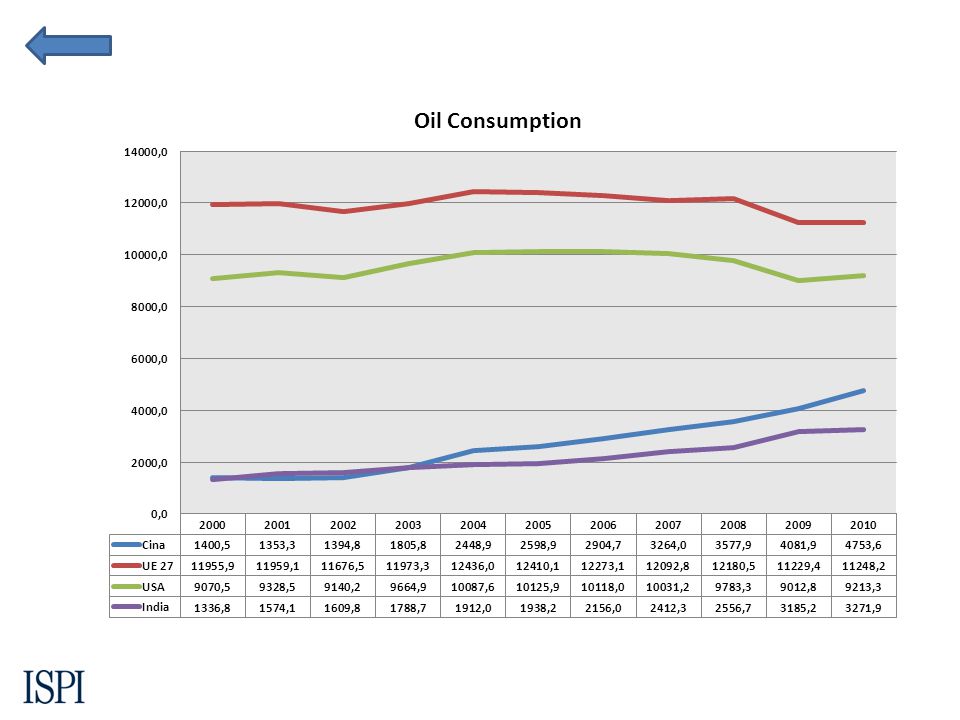

The Gulf moves Eastwards The Gulf region has been economically and culturally tied with Asia for thousands of years. After the Second World War, these ties witnessed a temporary backslash due to the particular geopolitical context provided by the Cold War and the Gulf monarchies political and economic dependence on their relations with the West. In that period the relations of the GCC states with the Asian continent were concentrated almost completely with allies of the United States such as South Korea and Japan. After the end of the Cold War, this situation has been slowly mutating. Since the beginning of the 1990s, China and India have been increasing their oil consumption to support their rapid economic growth. Especially China – which had been an oil net exporter until 1993 – began to dramatically increase its consumption at double-digit rates, a trend which has lasted for the last two decades and made Beijing the worlds second largest oil importer after the United States, with 5,42 barrel-per-day in 2012. The growing energy needs of the Asian giants have led these countries to rapidly intensify and strengthen their ties with the big oil&gas producers of the Gulf while, on the other side, the worsening of the Gulf monarchies ties with the West after the 9/11 attacks led their leaderships to look at Asia with a renewed interest. In the last 15 years, economic ties and political ties have been rapidly strengthening each other: Indian companies have been increasingly active in the GCC market, while a growing amount of Gulf investments has been directed towards India, especially after the signature of the Framework Agreement of Economic Cooperation between India and the GCC countries in 2004. The relations with China have gone beyond the simple intensification of the economic exchanges: a growing number of first-rank political contacts that have been established over the last two decades and culminated in the state visit of the Saudi King Abdallah bin Saud to Beijing, the first visit of a Saudi King to China and the first visit to a foreign country by the than just appointed monarch. In the last years, the GCC as a whole exported oil and petrochemical products to the major Asian powers three and a half times as much as the US and the European Union combined. Such trends are bound to increase in the coming years, sustained by the stagnant oil consumption in the EU area due to the economic crisis and the decreasing dependence of North America on energy commodities imports, caused by the growing shale-gas exploitation in the US. The IEA forecasts a decrease in the US imports from the Middle East of 1 million b/d (from 2.7 to 1.7) and of 300.000 b/d for the European Union within 2018 while Chinas and Indias imports are forecasted to increase by more than 1 milion b/d. If, on the one hand, the current eastward trend of the GCC trade is meant to grow in the forthcoming years, on the other hand, the GCC ties with the United States will remain central in the military and security fields due to the US armys overwhelming strategic superiority and the central role of the US in preserving the stability of the market and, with it, the stability of the still fragile world economy.

and of b/d for the European Union within 2018 while Chinas and Indias imports are forecasted to increase by more than 1 milion b/d. If, on the one hand, the current eastward trend of the GCC trade is meant to grow in the forthcoming years, on the other hand, the GCC ties with the United States will remain central in the military and security fields due to the US armys overwhelming strategic superiority and the central role of the US in preserving the stability of the market and, with it, the stability of the still fragile world economy..")

6

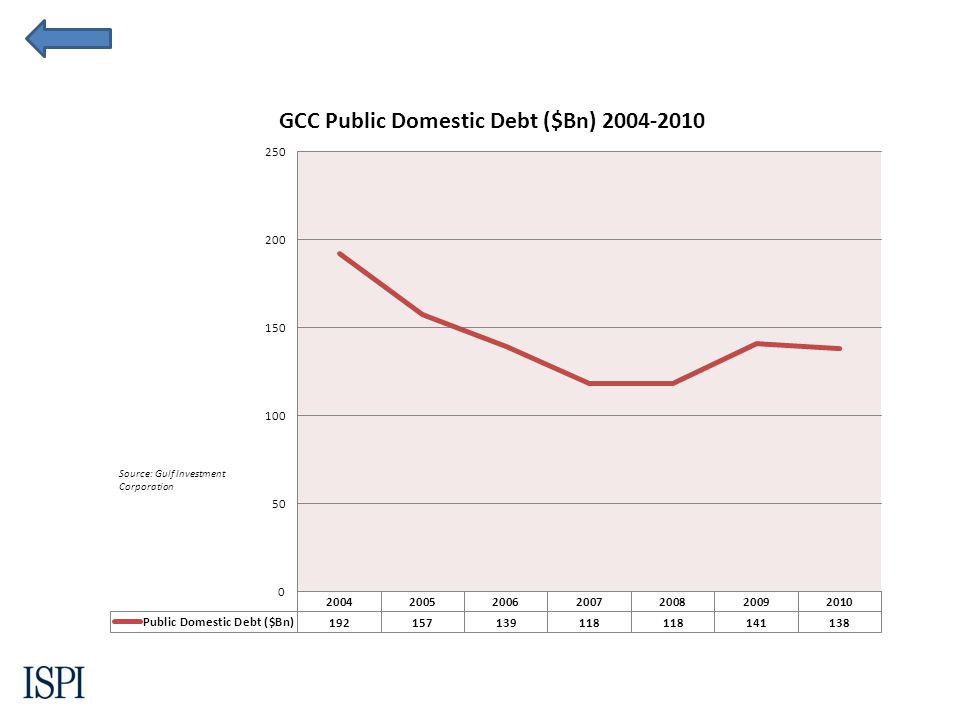

The Budget Risk The GCC countries have been constantly increasing budget expenditures in the last years. This peace was boosted in 2011 by the wave of protests that crossed the Arab world. In order to prevent unrest in their countries, the Gulf monarchies leaderships increased current and capital expenditures in different ways such as public sector wage increases, new state jobs, increased commodities and unemployment subsidies. New social housing plans have been launched, together with infrastructure projects for new schools and new hospitals. The new current expenditures and the new rises in public wages may curb investment and efforts in diversification plans and in the programs aimed at increasing public sector employment for nationals, which anyway will remain the main economic policy focus for the next years. Until now, the increased expenditures have been offset by a steady rise in oil&gas prices on which most of the GCC budgets depend. Almost all the budgets of the GCC have been further increased for 2013, in some countries by as much as 20% year on year. The slowdown of the oil prices forecasted for 2013-2014 may put under pressure the GCC balances, especially in the countries whose budgets are more exposed. The surpluses in the balance sheets will be narrowing in the all the Gulf monarchies, with some of them probably showing budget deficits in the next years such as Oman, Bahrain and Saudi Arabia. Inflation and Exchange rates Inflation in the last years has been curbed by the high level of commodities subsidies and the 2009 real estate bubble that decreased significantly the house prices, especially in the UAE. Real estate prices have started to rise again but the risks of a new bubble are significantly lower, due to the new set of bank and debt regulations which have been implemented in most GCC countries. The low commodities prices caused by the prolonged effects of the global economic crisis should support low inflation rates in the next years (around 3-4%). Risks of inflation upward pressure may arise from the programs aimed at increasing the private sector employment of nationals. The rising costs that these measures may encompass for private companies are likely to create an upward inflationary pressure on the consumption goods. The last two years have seen a substantial increase in private debt in countries such as UAE and Oman, which have been introducing several countermeasures to protect their credit systems. Loans have seen an upward trend due to the low interest rates caused by the Federal Reserve policies on the American dollar, to which all the GCC currencies are pegged. Despite the much-debated project of a GCC monetary union (which Oman and the UAE have already quit) it is difficult that concrete steps forward will be taken in the short-medium term.

. Risks of inflation upward pressure may arise from the programs aimed at increasing the private sector employment of nationals. The rising costs that these measures may encompass for private companies are likely to create an upward inflationary pressure on the consumption goods. The last two years have seen a substantial increase in private debt in countries such as UAE and Oman, which have been introducing several countermeasures to protect their credit systems. Loans have seen an upward trend due to the low interest rates caused by the Federal Reserve policies on the American dollar, to which all the GCC currencies are pegged. Despite the much-debated project of a GCC monetary union (which Oman and the UAE have already quit) it is difficult that concrete steps forward will be taken in the short-medium term..")

7

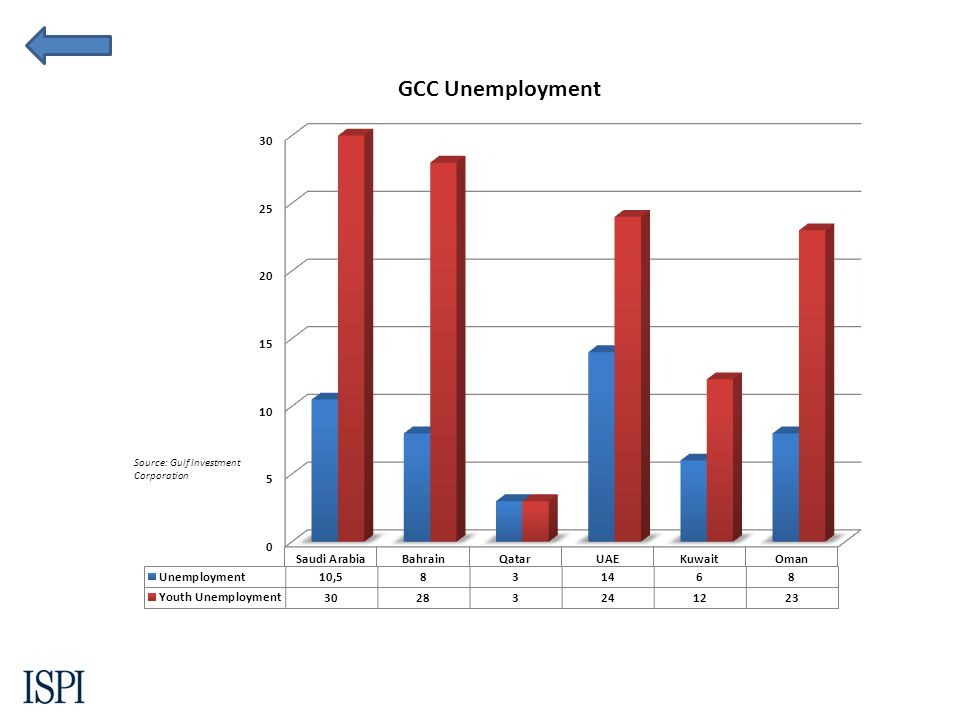

The Unemployment Issue The unemployment issue is crucial for the stability of the GCC economies. Their endowment consists mainly of oil and gas, which are both finite and technologically replaceable resources. In the last decades, the GCC countries have been pushing to diversify their economies, developing high-technology sectors such as aerospace, renewable technologies and IT, which all depend on high-skilled educated workforce. The downside of this process has been the massive inflow of foreign workers, a phenomenon that along the decades has changed the wages and skill composition of the GCC labour market. Foreigners amount to almost 70% of the total employed workers in the GCC; they nearly monopolize the private sector, while the nationals have been increasingly filling the public sector, whose wages are averagely more than 50% higher. The wages disparity problem has exacerbated since the spark of the Arab Awakening, during which the Gulf monarchies governments have increased salaries and benefits of the public employees in order to defuse the risks of social unrest in their countries. The impressive demographic growth which has affected the Gulf States in the last decades has made the youth unemployment a serious issue for the long-term social stability of these states. In order to absorb the young cohorts that are going to approach the labour market in the coming years, the GCC economies have to create almost 3.300.000 jobs. Since it is impossible for state budgets to keep on with the current trend of public-jobs creation, this new workforce has to be absorbed by the private sector. In order to achieve this objective, the GCC economies Unemployed/Private-Sector-Employed ratio (how many unemployed nationals there are for every employed in the private sector) – which now is close to 80 due to the overwhelming presence of foreigners – has to decrease dramatically. To tackle this major issue, some GCC countries have introduced special labour legislations aimed to substitute foreign workforce with locals. The main example has been the Nitiquaat programme introduced by the Saudi authorities, which has the explicit aim of Saudinaizing the national labour market. The authorities have been adopting measures such as setting compulsory minimum levels of national employees in the private firms workforce or strongly tackling the illegal foreign workers dwelling the kingdom. Nevertheless, the programme has had mixed results until now. The main problems are related to the much higher costs of the national workforce and its degree of education. The education system needs deep reforms to prepare the national youth to enter the labour market with competitive skills. In general, economy has to progress along the path of diversification to develop sectors that are much more labour intensive than the oil&gas. Nowadays the GCC economy has to grow by the impressive average of 6% per year to create the necessary number of new jobs. This is due to the scarce employment elasticity of the economic structures, a problem affecting every Gulf State at different degrees, depending on their achievements in their economic diversification programmes.

– which now is close to 80 due to the overwhelming presence of foreigners – has to decrease dramatically. To tackle this major issue, some GCC countries have introduced special labour legislations aimed to substitute foreign workforce with locals. The main example has been the Nitiquaat programme introduced by the Saudi authorities, which has the explicit aim of Saudinaizing the national labour market. The authorities have been adopting measures such as setting compulsory minimum levels of national employees in the private firms workforce or strongly tackling the illegal foreign workers dwelling the kingdom. Nevertheless, the programme has had mixed results until now. The main problems are related to the much higher costs of the national workforce and its degree of education. The education system needs deep reforms to prepare the national youth to enter the labour market with competitive skills. In general, economy has to progress along the path of diversification to develop sectors that are much more labour intensive than the oil&gas. Nowadays the GCC economy has to grow by the impressive average of 6% per year to create the necessary number of new jobs. This is due to the scarce employment elasticity of the economic structures, a problem affecting every Gulf State at different degrees, depending on their achievements in their economic diversification programmes..")

12

Source: APICORP

13

Source: Eurostat

15

Source: IEA

16

Source: NBK

17

Source: IMF

18

Source: Gulf Investment Corporation

Similar presentations

>")

Lecturer, University of Athens, Dpt. of Economics & Senior R&D Dpt.>")