Download presentation

Presentation is loading. Please wait.

1

Sean Walker, Managing Principal Ryan Merryman, Senior Manager

Using Data Analytics as a Management Tool to Identify Organizational Risks Sean Walker, Managing Principal Ryan Merryman, Senior Manager

2

Objectives Discuss how data analytics can be used to better identify various risks in an organization. Encourage you to use technology to protect the organization. Demonstrate the power of data analytics using a case study.

3

What and Why Data Analytics?

Data analytics is the process of accessing, normalizing, and modeling data with the intent of discovering useful information Often consider a forensic tool Much more can be learned about your organization Large organizations such as States process very large amount of data and often in a decentralized manner Risk of misappropriations Risk of management override of internal controls Risk of the unknown

4

Misconceptions It’s hard. It’s time consuming. It’s expensive.

It’s an audit tool. Get it done – Outsource it Get trained and get coached

5

Organizational Studies

What is normal for my organization? What is abnormal? Who is working in the system? When are they working in the system? Who is making all those journal entries? What systems feed information to the financial system?

6

Types of Risks and Areas of Analysis

Accounts Payable Fictitious vendors Fictitious, inflated and / or duplicate invoices Structured payments Conflicts of interest Kickbacks Bid-rigging Purchase Cards Duplicate purchasing and reimbursement schemes Unauthorized and/or improper purchases Unauthorized users Unauthorized SIC codes Payroll Ghost employees Improper supplemental payments Improper bonus or incentive compensation payments Inflated salaries Inflated hours Travel and Entertainment Expense False or inflated reimbursement submissions Improper use of corporate credit card Purchase for personal use Foreign Corrupt Practices Act Journal Entries Unbalanced journal entries Improper management override Improper expense capitalization Improper revenue recognition Entries to unusual or seldom used accounts Improper or unauthorized user activity Entries during non-business hours

7

Types of Risks and Areas of Analysis

Accounts Receivable Fictitious customers Lapping Credit balance fraud Offsets with unauthorized or improper expenses Improper AR aging Inventory Fictitious, inflated, duplicate or unnecessary purchases Theft through improper write-off Excessive shrinkage Revenue False or inflated sales Fictitious customers Improper commission or bonus payments Revenue recognition abuses including channel stuffing, liberal return policies or bill and hold schemes Non-Financial Weblog analysis Building access logs Computer print reports Client proprietary database analysis

8

State Specific Risks Internal control overrides General disbursements

Avoid purchase authority escalation Journal entries General disbursements Payroll Derived revenues (sales tax, etc.) Beneficiary payments Health and Human Service Grant payments

Beneficiary payments. Health and Human Service. Grant payments.")

9

State Pension Plan Brief Case Study

10

Cash Disbursement Testing: Objective - Test 3

Cash Disbursement Testing: Objective - Test 3.1 Million Payments Totaling $7.0 Billion Challenges faced by us: Each monthly report provided by the State: Was in a massive .pdf “print report” format, each monthly files was approximately 15,000 pages There were 3.1 Million payments in FY 2013 The files were too large to print and so large they crippled laptops 123 ft 360,000 pages 6 ft

11

Cash Disbursement Testing: The Monthly Report was Over 15,000 Pages

12

Most Systems Provide Data in a Usable Form

Time and Effort Most Systems Provide Data in a Usable Form

13

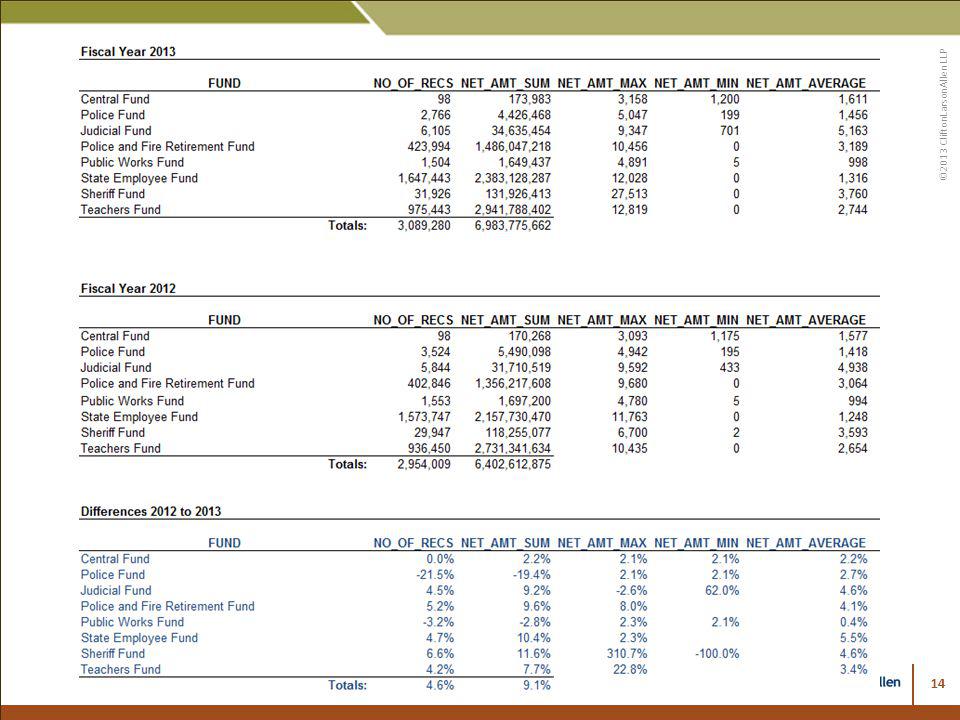

Cash Disbursement Testing: Understanding the Data and Year over Year Comparisons

We were able to analyze the files and compare activity from FY 2013 to FY 2012

15

Benford’s Analysis FY 2013 FY 2012

16

Stratification by Payment Amount

FY 2013 FY 2012

17

Cash Disbursement Testing: Abnormal Payments

Specific Analysis that would be difficult/impossible without Forensic Data Analysis: Payees whose payments amounts varied significantly

18

Cash Disbursement Testing: Specific Analytics

Specific Analysis that would be difficult/impossible without Forensic Data Analysis: Retirement Numbers that had more than one name associated

19

Cash Disbursement –Data Analysis vs. Traditional Procedures

Imported 100% of data Reconciled totals to F/S for Completeness Testing Summary Results that tie to F/S balances and compared to PY Run specific queries from which to make Risk Based selections for test work More efficient - Analysis FY 2013 procedure took only about 60% of the time of FY 2012 Traditional Procedure Random Sampling No Completeness Testing Less efficient

20

Consider How much data is collected in your organization?

How quickly can you analyze the data for management decisions and internal risks? As Comptroller’s do you believe you have your hands around all the state’s transactions?

21

Sean M. Walker, CPA, CGFM, CGMS Managing Principal State and Local Government Ryan Merryman, CPA/CFF/CITP, CFE Senior Manager Forensic Services

Similar presentations

>")