Download presentation

Presentation is loading. Please wait.

1

The Time Value of Money Chapter 5

2

LEARNING OBJECTIVES 1. Explain the mechanics of compounding when invested. 2. Present value and future value. 3. Ordinary annuity and its future value. 4. An ordinary annuity and an annuity due. 5. Non-annual future or present value of a sum . 6. Determine the present value of a perpetuity.

3

Power of time of value of money

History of Interest Rates $1000 ( )400 = ?

400 =")

4

Power of time value of money

Money Angles: by Andrew Tobias. 1. Chessboard with the King 2. Manhattan

5

Terms Compound Interest Future value and Present Value Annuities

Annuities Due Amortized Loans Compound Interest with Non-annual Periods Present Value of an Uneven Stream· Perpetuities

6

COMPOUND INTEREST FV1=PV (1+i) (5-1)

Where FV1=the future value of the investment at the end of one year i=the annual interest (or discount) rate PV=the present value, or original amount invested at the beginning of the first year

rate. PV=the present value, or original amount invested at the beginning of the first year.")

7

Future value 1. Simple compounding 2. Complex compounding

9

Future value

10

FV1=PV (1+i) =$100(1+0.06) =$100(1.06) =$106

=$100(1+0.06) =$100(1.06) =$106")

11

Compound twice a year

12

Compound four times a year

13

Compound 12 times a year

14

Compound 360 times a year

15

Continuous compounding

16

Illustration of Compound Interest Calculations

Year Beginning Value Interest Earned Ending Value $ $ $106.00

20

Future value and future value interest factor

21

FVn=PV(FVIFi,n)

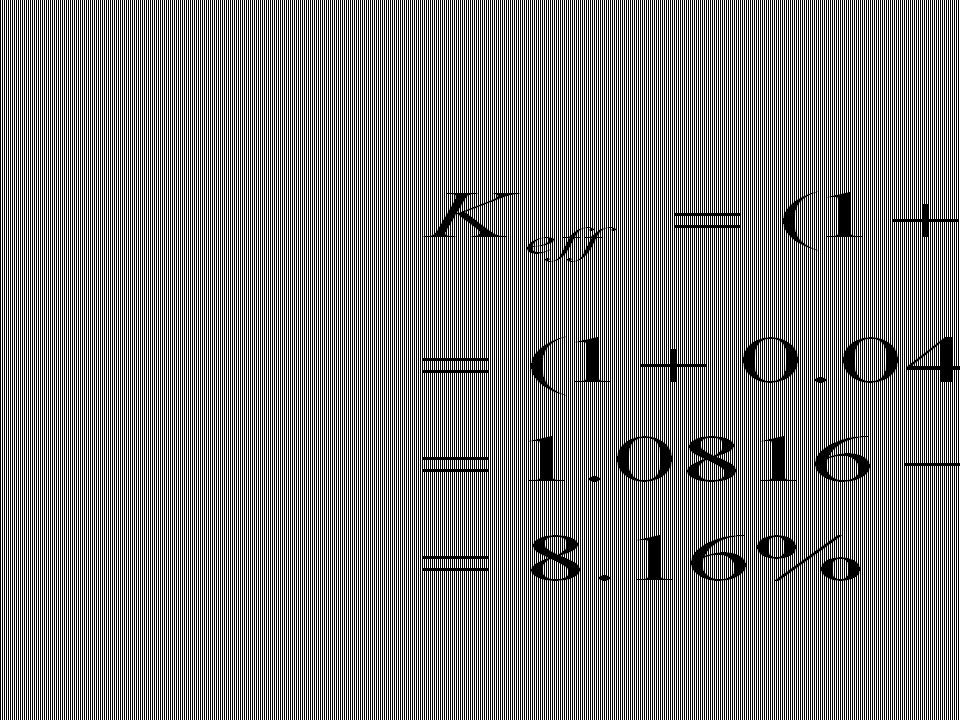

")

22

FVIFi,n or the Compound Sum of $1

Table 5-2 FVIFi,n or the Compound Sum of $1 N % % % % % % % % % %

23

PV=$300, Vn=$774; i=9 % N= ?

24

PV=$100; FVn=$179.10; n=10 years. I= ?

25

PRESENT VALUE

26

FV10=$500, n=10, i=6 % PV = ?

27

(PVIF i, n) (PVIF i, n) = 1/(1+i)

present-value interest factor for I and n (PVIF i, n), (PVIF i, n) = 1/(1+i)

, (PVIF i, n) = 1/(1+i)")

28

Present value FV10 =$1,500 N= 10 years discount rate= 8 %

PV=$1500(0.463) =$694.50

=$")

29

PVIFi,n or the Present Value of $1

Table 5-3 PVIFi,n or the Present Value of $1 N % % % % % % % % % %

30

ANNUITIES Annuity: equal annual cash flows.

Ordinary annuity: at the end of each period. Annuity due: at the beginning of each eriod.

31

Table 5-4 Illustration of a Five-Year $500 Annuity Compounded at 6 percent YEAR DOLLAR DEPOSITS AT END OF YEAR $500.00 530.00 562.00 595.50 631.00 Future value of the annuity $2,818.50

33

Ordinary annuity FVIFAk,n = [(1/k) ( (1+ k)n – 1)]

![Ordinary annuity FVIFAk,n = [(1/k) ( (1+ k)n – 1)]](http://slideplayer.com/slide/1425454/4/images/33/Ordinary+annuity+FVIFAk%2Cn+%3D+%5B%281%2Fk%29+%28+%281%2B+k%29n+%E2%80%93+1%29%5D.jpg "Ordinary annuity FVIFAk,n = [(1/k) ( (1+ k)n – 1)]")

34

Present value of an Annuity

35

Table 5-6 Illustration of a Five-Year $500 Annuity Discounted to the Present at 6 percent YEAR Dollars received at the the end of year $471.50 445.00 420.00 396.00 373.50 PV annuity $2,106.00

36

PVIFAK,n = (1/k) [( 1 – 1/(1+k)n]

![PVIFAK,n = (1/k) [( 1 – 1/(1+k)n]](http://slideplayer.com/slide/1425454/4/images/36/PVIFAK%2Cn+%3D+%281%2Fk%29+%5B%28+1+%E2%80%93+1%2F%281%2Bk%29n%5D.jpg "PVIFAK,n = (1/k) [( 1 – 1/(1+k)n]")

37

PVIFi,n or the Present Value of an Annuity of $1

Table 5-7 PVIFi,n or the Present Value of an Annuity of $1 N % % % % % % % % % %

38

n=10 years, I=5 percent, and current PMT=$1,000

PV= $1,000(7.722) = $7,722

= $7,722.")

39

PMT Annuity: $5,000, n =5 years, i=8 percent, PMT:?

40

AMORTIZED LOANS

41

Loan Amortization Schedule Involving a $6,000 Loan at 15 Percent to Be Repaid in Four Years

Year Annuity Interest Portion Repayment of Outstanding Of The Annuity The Principal Loan Balance Portion Of The After The An- Annuity nuity Payment $2, $ $1, $4,798.42 , , ,416.60 , , ,827.51 , ,827.51

42

ANNUITIES DUE FVn (annuity due)=PMT(FVIFA I,n)(1+I) (5-10)

FV5=$500(FVIFA5%,5)(1+0.06) =$500(5.637)(1.06) =$2,987.61 from $2,106 to $2,232.36, PV=$500(PVIFA6%,5)(1+0.06) =$500(4.212)(1.06) =$2,232.36

(1+0.06) =$500(5.637)(1.06) =$2, from $2,106 to $2,232.36, PV=$500(PVIFA6%,5)(1+0.06) =$500(4.212)(1.06) =$2,")

43

End of year principal(5)

End year Loan payment (1) Beginning principal (2) payments End of year principal(5) [(2) -(4)] Interest(3) [0.1 × (2)] Principal(4) [(1) - (3)] 1 $ $ $600.00 $ $ 2 $470.73 $ $ 3 $328.53 $ $ 4 $172.10 $

Beginning principal. (2) payments. End of year principal(5) [(2) -(4)] Interest(3) [0.1 × (2)] Principal(4) [(1) - (3)] 1. $ $ $ $ $ $ $ $ $ $ $ $ $")

44

The Value of $100 Compounded at Various Intervals FOR 1 YEAR AT i PERCENT

Compounded annually $ $ $ $115.00 Compounded semiannually Compounded quarterly Compounded monthly Compounded weekly (52) Compounded daily (365)

Compounded daily (365)")

45

PRESENT VALUE OF AN UNEVEN STREAM

YEAR CASH FLOW YEAR CASH FLOW $

46

Present value of $500 received at the end of one year

= $500(0.943) = $471.50 2. Present value of $200 received at the end of tree years = $200(0.890) = 3. Present value of a $400 outflow at the end of three years = -400(0.840) = 4. (a) Value at the end of year 3 and a $500 annuity, years 4 through 10 = $500 (5.582) = $2,791.00 (b) Present value of $2, received at the end of year 3 = 2,791(0.840) = 2,344.44 5. Total present value = $2,657.94

= $ Present value of $200 received at the end of tree years. = $200(0.890) = Present value of a $400 outflow at the end of three years. = -400(0.840) = (a) Value at the end of year 3 and a $500 annuity, years 4 through 10. = $500 (5.582) = $2, (b) Present value of $2, received at the end of year 3. = 2,791(0.840) = 2, Total present value = $2,")

47

Quiz 1 Warm up Quiz. Terms:

: n = 5, m = 4, I =12 percent, and PV =$100 solve for fv

48

Quiz 2 What is the present value of an investment involving $200 received at the end of years 1 through 4, a $300 cash outflow at the end of year 5 to 8, and $500 received at the end of years 9 through 10, given a 5 percent discount rate?

49

Quiz 3 A 25 year-old graduate has his $50,000 salary a year. How much will he get when he reaches to 60 (35 years later)year-old with a value rate of 8%(annual compounding). The graduate will have his $80,000 salary at age of 30. How much will he get when he reaches to his age of 60(30 years later) with the value rate of 8%(semi-annual compounding).

year-old with a value rate of 8%(annual compounding). The graduate will have his $80,000 salary at age of 30. How much will he get when he reaches to his age of 60(30 years later) with the value rate of 8%(semi-annual compounding).")

50

Quiz 4 The graduate will have his $100,000 salary at age of 40. How much will he get when he reaches to his age of 60(20 years later) with the value rate of 12%(quarterly-annual compounding). Compute the future value from 25-30/30-40/40-60 year old with the same rate and the compounding rate.

with the value rate of 12%(quarterly-annual compounding). Compute the future value from 25-30/30-40/40-60 year old with the same rate and the compounding rate.")

51

PERPETUITIES $500 perpetuity discounted back to the present at 8 percent? PV = $500/0.08 = $6,250

52

Power of time of value of money

History of Interest Rates $1000 ( )400 = ?

400 =")

53

Power of time value of money

Money Angles: by Andrew Tobias. Chessboard with the King Manhattan

Similar presentations

YOU 1 x 1 = 1 x 10 =10 1 x 1 = 1 x 3 =3 1 x 1 = 1 x 2.75 =2.75 1 x 1 = 1 x 2.50 =2.5 1 x 1 = 1 x 2 =2 1 x 1 = 1.>")

Demonstration Workshop Brussels, 26.11.2008.>")

Geometry (29%)>")