Download presentation

Presentation is loading. Please wait.

1

A New World of Finance: Business Rates & Beyond Rob Whiteman Chaired by Cllr David Borrow

2

cipfa.org Anticipating Comprehensive Spending Review Rob Whiteman CEO, CIPFA e: rob.whiteman@cipfa.org / t: @robwhitemanrob.whiteman@cipfa.org

3

cipfa.org Outline: Funding - impact of CSR cuts to date Protected vs Unprotected Who are the winners / losers within local government? Key battleground areas going forward CSR projections (25 th November) Where does that leave us?

Where does that leave us .")

4

cipfa.org Funding context Only part way through the cuts Real-terms cuts in non-protected services of £19bn (12.6%) between 2015- 16 and 2019-20 (38.1% since 2010-11) Not much room for under-delivery, only planning to achieve balanced budget in 2012-21 Real-terms protection for NHS - but unlikely to be sufficient for growing needs / demography Significant cash-terms cuts in local government funding

between and (38.1% since ) Not much room for under-delivery, only planning to achieve balanced budget in Real-terms protection for NHS - but unlikely to be sufficient for growing needs / demography Significant cash-terms cuts in local government funding")

5

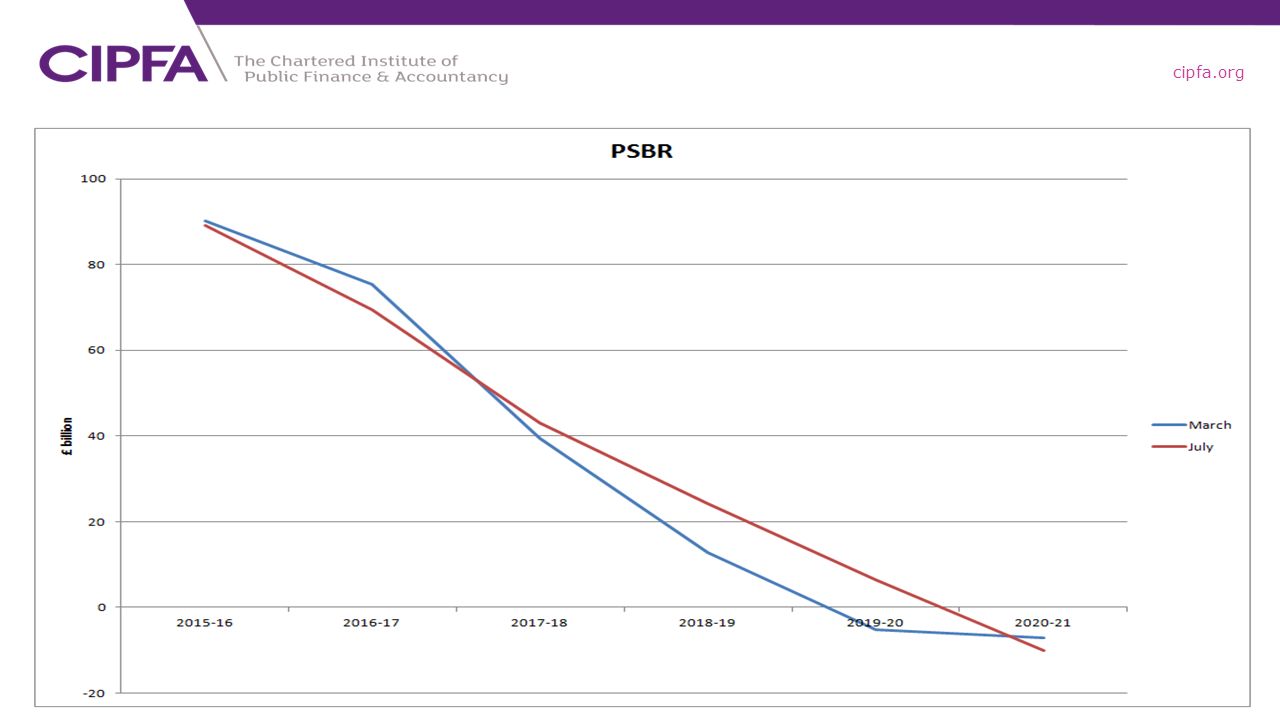

cipfa.org Good news, bad news Position and forecast for funding for services has actually improved - looked worse in Autumn Statement 2014. Allegations that some public services going back to the 1930s. March 2015 Budget projection looked very challenging; “big dipper” effect looked odd; expected a flatter profile. July Budget is both flatter and reflects the improved economic position (OBR). Flat in cash terms in July Budget – but includes protected services, additional NHS commitment, and likely new burdens (childcare).

. Flat in cash terms in July Budget – but includes protected services, additional NHS commitment, and likely new burdens (childcare)..")

6

cipfa.org

8

Protected services More than half DEL is spent on protected services Government commitments: NHS - £10bn increase in real terms by 2020-21 MOD – increase by 0.5% per year in real terms Schools – protect per-pupil funding International Development – spend 0.7% of GNI Ramps-up required cuts in other services

9

cipfa.org Protected services

10

cipfa.org

11

Estimated cuts to LG funding

12

cipfa.org Unprotected services HMT has asked departments to exemplify savings of 25% and 40% Consistent with CIPFA estimates (12% in 2016-17 and 2017-18, 6% in 2018-19 and 2019-20) Who will get below-average cut in funding?

Who will get below-average cut in funding")

13

cipfa.org Key battleground: social care Social care spending decreased by £1.6bn over last 5 years Real-terms cut estimated at £4.6bn, of which, demographic pressures (£1.75bn) and price increases (£1.25bn) Reduction in preventative spending for first time in 2015-16 Continuing reduction in the number of people receiving social care support

and price increases (£1.25bn) Reduction in preventative spending for first time in Continuing reduction in the number of people receiving social care support")

14

cipfa.org

15

Local authority financial failure? Warning signs? And who is checking? Financial failure or service failure first? Taking action – Section 25 robustness of estimates; Section 114 deficits Some authorities more exposed than others: Social care/ children’s services – demand-led services Reliant on Government grant rather than local taxation, and no growth in tax base Developing an index – next slide

16

cipfa.org Local authority financial risk measures

17

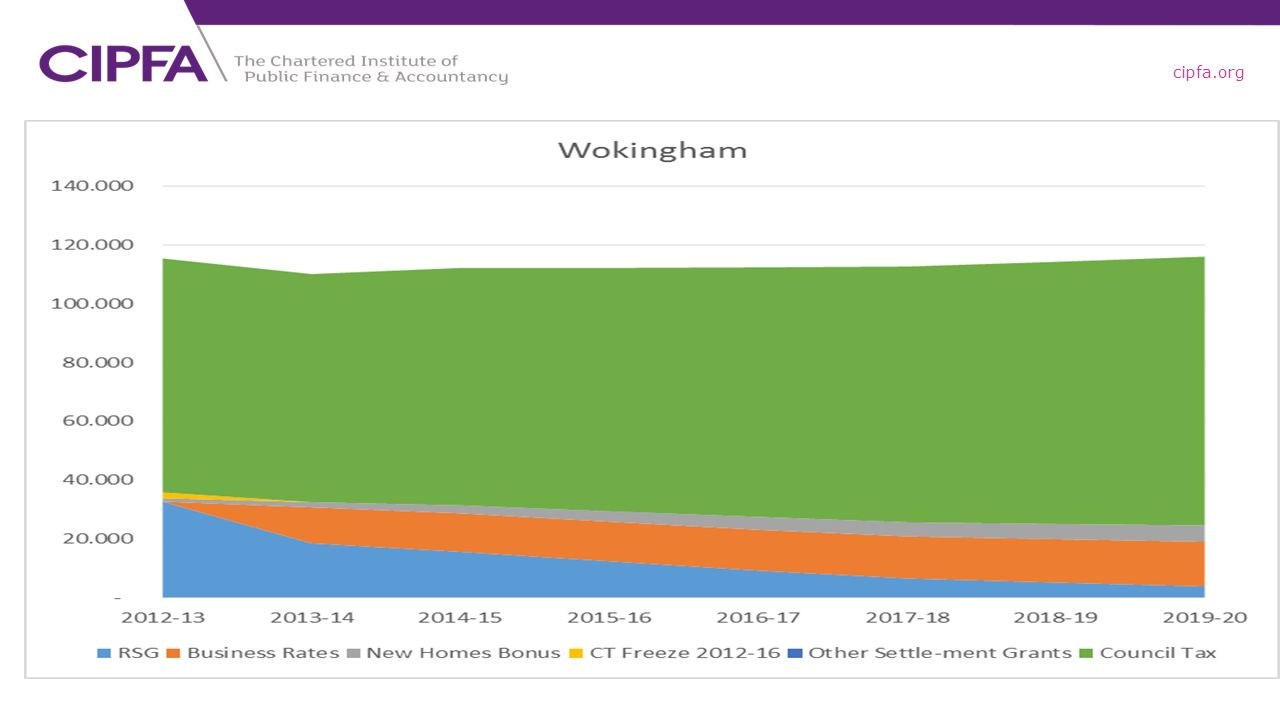

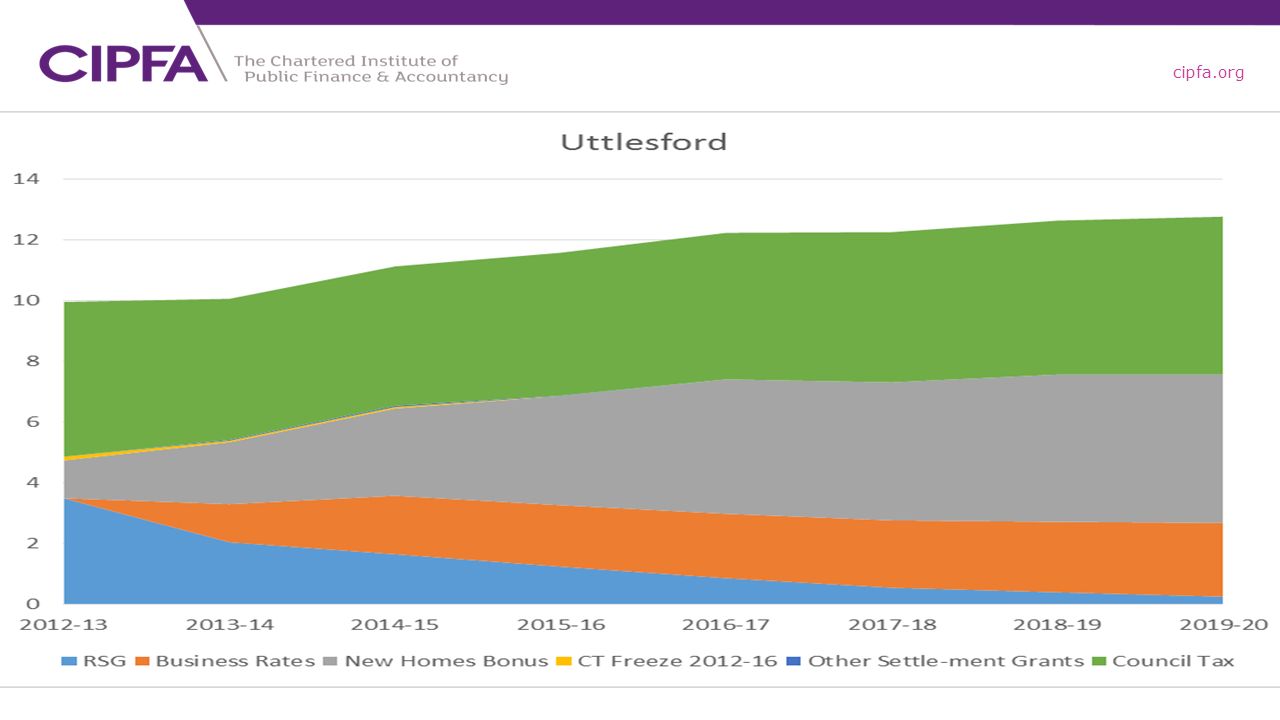

cipfa.org Distribution between authorities Major redistribution of resources since 2010 Greater weight placed on local taxation and incentives Some anomalies remaining in funding formula (pre-2010 settlement not tackled – e.g. damping) Some authorities have had increases in spending power; others 10% year-on-year cuts in spending power

Some authorities have had increases in spending power; others 10% year-on-year cuts in spending power.")

18

cipfa.org

21

100% business rates retention Chancellor announced plans to increase LG retention of business rates from 50% to 100% by end of parliament Has numerous technical challenges – but not new money Will favour those with largest business rates growth (and lowest needs)

")

22

cipfa.org Key messages re funding reality Local Government is not a priority Protected services will continue to take a bigger percentage of spend and put more pressure on unprotected areas NHS likely to overspend and break vote allocation Welfare reform impact – after House of Lords vote? RSG likely to end by end of this parliament The longer term may see benefits of devolution, rate retention and integration Short to medium term there is no good news – Sorry!

23

cipfa.org Financial reform Really exciting times – localism, regional tax, business growth retention Need to know more on mechanics, redistribution/ equalisation plans How will grant changes and new burdens impact? Councils must forecast, plan and look for more radical options to balance the books Full fiscal autonomy is key, but so too a balance between Localism and Fairness Far greater risk of insolvency and s114 notices than ever before My Advice: Don’t spend your reserves!

Similar presentations