Download presentation

Presentation is loading. Please wait.

1

FUND BASED FACILITIES CONTINUED

2

Bridge Financing ► Accommodation for the interim period. ► To bridge the gap to meet an urgent need of customer. ► Markup is charged. Consortium Financing Consortium Financing or Participation Loan is an arrangement where a number of banks join together to arrange funds for the borrower. ► To disperse the risk. ► Against a common security. ► A consortium agreement is drawn specifying the mode of sharing risk and remuneration.

3

RUNNING FINANCE Normally a business loan. Normally a business loan. This meets the days to day requirements of the customer. This meets the days to day requirements of the customer. Mark-up is charged on the utilized amount. Mark-up is charged on the utilized amount. It is granted against hypothecation of stocks. It is granted against hypothecation of stocks. Mark-up is charged on quarterly basis. Mark-up is charged on quarterly basis.

4

CASH FINANCE Normally a business loan. Normally a business loan. This meets the seasonal requirements of the customer like sugar & cotton. This meets the seasonal requirements of the customer like sugar & cotton. Mark-up is charged on the utilized amount. Mark-up is charged on the utilized amount. It is granted against pledge of stocks depending upon the nature of the goods. It is granted against pledge of stocks depending upon the nature of the goods. Mark-up is charged on quarterly basis. Mark-up is charged on quarterly basis.

5

DEMAND FINANCE Normally a business loan. Normally a business loan. This meets the requirements of the BIG customer to setup factories like sugar & cotton. This meets the requirements of the BIG customer to setup factories like sugar & cotton. Mark-up is charged on the full amount. Mark-up is charged on the full amount. It is granted against mortgage of fixed assets. It is granted against mortgage of fixed assets. Mark-up is charged on bi-annual basis. Mark-up is charged on bi-annual basis.

6

Purchase & Discounting of Bills Types: i.Documentary Bills of Exchange ii.Clean Bills of Exchange And i.Demand Bills ii.Time or Usance Bills Bills Purchased: ► A financing facility against a suitable margin of security ► Bank holds the bill as security till the time it gets mature. ► Bank does not becomes the purchaser or owner of the bill.

7

Bills Discounted: ► For Usance & Sight Bills. ► Given to only selected customers ► Discount is being deducted before grant of value

8

NON-FUND BASED FACILITIES

9

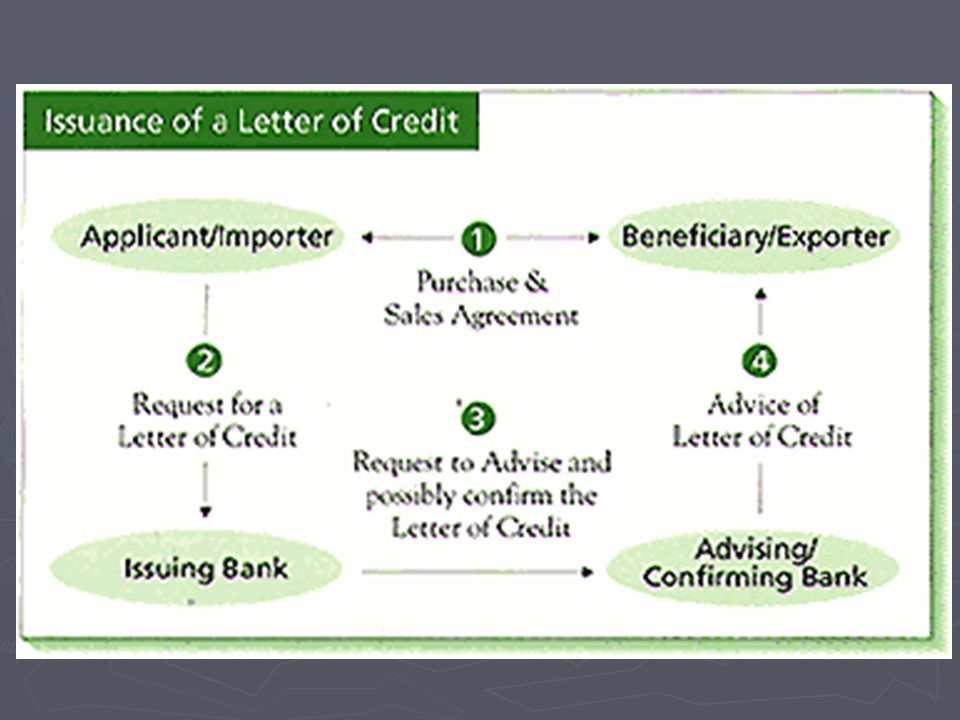

Letter of Credit An L/C An L/C is a written undertaking by a bank (issuing bank) given to the seller (beneficiary) at the request, and in accordance with the buyer’s (applicant) instructions to effect payment — that is by making a payment, or by accepting or negotiating bills of exchange (drafts) — up to a stated amount, against stipulated documents and within a prescribed time limit. Parties to L/C: The Applicant (importer) Opening Bank or Issuing Bank Advising Bank Beneficiary (Exporter) Confirming Bank Negotiating Bank Reimbursing Bank

Opening Bank or Issuing Bank Advising Bank Beneficiary (Exporter) Confirming Bank Negotiating Bank Reimbursing Bank.")

11

1. 1. Application & Agreement 2. 2. Issuance of the Letter of Credit 3. 3. Advising L/C i. i. Draft ii. ii. Commercial Invoice iii. iii. Bill of Lading iv. iv. Air Waybill v. v. Insurance Policy or Certificate vi. vi. Certificate of Origin vii. vii. Inspection Certificate viii. viii. Packing List 4. 4. Shipment of Goods 5. 5. Presentation of Documents by Beneficiary 6. 6. Sending Documents to the Issuing Bank 7. 7. Delivering Documents to the Applicant

13

Types of Documentary Credit: ► Revocable L/C ► Irrevocable L/C ► Irrevocable Confirmed L/C ► Revolving Credit ► Transferable Credit ► Back to Back Credit ► Red Clause or Packing Credit ► Stand by Credit Modes of Payment: ► L/C available by Negotiation ► L/C available by Acceptance ► L/C available by Sight Payment ► L/C available by Deferred Payment

14

Transferable Letter of Credit A transferable L/C allows the beneficiary to act as a middleman and transfer his rights under an L/C to another party or parties who may be suppliers of the goods. Depending on whether the L/C permits partial shipments, fractional amounts may be transferred to more than one beneficiary. The L/C however, can be transferred only once: the secondary beneficiaries cannot transfer their rights to a third party. Transfer of an L/C can be made on specific application by the original beneficiary. The applicant should be aware that any second beneficiary, the probable supplier, is usually a party not likely known to the applicant. The terms and conditions of the transferred L/C must be identical to those of the original L/C with the following exceptions: The original beneficiary may be shown as the applicant on the transferred credit. The amount of the L/C, and unit prices if any, may be less than in the original L/C. (the diff. being the original beneficiary’s profit margin). The latest shipment date, if any, and expiry date as shown on the original letter of credit should be shortened. The percentage of insurance coverage, if any, should be increased to satisfy the requirements of the original letter of credit. When a drawing takes place, the original beneficiary normally substitutes his invoices for those of the second beneficiary for up to the amount and unit prices available under the original L/C, and draws the difference as profit.

. The latest shipment date, if any, and expiry date as shown on the original letter of credit should be shortened. The percentage of insurance coverage, if any, should be increased to satisfy the requirements of the original letter of credit. When a drawing takes place, the original beneficiary normally substitutes his invoices for those of the second beneficiary for up to the amount and unit prices available under the original L/C, and draws the difference as profit..")

15

Back-to-Back Letter of Credit Although not recorded on a letter of credit, “back-to-back” is a term used in transactions involving two irrevocable letters of credit. Such transactions originate when a seller receives a letter of credit covering goods which must be obtained from a third party who in turn requires a letter of credit. The “second” issuing bank looks to the first issuing bank for reimbursement after paying under the second letter of credit. The difference between back-to-back letters of credit and transferable letters of credit, is such that in a transferable letter of credit, the rights under the existing letter of credit are transferred. In a back-to-back transaction, different letters of credit are actually issued. Because technical problems can arise in back-to-back transactions, banks tend to discourage their use.

16

Red Clause Letter of Credit A red clause letter of credit incorporates a clause, traditionally written in red, which authorizes the bank acting as the negotiating or paying bank to pay the beneficiary in advance of shipment. This enables the purchase and accumulation of goods from a number of different suppliers, and the arrangement of shipment in accordance with the L/C terms. Such advances will be deducted from the amount due to be paid when the documents called for are presented under the L/C. If the beneficiary fails to ship the goods or cannot do so before the expiry of the letter of credit, the issuing bank is bound to reimburse the negotiating or paying bank, recovering its payment from the applicant. Variations of such credits may also require that any advances be secured by temporary warehouse receipts until shipment is effected. Beneficiaries of red clause letters of credit are invariably brokers/agents of buyers in a particular field.

17

Standby Letters of Credit Standby L/C may apply to transactions which are based on the concept of default by the applicant in performance of a contract or obligation. In the event of default, the beneficiary is permitted to draw under the L/C. Standby L/Cs may be used as a substitute for performance guarantees, or issued to guarantee loans granted by one firm to another. Even if the applicant claims to have performed, the bank issuing the letter of credit is obliged to make payment provided the beneficiary produces complying documents, usually a sight draft, and a written demand for payment.

18

Broad Classification: Sight L/C Usance L/C Procedure for Establishment of L/C: Documents required: L/C Form IB-8 Indent / Proforma Invoice / Purchase Order duly confirmed by the Counter Party Issuance Cover Note / Marine Insurance Policy Form I

19

General Principles of UCP Letters of credit are separate transactions from the sales or other contracts on which they may be based, and banks are in no way involved with or bound by such contracts, even if reference to them is included in the letter of credit. In letters of credit transactions, all parties deal with documents and not with the underlying contracts to which the documents may relate. Before payment or acceptance of drafts is effected, banks bear the responsibility for examining the documents to ensure that they appear on their face to be in accordance with the terms and conditions of the letter of credit. Banks bear no responsibility for: the form or genuineness of documents; for the goods described in the documents; or the performance of the seller of the goods.

20

Scrutiny of L/C Application: Confirmation of names & addresses of customer and as well as of beneficiary. Signature on L/C Application being verified L/C Application properly filled in and complete Tenor of L/C exactly mentioned (Sight / Usance) Foreign Exchange Booking? (Yes / No) Item being permissible according to H.S. Code List? Is Proforma Invoice duly signed? Is Insurance Cover covering the L/C amount + 10% issued by approved insurance company. Do L/C contents match with Proforma Invoice? Country of Origin, not restricted by GOP. Is Mode of Shipment clearly defined? Is proper date of shipment & negotiation clearly mentioned? Is Port of Shipment not prohibited under Import Policy Order? Is there an approved valid credit limit? Has the required margin duly obtained? Etc.

Foreign Exchange Booking. (Yes / No) Item being permissible according to H.S. Code List. Is Proforma Invoice duly signed. Is Insurance Cover covering the L/C amount + 10% issued by approved insurance company. Do L/C contents match with Proforma Invoice. Country of Origin, not restricted by GOP. Is Mode of Shipment clearly defined. Is proper date of shipment & negotiation clearly mentioned. Is Port of Shipment not prohibited under Import Policy Order. Is there an approved valid credit limit. Has the required margin duly obtained. Etc..")

Similar presentations

1.Cash 2.Letter of Credit 3.Collections (Payment against documents,>")