Download presentation

Presentation is loading. Please wait.

1

Chapter 6 Annual Equivalent Worth Criterion

2

Chapter 6 Annual Equivalence Analysis Annual equivalent criterion Applying annual worth analysis Mutually exclusive projects

3

Annual Worth Analysis Principle: Measure an investment worth on annual basis Find the net present worth of the original series and multiply by the capital recovery factor Annual Equivalent (AE) = PW (A/P,i%,N)

= PW (A/P,i%,N)")

4

Annual Worth Analysis Evaluating a single revenue project AE > 0 accept the investment AE = 0 indifferent AE < 0 reject the investment Comparing multiple alternatives Revenue project: alternative with highest AE is selected Service project: alternative with lowest annual equivalent cost is selected

5

Annual Worth Analysis Benefit: By knowing the annual equivalent worth, we can: Seek consistency with the annual report format Determine the unit cost (or unit profit) Facilitate the unequal project life comparison

Facilitate the unequal project life comparison")

6

Computing Equivalent Annual Worth $15 $3.5 $5 $12 $8 0 2 3 4 5 6 1 A = $1.835 2 3 4 5 6 1 AE(15%) = $6.946(A/P, 15%, 6) = $1.835 $6.946 0 0 PW(15%) = $6.946 $9 $10

= $6.946(A/P, 15%, 6) = $1.835 $ PW(15%) = $6.946 $9 $10")

7

Annual Equivalent Worth - Repeating Cash Flow Cycles $500 $700 $800 $400 $500 $700 $800 $400 $1,000 Repeating cycle

8

First Cycle: PW(10%) = -$1,000 + $500 (P/F, 10%, 1) +... + $400 (P/F, 10%, 5) = $1,155.68 AE(10%) = $1,155.68 (A/P, 10%, 5) = $304.87 Both Cycles: PW(10%) = $1,155.68 + $1,155.68 (P/F, 10%, 5) = $1,873.27 AE(10%) = $1,873.27 (A/P, 10%,10) = $304.87

= $1, AE(10%) = $1, (A/P, 10%, 5) = $ Both Cycles: PW(10%) = $1, $1, (P/F, 10%, 5) = $1, AE(10%) = $1, (A/P, 10%,10) = $")

9

Annual Equivalent Cost When only costs are involved, the AE method is called the annual equivalent cost. Revenues must cover two kinds of costs: Operating costs (incurred by operation of plants or equipment) and Capital costs (incurred by purchasing the assets). Capital costs are one-time costs, whereas operating costs are recurring. Capital costs Operating costs + Annual Equivalent Costs

and Capital costs (incurred by purchasing the assets). Capital costs are one-time costs, whereas operating costs are recurring. Capital costs Operating costs + Annual Equivalent Costs.")

10

Capital (Ownership) Costs Def: Owning an equipment is associated with two transactions—(1) its initial cost (I) and (2) its salvage value (S). Capital recovery cost: the annual equivalent of a capital cost 0 1 2 3 N 0 N I S CR(i)

.")

11

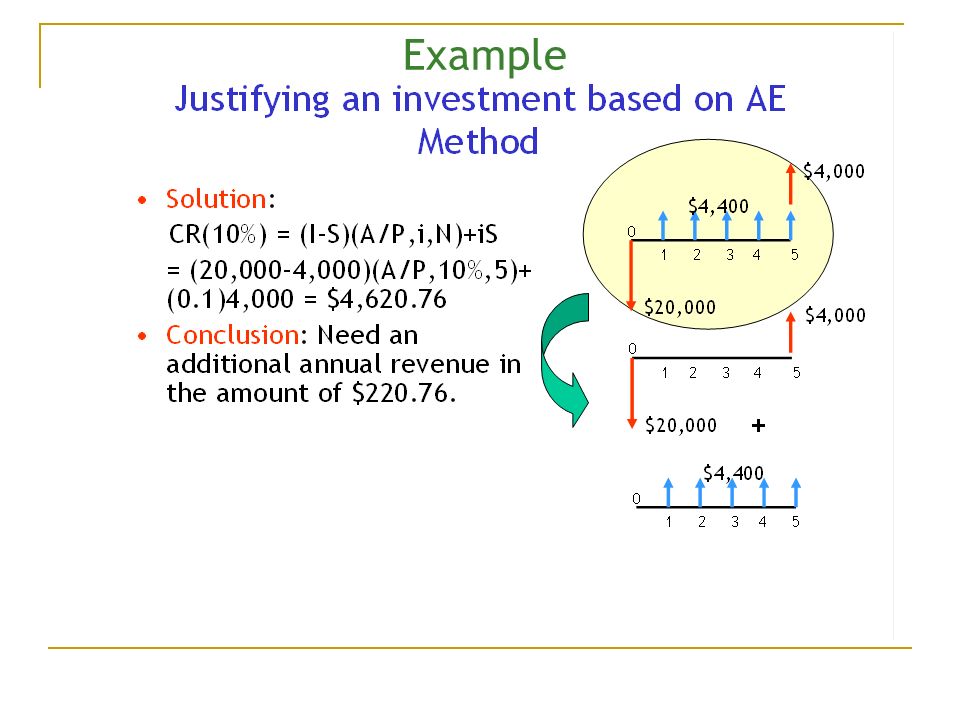

Example What is the equivalent annual cost of a machine that has an initial cost of $8,000, a salvage value of $500 after 8 years and annual operating costs of $900 if MARR=20%?

12

Solution AE = 8000 (A/P,20%,8) + 900 – 500 (A/F,20%,8) = 8000 (0.2606) + 900 – 500 (0.0606) = $2954.5 OR AE = (8000 - 500) (A/P,20%,8) + 500 (0.2) + 900 = 7500 (0.2606) + 100 + 900 = $2954.5

– 500 (A/F,20%,8) = 8000 (0.2606) – 500 (0.0606) = $ OR AE = ( ) (A/P,20%,8) (0.2) = 7500 (0.2606) = $2954.5")

13

Example

15

Applying Annual Worth Analysis Some economic analysis problems can be solved more efficiently by annual worth analysis Unit Cost (Unit Profit) Calculation Make-or-Buy Decision

Calculation Make-or-Buy Decision")

16

Unit Cost (Unit Profit) Calculation Determine the number of units to be produced each year Identify the cash flow series Calculate the annual worth Divide the annual worth by the number of units to be produced each year. If the number of units varies, then convert to equivalent annual units.

17

Example Equivalent Worth per Unit of Time 0 1 2 3 $24,400 $55,760 $27,340 $75,000 Operating Hours per Year 2,000 hrs. Compute the equivalent savings per machine hour with i=15%.

18

Example Equivalent Worth per Unit of Time PW (15%) = -75,000+24,400(P/F,15%,1) +27,370(P/F,15%,2)+55,760(P/F,15%,3) = $3,553 AE (15%) = $3,553 (A/P, 15%, 3) = $1,556 Savings per Machine Hour = $1,556/2,000 = $0.78/hr.

= -75,000+24,400(P/F,15%,1) +27,370(P/F,15%,2)+55,760(P/F,15%,3) = $3,553 AE (15%) = $3,553 (A/P, 15%, 3) = $1,556 Savings per Machine Hour = $1,556/2,000 = $0.78/hr.")

19

Example: Mutually Exclusive Alternatives with Equal Project Lives StandardPremium MotorEfficient Motor25 HP $13,000$15,60020 Years$0 89.5%93%$0.07/kWh3,120 hrs/yr. Size Cost Life Salvage Efficiency Energy Cost Operating Hours (a) At i= 13%, determine the operating cost per kWh for each motor. (b) At what operating hours are they equivalent?

At i= 13%, determine the operating cost per kWh for each motor. (b) At what operating hours are they equivalent .")

20

Solution: (a) Operating cost per kWh per unit Determine total input power 1 HP = 0.7457 kW 25HP=18.65 kW Standard motor: input power = 18.650 kW/ 0.895 = 20.838kW PE motor: input power = 18.650 kW/ 0.93 = 20.054kW

Operating cost per kWh per unit Determine total input power 1 HP = kW 25HP=18.65 kW Standard motor: input power = kW/ = kW PE motor: input power = kW/ 0.93 = kW")

21

Determine total kWh per year with 3120 hours of operation Standard motor: 3120 hrs/yr (20.838 kW) = 65,018 kWh/yr PE motor: 3120 hrs/yr (20.054 kW) = 62,568 kWh/yr Determine annual energy costs at $0.07/kwh: Standard motor: $0.07/kwh 65,018 kwh/yr = $4,551/yr PE motor: $0.07/kwh 62,568 kwh/yr = $4,380/yr

= 65,018 kWh/yr PE motor: 3120 hrs/yr ( kW) = 62,568 kWh/yr Determine annual energy costs at $0.07/kwh: Standard motor: $0.07/kwh 65,018 kwh/yr = $4,551/yr PE motor: $0.07/kwh 62,568 kwh/yr = $4,380/yr")

22

Capital cost: Standard motor : $13,000(A/P, 13%, 20) = $1,851 PE motor : $15,600(A/P, 13%, 20) = $2,221 Total annual equivalent cost = Capital Cost + Energy Cost Standard motor: AE(13%) = $4,551 + $1,851 = $6,402 Cost per output kwh = $6,402/58,188* kwh = $0.11/kwh PE motor: AE(13%) = $4,380 + $2,221 = $6,601 Cost per output kwh = $6,601/58,188 kwh = $0.1134/kwh (* 58,188 kwh/year = 3120 hours/year*25 HP*0.7457kwh/HP)

= $1,851 PE motor : $15,600(A/P, 13%, 20) = $2,221 Total annual equivalent cost = Capital Cost + Energy Cost Standard motor: AE(13%) = $4,551 + $1,851 = $6,402 Cost per output kwh = $6,402/58,188* kwh = $0.11/kwh PE motor: AE(13%) = $4,380 + $2,221 = $6,601 Cost per output kwh = $6,601/58,188 kwh = $0.1134/kwh (* 58,188 kwh/year = 3120 hours/year*25 HP*0.7457kwh/HP)")

23

(b) break-even Operating Hours = 6,742

break-even Operating Hours = 6,742")

24

Model A: 0 123 $12,500 $5,000 $3,000 Model B: 0 123 4 $15,000 $4,000 $2,500 Example: Mutually Exclusive Alternatives with Unequal Project Lives Required service Period = Indefinite Analysis period = LCM (3,4) = 12 years

= 12 years")

25

Model A: $12,500 $5,000 $3,000 0 12 3 First Cycle: PW(15%) = -$12,500 - $5,000 (P/A, 15%, 2) - $3,000 (P/F, 15%, 3) = -$22,601 AE(15%) = -$22,601(A/P, 15%, 3) = -$9,899 With 4 replacement cycles: PW(15%) = -$22,601 [1 + (P/F, 15%, 3) + (P/F, 15%, 6) + (P/F, 15%, 9)] = -$53,657 AE(15%) = -$53,657(A/P, 15%, 12) = -$9,899

![Model A: $12,500 $5,000 $3, First Cycle: PW(15%) = -$12,500 - $5,000 (P/A, 15%, 2) - $3,000 (P/F, 15%, 3) = -$22,601 AE(15%) = -$22,601(A/P, 15%, 3) = -$9,899 With 4 replacement cycles: PW(15%) = -$22,601 [1 + (P/F, 15%, 3) + (P/F, 15%, 6) + (P/F, 15%, 9)] = -$53,657 AE(15%) = -$53,657(A/P, 15%, 12) = -$9,899](http://images.slideplayer.com/36/10637896/slides/slide_25.jpg "Model A: $12,500 $5,000 $3, First Cycle: PW(15%) = -$12,500 - $5,000 (P/A, 15%, 2) - $3,000 (P/F, 15%, 3) = -$22,601 AE(15%) = -$22,601(A/P, 15%, 3) = -$9,899 With 4 replacement cycles: PW(15%) = -$22,601 [1 + (P/F, 15%, 3) + (P/F, 15%, 6) + (P/F, 15%, 9)] = -$53,657 AE(15%) = -$53,657(A/P, 15%, 12) = -$9,899")

26

Model B: $15,000 $4,000 $2,500 0 12 3 4 $4,000 First Cycle: PW(15%) = - $15,000 - $4,000 (P/A, 15%, 3) - $2,500 (P/F, 15%, 4) = -$25,562 AE(15%) = -$25,562(A/P, 15%, 4) = -$8,954 With 3 replacement cycles: PW(15%) = -$25,562 [1 + (P/F, 15%, 4) + (P/F, 15%, 8)] = -$48,534 AE(15%) = -$48,534(A/P, 15%, 12) = -$8,954

![Model B: $15,000 $4,000 $2, $4,000 First Cycle: PW(15%) = - $15,000 - $4,000 (P/A, 15%, 3) - $2,500 (P/F, 15%, 4) = -$25,562 AE(15%) = -$25,562(A/P, 15%, 4) = -$8,954 With 3 replacement cycles: PW(15%) = -$25,562 [1 + (P/F, 15%, 4) + (P/F, 15%, 8)] = -$48,534 AE(15%) = -$48,534(A/P, 15%, 12) = -$8,954](http://images.slideplayer.com/36/10637896/slides/slide_26.jpg "Model B: $15,000 $4,000 $2, $4,000 First Cycle: PW(15%) = - $15,000 - $4,000 (P/A, 15%, 3) - $2,500 (P/F, 15%, 4) = -$25,562 AE(15%) = -$25,562(A/P, 15%, 4) = -$8,954 With 3 replacement cycles: PW(15%) = -$25,562 [1 + (P/F, 15%, 4) + (P/F, 15%, 8)] = -$48,534 AE(15%) = -$48,534(A/P, 15%, 12) = -$8,954")

27

Summary Annual equivalent worth analysis, or AE, is—along with present worth analysis—one of two main analysis techniques based on the concept of equivalence. The equation for AE is AE(i) = PW(i)(A/P, i, N). AE analysis yields the same decision result as PW analysis.

= PW(i)(A/P, i, N). AE analysis yields the same decision result as PW analysis..")

28

The capital recovery cost factor, or CR(i), is one of the most important applications of AE analysis in that it allows managers to calculate an annual equivalent cost of capital for ease of itemization with annual operating costs. The equation for CR(i) is CR(i)= (I – S)(A/P, i, N) + iS, where I = initial cost and S = salvage value.

is CR(i)= (I – S)(A/P, i, N) + iS, where I = initial cost and S = salvage value..")

29

AE analysis is recommended over NPW analysis in many key real-world situations for the following reasons: 1. In many financial reports, an annual equivalent value is preferred to a present worth value. 2. Calculation of unit costs is often required to determine reasonable pricing for sale items. 3. Calculation of cost per unit of use is required to reimburse employees for business use of personal cars. 4. Make-or-buy decisions usually require the development of unit costs for the various alternatives.

Similar presentations

2001 Contemporary Engineering Economics 1 Chapter 8 Annual Equivalent Worth Analysis Annual equivalent criterion Applying annual worth analysis Mutually.>")

2001 Contemporary Engineering Economics 1 Chapter 7 Present Worth Analysis Describing Project Cash Flows Initial Project Screening Method Present Worth.>")