Download presentation

Presentation is loading. Please wait.

1

By: David Johnston, James Mataras, Jesse Pirnat, Daniel Sanchez, Eric Shaw, Sean Vazquez, Brad Warren Stevens Institute of Technology Department of Quantitative Finance: Professor Calhoun Department of Computer Science: Professor Klappholz

2

Table of Contents Introduction Requirements Software Design Features Financial Models Security Challenges

3

Introduction System will enable more efficient and effective portfolios and risk management Providing tools and analytics to drive investment decisions Tools to support portfolio construction, position and trade analysis, risk metrics, and monitoring performance System features a market model to help identify risks and trading opportunities Client may leverage these tools to build a custom strategy based on quantitative analysis

4

Objectives Provide access to stock data without the need to pay for a subscription data source Manage virtual trading accounts Track portfolio performance Risk forecasts and analytics Analyze potential trades

5

Functional Requirements Portfolio Tracking Input a portfolio and enter trades in the system From the online feed for market data, system will provide updated quotes and charting capability for viewing portfolio performance Portfolio will be made up of cash and long equities Will not maintain a margin account Risk Management System shall provide portfolio risk metrics Volatility forecasts Scenario analysis Sensitivities and correlations Value-at-Risk User may also drill down to position-level granularity

6

Functional Requirements Cont. Trade Analysis With the risk management technology, the user shall be able to: Analyze potential trades Assess risk and return See the effects on the portfolio as a whole

7

Software Design

8

Features and Usability Multi platform usability iPhone, Android, Tablet, Laptop/Desktop Instant Access to Profile data and online data Save all data on your profile online Detailed graphing interface No installation required!

9

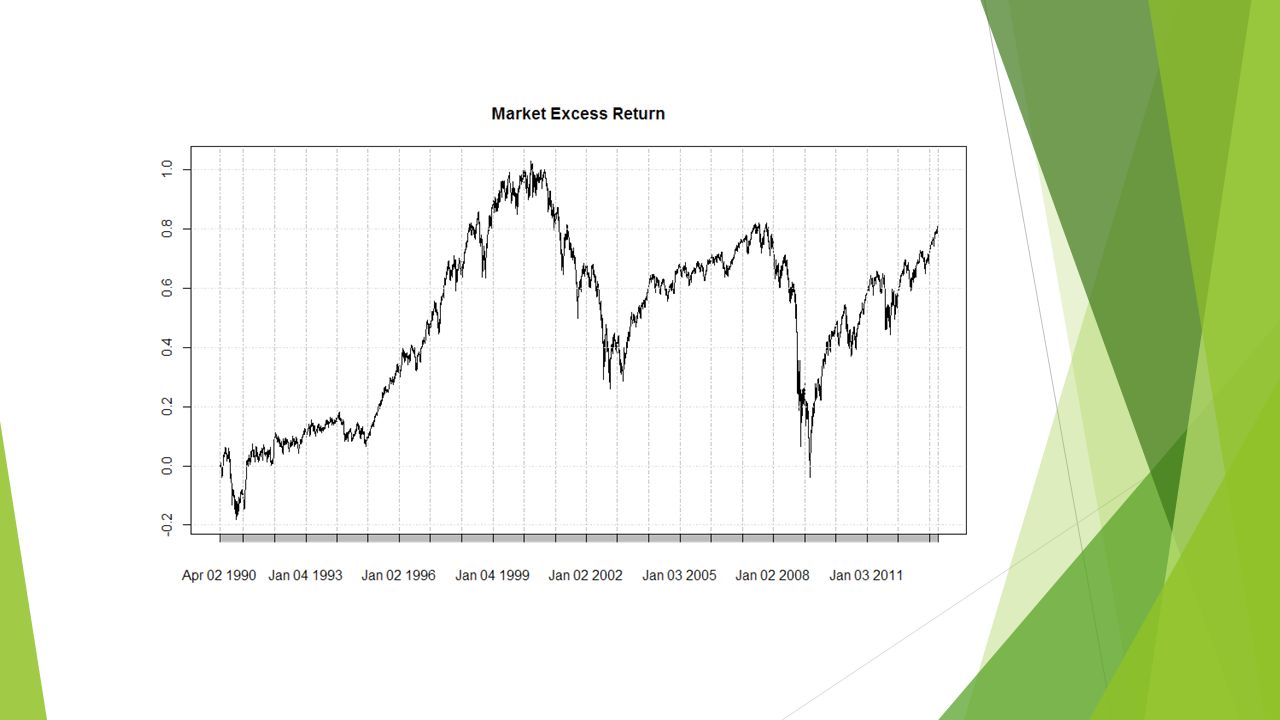

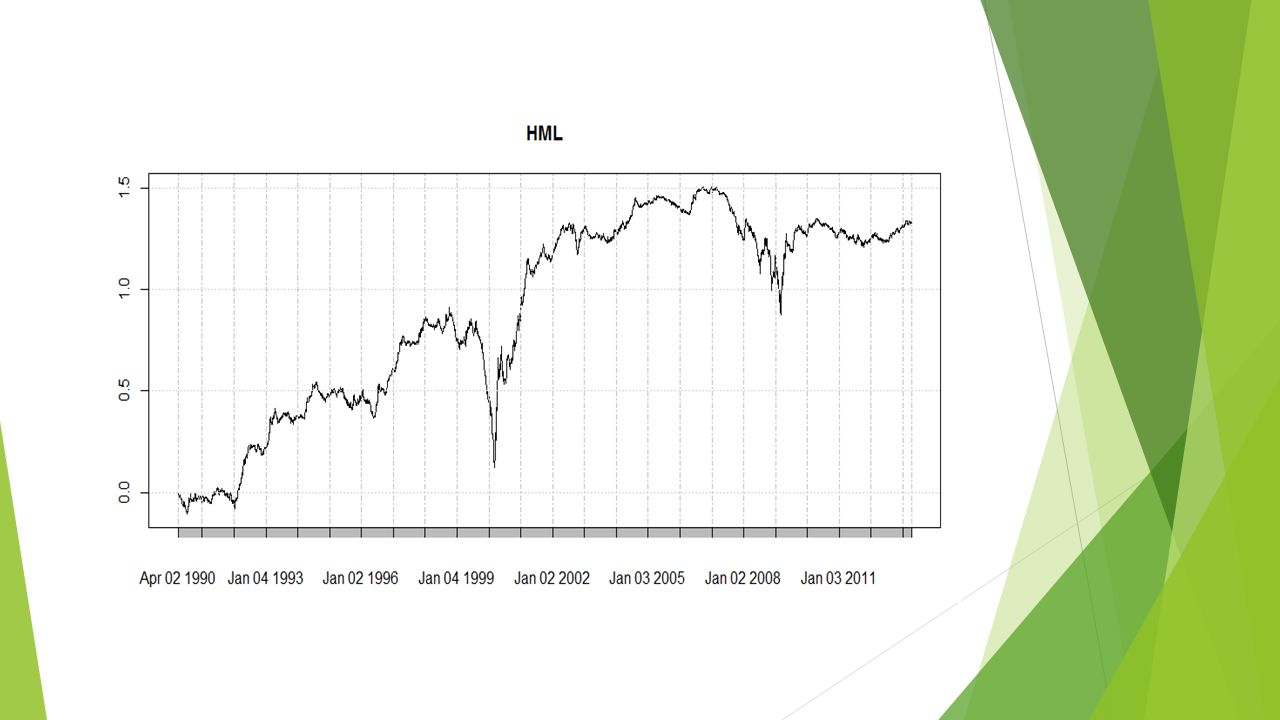

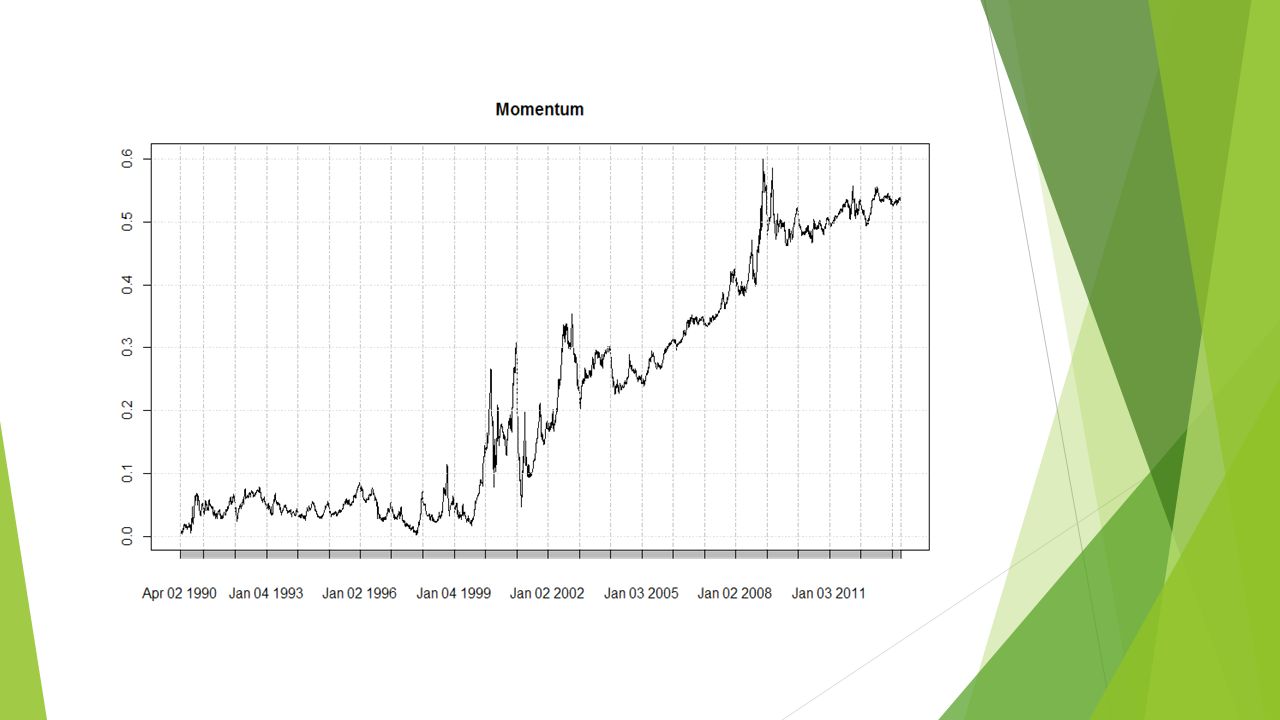

Factor Model Stock returns are explained by a set of factors As well as an idiosyncratic component We use 4 factors Total market return Market cap Value Momentum Makes for a tractable model Dimensionality reduction Intuition

14

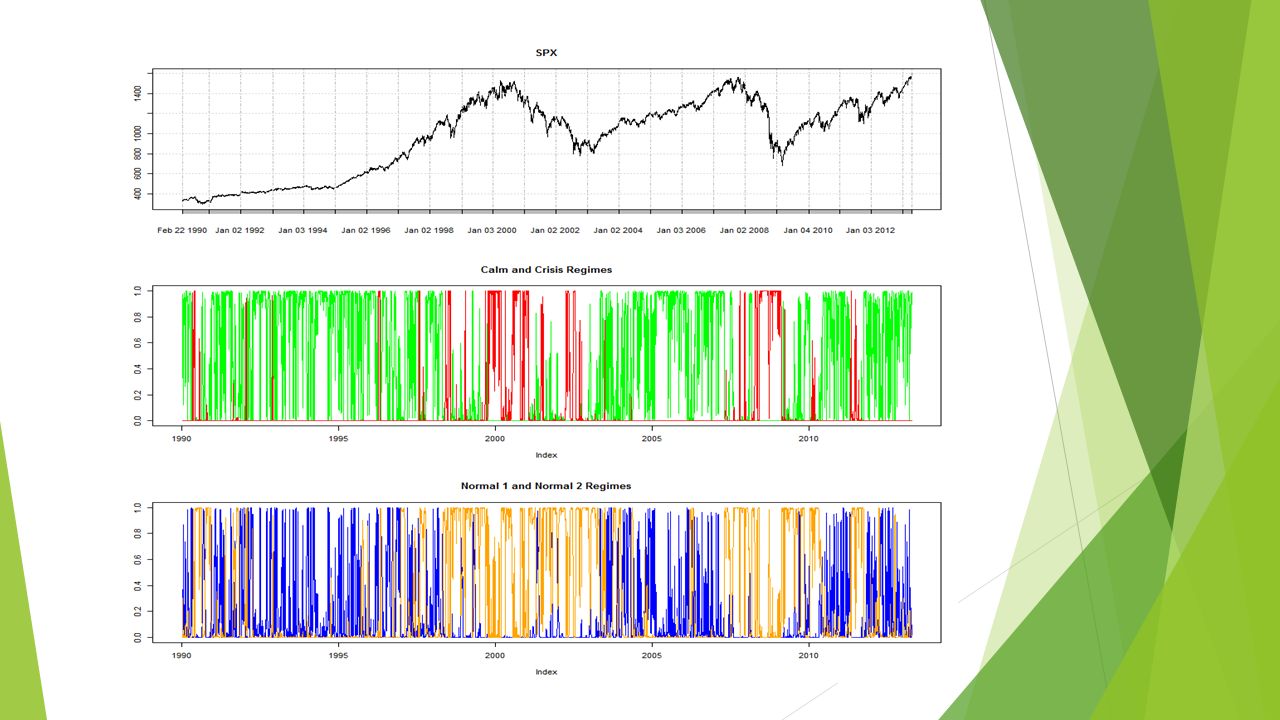

Regime Switching Define a latent variable for the current regime Returns in each regime are determined by a factor model with different parameters Model dynamics using a Hidden Markov Model (HMM) Regime transitions are described by a Markov process Model calibration is data driven, using Machine Learning Bayesian inference Expectation-Maximization algorithm Advantages over traditional factor models Traditional factor models are Gaussian and stationary Regime switching can generate behavior that better approximates empirical market dynamics E.g. fat tails, heteroskedasticity, leverage effect, time-varying correlations

16

Forecasts and Analytics Monte Carlo simulation based on model Forecasts the distribution of returns Perform risk analysis based on simulation results Return and volatility forecasts Value at Risk Marginal impact of individual positions and potential trades

17

Security Requirements Confidentiality User Information Account Password Anonymity Integrity Data loss prevention Data modification restrictions Accessibility In production: accessible anywhere at any time Currently: only accessible on Stevens Campus

18

Security Risks User Accounts Session Management Authentication Mechanisms Data Communication Source Verification HTTPS Input Validation XSS, JavaScript Injection, SQL Injection etc. Denial of Service (DoS)

.")

19

Challenges: Implementation Interfacing with live data Integrating different technologies and algorithms in application Wt C++ Framework Caused significant setbacks Was not familiar with any of the standard web tools and technologies: HTML5, CSS3, JavaScript, jQuery Time constraints after moving off original Wt C++ web toolkit Did not know about responsive web design Gained familiarity and understanding of the traditional web technologies Gained exposure to widely used Twitter Bootstrap framework and learned how responsive web design is done.

20

Challenges: Financial Modeling Model research and development Literature research and applied quantitative analysis Algorithm implementation Efficiency is critical Data acquisition Bloomberg Terminal Data cleaning Size of historical dataset

Similar presentations

1.>")