Download presentation

Presentation is loading. Please wait.

1

The Accounting Information System

Chapter 02 The Accounting Information System Chapter 2: The Accounting Information System The chapter is divided into 2 parts. Part A: Measuring Business Activities Part B: Debits and Credits McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc.

2

Chapter 2 Participation Questions

Why are there Accounting Principles and Rules, such as GAAP, to guide modern financial accounting and the preparation of financial statements in North America? To build consistency in the financial statements; To make it more difficult to prepare financial statements; or To develop a level of confusion in the financial statements based on too many rules. What is the actual origin of the terms debit and credit? They are philosophical terms that are used in accounting; They are both ancient mathematical terms; or No one really knows where they originated, but they have been in use for in excess of 500 years. What does CPA stand for? Confirmed 'Perfect' Accounting; Certified 'Public' Accountant; or Committed Person in Accounting What was the name of the Company used for the final in-lecture problem at the very end of chapter 2 where we assembled an unadjusted trial balance? ABC Construction; UTE Sewing Shop; or JRB Law Firm What is the minimum number of entries for each transaction in double entry accounting? One; two; or three

3

Announcements Connect Enrollment Date closes on 1/24/16 – USE KNIGHTS ADDRESS ONLY 600 out of 1,235 signed up Free trial access includes e-book – free trial ends on 1/24/16 “Connect” - $85.00 includes no e-book – purchase through Connect Website “Connect Plus” - $ includes e-book – purchase through Connect Website Assignments January 19th Syllabus Quiz #1 – used for attendance for Federal Student Aid (Webcourses) – 2 attempts January 24th Participation Questions for Chapter #1 questions (Webcourses) – 1 attempt Connect Homework Assignment #1 (Connect) – unlimited attempts Materia Homework Assignment #1 (Webcourses) – unlimited attempts January 31st Participation Questions for Chapter #2 questions (Webcourses) – 1 attempt Connect Homework Assignment #2 (Connect) – unlimited attempts Materia Homework Assignment #2 (Webcourses) – unlimited attempts Definitions Quiz (Webcourses) – 2 attempts Links for Materia flash Cards – In Chapter 2 Introduction & Below: Practice Flash Cards – Part 1: Practice Flash Cards – Part 2:

– 2 attempts. January 24th. Participation Questions for Chapter #1 questions (Webcourses) – 1 attempt. Connect Homework Assignment #1 (Connect) – unlimited attempts. Materia Homework Assignment #1 (Webcourses) – unlimited attempts. January 31st. Participation Questions for Chapter #2 questions (Webcourses) – 1 attempt. Connect Homework Assignment #2 (Connect) – unlimited attempts. Materia Homework Assignment #2 (Webcourses) – unlimited attempts. Definitions Quiz (Webcourses) – 2 attempts. Links for Materia flash Cards – In Chapter 2 Introduction & Below: Practice Flash Cards – Part 1: Practice Flash Cards – Part 2:")

4

UCF ACG 2021 tutoring opportunities: College of Business Accounting Tutoring Lab - BA 1 – Room 355 Monday 10:30 AM – 9:00 PM Tuesday 10:00 AM – 1:15 PM 2:45 PM – 6:00 PM Wednesday 10:00 AM – 12:45 PM 1:20 PM – 5:50 PM Thursday 8:20 AM – 1:20 PM 3:00 PM – 5:45 PM SARC - UCF Student Academic Resource Center (SARC) – Howard Phillips Hall – Room FRIDAY 10:00 AM – 1:00 PM & 2:00 PM – 5:00 PM VARC - UCF Veteran’s Academic Resource Center (VARC) – UCF Arena (next to Jimmy John's). Tutoring is open to all UCF students. MONDAY 2:00 PM – 4:00 PM

– UCF Arena (next to Jimmy John s). Tutoring is open to all UCF students. MONDAY 2:00 PM – 4:00 PM.")

8

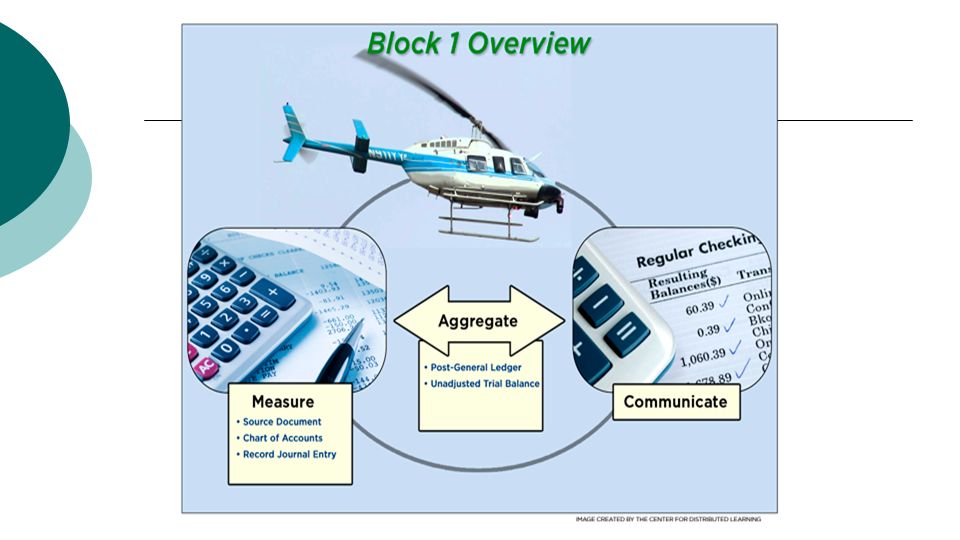

Block 1 Chapter 1: Overview of Accounting and Financial Reporting

Measure Aggregate Communicate Chapter 2 – 3: Accounting Cycle – Measure/analyze business transactions to aggregate and construct financial statements for communication with decision makers

9

Questions to be Answered

Overall - How has society shaped today’s financial reporting? Chapter 2 – How do we begin to make sense of the abundance of transactions that occur in an organization each year (accounting period)?

")

10

Chapter 2 - Learning Objectives

Identify the Basic Steps in Measuring During the Period Transactions (Business Activities). Analyze the Impact of During the Period (External) Business Transactions on the Accounting Equation. Debits and Credits Unadjusted Trial Balance Part A: Measuring Business Activities In this chapter, we examine the accounting information process using a manual accounting system. Process accountants use to identify, analyze, record, and summarize economic events affecting a company’s financial position. 2-10

. Analyze the Impact of During the Period (External) Business Transactions on the Accounting Equation. Debits and Credits. Unadjusted Trial Balance. Part A: Measuring Business Activities. In this chapter, we examine the accounting information process using a manual accounting system. Process accountants use to identify, analyze, record, and summarize economic events affecting a company’s financial position")

11

Classification of Business Activities

During the Month (External) transactions Transaction with a separate economic entity (Basically, any organization or unit in society can be an economic entity.) Includes Other businesses Government entities Employees End of the month (internal) transactions Transaction NOT with a separate economic entity Recognize the passage of time for prepaid rent, insurance, etc. Recognize the depreciation expense associated with long-term asset purchases. Recognized the amount of supplies utilized during the accounting period. With in the company With a separate economic entity Do not include a separate economic entity Basically, any organization or unit in society can be an economic entity. 2-11

transactions. Transaction with a separate economic entity (Basically, any organization or unit in society can be an economic entity.) Includes. Other businesses. Government entities. Employees. End of the month (internal) transactions. Transaction NOT with a separate economic entity. Recognize the passage of time for prepaid rent, insurance, etc. Recognize the depreciation expense associated with long-term asset purchases. Recognized the amount of supplies utilized during the accounting period. With in the. company. With a separate. economic entity. Do not include. a separate. economic entity. Basically, any organization or unit in society can be an economic entity")

12

6 Steps for Measuring “During the Period” Business Transactions

FYI - For the accounting cycle, Steps 2, 3 & 4 are combined together into the Record Journal Entry Step. Analyze the impact of the transaction on the accounting equation Assess whether the transaction results in a debit or credit 2-12

13

Measuring External Transactions

1. Source Document Record Journal Entry (includes steps 2 – 4) 2. Analyze transaction using Accounting Equation 3. Debit or Credit Account 4. ‘Record’ in general journal 5. ‘Post’ to general Ledger 6. Prepare ‘Unadjusted Trial Balance’

2. Analyze transaction using Accounting Equation 3. Debit or Credit Account 4. ‘Record’ in general journal 5. ‘Post’ to general Ledger 6. Prepare ‘Unadjusted Trial Balance’")

14

Step 1 – Obtain Sample Source Document

15

Sample Chart of Accounts from QuickBooks Accounts used in our class

Located on back cover of Textbook

16

Sample of Chart of Accounts used in During the Month (External) Transactions

Cash – liquid assets. Accounts Receivable – amounts the company expects to collect from customers. Supplies – items that will be consumed by the company during the operation of the business such as office supplies. Prepaid expenses – prepayments for items such as rents and insurance that will be utilized at a future date. Equipment – Equipment utilized in the operation of the business Accounts Payable – Promise to pay cash in the future to creditors for the purchase supplies or materials. Notes payable –Total amounts owed to creditors for loaning money to the company. Unearned Revenue – Advance payment of cash received by the company for services or products to be furnished in the future. Key factor is revenue has not been earned. An example is the retainer for legal services. Common Stock – Amount shareholders have invested in the business. Service Revenue - Amounts earned from providing services to customers. Salary Expense – Labor expended while providing goods or services. Dividend – payment of cash to stockholders (owners). Cash is never part of an internal transaction

. Cash is never part of an internal transaction.")

17

Learning Objective (LO) #2 and Step #2

Analyze the Impact of During the Period (External) Business Transactions on the Accounting Equation

Business Transactions on the Accounting Equation.")

18

Analyze the Impact of During the Period Transactions on the Accounting Equation

Each transaction will have a dual effect. If an economic event increases one side of the equation, then it also increases the other side of the equation by the same amount. Recall that the basic accounting equation must always remain in balance; i.e., the left side (assets) equals the right side (liabilities and stockholders’ equity). Each transaction will have a dual effect. If an economic event increases one side of the equation, then it also increases the other side of the equation by the same amount. Record transactions that affect financial position of company – record sales vs. sales calls 2-18

equals the right side (liabilities and stockholders’ equity). Each transaction will have a dual effect. If an economic event increases one side of the equation, then it also increases the other side of the equation by the same amount. Record transactions that affect financial position of company – record sales vs. sales calls")

19

Step 2 - Ask these three questions to analyze (measure) during the month transactions

First account affected by the transaction – increase of decrease? If the transaction states ‘on account’, think Accounts Receivable or Accounts Payable; Otherwise, think CASH Second account affected by the transaction – increase of decrease? Accounting equation still balance? For each transaction, ask yourself these questions: 1. “What is one account in the accounting equation affected by the transaction? Does that account increase or decrease?” 2. “What is a second account in the accounting equation affected by the transaction? Did that account increase or decrease?” After noting the effects of the transaction on the accounting equation, ask yourself this: 3. ”Do assets still equal liabilities plus stockholders’ equity?” The answer to this question must be “yes.”. At least two accounts will be affected by every transaction or economic event. While some economic events will affect more than two accounts, most events we record affect only two accounts. 2-19

20

During the Month (External) Transactions of Eagle Golf Academy

The best way to understand the impact of a transaction on the accounting equation is to see it demonstrated by a few examples. Let’s return to the Eagle Golf Academy from Chapter 1. The illustration in the slide summarizes the first five external transactions for Eagle in January, the first month of operations. Note that business activities usually occur in this same order for a new company—obtain external financing, use those funds to invest in long-term productive assets, and then begin normal operations. We have discussed these business activities in Chapter 1. 2-20

21

Transaction(1): Issue Common Stock

To generate cash from external sources, Eagle sells shares of common stock for $25,000. Eagle Golf Academy Investors Stock certificate It’s time to ask the three questions we asked earlier: What is one account in the accounting equation affected by the transaction? Does that account increase or decrease? Answer: Cash. Cash is a resource owned by the company, which makes it an asset. The company receives cash from you, so cash and total assets increase by $25,000. To begin operations, Eagle Golf Academy needs cash. To generate cash from external sources, Eagle sells shares of common stock for $25,000. It’s time to ask the three questions we asked earlier: 1. What is one account in the accounting equation affected by the transaction? Does that account increase or decrease? Answer: Cash. Cash is a resource owned by the company, which makes it an asset. The company receives cash from you, so cash and total assets increase by $25,000. 2-21

22

Transaction(1): Issue Common Stock

What is a second account in the accounting equation affected by the transaction? Does that account increase or decrease? Answer: Common stock. Common stock is a stockholders’ equity account. Issuing common stock to you in exchange for your $25,000 increases the amount of common stock owned by stockholders, so common stock and total stockholders’ equity both increase. 2. “What is a second account in the accounting equation affected by the transaction? Does that account increase or decrease?” Answer: Common stock. Common stock is a stockholders’ equity account. Issuing common stock to you in exchange for your $25,000 increases the amount of common stock owned by stockholders, so common stock and total stockholders’ equity both increase. 2-22

23

Transaction(1): Issue Common Stock

Do assets equal liabilities plus stockholders’ equity? Answer: Yes. Note: The accounting equation balances. If one side of the equation increases, so does the other side. We can use this same series of questions to understand the effect of any business transaction. 3. Do assets equal liabilities plus stockholders’ equity? Answer: Yes. Note: The accounting equation balances. If one side of the equation increases, so does the other side. We can use this same series of questions to understand the effect of any business transaction. 2-23

24

Assets = Liabilities + Stockholders Equity

Check-in Transaction #3 – Increase which account? A) Cash, B) Accounts Receivable, C) Accounts Payable, D) Equipment

Cash, B) Accounts Receivable, C) Accounts Payable, D) Equipment.")

25

Using the current account balances to create a balance sheet

(FYI - this balance sheet is created out of the correct ordering, but shown to illustrate how the account balances are used in the financial statements).

.")

26

Transaction(2): Borrow from the Bank

Seeking cash from another external source, Eagle borrows $10,000 from the bank and signs a note for it. Eagle Golf Academy Bank 1. What is one account in the accounting equation affected by the transaction? Does that account increase or decrease? Answer: Cash. Cash is a resource owned by the company, which makes it an asset. The company receives cash, so cash and total assets increase. 2. What is a second account in the accounting equation affected by the transaction? Does that account increase or decrease? Answer: Notes payable. Notes payable represents the amount owed to a creditor (the bank in this case), which makes it a liability. The company incurs debt when signing the note, so notes payable and total liabilities increase. 3. Do assets equal liabilities plus stockholders’ equity? Answer: Yes. 2-26

, which makes it a liability. The company incurs debt when signing the note, so notes payable and total liabilities increase. 3. Do assets equal liabilities plus stockholders’ equity Answer: Yes")

27

Transaction(3): Purchase Equipment

Purchase equipment with cash, $24,000. Eagle Golf Academy Supplier Once Eagle obtains financing by issuing common stock and borrowing from the bank, the company can invest in long-term assets necessary to operate the business. Buying equipment from a supplier causes one asset to increase and another asset to decrease. Notice that purchasing one asset (equipment) with another asset (cash) has no effect on the category totals in the accounting equation. One asset increases, while another asset decreases. 2-27

with another asset (cash) has no effect on the category totals in the accounting equation. One asset increases, while another asset decreases")

28

Transactions(4) and(5): Incur Costs for Rent and Supplies

Pay one year of rent in advance, $6,000. Rental space Eagle Golf Academy Landlord Eagle Academy pays one year of rent in advance, $6,000. Purchasing rent in advance causes one asset to increase and one asset to decrease. Because the rent paid is for occupying space in the future, we don’t want to record it as an expense immediately. Instead, we record it as an asset representing the right to occupy the space in the future. We call the asset prepaid rent and, as we discuss later in the course, we’ll report this amount as expense over the next 12 months, as the time we’ve paid for expires. 2-28

29

Transactions(4) and(5): Incur Costs for Rent and Supplies

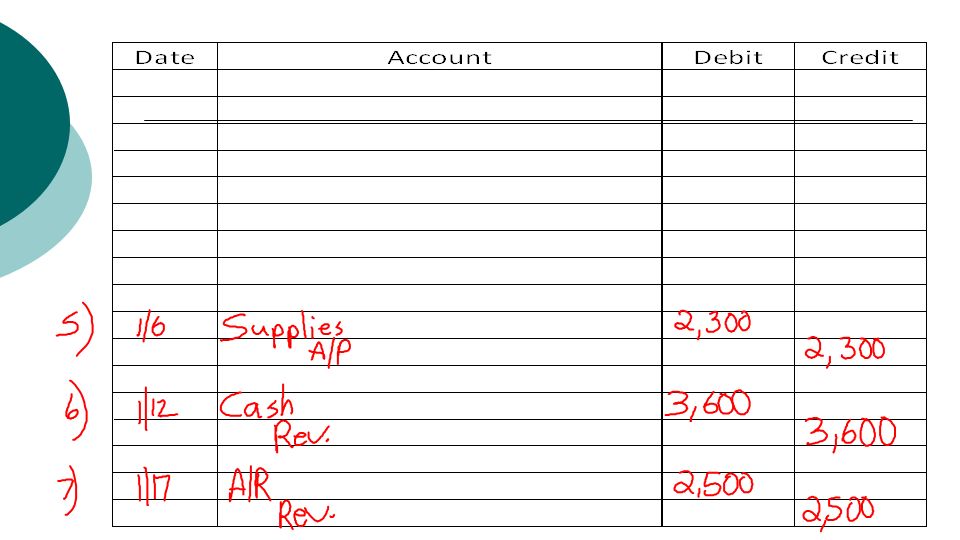

Purchase of supplies on account, $2,300. Eagle Golf Academy Supplier Purchases supplies on account, $2,300. Purchasing supplies with the promise to pay cash in the future causes an asset (supplies) to increase and also creates a liability (accounts payable) to increase. 2-29

to increase and also creates a liability (accounts payable) to increase")

30

Effects of transactions on the Expanded Accounting Equation

Transactions that affect stockholders’ equity on the balance sheet due to transactions on the income statement To better understand how revenues increase stockholders’ equity, let’s expand the accounting equation. As discussed in Chapter 1, we can divide stockholders’ equity into its two components—Common stock and Retained earnings. Common stock represents investments by stockholders, while retained earnings represent net income earned over the life of the company that has not been distributed to stockholders as dividends. Both of these amounts represent stockholders’ claims to the company’s resources. Next, we can split retained earnings into its three components—revenues, expenses, and dividends. Notice that in the previous transaction we add revenues to stockholders' equity. That’s because revenues increase net income, and net income increases stockholders’ claims to resources. Therefore, an increase in revenues has the effect of increasing stockholders’ equity in the basic accounting equation. We subtract expenses and dividends. Expenses reduce net income, and dividends represent a distribution of net income to stockholders. Both expenses and dividends reduce stockholders’ claims to the company’s resources. Therefore, an increase in expenses or dividends has the effect of decreasing stockholders’ equity in the basic accounting equation. 2-30

31

Assets = Liabilities + Stockholders Equity

(Stock + Retained Earnings) Rev. – Exp. – Div. Check-in Transaction #7 – Which accounts are used? A) Cash, B) Accounts Receivable, C) Accounts Payable, D) Revenue

Rev. – Exp. – Div. Check-in Transaction #7 – Which accounts are used A) Cash, B) Accounts Receivable, C) Accounts Payable, D) Revenue.")

32

Transitions(6) and (7): Provide Services to Customers

Providing service to customers for cash causes both assets and stockholders’ equity to increase. Eagle Golf Academy Training Customers Net Income Retained Earnings Stockholders’ Equity To see an example of how revenue affects the expanded accounting equation, let’s look at the two revenue transactions for Eagle Golf Academy. In transaction (6) , Eagle provides golf training to customers who pay cash at the time of the service, $3,600. Providing training to customers for cash causes both assets and stockholders’ equity to increase. Notice that an increase in service revenue increases stockholders’ equity by increasing the retained earnings account ( + $3,600 ). Therefore, the basic accounting equation remains in balance (Assets = Liabilities + Stockholders’ Equity). Revenue 2-32

, Eagle provides golf training to customers who pay cash at the time of the service, $3,600. Providing training to customers for cash causes both assets and stockholders’ equity to increase. Notice that an increase in service revenue increases stockholders’ equity by increasing the retained earnings account ( + $3,600 ). Therefore, the basic accounting equation remains in balance (Assets = Liabilities + Stockholders’ Equity). Revenue")

33

Transitions(6) and (7): Provide Services to Customers

Similarly, providing service to customers on account causes both assets and stockholders’ equity to increase Eagle Golf Academy Customers Training In transaction (7) , other customers receive golf training but promise to pay $2,500 cash at some time in the future. The fact that some customers do not pay cash at the time of the service doesn’t prevent Eagle from recording revenue. Eagle has earned the revenue by providing services. In addition, the right to receive cash from a customer is something of value the company owns, and therefore is an asset. When a customer does not immediately pay for services with cash, we traditionally say the services are performed “on account,” and we record an account receivable. Providing services to customers on account causes both assets and stockholders’ equity to increase. 2-33

, other customers receive golf training but promise to pay $2,500 cash at some time in the future. The fact that some customers do not pay cash at the time of the service doesn’t prevent Eagle from recording revenue. Eagle has earned the revenue by providing services. In addition, the right to receive cash from a customer is something of value the company owns, and therefore is an asset. When a customer does not immediately pay for services with cash, we traditionally say the services are performed on account, and we record an account receivable. Providing services to customers on account causes both assets and stockholders’ equity to increase")

34

Transaction(8): Receive Cash in Advance from Customer

Receive cash in advance from customers, $600. Training Eagle Golf Academy Customers Companies sometimes receive cash in advance from customers. We’re assuming that Eagle receives $600 from customers for golf training to be provided later. In this case, the company cannot report revenue from training now because it has yet to provide the training to earn those revenues. Instead, the advance payment from customers creates an obligation for the company to perform services in the future, and this future obligation is a liability (or debt), most commonly referred to as unearned revenue. Receiving cash in advance causes both assets and liabilities to increase: 2-34

, most commonly referred to as unearned revenue. Receiving cash in advance causes both assets and liabilities to increase:")

35

Transaction(9): Incur Cost for Salaries

Pay salaries to workers, $2,800 Labor Eagle Golf Academy Employee Net Income Retained Earnings Stockholders’ Equity Companies incur a variety of expenses in generating revenues. Eagle Academy incurs salaries expense of $2,800. Paying salaries for the current period causes assets and stockholders’ equity to decrease. Notice that an increase in salaries expense results in a decrease in retained earnings ( − $2,800 ). As a result, the accounting equation remains in balance, with both sides decreasing by $2,800. The concept of expenses flowing into retained earnings is the same concept that we see in transactions (6) and (7) where revenues also flow into retained earnings, but in the opposite direction. Expense 2-35

. As a result, the accounting equation remains in balance, with both sides decreasing by $2,800. The concept of expenses flowing into retained earnings is the same concept that we see in transactions (6) and (7) where revenues also flow into retained earnings, but in the opposite direction. Expense")

36

Transaction (10): Pay Dividends

Pay dividends to stockholders, $200 Reduced Claims to Company’s Resources Eagle Golf Academy Investors Retained Earnings Stockholders’ Equity The final financing transaction of Eagle Golf Academy for the month is the payment of a $200 cash dividend to stockholders. Recall from the previous chapter that a dividend represents a payment of cash to the owners (stockholders) of the company. Dividends are not expenses. Instead, dividends are distributions of part of the company’s net income to the owners and thus reduce retained earnings, a stockholders’ equity account. Normally a company wouldn’t pay dividends after only a month in business, but we make this assumption here for purposes of illustration. Dividends decrease stockholders’ equity because dividends are distributions of the company’s earnings (net income) and therefore reduce retained earnings. Since retained earnings is a stockholders’ equity account, when retained earnings decreases, so does stockholders’ equity. Dividends 2-36

of the company. Dividends are not expenses. Instead, dividends are distributions of part of the company’s net income to the owners and thus reduce retained earnings, a stockholders’ equity account. Normally a company wouldn’t pay dividends after only a month in business, but we make this assumption here for purposes of illustration. Dividends decrease stockholders’ equity because dividends are distributions of the company’s earnings (net income) and therefore reduce retained earnings. Since retained earnings is a stockholders’ equity account, when retained earnings decreases, so does stockholders’ equity. Dividends")

37

Summary of All Ten External (During the Month) Transactions of Eagle Golf Academy

Transactions of Eagle Golf Academy")

38

Summary of the accounts impacted in the first ten transactions – beginning of aggregation

39

Using the current account balances to create a balance sheet

(FYI - this balance sheet is created out of the correct ordering, but shown to illustrate how the account balances are used in the financial statements). Depreciation relocates an asset’s cost from the balance sheet as an expense in the income statement.

. Depreciation relocates an asset’s cost from the balance sheet as an expense in the income statement.")

40

Learning Objective #3 Debits and Credits

While the actual origin of the terms debit and credit is unknown, the first known recorded use of the terms is Venetian Luca Pacioli's 1494 work, Summa de Arithmetica, Geometria, Proportioni et Proportionalita (translated: Everything About Arithmetic, Geometry and Proportion). Pacioli devoted one section of his book to documenting and describing the double-entry bookkeeping system in use during the Renaissance by Venetian merchants, traders and bankers. This system is still the fundamental system in use by modern bookkeepers.[12]

. Pacioli devoted one section of his book to documenting and describing the double-entry bookkeeping system in use during the Renaissance by Venetian merchants, traders and bankers. This system is still the fundamental system in use by modern bookkeepers.[12]")

41

Left & Right & The Accounting Equation

Stockholders’ Equity Assets Liabilities Assets are to the LEFT of the equal sign: INCREASE with a DEBIT (left) Liabilities & Equity are to the RIGHT of the equal sign: INCREASE with a CREDIT (right) The accounting equation expresses the basic relationships of accounting. For each asset, each liability, and each element of stockholders’ equity, we use a record called the account. An account is the record of all the changes in a particular asset, liability, or stockholders’ equity during a period. The account is the basic summary device in accounting. 41 41

Liabilities & Equity are to the RIGHT of the equal sign: INCREASE with a CREDIT (right) The accounting equation expresses the basic relationships of accounting. For each asset, each liability, and each element of stockholders’ equity, we use a record called the account. An account is the record of all the changes in a particular asset, liability, or stockholders’ equity during a period. The account is the basic summary device in accounting")

42

Debit and Credit Effects on Accounts in the Accounting Equation

"Normal Balance” Although debit and credit are derived from Latin terms, today debit simply means “left” and credit means “right.” It is easy to visualize the use of these directional signals by means of an accounting convention called a “T-account.” A T-account is a simplified presentation of an account, in the shape of the letter T. Across the top, we show the account title. We refer to increases in accounts on the left side of the accounting equation—assets —as debits. Just the opposite is true for accounts on the right-hand side of the equation. We refer to increases in liabilities and stockholders’ equity as credits. The rules reverse for decreases in accounts: Assets decrease with a credit. Liabilities and stockholders’ equity decrease with a debit. 2-42

43

Debit and Credit Effects on Accounts in the Expanded Accounting Equation – Page 56

Remember that accounts on the left side of the accounting equation (assets) increase with debits or the left side of an account. Accounts on the right side of the accounting equation (liabilities and stockholders’ equity) increase with credits or the right side of an account. We can expand the basic accounting equation to include the components of stockholders’ equity (common stock and retained earnings) and the components of retained earnings (revenues, expenses, and dividends). Because common stock and retained earnings are part of stockholders’ equity, it follows directly that we increase both with a credit. Revenues increase retained earnings (“there’s more to keep”). Retained earnings is a credit account, so we increase revenues with a credit. Expenses, on the other hand, decrease retained earnings (“there’s less to keep”). Thus, we do the opposite of what we do with revenues: We increase expenses with a debit. A debit to an expense is essentially a debit to retained earnings, decreasing the account. Similarly, dividends decrease retained earnings, so we also record an increase in dividends with a debit. 2-43

increase with debits or the left side of an account. Accounts on the right side of the accounting equation (liabilities and stockholders’ equity) increase with credits or the right side of an account. We can expand the basic accounting equation to include the components of stockholders’ equity (common stock and retained earnings) and the components of retained earnings (revenues, expenses, and dividends). Because common stock and retained earnings are part of stockholders’ equity, it follows directly that we increase both with a credit. Revenues increase retained earnings ( there’s more to keep ). Retained earnings is a credit account, so we increase revenues with a credit. Expenses, on the other hand, decrease retained earnings ( there’s less to keep ). Thus, we do the opposite of what we do with revenues: We increase expenses with a debit. A debit to an expense is essentially a debit to retained earnings, decreasing the account. Similarly, dividends decrease retained earnings, so we also record an increase in dividends with a debit")

44

For Step 3 - Ask yourself these questions…

First account affected by the transaction – debit or credit? Second account affected by the transaction – debit or credit? Do total debits equal total credits? Let’s look again at the transactions of Eagle Golf Academy, but this time using debits and credits rather than increases and decreases to record the account changes. As we do, ask yourself these three questions for each transaction: 1. “Is there an increase or decrease in the first account involved in the transaction? Should I record that increase or decrease with a debit or a credit?” 2. “Is there an increase or decrease in the second account involved in the transaction? Should I record that increase or decrease with a debit or a credit?” 3. “Do total debits equal total credits?” The answer to this last question must be “yes.” 2-44

45

Recall Our Example Eagle issues common stock for cash of $25,000 in transaction (1). 1. “Is there an increase or decrease in the first account involved in the transaction? Should I record that increase or decrease with a debit or a credit?” Answer: Cash increases. Cash is an asset, and assets have a debit balance. We record an increase in cash with a debit. 2. “Is there an increase or decrease in the second account involved in the transaction? Is that increase or decrease recorded with a debit or credit?” Answer: Common stock increases. Common stock is a stockholders’ equity account, and stockholders’ equity has a credit balance. We record an increase in common stock with a credit. 3. Do total debits equal total credits? Answer: Yes. 2-45

46

Recall Our Example The bank borrowing of $10,000 in transaction (2) has the following effects: 1. “Is there an increase or decrease in the first account involved in the transaction? Should I record that increase or decrease with a debit or a credit?” Answer: Cash increases. Cash is an asset, and assets have a debit balance. We record an increase to cash with a debit. 2. “Is there an increase or decrease in the second account involved in the transaction? Should I record that increase or decrease with a debit or a credit?” Answer: Notes payable increases. Notes payable is a liability, and liabilities have a credit balance. We record an increase to notes payable with a credit. 3. Do total debits equal total credits? Answer: Yes. So for the remaining transactions of Eagle Gold Academy, same procedure should be applied. 2-46

47

Check In – For transaction #4 – cash is a) debited or b) credited

Check In – For transaction #4 – cash is a) debited or b) credited. For transaction # 5 – supplies is a) debited or b) credited. Do transaction #3 on this power point

debited or b) credited. For transaction # 5 – supplies is a) debited or b) credited. Do transaction #3 on this power point.")

48

LO#4 and Step 4 Record Transactions in the ‘Journal’

CHRONOLOGICAL RECORD OF TRANSACTIONS Three steps Record debits first along with the $ amount. Record credits second along with the $ amount. The account name of the credits are always indented in the journal. Provide a description of the transaction (Not usually completed in class examples to save time) Accountants use a chronological record of transactions called a journal. The journalizing process follows three steps: 1. Specify each account affected by the transaction and classify each account by type (asset, liability, stockholders’ equity, revenue, or expense). 2. Determine whether each account is increased or decreased by the transaction. Use the rules of debit and credit to increase or decrease each account. Remember that the amount of the debits must equal the amount of the credits. 3. Record the transaction in the journal, including a brief explanation. The debit side is entered on the left margin, and the credit side is indented to the right. Step 3 is also called “making the journal entry” or “journalizing the transaction.” 48 48

Accountants use a chronological record of transactions called a journal. The journalizing process follows three steps: 1. Specify each account affected by the transaction and classify each account by type (asset, liability, stockholders’ equity, revenue, or expense). 2. Determine whether each account is increased or decreased by the transaction. Use the rules of debit and credit to increase or decrease each account. Remember that the amount of the debits must equal the amount of the credits. 3. Record the transaction in the journal, including a brief explanation. The debit side is entered on the left margin, and the credit side is indented to the right. Step 3 is also called making the journal entry or journalizing the transaction")

49

LO4 Record Transactions Using Debits and Credits

A journal provides a chronological record of all transactions affecting a firm. Think of recording a transaction as if you’re writing a sentence form of the “accounting language”. In transaction (1) On January 1, Eagle Golf Academy issues shares of common stock for cash of $25,000.” This same sentence written in the language of accounting above. This transaction causes total assets to increase (+A) and total stockholders’ equity to increase (+SE). In transaction (2), Eagle Academy borrows $10,000 from the bank. Eagle records the transaction as above. Both total assets and total liabilities increase by $10,000. Check in - Transactions 3 - 4 2-49

On January 1, Eagle Golf Academy issues shares of common stock for cash of $25,000. This same sentence written in the language of accounting above. This transaction causes total assets to increase (+A) and total stockholders’ equity to increase (+SE). In transaction (2), Eagle Academy borrows $10,000 from the bank. Eagle records the transaction as above. Both total assets and total liabilities increase by $10,000. Check in - Transactions")

52

LO #5 & Step 5 – Post Transactions to T-accounts in the General Ledger

The process of transferring the debit and credit information from the journal to individual accounts in the general ledger is called posting. A T-account is a simplified form of a general ledger account with space at the top for the account title and two sides for recording debits and credits. ACCOUNT TITLE DEBIT CREDIT The journal provides in a single location a chronological listing of every transaction affecting a company. As such, it serves as a handy way to review specific transactions that have occurred and to locate any accounting errors at their original source. But it’s not a convenient format for calculating account balances to use in preparing financial statements. To make the process more efficient, we transfer information about transactions recorded in the journal to the specific accounts in the general ledger. The general ledger includes all accounts used to record the company’s transactions. The process of transferring the debit and credit information from the journal to individual accounts in the general ledger is called posting. A T-account is a simplified form of a general ledger account with space at the top for the account title and two sides for recording debits and credits. 2-52

53

T-Account Account Title Left side Right side Debit

Normal balance for assets, treasury stock, dividends, expenses & losses Credit Normal balance for liabilities, common stock, paid-in-capital, retained earnings, revenue & gains An account can be represented by the letter T. We call them T-accounts. The vertical line in the letter divides the account into its two sides: left and right. The account title appears at the top of the T. The left side of each account is called the debit side, and the right side is called the credit side. Often, students are confused by the words debit and credit. Every business transaction involves both a debit and a credit. The debit side of an account shows what you received. The credit side shows what you gave. Copyright ©2010 Pearson Education Inc. Publishing as Prentice Hall.

54

Check in - #5 Transactions 4 & 9

Post Transactions to T-accounts in the General Ledger (shows cumulative totals for each account) Let’s see how debits and credits are posted to a T-account by looking in the slide where we have posted the cash transactions of Eagle Golf Academy (the corresponding transaction numbers are in parentheses). For each transaction that involves cash, we post the debit in the journal as a debit to the T-account. Similarly, we post every credit in the journal as a credit to the T-account. Notice that we can now easily calculate the ending balance of cash after collecting all cash transactions in one place. We calculate the ending balance of $6,200 by totaling all debits and subtracting the total of all credits. Note that we do not have to put “+” signs or “–” signs beside the numbers in the T-account. Because cash is an asset, an amount in the debit or left column always means an increase in the balance. An amount in the credit or right column always means a decrease in the balance. Check in - # Transactions 4 & 9 2-54

Let’s see how debits and credits are posted to a T-account by looking in the slide where we have posted the cash transactions of Eagle Golf Academy (the corresponding transaction numbers are in parentheses). For each transaction that involves cash, we post the debit in the journal as a debit to the T-account. Similarly, we post every credit in the journal as a credit to the T-account. Notice that we can now easily calculate the ending balance of cash after collecting all cash transactions in one place. We calculate the ending balance of $6,200 by totaling all debits and subtracting the total of all credits. Note that we do not have to put + signs or – signs beside the numbers in the T-account. Because cash is an asset, an amount in the debit or left column always means an increase in the balance. An amount in the credit or right column always means a decrease in the balance. Check in - #5 Transactions 4 &")

56

Review of the purpose for the Journal and General Ledger

RECORD in journal - MEASURE Each journal entry is limited to one specific transaction Cumulative entries of all individual transactions in organization POST transactions to the general ledger – Begin AGGREGATION Cumulative balance for each account (account specific) – the aggregation part…

– the aggregation part…")

57

In-Class Exercise On 1/1 Seventh Investments, Inc., began by issuing common stock for $140,000 in exchange for cash. The company immediately purchased computer equipment for $100,000 using cash. Set up the following general ledger T-accounts of Seventh Investments, Inc.: Cash, Equipment, Accounts Payable (A/P), Common Stock (C.S). 1. Record in the journal. 2. Post in the General Ledger. 3. Show that total debits equals total credits.

, Common Stock (C.S). 1. Record in the journal. 2. Post in the General Ledger. 3. Show that total debits equals total credits.")

58

What is the total $ amount of all of the debits from the two journal entries? A) $140,000; B) $240,000; C)$480,000; D) $100,000 What is the cash balance after posting to the general ledger? A) $240,000; B) (-40,000); C)$40,000; D) $100,000

$240,000; B) (-40,000); C)$40,000; D) $100,000.")

59

Summary of the Expanded Measurement Process

To better understand the measurement of external transactions, let’s apply the first five steps outlined in the slide to the first transactions of Eagle Golf Academy. 2-59

60

LO6 & Step 6 Prepare a Trial Balance

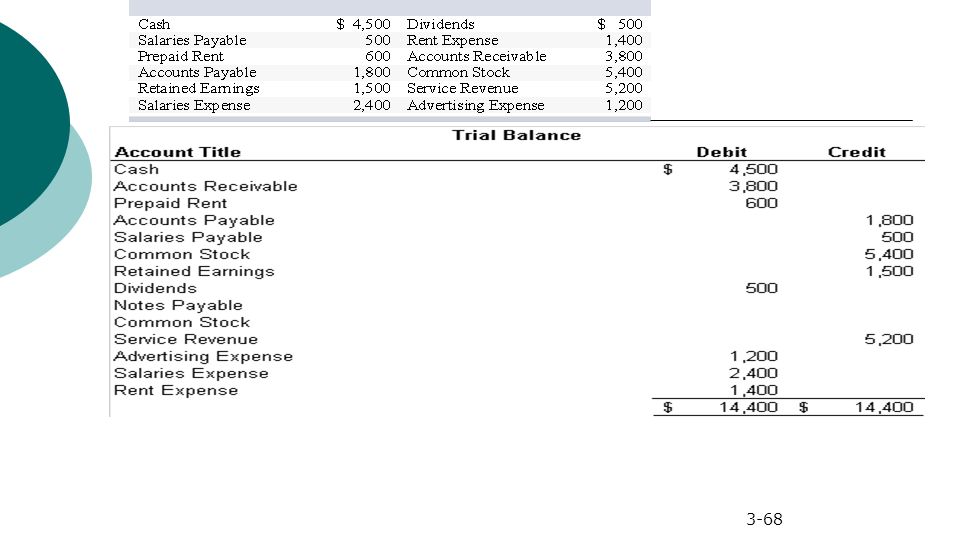

A trial balance is a list of all accounts and their aggregated totals at a particular date, showing that total debits equal total credits (Balance). Another purpose of the trial balance is to assist us in preparing adjusting entries (for end of the period transactions – chapter 3). It is not a published financial statement to be used by external parties, there is no required order for listing accounts in the trial balance, but it typically shows First, the balance sheet accounts, Second, statement of stockholders’ equity, and Lastly, the Income Statement. The trial balance is used for internal purposes only and provides a check on the equality of the debits and credits. A trial balance is a list of all accounts and their balances at a particular date, showing that total debits equal total credits. Another purpose of the trial balance is to assist us in preparing adjusting entries (for internal transactions). We discuss adjusting entries in Chapter 3. Since the trial balance is not a published financial statement to be used by external parties, there is no required order for listing accounts in the trial balance. The trial balance is used for internal purposes only and provides a check on the equality of the debits and credits. However, most companies list accounts in the following order: assets, liabilities, stockholders’ equity, dividends, revenues, and expenses. 2-60

. Another purpose of the trial balance is to assist us in preparing adjusting entries (for end of the period transactions – chapter 3). It is not a published financial statement to be used by external parties, there is no required order for listing accounts in the trial balance, but it typically shows. First, the balance sheet accounts, Second, statement of stockholders’ equity, and. Lastly, the Income Statement. The trial balance is used for internal purposes only and provides a check on the equality of the debits and credits. A trial balance is a list of all accounts and their balances at a particular date, showing that total debits equal total credits. Another purpose of the trial balance is to assist us in preparing adjusting entries (for internal transactions). We discuss adjusting entries in Chapter 3. Since the trial balance is not a published financial statement to be used by external parties, there is no required order for listing accounts in the trial balance. The trial balance is used for internal purposes only and provides a check on the equality of the debits and credits. However, most companies list accounts in the following order: assets, liabilities, stockholders’ equity, dividends, revenues, and expenses")

61

Unadjusted Trial Balance of Eagle Golf Academy

Notice that accounts are listed with the debit balances in one column and the credit balances in another column. Asset, expense, and dividend accounts normally have debit balances, while liability, stockholders’ equity, and revenue accounts normally have credit balances. It may seem unusual that the retained earnings account has a balance of $0. As we explained earlier, retained earnings is a composite of three other types of accounts—revenues, expenses, and dividends. Those three accounts have balances at this point, but those balances haven’t yet been transferred to retained earnings. This transfer is known as the closing process and we will discuss it in Chapter 3. Since this is the first period of the company’s operations, retained earnings will start at $0. As time goes by, the retained earnings balance will be the accumulated net amount of revenues minus expenses and dividends. 2-61

62

For the accounting cycle, Steps 2, 3 & 4 are combined together into the Record Journal Entry Step.

Step 2 - Analyze the impact of the transaction on the accounting equation Step 3 - Assess whether the transaction results in a debit or credit Step 4 – “Record the transaction. ”

63

Brief Exercise 2-4 Analyze the impact of transactions on the accounting equation [LO2]

Assets = Liabilities + Stockholders’ Equity

![Brief Exercise 2-4 Analyze the impact of transactions on the accounting equation [LO2]](http://slideplayer.com/slide/10502559/35/images/63/Brief+Exercise+2-4+Analyze+the+impact+of+transactions+on+the+accounting+equation+%5BLO2%5D.jpg "Assets = Liabilities + Stockholders’ Equity.")

64

DEBIT – Balance???

65

CREDIT – Balance???

67

Cash Balance??

69

UTE SEWING SHOP Transactions for March: March 1

Transactions for March: March 1 Issues common stock for cash $ ,000 March 3 Purchases sewing equipment with bank note $ ,700 March 5 Pays rent for March $ March 7 Alterations performed on account $ 1.) Prepare Journal Entries 2.) Post journal entries to general ledger T accounts 3.) Prepare Trial Balance

Prepare Journal Entries. 2.) Post journal entries to general ledger T accounts. 3.) Prepare Trial Balance.")

70

Journal Entries

71

General Ledger

72

Trial Balance

73

Trial Balance

74

Learning Objectives Steps for measuring ‘During the Period’ (external) Transactions. Analyze the transaction using the Accounting Equation. Analyze the transaction using the Accounting Equation and debits/credits. Record the transaction in the Journal. Post the transaction to the General Ledger. Unadjusted Trial Balance.

75

Chapter 2 Participation Questions

Why are there Accounting Principles and Rules, such as GAAP, to guide modern financial accounting and the preparation of financial statements in North America? To build consistency in the financial statements; To make it more difficult to prepare financial statements; or To develop a level of confusion in the financial statements based on too many rules. What is the actual origin of the terms debit and credit? They are philosophical terms that are used in accounting; They are both ancient mathematical terms; or No one really knows where they originated, but they have been in use for in excess of 500 years. What does CPA stand for? Confirmed 'Perfect' Accounting; Certified 'Public' Accountant; or Committed Person in Accounting What was the name of the Company used for the final in-lecture problem at the very end of class where we assembled an unadjusted trial balance? ABC Construction; UTE Sewing Shop; or JRB Law Firm What is the minimum number of entries for each transaction in double entry accounting? One; two; or three

76

End of chapter 02 2-76

Similar presentations