Download presentation

Presentation is loading. Please wait.

1

Valuation of HCC For Acquisition by Gammon Group # 6 Ritu Mehlawat (034) Sabyasachi Panda (039) Saumya Prakash (045) Stambhit Saha (055) Nishant Kumar (103)

Sabyasachi Panda (039) Saumya Prakash (045) Stambhit Saha (055) Nishant Kumar (103)")

2

Overview of the Presentation Part 1: Due Diligence of HCC Part 1: Due Diligence of HCC Construction Industry – Global & Indian Scenario Construction Industry – Global & Indian Scenario Snapshot of Hindustan Construction Company Snapshot of Hindustan Construction Company Analysis of projects Analysis of projects Past and ongoing projects in Power, Transportation, Irrigation Past and ongoing projects in Power, Transportation, Irrigation Overview of the business strategy Overview of the business strategy Past Financials & Accounting Policy Past Financials & Accounting Policy Part 2: Valuation of HCC Part 2: Valuation of HCC Valuation using Comparables Valuation using Comparables Valuation using DCF Valuation using DCF Sensitivity Analysis – WACC, growth rate, RM prices Sensitivity Analysis – WACC, growth rate, RM prices

3

Overview of the Presentation Part 3: Overview of Gammon India Part 3: Overview of Gammon India Overview of the company Overview of the company Ongoing projects Ongoing projects Past Financials Past Financials Part 4: Investment Perspective for M&A Part 4: Investment Perspective for M&A Concerns about Construction Sector & Risks of proposed M&A Concerns about Construction Sector & Risks of proposed M&A Argument in favour of investment in HCC Argument in favour of investment in HCC Synergy benefits for Gammon from M&A Synergy benefits for Gammon from M&A Part 5: Deal Structure & Transaction Details Part 5: Deal Structure & Transaction Details Rationale for Stock Offer Method of Payment Rationale for Stock Offer Method of Payment Structure of the Deal Structure of the Deal Appendix Appendix

4

Part 1: Due Diligence of HCC

5

The Construction Sector Global & Indian Scenario

6

Snapshot of Global Construction Industry Global scenario is on the growing path Global scenario is on the growing path The forecasted CAGR of the total spending is 6.7% The forecasted CAGR of the total spending is 6.7% Expected order book is Rs.1350 billion by year 2010 Expected order book is Rs.1350 billion by year 2010

7

Growth in Order Book Size Worldwide

8

Global Construction Spending Source: www.globalinsight.com

9

Where Indian Construction Industry Stands Source: www.globalinsight.com High Growth Phase

10

Snapshot of Indian Construction Industry Indian Construction industry accounts for nearly: Indian Construction industry accounts for nearly: 12.5% of the India’s GDP and 13% of the gross fixed capital formation 12.5% of the India’s GDP and 13% of the gross fixed capital formation Nearly 2% of the global construction market Nearly 2% of the global construction market Estimated revenue CAGR (FY 2005–09E)- 20% Recorded the highest construction spending growth in FY2005- 06 driven by the infrastructure and real estate sectors Introduction of Real Estate Investment Trusts (REITs) by mobilizing capital markets will further accelerate real estate growth Technological developments like ready-mix concrete, 3-D modeling, and mobile computing are gradually being adopted

- 20% Recorded the highest construction spending growth in FY driven by the infrastructure and real estate sectors Introduction of Real Estate Investment Trusts (REITs) by mobilizing capital markets will further accelerate real estate growth Technological developments like ready-mix concrete, 3-D modeling, and mobile computing are gradually being adopted")

11

Snapshot of Indian Construction Industry Increased government commitment and dedicated funding for Infrastructure Projects Increased government commitment and dedicated funding for Infrastructure Projects Strengthening of Institutional capacity for implementation Strengthening of Institutional capacity for implementation Funding from Multilateral agencies (FDI) Funding from Multilateral agencies (FDI) Private participation to bridge funding gap Private participation to bridge funding gap Tax benefits accorded to the sector Tax benefits accorded to the sector Introduction of viability gap funding and annuity mechanism Introduction of viability gap funding and annuity mechanism Strong possibility of EBITDA margin expansion Strong possibility of EBITDA margin expansion Increase in net worth of companies has improved their bidding capacity Increase in net worth of companies has improved their bidding capacity

Funding from Multilateral agencies (FDI) Private participation to bridge funding gap Private participation to bridge funding gap Tax benefits accorded to the sector Tax benefits accorded to the sector Introduction of viability gap funding and annuity mechanism Introduction of viability gap funding and annuity mechanism Strong possibility of EBITDA margin expansion Strong possibility of EBITDA margin expansion Increase in net worth of companies has improved their bidding capacity Increase in net worth of companies has improved their bidding capacity")

12

Industry Segments Segment Current Status Future Growth Prospects Housing Largest and most fragmented segment Largest and most fragmented segment Large number of small builders Large number of small builders Very few big builders: DLF Very few big builders: DLF Single Houses-large Housing Colony Single Houses-large Housing Colony Entry of foreign players Entry of foreign players Infrastructure Second Largest and least fragmented sector Second Largest and least fragmented sector Roads-low technical complexity- fragmented Roads-low technical complexity- fragmented Hydropower, tunnels only 4-5 players Hydropower, tunnels only 4-5 players More organized: Increased Complexity, technical expertise, size of contract More organized: Increased Complexity, technical expertise, size of contract Large players to grow market share Large players to grow market share Industrial Fragmented-Pricing main criteria Fragmented-Pricing main criteria Will remain unchanged Will remain unchanged Capex revival –increased Capex revival –increasedspending Retail/Commercial Fragmented Fragmented Presence of large players increasing Presence of large players increasing Large companies will gain share with expansion of retail space projects Large companies will gain share with expansion of retail space projects Source: Morgan Stanley Research

13

Projected Infrastructure Spending in India SECTORCAGR(FY09-FY05) Electricity, Gas and Water Supply 13% - Electricity - Electricity10% - Gas - Gas22% - Water Supply and others - Water Supply and others10% Transport, Storage & Commercial 21% - Railways - Railways25% - Roads - Roads29% - Ports - Ports30% Source: Morgan Stanley Research estimates

Electricity, Gas and Water Supply 13% - Electricity - Electricity10% - Gas - Gas22% - Water Supply and others - Water Supply and others10% Transport, Storage & Commercial 21% - Railways - Railways25% - Roads - Roads29% - Ports - Ports30% Source: Morgan Stanley Research estimates")

14

Infrastructure Potential Over Next 5 Yrs

15

Ranking of Major Indian Players by Sales (Rs Crore) Source: Company financial statements CompanyRank Order Backlog FY06 Order Booking FY06Sales FY 06 OrderBooking (Q1) FY07 L&T12466422318147636326 Jai Prakash 23651 HCC3967262811990.145 Nagarjuna45428367618401101 IVRCL5625053001495877 Gammon66500151914831519

Source: Company financial statements CompanyRank Order Backlog FY06 Order Booking FY06Sales FY 06 OrderBooking (Q1) FY07 L&T Jai Prakash HCC Nagarjuna IVRCL Gammon")

16

Quarterly Variation of Margins HCC

17

Revenue Breakup by Industry Segments %HCCGammonNCCIVRCLMPLL&TJAL Roads344743225925- Power351748-5100 Water & Irrigation 2610365038-- Industrial Structures -51720--- Others521--470- Total100100100100100100100 Source: Company

18

Impact of Hike in Costs and Interest Rate on Infrastructure Projects Equity IRR (basis points) Impact on Equity (NPV) Remark(s) Rise in project cost (10%) (150-250)(10-14%) Higher gearing, lower the impact Rise in interest cost (+1%) (40-120)(10-16%) Higher gearing, higher the impact Rise in toll rate (+1%) 130-30020-33% High traffic density corridors to benefit Rise in discount rate (+1%) (9-17%) Higher gearing, higher the impact Overall impact (40) - 40 (0-10%) Primarily offset by increase in toll revenues Source: SSKI Research

Impact on Equity (NPV) Remark(s) Rise in project cost (10%) ( )(10-14%) Higher gearing, lower the impact Rise in interest cost (+1%) (40-120)(10-16%) Higher gearing, higher the impact Rise in toll rate (+1%) % High traffic density corridors to benefit Rise in discount rate (+1%) (9-17%) Higher gearing, higher the impact Overall impact (40) - 40 (0-10%) Primarily offset by increase in toll revenues Source: SSKI Research")

19

Hindustan Construction Company (HCC)

")

20

Background Incorporated: 1926 Incorporated: 1926 Ownership: Gulabchand Doshi Group Ownership: Gulabchand Doshi Group Registered HQ: Mumbai Registered HQ: Mumbai HCC is one of the oldest and largest construction companies in India with pre-qualification skills and proven execution capabilities across sectors like power, roads, bridges, ports HCC is one of the oldest and largest construction companies in India with pre-qualification skills and proven execution capabilities across sectors like power, roads, bridges, ports HCC specializes in the construction of technologically complex and long- gestation period projects HCC specializes in the construction of technologically complex and long- gestation period projects The company has successfully and gradually transformed from a civil engineering contractor to an integrated EPC executor The company has successfully and gradually transformed from a civil engineering contractor to an integrated EPC executor Known for taking giant strides in technology and innovation Known for taking giant strides in technology and innovation First construction company in India to be certified for First construction company in India to be certified for ISO 9001, ISO 14001 and OHSAS 18001 ISO 9001, ISO 14001 and OHSAS 18001 for its Quality, Environmental and Occupational Health & Safety Management System for its Quality, Environmental and Occupational Health & Safety Management System

21

HCC - Subsidiary Companies Subsidiary Companies Western Securities Ltd. Western Securities Ltd. Pune Paud Toll Road Co. Ltd. Pune Paud Toll Road Co. Ltd. Hincon Technoconsult Ltd. Hincon Technoconsult Ltd. H C C Infotech Lt H C C Infotech Lt Parties Where Control Exists Nathpa Jhakri Joint Venture Nathpa Jhakri Joint Venture Lavasa Corporation Ltd. Lavasa Corporation Ltd. Kumagal-Skanska-Hcc-Itochu Group Kumagal-Skanska-Hcc-Itochu Group Hcc-Pati Joint Venture Hcc-Pati Joint Venture Hcc-L & T Purulia Joint Venture Hcc-L & T Purulia Joint Venture

22

Product Portfolio Project assignments across diverse sectors Project assignments across diverse sectors Transportation, nuclear & hydro power generation Transportation, nuclear & hydro power generation Water supply and irrigation Water supply and irrigation Dams Dams Barrages Barrages Tunnels Tunnels Current project Portfolio consists of: Current project Portfolio consists of: 6 Hydel Project contracts 6 Hydel Project contracts 4 Nuclear Project contracts 4 Nuclear Project contracts 20 Transportation Project contracts 20 Transportation Project contracts 4 Water Supply and Irrigation Project contracts 4 Water Supply and Irrigation Project contracts

23

Source: Company – Financial Reports Order Book in FY’06

24

Order Bookings During FY’06 Order book has grown at Order book has grown at CAGR of 20% since 2002 CAGR of 20% since 2002 Currently stands at over Rs.9692 crores Currently stands at over Rs.9692 crores Almost five times its FY 2005-06 turnover Almost five times its FY 2005-06 turnover Out of the total order book Out of the total order book Hydel power project for Savalkote (Rs 1900 crore) is 7 years duration Hydel power project for Savalkote (Rs 1900 crore) is 7 years duration Rest all are average of about 3 years duration Rest all are average of about 3 years duration

is 7 years duration Hydel power project for Savalkote (Rs 1900 crore) is 7 years duration Rest all are average of about 3 years duration Rest all are average of about 3 years duration")

25

HCC - Recent Performance (05-06) Order book increased by 80% Order book increased by 80% From Rs 5381 crore on Mar`05 to Rs 9672 crore on 31 st March 2006 From Rs 5381 crore on Mar`05 to Rs 9672 crore on 31 st March 2006 Revenue from operations increased by 28.7% ( Rs 2028 crore ) Revenue from operations increased by 28.7% ( Rs 2028 crore ) Profits after tax increased by 68.6% Profits after tax increased by 68.6% Rs 74 crore to Rs 124.8 crore Rs 74 crore to Rs 124.8 crore EBDITA margin improved to 9.38 % from 8.53% PY EBDITA margin improved to 9.38 % from 8.53% PY 35 projects under execution 35 projects under execution Out of 35 projects,18 projects are under mobilization or non revenue recognition stage Out of 35 projects,18 projects are under mobilization or non revenue recognition stage 4 running project lost planned work due to heavy rains and flooding 4 running project lost planned work due to heavy rains and flooding

Order book increased by 80% Order book increased by 80% From Rs 5381 crore on Mar`05 to Rs 9672 crore on 31 st March 2006 From Rs 5381 crore on Mar`05 to Rs 9672 crore on 31 st March 2006 Revenue from operations increased by 28.7% ( Rs 2028 crore ) Revenue from operations increased by 28.7% ( Rs 2028 crore ) Profits after tax increased by 68.6% Profits after tax increased by 68.6% Rs 74 crore to Rs crore Rs 74 crore to Rs crore EBDITA margin improved to 9.38 % from 8.53% PY EBDITA margin improved to 9.38 % from 8.53% PY 35 projects under execution 35 projects under execution Out of 35 projects,18 projects are under mobilization or non revenue recognition stage Out of 35 projects,18 projects are under mobilization or non revenue recognition stage 4 running project lost planned work due to heavy rains and flooding 4 running project lost planned work due to heavy rains and flooding")

26

Analysis of HCC Projects

27

Power Projects in India 131,400 MW of electricity generation with 76% controlled by the public sector Efficiency Metric Efficiency Metric Industrial users pay 2.5 times that of China for electricity. Cross subsidization for electricity supplied to farmers/residential users is very high High level of theft is an added issue. Current Spending p.a. - Current Spending p.a. - US$6.5 bn (0.9% of GDP) Estimated Spending (F2009) p.a - Estimated Spending (F2009) p.a - US$ 9.7 bn (1% of GDP) Major Policy Initiatives Major Policy Initiatives Accelerated Power Development Program Enactment and Implementation of Electricity Act Funding Plans Funding Plans About 20% of the generation capacity will come from the private sector (developed for captive use) Balance of 80% from the public sector

Estimated Spending (F2009) p.a - Estimated Spending (F2009) p.a - US$ 9.7 bn (1% of GDP) Major Policy Initiatives Major Policy Initiatives Accelerated Power Development Program Enactment and Implementation of Electricity Act Funding Plans Funding Plans About 20% of the generation capacity will come from the private sector (developed for captive use) Balance of 80% from the public sector.")

28

HCC - Power Projects Completed in the Past ProjectYear 1,020 MW Tala Hydroelectric Project, which involved a 92 m high dam and 13 km of tunnels with three desilting chambers - Bhutan 2005 1,500 MW Napth Jhakri Power Project, which involved 11 km of tunnels and 294 m of shafting. - India 2002 1,000 MW Koyna Hydroelectric Project – the company was involved in all four stages of India’s second largest underground power station - Koyna 2000 Rajasthan Atomic Power Project – India’s first indigenously designed and built nuclear power plants. Units 1 and 2 were built in 1973, and units 3 and 4 were built in 2000. The company is currently constructing units 5 and 6. - Rajasthan 2000

29

HCC - Ongoing Power Projects Project Value (Rs Crore) Purulia Pumped Storage Project West Bengal - Construction of a powerhouse and allied tunnels of 900 MW project 220 Uri Hydroelectric Project (J&K) - Construction of a 240 MW underground power station powerhouse including dam, tunnels and shafts 575 Kudankulam Nuclear Power Project (Tamil Nadu) - Civil construction of two reactor units of 1,000 MW each 273 Rajasthan Atomic Power Project (Rajasthan) - Civil works for reactor units 5 and 6 of 220 MW each, and other ancillary buildings 238 Kudankulam Nuclear Power Project (Tamil Nadu) - Construction of breakwater, pump houses, intake structures, seawater pipelines, chlorination plant, discharge channels and other related works 349

Purulia Pumped Storage Project West Bengal - Construction of a powerhouse and allied tunnels of 900 MW project 220 Uri Hydroelectric Project (J&K) - Construction of a 240 MW underground power station powerhouse including dam, tunnels and shafts 575 Kudankulam Nuclear Power Project (Tamil Nadu) - Civil construction of two reactor units of 1,000 MW each 273 Rajasthan Atomic Power Project (Rajasthan) - Civil works for reactor units 5 and 6 of 220 MW each, and other ancillary buildings 238 Kudankulam Nuclear Power Project (Tamil Nadu) - Construction of breakwater, pump houses, intake structures, seawater pipelines, chlorination plant, discharge channels and other related works 349")

30

Transportation Projects in India : Roads Road and highways network covers 3.3 mn kms and 0.2 mn kms, respectively Efficiency Metric Efficiency Metric Only 9% of India's national highways are four-laned Average speed is less than 50 km/hour Current Spending p.a. Current Spending p.a. - US$2.5-3 bn (0.4% of GDP) Estimated Spending (F2009) Estimated Spending (F2009) - US$ 6.2 bn (0.6% of GDP) Major Policy Initiatives Major Policy Initiatives Seven Phase National Highway Development Program Funding Plans Funding Plans Earmarked revenues collected from levy on petroleum products Seeking private sector participation by providing capital grants and long-term annuity support

Estimated Spending (F2009) Estimated Spending (F2009) - US$ 6.2 bn (0.6% of GDP) Major Policy Initiatives Major Policy Initiatives Seven Phase National Highway Development Program Funding Plans Funding Plans Earmarked revenues collected from levy on petroleum products Seeking private sector participation by providing capital grants and long-term annuity support.")

31

Transportation Projects in India : Railways Rail network spans 63,000 kms and carries 14 million passengers and 1.5 million tonnes of freight daily Efficiency Metric Efficiency Metric The Chinese railways’output in traffic units is 2.5 times that of the Indian railways Current Spending p.a. Current Spending p.a. -US$3.1 bn (0.4% of GDP) Estimated Spending (F2009) - Estimated Spending (F2009) - US$ 7.5 bn (0.8% of GDP) Major Policy Initiatives Major Policy Initiatives Greenfield railway network dedicated for freight traffic (Freight Corridor) Greenfield metro projects at Hyderabad, Bangalore and Mumbai Funding Plans Funding Plans - Projects to be largely funded by the public sector (central and state governments) -Japanese government has agreed to fund US$ 4 bn (30%) of the cost of the Rail Freight Corridor project

Estimated Spending (F2009) - Estimated Spending (F2009) - US$ 7.5 bn (0.8% of GDP) Major Policy Initiatives Major Policy Initiatives Greenfield railway network dedicated for freight traffic (Freight Corridor) Greenfield metro projects at Hyderabad, Bangalore and Mumbai Funding Plans Funding Plans - Projects to be largely funded by the public sector (central and state governments) -Japanese government has agreed to fund US$ 4 bn (30%) of the cost of the Rail Freight Corridor project.")

32

HCC - Transportation Projects Completed in the Past ProjectYear Delhi Metro Rail Corridor – 4 km underground section, including station buildings - Delhi 2004 West Bengal Road Project – one of the largest road packages awarded by the National Highways – West Bengal 2004 Mumbai-Pune Expressway – India’s first concrete paved expressway – Mumbai 2000

33

HCC - Ongoing Transportation Projects Project Value (Rs Crore) Allahabad bypass project - Construction of a 40 km four lane concrete road with bridges as part of the Allahabad bypass. The project aided by the World Bank 447 Chennai bypass CBP2 - Construction of 32.5 km of highways with 3 km of elevated structures as part of the Chennai bypass project 405 Source: B&K

34

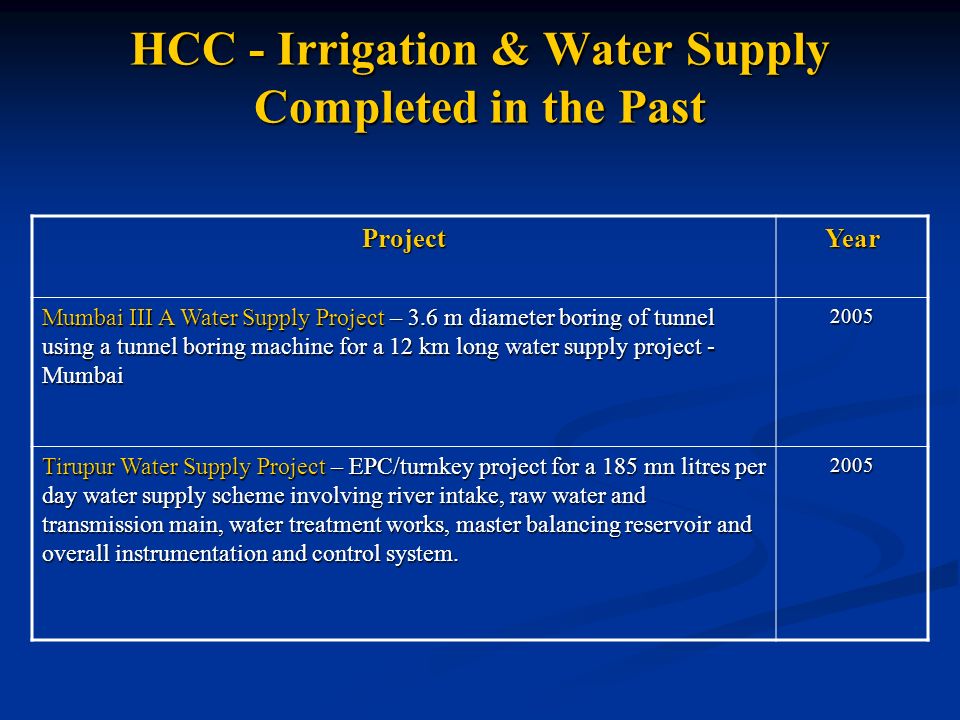

HCC - Irrigation & Water Supply Completed in the Past ProjectYear Mumbai III A Water Supply Project – 3.6 m diameter boring of tunnel using a tunnel boring machine for a 12 km long water supply project - Mumbai 2005 Tirupur Water Supply Project – EPC/turnkey project for a 185 mn litres per day water supply scheme involving river intake, raw water and transmission main, water treatment works, master balancing reservoir and overall instrumentation and control system. 2005

35

HCC - Ongoing Irrigation and Water Supply Projects Project Value (Rs Crore) Godavari Lift Irrigation Scheme Phase I (Andhra Pradesh) EPC/turnkey project for 135 km long water pipeline with intake and three intermediate pumping stations for 10 cumec lift irrigation scheme 844 Godavari Lift Irrigation Scheme Phase II (Andhra Pradesh) 1887 Source: B&K

Godavari Lift Irrigation Scheme Phase I (Andhra Pradesh) EPC/turnkey project for 135 km long water pipeline with intake and three intermediate pumping stations for 10 cumec lift irrigation scheme 844 Godavari Lift Irrigation Scheme Phase II (Andhra Pradesh) 1887 Source: B&K")

36

HCC - Others Projects Completed in the Past ProjectYear Bandra Influent and Effluent Treatment Plant – first twin shaft pumping station in India with a capacity of 1,800 mn litres per day for discharging sewage into the sea. 2003 Lagoon works at Ghatkopar and Bhandup (Mumbai) – civil works for 285 mn litres per day aerated lagoons. 2001

– civil works for 285 mn litres per day aerated lagoons")

37

HCC - Others Ongoing Projects Project Value (Rs Crore) Lavasa Township of 10,000 acres 566 Kalol Mehsana gas pipeline (Gujarat) 41 km pipeline and 18 km 550 spur pipeline 55 Source: B&K

Lavasa Township of 10,000 acres 566 Kalol Mehsana gas pipeline (Gujarat) 41 km pipeline and 18 km 550 spur pipeline 55 Source: B&K")

38

HCC - Change in Revenue Breakup Source : B&K

39

Change in Order Book Composition Order Book Composition (%) Sep – 06 Mar – 06 Sep - 05 Power (Hydro and Nuclear) 473812 Transportation384344 Water Supply / Irrigation 111535 Others449 Source: Company

Sep – 06 Mar – 06 Sep - 05 Power (Hydro and Nuclear) Transportation Water Supply / Irrigation Others449 Source: Company")

40

Overview of HCC Business Strategy

41

HCC - Business Strategy YOY growth in absolute terms YOY growth in absolute terms Low value addition & high turnover project - Pipes, Roads Low value addition & high turnover project - Pipes, Roads High value addition but low turnover project - Hydel or Nuclear Power; Bridges High value addition but low turnover project - Hydel or Nuclear Power; Bridges Selectively bid for BOT/ EPC/ Turnkey projects Selectively bid for BOT/ EPC/ Turnkey projects BOT projects BOT projects Higher risk & higher reward than construction projects Higher risk & higher reward than construction projects Main challenge to execute on time Main challenge to execute on time Delay -> Construction cost increases Delay -> Construction cost increases Reduced concession period Reduced concession period New BOT projects: lower margins( interest cost ) New BOT projects: lower margins( interest cost ) Annuity & shadow tolling projects Annuity & shadow tolling projects less risky : limited upside less risky : limited upside Enhance capital efficiency Enhance capital efficiency Attract, train & retain trained personnel Attract, train & retain trained personnel

New BOT projects: lower margins( interest cost ) Annuity & shadow tolling projects Annuity & shadow tolling projects less risky : limited upside less risky : limited upside Enhance capital efficiency Enhance capital efficiency Attract, train & retain trained personnel Attract, train & retain trained personnel")

42

HCC - Past Financials

43

YOY Change in Net Margins (%)

")

44

YOY Change in Operating Margins (%)

")

45

Share Price Movement Over the Past One Year Source: BSE Website HCC BSE Construction Index

46

Financial Highlights Particular31.3.0531.3.06 Share Capital 35.6238.32 Net Worth 350.42842.17 PAT74.02124.80 Net Fixed Assets 446.22604.32 Net Current Assets 112.051365.23 Source: Company In Crores

47

Summary P/L Account Particular`04`05`06 Net Sales 1171.791633.911564.71 Other Income 1.645.7912.02 Expenditure1026.911445.311851.28 PBDIT147.52171.24199.48 Depreciation46.2746.8854.22 Interest39.2042.7348.65 PBT62.0581.6396.61 PAT36.2771.3979.37 Source: Company In Crores

48

Summary Balance Sheet Particular`04`05`06 Share Capital 20.5335.6238.32 Reserves &Surplus 143.89327.43816.08 Loans433.524311316.28 Net Fixed Assets 381.43446.22604.32 Investments41.79181.6772.65 Net Current Assets 129.09112.051365.23 Source: Company In Crores

49

Key Ratios Particular`04`05`06 Current Ratio 1.2421.1672.451 Debt/Equity2.5601.2061.459 RONW(%)23.33%24.54%12.50% ROCE(%)33.56%30.15%15.03% EPS17.1731.434.77 Dividend(%)50%60%70% Source: Company In crores

23.33%24.54%12.50% ROCE(%)33.56%30.15%15.03% EPS Dividend(%)50%60%70% Source: Company In crores")

50

Financial Projections for the Company Particular`07`08 Net Sales 2547.83312.7 EBITDA220.6309.1 Tax104.7130.6 EBIT154.8230.9 Net Profit 116178.6 ROE(%)12%17% ROCE(%)8%12% In Crores

12%17% ROCE(%)8%12% In Crores")

51

Capital History Security Type: FCD, ECB, PCD, Equity, Global Depository Receipts Security Type: FCD, ECB, PCD, Equity, Global Depository Receipts Bonus Issue in June 1995 in ratio of 1:1 Bonus Issue in June 1995 in ratio of 1:1 Dividends: Dividends: Year Rate of Dividend March 2004 50% March 2005 60% March 2006 70%

52

Shareholding Pattern

53

Share Capital Total Number of Shares 25,62,49,600 Total Number of Shares 25,62,49,600 Par Value of 1 Share Rs.10 Par Value of 1 Share Rs.10 Market Price as on 29th January Rs.147.65 Market Price as on 29th January Rs.147.65 Shareholding as on June 06: Shareholding as on June 06: Promoters holding 46.93% :Breakup Promoters holding 46.93% :BreakupBreakup Non Promoters holding 47.60% : Breakup Non Promoters holding 47.60% : BreakupBreakup Custodians holding 5.47% Custodians holding 5.47%

54

Borrowings Year200420052006 Secured195.93218.19197.33 Unsecured223.62207.491100.52 Current portion of long term debt 08.679.81 In Rs. Crores Debt Equity Ratio in the year 2006 is 1.459 Industry Average is 1.20 Contingent Liabilities

55

Recent Financing Instruments Used to Fund Growth USD 100 million through a GDS placement USD 100 million through a GDS placement 2.69Cr GDS issued at Rs. 167 per share 2.69Cr GDS issued at Rs. 167 per share USD 100 million as unsecured loans - FCCB USD 100 million as unsecured loans - FCCB On conversion equity base would increase by 4% On conversion equity base would increase by 4% USD 200 million (Rs 878.7 crore net of issue expenses) will be utilized for USD 200 million (Rs 878.7 crore net of issue expenses) will be utilized for USD 100 million deployed in construction business & capital expenditure USD 100 million deployed in construction business & capital expenditure USD 50 million in Hincon Realty (real estate arm) USD 50 million in Hincon Realty (real estate arm) USD 50 million for funding SPVs for (BOT) power project USD 50 million for funding SPVs for (BOT) power project

will be utilized for USD 200 million (Rs crore net of issue expenses) will be utilized for USD 100 million deployed in construction business & capital expenditure USD 100 million deployed in construction business & capital expenditure USD 50 million in Hincon Realty (real estate arm) USD 50 million in Hincon Realty (real estate arm) USD 50 million for funding SPVs for (BOT) power project USD 50 million for funding SPVs for (BOT) power project.")

56

Accounting Policies - HCC

57

Revenue Recognition Policy (For Construction Contracts) The Company follows percentage completion method The Company follows percentage completion method Stated on the basis of physical measurement of work actually completed at the balance sheet date taking into account the contractual price and revision thereto. Stated on the basis of physical measurement of work actually completed at the balance sheet date taking into account the contractual price and revision thereto. The site mobilization expenditure for site installation is apportioned over the period of contract in proportion to the value of work done The site mobilization expenditure for site installation is apportioned over the period of contract in proportion to the value of work done Losses on contracts are fully accounted for as and when incurred Losses on contracts are fully accounted for as and when incurred Foreseeable losses are accounted for when they are determined except to the extent they are expected to be recovered through claims presented or to be presented to the customer or in arbitration. Foreseeable losses are accounted for when they are determined except to the extent they are expected to be recovered through claims presented or to be presented to the customer or in arbitration.

58

Revenue Recognition for JV Contracts executed in Joint Venture under work sharing arrangement are accounted in accordance with the accounting policy followed by the company as that of an independent contract to the extent work is executed. Contracts executed in Joint Venture under work sharing arrangement are accounted in accordance with the accounting policy followed by the company as that of an independent contract to the extent work is executed. In respect of contracts executed in Integrated Joint Ventures under profit sharing arrangement (assessed as AOP under Income tax laws), the services rendered to the Joint Ventures are accounted as income on accrual basis. The profit / loss is accounted for, as and when it is determined by the Joint Venture and the net investment in the Joint Venture is reflected as investments, loans & advances or current liabilities. In respect of contracts executed in Integrated Joint Ventures under profit sharing arrangement (assessed as AOP under Income tax laws), the services rendered to the Joint Ventures are accounted as income on accrual basis. The profit / loss is accounted for, as and when it is determined by the Joint Venture and the net investment in the Joint Venture is reflected as investments, loans & advances or current liabilities. Expenditure incurred in respect of additional costs/delays are accounted in the year in which they are incurred. Claims made in respect thereof are accounted as income in the year of receipt of arbitration award or acceptance by client. Expenditure incurred in respect of additional costs/delays are accounted in the year in which they are incurred. Claims made in respect thereof are accounted as income in the year of receipt of arbitration award or acceptance by client.

, the services rendered to the Joint Ventures are accounted as income on accrual basis. The profit / loss is accounted for, as and when it is determined by the Joint Venture and the net investment in the Joint Venture is reflected as investments, loans & advances or current liabilities. In respect of contracts executed in Integrated Joint Ventures under profit sharing arrangement (assessed as AOP under Income tax laws), the services rendered to the Joint Ventures are accounted as income on accrual basis. The profit / loss is accounted for, as and when it is determined by the Joint Venture and the net investment in the Joint Venture is reflected as investments, loans & advances or current liabilities. Expenditure incurred in respect of additional costs/delays are accounted in the year in which they are incurred. Claims made in respect thereof are accounted as income in the year of receipt of arbitration award or acceptance by client. Expenditure incurred in respect of additional costs/delays are accounted in the year in which they are incurred. Claims made in respect thereof are accounted as income in the year of receipt of arbitration award or acceptance by client..")

59

Profit booking Threshold Limit Company Threshold limit for profit booking HCC10% NagarjunaProportionate MadhuconProportionate L&T50% Gammon 15% ( 2.5 Bn) IVRCLProportionate JP associates Proportionate Source: Companies, SSKI Report

IVRCLProportionate JP associates Proportionate Source: Companies, SSKI Report")

60

Accounting for Foreign Exchange Transaction Current assets and current liabilities are translated at the exchange rate prevailing on the last day of the year. Current assets and current liabilities are translated at the exchange rate prevailing on the last day of the year. Gains or losses arising out of remittance / translations at the year-end are credited/debited to the profit and loss account for the year. Gains or losses arising out of remittance / translations at the year-end are credited/debited to the profit and loss account for the year. Foreign exchange transactions are converted into Indian rupees at the prevailing rate on the date of the transaction. Foreign exchange transactions are converted into Indian rupees at the prevailing rate on the date of the transaction. Gains & losses in respect of foreign exchange contracts are recognized as income or expenses over the life of the contract, except in respect of fixed assets where such gains or losses are adjusted in the carrying amount of the fixed assets. Gains & losses in respect of foreign exchange contracts are recognized as income or expenses over the life of the contract, except in respect of fixed assets where such gains or losses are adjusted in the carrying amount of the fixed assets.

61

Other Accounting Policies Taxation Taxation Tax expense comprises of current tax and deferred tax charged /credited to the P/L Tax expense comprises of current tax and deferred tax charged /credited to the P/L In case of unabsorbed depreciation or carry forward losses, deferred tax asset is recognized only if there is a virtual certainty of realization of such asset In case of unabsorbed depreciation or carry forward losses, deferred tax asset is recognized only if there is a virtual certainty of realization of such asset At each balance sheet date recognized and unrecognized deferred tax are reviewed At each balance sheet date recognized and unrecognized deferred tax are reviewed Depreciation Policy Depreciation Policy The depreciation on assets used for construction has been treated as period cost The depreciation on assets used for construction has been treated as period cost In respect of buildings and sheds, furniture and office equipment on the written down value method at rates prescribed in the Companies Act, 1956. In respect of buildings and sheds, furniture and office equipment on the written down value method at rates prescribed in the Companies Act, 1956. In respect of plant & machinery, heavy vehicles, on the straight line method at rates prescribed in Companies Act, 1956 on a pro-rata basis In respect of plant & machinery, heavy vehicles, on the straight line method at rates prescribed in Companies Act, 1956 on a pro-rata basis

62

Other Accounting Policies Inventories Inventories The stock of stores, spares and embedded goods and fuel is valued at cost (weighted average basis) or net realizable value whichever is lower The stock of stores, spares and embedded goods and fuel is valued at cost (weighted average basis) or net realizable value whichever is lower Work-in-progress is valued at the contract rates and site mobilization expenditure of incomplete contracts is stated at cost. Work-in-progress is valued at the contract rates and site mobilization expenditure of incomplete contracts is stated at cost. Certain loose plant, tools & service equipments costing below Rs. 5 lacs are valued at proportionate written down value 3% p.m. over a period of 32 months. Certain loose plant, tools & service equipments costing below Rs. 5 lacs are valued at proportionate written down value 3% p.m. over a period of 32 months. Investments Investments Investments are classified as long-term and current investments. Investments are classified as long-term and current investments. Long-term investments are shown at cost or written down value (in case of other than temporary diminution) and current Investments are shown at cost or market value whichever is lower Long-term investments are shown at cost or written down value (in case of other than temporary diminution) and current Investments are shown at cost or market value whichever is lower

and current Investments are shown at cost or market value whichever is lower Long-term investments are shown at cost or written down value (in case of other than temporary diminution) and current Investments are shown at cost or market value whichever is lower.")

63

Part 2: Valuation of HCC

64

Valuation Methods Used Comparables Comparables DCF Valuation DCF Valuation

65

Valuation using Comparables Companies taken as comparables: Companies taken as comparables: -Gammon India Ltd -Gammon India Ltd -IVRCL -IVRCL -Nagarjuna Constructions -Nagarjuna Constructions -Jai Prakash Industries Ltd -Jai Prakash Industries Ltd Divided the business into BOT and Contracting business Divided the business into BOT and Contracting business Calculated the average multiples for these four companies Calculated the average multiples for these four companies Used the expected earnings of 07’ and 08’ Used the expected earnings of 07’ and 08’ Used the following multiples: Used the following multiples: - P/E multiple of HCC - P/E multiple of HCC - Average P/E multiple of the four companies - Average P/E multiple of the four companies - Highest P/E multiple amongst the four companies - Highest P/E multiple amongst the four companies

66

Trading Comparables Comparables

67

Valuation Chart Comparables

68

WACC Cost of Equity = 14.79% Cost of Equity = 14.79% Cost of Debt (Post Tax) = 4.73% Cost of Debt (Post Tax) = 4.73% Cost of Capital = 12.49% Cost of Capital = 12.49% Assumptions Used: Tax Rate = 33.66% Risk Premium = 7% Target Debt/Equity = 0.2967 WACC Calculations

= 4.73% Cost of Debt (Post Tax) = 4.73% Cost of Capital = 12.49% Cost of Capital = 12.49% Assumptions Used: Tax Rate = 33.66% Risk Premium = 7% Target Debt/Equity = WACC Calculations")

69

DCF Perpetual Growth Rate = 6% Perpetual Growth Rate = 6% Terminal Value (discounted) = Rs.3137.99 Cr. Terminal Value (discounted) = Rs.3137.99 Cr. FCF (discounted) = Rs.2418.62 Cr. FCF (discounted) = Rs.2418.62 Cr. Total DCF = Rs.5556.61 Cr. Total DCF = Rs.5556.61 Cr. Total Value of Other Projects = Rs.935 Cr. Total Value of Other Projects = Rs.935 Cr. Total Debt = Rs.1316 Cr. Total Debt = Rs.1316 Cr. Total Value to Equity = Rs.5175.23 Cr. Total Value to Equity = Rs.5175.23 Cr. Shares Outstanding = 25.62 Cr. Shares Outstanding = 25.62 Cr. Value per Share = Rs.201.97 Value per Share = Rs.201.97 DCF Valuation Calculations

= Rs Cr. FCF (discounted) = Rs Cr. FCF (discounted) = Rs Cr. Total DCF = Rs Cr. Total DCF = Rs Cr. Total Value of Other Projects = Rs.935 Cr. Total Value of Other Projects = Rs.935 Cr. Total Debt = Rs.1316 Cr. Total Debt = Rs.1316 Cr. Total Value to Equity = Rs Cr. Total Value to Equity = Rs Cr. Shares Outstanding = Cr. Shares Outstanding = Cr. Value per Share = Rs Value per Share = Rs DCF Valuation Calculations.")

70

Other Projects Other Projects: Lavasa Project = 635 Cr. Hincon Realty = 300 Cr. Total = 935 Cr.

71

Sensitivity Analysis Sensitivity WACC 11.00%11.50%12.00%12.50%13.00%13.50%14.00% Perpetual Growth Rate 5.00%247.07222.64201.93184.17168.80155.39143.61 5.25%254.33228.46206.65188.04172.00158.07145.86 5.50%262.25234.76211.73192.18175.42160.91148.24 5.75%270.93241.61217.22196.64179.07163.93150.76 6.00%280.47249.09223.16201.43182.99167.16153.45 6.25%291.02257.27229.63206.61187.19170.61156.31 6.50%302.74266.27236.68212.22191.72174.30159.35 6.75%315.84276.22244.40218.32196.61178.27162.61 7.00%330.58287.28252.89224.98201.91182.55166.10

72

Volatility of RM Prices Price escalation Price escalation Available for road, water and power projects Available for road, water and power projects Not available for EPC or BOT projects Not available for EPC or BOT projects Cost escalation Cost escalation Based on detailed formula Based on detailed formula Encompassing the labour and fuel component besides the direct raw materials Encompassing the labour and fuel component besides the direct raw materials Inc in RM prices like steel and cement escalated based on WPI formula (under cover possible) Inc in RM prices like steel and cement escalated based on WPI formula (under cover possible) In NHAI, Irrigation and Power projects majority of the cost increases are passed on to the client. In NHAI, Irrigation and Power projects majority of the cost increases are passed on to the client. Source: Company

73

Bandra Worli Sea Link Project Scenario analysis of BW sea link (Rs in Crores) FY07 E FY08 E Scenario 1 Scenario 2 Scenario 1 Scenario 2 Net Sales 2504.82544.83265.33305.2 EBITDA232.6272.6321.1361.1 EBITDA Margin 9.30%10.70%9.80%10.90% PAT115.4166.8176.02274 Net Margin 4.60%6.60%5.40%6.90% No of shares* 256256256256 EPS4.56.56.98.9 % YoY 45%110%53%36% Source: J P Morgan estimates, Company Note: Scenario 1: Worst case - Assuming Bandra Worli sea link losses continue for FY07 and FY08E Scenario 2: Company does not make any losses in FY07 and FY08, losses booked in iH FY07 are reversed, no one time grant for part losses

FY07 E FY08 E Scenario 1 Scenario 2 Scenario 1 Scenario 2 Net Sales EBITDA EBITDA Margin 9.30%10.70%9.80%10.90% PAT Net Margin 4.60%6.60%5.40%6.90% No of shares* EPS % YoY 45%110%53%36% Source: J P Morgan estimates, Company Note: Scenario 1: Worst case - Assuming Bandra Worli sea link losses continue for FY07 and FY08E Scenario 2: Company does not make any losses in FY07 and FY08, losses booked in iH FY07 are reversed, no one time grant for part losses")

74

Overview of Gammon India

75

Gammon India Overview Overview Established: 1919 Established: 1919 Private Limited Company: 1922 and Went Public: 1962 Private Limited Company: 1922 and Went Public: 1962 Registered HQ: Prabhadevi, Mumbai, Maharashtra Registered HQ: Prabhadevi, Mumbai, Maharashtra 1600 in the Management & Staff Category 1600 in the Management & Staff Category 6500 Skilled Personnel engaged at various sites 6500 Skilled Personnel engaged at various sites Pioneer of pre-stressed concrete in India Pioneer of pre-stressed concrete in India Builder of the largest number of bridges and flyovers in India Builder of the largest number of bridges and flyovers in India Pioneered cantilever construction and pre-cast segmental bridge construction Pioneered cantilever construction and pre-cast segmental bridge construction ISO 9001:1994 certification ISO 9001:1994 certification Subsidiary Companies Subsidiary Companies Andhra Express Andhra Express Gammon & Billimori Gammon & Billimori Gammon Infrastructure Gammon Infrastructure Gammon Power Gammon Power Rajamundry Exprs Rajamundry Exprs Source: Gammon India Website – http://www.gammonindia.com/

76

Shareholding Pattern Source: Batlivala & Karani Sucurities Research Report (June, 2006)

")

77

Order Book FY’06 Source: SSKI India Research (31 st Oct, 2006)

")

78

Gammon - Ongoing Projects Transportation projects Transportation projects Transportation projects Transportation projects Hydro-electric & nuclear power projects Hydro-electric & nuclear power projects Hydro-electric & nuclear power projects Hydro-electric & nuclear power projects Chimney & cooling towers Chimney & cooling towers Chimney & cooling towers Chimney & cooling towers Irrigation and tunnel engineering projects Irrigation and tunnel engineering projects Irrigation and tunnel engineering projects Irrigation and tunnel engineering projects Multi storey building projects Multi storey building projects Multi storey building projects Multi storey building projects Pipeline projects Pipeline projects Pipeline projects Pipeline projects Current Order Backlog of Rs.78bn (as on 30 th September, 2006) Current Order Backlog of Rs.78bn (as on 30 th September, 2006) Growth of 66% yoy Growth of 66% yoy Order Book expected to grow rapidly over the next 12 months on the back of strong pipeline of projects such as roads, hydel power, etc. Order Book expected to grow rapidly over the next 12 months on the back of strong pipeline of projects such as roads, hydel power, etc. Source: SSKI India Research (31st Oct, 2006)

.")

79

Past Financials - Gammon

80

YOY Change in Net Profit Source: Capitaline

81

YOY Change in Operating Margin Source: Capitaline

82

Summary P&L Particulars Mar ‘04 Dec ‘04 Mar ’06 Net Sales 1119.72866.681467.93 Other Income 9.9610.5533.20 Expenditure1096.02857.561407.45 PBDIT118.44105.34215.53 Depreciation19.9416.4537.10 Interest44.0437.3067.26 PBT54.4651.59111.17 PAT34.0942.90102.84 Source: Capitaline. In Rs.Cr.

83

Summary Balance Sheet Particulars Mar ‘04 Dec ‘04 Mar ’06 Share Capital 12.8415.5817.69 Reserves & Surplus 209.47378.75908.14 Loans218.18303.09170.59 Net Fixed Assets 290.50309.66369.74 Investments80.4989.62116.18 Net Current Assets 96.67321.92637.68 Source: Capitaline. In Rs.Cr.

84

Key Ratios Particulars Mar ‘04 Dec ‘04 Mar ’06 Current Ratio 0.860.991.52 Debt/Equity1.461.090.40 RONW (%) 24.4823.9713.90 ROCE (%) 28.7623.7417.23 BVPS118.45208.7397.06 EPS26.2336.259.24 Dividend (%) 2533.3324 EV/EBITDA6.3613.5222.14 Source: Capitaline In Rs.Cr.

ROCE (%) BVPS EPS Dividend (%) EV/EBITDA Source: Capitaline In Rs.Cr.")

85

Part 4: Investment Perspective for M&A

86

Concerns About Construction Sector Higher raw material prices impact margin Higher raw material prices impact margin Star contracts Star contracts Cost escalation-based contracts, wherein the raw material cost increases are reimbursed based on an index or the actual purchase price Cost escalation-based contracts, wherein the raw material cost increases are reimbursed based on an index or the actual purchase price Fixed price contracts – the increase in raw material costs has to be borne by contractors Fixed price contracts – the increase in raw material costs has to be borne by contractors Fixed price contracts from BOT SPVs Fixed price contracts from BOT SPVs Construction contracts given to parent on fixed price basis Construction contracts given to parent on fixed price basis Parent construction companies factor in high raw material costs Parent construction companies factor in high raw material costs

87

Concerns About Construction Sector Business is highly capital intensive Business is highly capital intensive Accounting of mobilization advance impacts reported WC Accounting of mobilization advance impacts reported WC Retention money released through bank guarantees Retention money released through bank guarantees Cash reserves result in lower advances and higher cash discounts translating into higher working capital Cash reserves result in lower advances and higher cash discounts translating into higher working capital BOT Value impacted due to higher interest rates BOT Value impacted due to higher interest rates Higher interest expenses factored in while bidding for the project Higher interest expenses factored in while bidding for the project Projects are naturally hedged against rising interest rates Projects are naturally hedged against rising interest rates Fixed revenue projects likely to be impacted marginally Fixed revenue projects likely to be impacted marginally BOT projects – limited impact of higher construction cost BOT projects – limited impact of higher construction cost

88

Primary Risks of Proposed M&A Past reputation of HCC & ongoing projects Past reputation of HCC & ongoing projects Bonding of ongoing and future projects and bonding capacity Bonding of ongoing and future projects and bonding capacity Different revenue recognition policy from Gammon Different revenue recognition policy from Gammon Nature and extent of insurance coverage Nature and extent of insurance coverage Licensing Licensing Is the Valuation of existing contracts reasonable? Is the Valuation of existing contracts reasonable? Terms and conditions of construction contracts including assignability Terms and conditions of construction contracts including assignability Aggressive bids (in low technical expertise sectors such as roads) ignoring the business and regulatory risk leading to margin erosion Legal Risk with specific executory contract Legal Risk with specific executory contract

ignoring the business and regulatory risk leading to margin erosion Legal Risk with specific executory contract Legal Risk with specific executory contract.")

89

Primary Risks of Proposed M&A Land title clearance: HCC does not possess valid title to all land related to its Lavasa venture Land title clearance: HCC does not possess valid title to all land related to its Lavasa venture Risk of Marketing failure: Lavasa is the first real estate venture by the company. Though it has extensive construction experience; its experience in sales & marketing is limited Risk of Marketing failure: Lavasa is the first real estate venture by the company. Though it has extensive construction experience; its experience in sales & marketing is limited Pension and benefit plan liabilities Pension and benefit plan liabilities Employee stock ownership and other profit sharing agreements Employee stock ownership and other profit sharing agreements Union contracts and Employment contracts Union contracts and Employment contracts Environmental issues (e.g.asbestos and mold) Environmental issues (e.g.asbestos and mold)

Environmental issues (e.g.asbestos and mold).")

90

Synergy Benefits for Gammon from M&A

91

M&A Rationale Cost Synergies Cost Synergies Economies of Scale Economies of Scale Efficiencies Efficiencies Revenue Synergies Revenue Synergies More market power More market power Cross selling Cross selling Tax Considerations Tax Considerations Other reasons Other reasons Diversification Diversification Size Size Management Control Management Control Management Incentive Management Incentive

92

Value Drivers of Merger Top line growth opportunity Top line growth opportunity Order book size Order book size Handle large size orders (BS strength) Handle large size orders (BS strength) Ability to handle higher technical precision projects Ability to handle higher technical precision projects Diversification of business Diversification of business Real Estate (Lavasa Project) Real Estate (Lavasa Project) Greater focus on higher value addition segments Greater focus on higher value addition segments Power projects (Hydro/ Nuclear) Power projects (Hydro/ Nuclear) Bridges & Roads Bridges & Roads Greater pricing power vis-à-vis a consolidating cement industry Greater pricing power vis-à-vis a consolidating cement industry Improving existing relations with State Governments Improving existing relations with State Governments Work permits / contracts Work permits / contracts Geographical expansion Geographical expansion Presence in more states in India Presence in more states in India International Presence International Presence

Handle large size orders (BS strength) Ability to handle higher technical precision projects Ability to handle higher technical precision projects Diversification of business Diversification of business Real Estate (Lavasa Project) Real Estate (Lavasa Project) Greater focus on higher value addition segments Greater focus on higher value addition segments Power projects (Hydro/ Nuclear) Power projects (Hydro/ Nuclear) Bridges & Roads Bridges & Roads Greater pricing power vis-à-vis a consolidating cement industry Greater pricing power vis-à-vis a consolidating cement industry Improving existing relations with State Governments Improving existing relations with State Governments Work permits / contracts Work permits / contracts Geographical expansion Geographical expansion Presence in more states in India Presence in more states in India International Presence International Presence")

93

Ranking of Major Indian Players by Sales (Post Acquisition) (Rs Crore) Source: Company financial statements CompanyRank Order Backlog FY06 Order Booking FY06Sales FY 06 OrderBooking (Q1) FY07 L&T12466422318147636326 Jai Prakash 23651 Gammon31617278003473.11564 Nagarjuna45428367618401101 IVRCL5625053001495877

(Rs Crore) Source: Company financial statements CompanyRank Order Backlog FY06 Order Booking FY06Sales FY 06 OrderBooking (Q1) FY07 L&T Jai Prakash Gammon Nagarjuna IVRCL")

94

Value Drivers of Merger Increased debt capacity Increased debt capacity Increase return on equity Increase return on equity Higher combined market share Higher combined market share Complimentary strength in execution of infrastructure projects Complimentary strength in execution of infrastructure projects Pre-mergerHCCPre-mergerGammon Leverage (BV) D/E 1.56.805 EV/ EBITDA 1110.7 ROCE10%18% ROE14%17%

D/E EV/ EBITDA ROCE10%18% ROE14%17%")

95

Sources of Tax Benefits MV of depreciable assets in excess of BV MV of depreciable assets in excess of BV Revaluation by sale provides greater depreciation & hence tax shelter Revaluation by sale provides greater depreciation & hence tax shelter Substitution of capital gains for ordinary income Substitution of capital gains for ordinary income Unused and/or unusable tax credit carry-overs Unused and/or unusable tax credit carry-overs Gammon &HCC may have investment tax credits or foreign tax credits they cannot use completely Gammon &HCC may have investment tax credits or foreign tax credits they cannot use completely Equity Dividend (%) ‘06‘05‘04‘03‘02 Gammon Gammon3025252510 HCC7060504030

‘06‘05‘04‘03‘02 Gammon Gammon HCC")

96

Key Arguments in Favour of Investment in HCC

97

Key Investment Arguments for HCC Proven execution capability Proven execution capability Possesses pre-qualifications & execution capability across sectors Possesses pre-qualifications & execution capability across sectors Has the youngest fleet of specialized equipments, skilled manpower, in- house fabrication facility Has the youngest fleet of specialized equipments, skilled manpower, in- house fabrication facility Will benefit from large ticket sized orders in hydro and nuclear sectors Will benefit from large ticket sized orders in hydro and nuclear sectors Considerable Progress in Real Estate Considerable Progress in Real Estate Lavasa project could be value accretive, and 10% increase in FSI can enhance shareholder returns by 100% Lavasa project could be value accretive, and 10% increase in FSI can enhance shareholder returns by 100% Tied up another 2,500 acres at Lavasa, (total 12,500 acres now) Tied up another 2,500 acres at Lavasa, (total 12,500 acres now) Contracted 450 acres (on the outskirts of Mumbai and Navi Mumbai) for township development and targeted total acreage of 1,000 acres by June 2007 Contracted 450 acres (on the outskirts of Mumbai and Navi Mumbai) for township development and targeted total acreage of 1,000 acres by June 2007 To commence construction of IT park (2m sq.ft.) at Vikhroli Mumbai To commence construction of IT park (2m sq.ft.) at Vikhroli Mumbai Undertaking slum rehabilitation for 25 acres (2m sq.ft) Undertaking slum rehabilitation for 25 acres (2m sq.ft) Other land banks Other land banks

Tied up another 2,500 acres at Lavasa, (total 12,500 acres now) Contracted 450 acres (on the outskirts of Mumbai and Navi Mumbai) for township development and targeted total acreage of 1,000 acres by June 2007 Contracted 450 acres (on the outskirts of Mumbai and Navi Mumbai) for township development and targeted total acreage of 1,000 acres by June 2007 To commence construction of IT park (2m sq.ft.) at Vikhroli Mumbai To commence construction of IT park (2m sq.ft.) at Vikhroli Mumbai Undertaking slum rehabilitation for 25 acres (2m sq.ft) Undertaking slum rehabilitation for 25 acres (2m sq.ft) Other land banks Other land banks")

98

Key Investment Arguments for HCC Strength in BOT Projects Strength in BOT Projects HCC has emerged as L1 in the annuity road project for the stretch of 30km, costing Rs2.7b, in Andhra Pradesh HCC has emerged as L1 in the annuity road project for the stretch of 30km, costing Rs2.7b, in Andhra Pradesh The concession period is 20 years The concession period is 20 years The semi-annual annuity receipt is Rs238.5m and expected ROE is 15% The semi-annual annuity receipt is Rs238.5m and expected ROE is 15% HCC has submitted bids for two more road projects on BOT basis HCC has submitted bids for two more road projects on BOT basis Also bidding for BOT projects in power, and has targeted US$50m as investments in this sector Also bidding for BOT projects in power, and has targeted US$50m as investments in this sector HCC is one of the three companies that pre-qualifies for nuclear ordering and expects an increase in nuclear order flow HCC is one of the three companies that pre-qualifies for nuclear ordering and expects an increase in nuclear order flow HCC is already looking at hydropower projects in Uttar Pradesh & Uttaranchal HCC is already looking at hydropower projects in Uttar Pradesh & Uttaranchal

99

Bandra-Worli Sealink project: Drag on Margins Bandra Worli Sea link: Revised Cost Rs.Crores Original Project cost 430 Escalations, based on Index 100 Variations to original work scope 90 Revised project cost 630 Source: Company, Motilal Oswal Securities

100

Part 5 : Deal Structure & Transaction Details

101

Rationale for Stock Offer Method of Payment Cash deals are higher in value due to Cash deals are higher in value due to Tax advantage Tax advantage Target shareholders’ taxable gains in stock-for-stock exchange may be deferred indefinitely Target shareholders’ taxable gains in stock-for-stock exchange may be deferred indefinitely The taxes on gains in cash transactions are payable immediately The taxes on gains in cash transactions are payable immediately Information effect of stock versus cash Information effect of stock versus cash Using cash signals that future cash flows will be large enough to exploit investment opportunities the merger will generate Using cash signals that future cash flows will be large enough to exploit investment opportunities the merger will generate Using stock suggests that bidder may not have sufficient internal financing Using stock suggests that bidder may not have sufficient internal financing

102

Structure of the Deal HCC Book Debt = 1316.28 Cr. Book Equity = 842.18 Cr. Market Equity = 3766.14 Cr. No. of Shares = 25.62 Cr. Share Price = Rs.147/share Shareholding Pattern: Promoters = 47% FIIs = 24% Institutional Investors = 10% Indian Public = 11% Others = 8% Gammon Book Debt = 812.84 Cr. Book Equity = 1058.85 Cr. Market Equity = 3668.53 Cr. No. of Shares = 8.745 Cr. Share Price = Rs.419.5/share Shareholding Pattern: Promoters = 32% FIIs = 18% Mutual Funds = 7% ADRs/GDRs/Other Foreign = 19% Institution = 4% Public and Others = 20% Current Status

103

Part Debt…Part Equity 51% of HCC to be acquired by Gammon 51% of HCC to be acquired by Gammon Acquisition price (Bidding Price) = Rs.170 per share for a total consideration of Rs.2221.254 Cr. Acquisition price (Bidding Price) = Rs.170 per share for a total consideration of Rs.2221.254 Cr. 27% Debt for a total of Rs.600 Cr. 27% Debt for a total of Rs.600 Cr. 73% Equity for a total of Rs.1621.254 Cr. 73% Equity for a total of Rs.1621.254 Cr. 3.38 shares of HCC to be traded for 1 share of Gammon 3.38 shares of HCC to be traded for 1 share of Gammon Debt could be raised via Inflation-Linked Bonds or Mezzanine Financing Debt could be raised via Inflation-Linked Bonds or Mezzanine Financing Deal Structuring Fianncials

= Rs.170 per share for a total consideration of Rs Cr. 27% Debt for a total of Rs.600 Cr. 27% Debt for a total of Rs.600 Cr. 73% Equity for a total of Rs Cr. 73% Equity for a total of Rs Cr shares of HCC to be traded for 1 share of Gammon 3.38 shares of HCC to be traded for 1 share of Gammon Debt could be raised via Inflation-Linked Bonds or Mezzanine Financing Debt could be raised via Inflation-Linked Bonds or Mezzanine Financing Deal Structuring Fianncials.")

104

Post Structuring Scenario Current Debt/Equity = 0.7677 Post Debt/Equity = 1.3343 Current Debt/Equity = 0.7677 Post Debt/Equity = 1.3343 New Shareholding Pattern: New Shareholding Pattern: Promoters22.19% FIIs12.48% Mutual Funds 4.85% ADRs/GDRs13.18% Institution2.77% Public & Oth 13.97% Total69.35% HCC Stake holders hold 30.35% of the post merged company RESTRICTION TO BE TAKEN CARE OF: Promoters of HCC cannot offload more than 36.93% of their 47% stake in HCC in this deal. They will have to sell it to the public or other players post deal.

105

Appendix

106

Breakup of Promoter Holding Name Percentage of shares Hincon Holdings Ltd 39.07% Hindustan Finvest Ltd 7.39% 7.39% Ajit Gulabchand 0.39% 0.39% Shalakha Investment Pvt Ltd 0.10% 0.10% Promoters Back

107

Break up of Non – Promoter Holding Name Percentage of shares Ritu Estate Developers Pvt Ltd 3.48% Goldman Sachs Investments India Ltd 2.91% Morgan Stanley Investment Management Inc 2.49% Morgan Stanley Mutual Fund A/C 2.18% Fid Funds Mauritius Ltd 2.02% Non Promoters Back

108

HCC - Contingent Liabilities Particulars`05`06 Counter Indemnities given to banks 875.181033.77 Counter Indemnities given to custom Auth. 1.921.92 Claims not acknowledged as debts by the company 1.180.57 Sales Tax Liability/Work Contract Tax Liability 01.8 Corporate Guarantees 38.1890.26 In Crores Back

109

Ongoing Transportation Projects ProjectValue Construction of Bridge over River Ganga at Kanpur for the DMRC Rs.159 Cr. Novel Extradosed Bridge in the contract with DMRC Kosi Bridge Rs.347 Cr. Cable Stayed Bridge with overseas JV partner at Kota, Rajasthan Rs.210 Cr. Elevated Road Project at Amritsar, Punjab Rs.173 Cr. Two Major Cont. for the elevated viaduct for DMRC (Phase – II) Rs.195.5 Cr River Bridge over Brahmaputra River in Guwahati Rs.238 Cr. Total Contract Value for Bridges and Flyovers Rs.1500 Cr. Road Project AS-24 in Assam Rs.172 Cr. Road Project AS-26 in Assam Rs.179 Cr. East-West Corridor in Bihar Rs.357 Cr. Nashik Project on BOT basis Rs.650 Cr. Source: Capitaline (Director’s Report) Back

Rs Cr River Bridge over Brahmaputra River in Guwahati Rs.238 Cr. Total Contract Value for Bridges and Flyovers Rs.1500 Cr. Road Project AS-24 in Assam Rs.172 Cr. Road Project AS-26 in Assam Rs.179 Cr. East-West Corridor in Bihar Rs.357 Cr. Nashik Project on BOT basis Rs.650 Cr. Source: Capitaline (Director’s Report) Back.")

110

Ongoing Hydro Electric Projects ProjectValue Parbati H.E. Project Stage III Rs.325 Cr. 85 MW Hydro Power Project in Sikkim on BOT basis Nuclear Power Plants Projects in Kaiga and Kalapakkam progressing well With India-US Nuclear Deal getting through, India is poised to emerge a strong player in Nuclear Engineering Field Proposals of starting 8 Nuclear Reactors in the near future (Opportunity for Gammon) Source: Capitaline (Director’s Report) Back

Source: Capitaline (Director’s Report) Back.")

111

Ongoing Chimney and Cooling Towers Projects ProjectValue Chimneys for Jindal Group Rs.47.35 Cr. Cooling Tower in Cooling Tower in Chandrapura Rs.24 Cr. Sugen Cooling Tower for Siemens Rs.47.98 Cr. Nevyeli Lignite Corporation Cooling Tower & Chimneys Rs.55.29 Cr. Paras Cooling Tower Rs.10 Cr. Source: Capitaline (Director’s Report) Back

Back.")

112

Irrigation Projects: Ongoing ProjectValue Modikunta Vagu Reservoir Project Rs.118.95 Cr. Kalwakurthy Lift Irrigation System Rs.632 Cr. Tunnel Engineering Teesta Hydroelectric Project – Tunnel under advance stage of completion Parbati (World Record) – Boring the 1 st inclined pressure shaft of length 1542m @ 30 degrees to the horizontal by TBM (Tunnel Boring Machine) Sewa Project – 11,800m of tunnel (60% complete) Source: Capitaline (Director’s Report) Back

– Boring the 1 st inclined pressure shaft of length 30 degrees to the horizontal by TBM (Tunnel Boring Machine) Sewa Project – 11,800m of tunnel (60% complete) Source: Capitaline (Director’s Report) Back.")

113

Multistorey Building Projects: Ongoing ProjectValue Contracts with Godrej Properties Ltd for construction of 7 towers of 14 storey with basement car parking at Bangalore Rs.60.53 Cr. Contracts with Neelkanth Reality for construction of 7 towers of 14 storey with basement car parking at Mumbai Rs.88.75 Cr. Source: Capitaline (Director’s Report) Back

Back.")

114

Pipeline Projects : Ongoing ProjectValue Completed Laying off 1875mm X 94Km X 1500mm X 20Km pipeline project of Chennai Metropolitan Water Supply & Sewage Board Rs.335.69 Cr. Almost completed the 170Kms X 30 feet pipeline work of IOCL for Paradip – Haldia Project Rs.33.89 Cr. Project of Water Transmission System at SOHAR by Ministry of Housing, Electricity & Water, Sultanate of Oman to be completed during 2006-07 Rs.642.5 Cr. Numaligarh Siliguri Pipeline Expansion Project of 6 feet X 206.3 Kms awarded by OIL (Duration = 12 months) Rs.47.98 Cr. IOCL project of laying cross country pipeline and associated facilities for Koyali-Ratlam Pipeline Project of 16 feet OD X 261 Km Rs.42.40 Cr. Successfully completed the tendering process for renowned Petroleum Companies like IOCL, GAIL, Reliance Industries and is likely to bag more Pipeline Projects in the next financial year Source: Capitaline (Director’s Report) Back

Rs Cr. IOCL project of laying cross country pipeline and associated facilities for Koyali-Ratlam Pipeline Project of 16 feet OD X 261 Km Rs Cr. Successfully completed the tendering process for renowned Petroleum Companies like IOCL, GAIL, Reliance Industries and is likely to bag more Pipeline Projects in the next financial year Source: Capitaline (Director’s Report) Back.")

115

Thank You

Similar presentations

LIMITED ANALYSTS MEET MAY 15, 2009.>")

and what a firm owes (liabilities) Asset = Liability.>")