Download presentation

Presentation is loading. Please wait.

1

Effectiveness of monetary policy communication in Indonesia and Thailand S. Sahminan (Bank of Indonesia) Discussion – P. Reding (University of Namur)

Discussion – P. Reding (University of Namur).")

2

Interest of Paper Additional light on question “Does transparency matter for MP ?” Special focus on two EM which are also Inflation targeters : Indonesia (since July 2005) & Thailand (since 2000); During tranquil (non crisis) period : 2004-2007 Empirical study allowing comparison with results for industrial countries (Ehrmann- Fratzscher 2007)

& Thailand (since 2000); During tranquil (non crisis) period : Empirical study allowing comparison with results for industrial countries (Ehrmann- Fratzscher 2007)")

3

Question addressed = effectiveness of MP communciation Focus on MP communication, measured as : Official statements after meetings Inter-meeting statements by members of the Board Coded as ‘tight’ – ‘neutral’ – ‘loose’ Effectiveness of MP communication : 3 relevant perspectives : Is MP communication informative ? Does the CB do as it had said it would do ? Is MP communication effective as a transmission channel of MP ? Is there « internal consistency » in MP communication?

4

Effectiveness as transmission channel (1) Only effect on market interest rates (yield curve) Conditional mean Conditional volatility Why not also on exchange rates? At least as important, especially in open EM with still not fully developped financial markets ? Direct effect on inflation expectations ?

5

Effectiveness as transmission channel (2) Econometric spécification (E-Garch) r t = daily changes in interbank rates & implied forward rates M +, M 0, M - and I +, I 0, I - the MP communication variables

Econometric spécification (E-Garch) r t = daily changes in interbank rates & implied forward rates M +, M 0, M - and I +, I 0, I - the MP communication variables")

6

Effectiveness as transmission channel (3) : Results MP announcements do move interest rates in the right direction in Indonesia and Thailand Effects on r t ( μ i ; θ i ) are larger than for Fed, Be and ECB (5 to 10 Bp vs 1.5 to 2.5 BP) Effects on σ 2 t ( τ i ) : MP announcements increase conditional volatility of r t in Thailand and Indonesia (after July 2005)

: Results MP announcements do move interest rates in the right direction in Indonesia and Thailand Effects on r t ( μ i ; θ i ) are larger than for Fed, Be and ECB (5 to 10 Bp vs 1.5 to 2.5 BP) Effects on σ 2 t ( τ i ) : MP announcements increase conditional volatility of r t in Thailand and Indonesia (after July 2005)")

7

Effectiveness as transmission channel (4) : Questions Control variables Policy rate (p t ) : why ? Should it not be orthogonal to MP announcement variable ? Macro news variables (GDP and inflation) : if purpose in to control for MP annoucement as a reaction to news, why not also a 0, 1, -1 coding (neutral, good, bad news)

: if purpose in to control for MP annoucement as a reaction to news, why not also a 0, 1, -1 coding (neutral, good, bad news).")

8

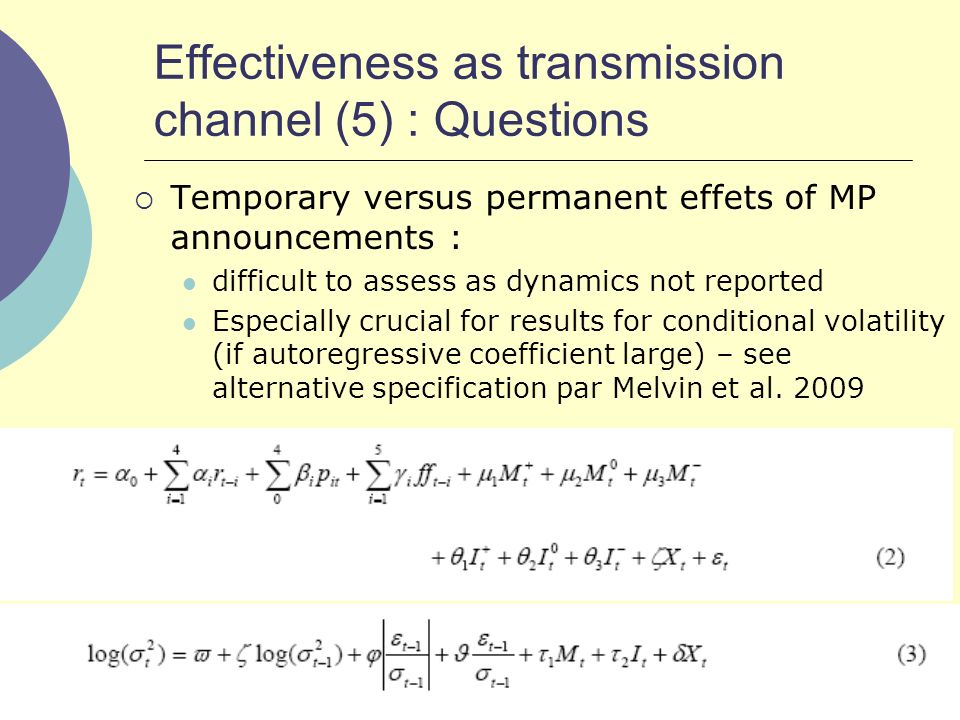

Effectiveness as transmission channel (5) : Questions Temporary versus permanent effets of MP announcements : difficult to assess as dynamics not reported Especially crucial for results for conditional volatility (if autoregressive coefficient large) – see alternative specification par Melvin et al. 2009

9

Effectiveness as transmission channel (6) : Questions Issue of exclusive focus on i-rates as transmission channel : why not joint estimation with exchange rate estimation (Bi- variate Garch) ?

: Questions Issue of exclusive focus on i-rates as transmission channel : why not joint estimation with exchange rate estimation (Bi- variate Garch)")

10

Effectiveness as transmission channel (7) : Questions Evaluating the impact of a shift to IT in Indonesia in July 2005 : Based on re- estimating on a reduced sample period would be worth a more formal testing procedure S: BIS (2008) WP 253

: Questions Evaluating the impact of a shift to IT in Indonesia in July 2005 : Based on re- estimating on a reduced sample period would be worth a more formal testing procedure S: BIS (2008) WP 253")

11

Predictability: Does the CB do as it had said it would do ? - Indonesia

12

Reconcile with econometric results ? – only loose (or neutral) MP announcements matter for markets and have some predictive power

MP announcements matter for markets and have some predictive power.")

Similar presentations

, the central bank sets monetary policy by picking.>")

& Jakob de Haan, Groningen University &>")