Download presentation

Presentation is loading. Please wait.

1

Learning Targets © 2014 Cengage Learning. All Rights Reserved. Lesson 3-1 Recording Transactions and the General Journal What: Journalizing Transactions

2

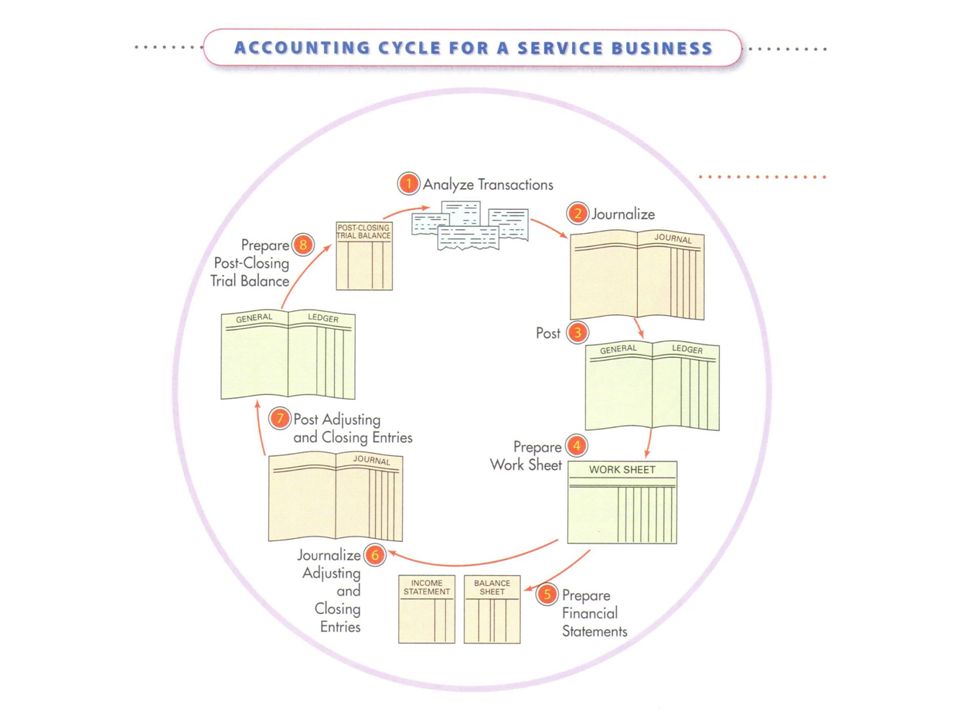

Learning Targets © 2014 Cengage Learning. All Rights Reserved. To understand different types of source documents and the journalizing process. STEP 2 of the Accounting Cycle Why:

3

Learning Targets © 2014 Cengage Learning. All Rights Reserved. How: LT1Define what a journal is and explain why it is used to record transactions. LT2 Compare and contrast different types of source documents. LT3 Identify the four parts of a journal entry. Use your Aplia “Work Together” and “On Your Own” to verify concept accuracy.

5

© 2014 Cengage Learning. All Rights Reserved. Journals and Journalizing ●A form for recording transactions in chronological order is called a journal. ●Recording transactions in a journal is called journalizing. SLIDE 5 Lesson 3-1 LO1

6

© 2014 Cengage Learning. All Rights Reserved. General Journal SLIDE 6 LO1 Lesson 3-1

7

© 2014 Cengage Learning. All Rights Reserved. A General Journal ●Accuracy ●Chronological record ●Double-entry accounting ●Information for each transaction recorded in a journal is called an entry. ●The recording of debit and credit parts of a transaction is called double-entry accounting. SLIDE 7 LO1 Lesson 3-1

8

© 2014 Cengage Learning. All Rights Reserved. Source Documents ●A business paper from which information is obtained for a journal entry is called a source document. SLIDE 8 LO2 Lesson 3-1

9

© 2014 Cengage Learning. All Rights Reserved. Checks ●A business form ordering a bank to pay cash from a bank account is called a check. SLIDE 9 LO2 Lesson 3-1

10

© 2014 Cengage Learning. All Rights Reserved. Invoice ●A form describing the goods or services sold, the quantity, the price, and the terms of sale is called an invoice. SLIDE 10 LO2 Lesson 3-1

11

© 2014 Cengage Learning. All Rights Reserved. Sales Invoice ●An invoice used as a source document for recording a sale on account is called a sales invoice. ● A sales invoice is also referred to as a sales ticket or a sales slip. SLIDE 11 LO2 Lesson 3-1

12

© 2014 Cengage Learning. All Rights Reserved. Receipt ●A business form giving written acknowledgement for cash received is called a receipt. SLIDE 12 LO2 Lesson 3-1

13

© 2014 Cengage Learning. All Rights Reserved. Memorandums ●A form on which a brief message is written to describe a transaction is called a memorandum. SLIDE 13 LO2 Lesson 3-1

14

© 2014 Cengage Learning. All Rights Reserved. Calculator Tapes SLIDE 14 LO2 Lesson 3-1

15

© 2014 Cengage Learning. All Rights Reserved. 2. 2.Write the title of the account debited in the Account Title column. Write the debit amount in the Debit column. Received Cash from Owner as an Investment SLIDE 15 LO3 Lesson 3-1 January 2. Received cash from owner as an investment, $2,000.00. Receipt No. 1. Cash 2,000.00 Michael Delgado, Capital 2,000.00 1. 1.Write the date in the Date column. 3. 3.On the next line, indented about one centimeter, write the title of the account credited in the Account Title column. Write the credit amount in the Credit column. 4. 4.Write the source document number in the Doc. No. column. 1 1 Date 4 4 Source Document Credit 3 3 2 2 Debit

16

© 2014 Cengage Learning. All Rights Reserved. Paid Cash for Supplies SLIDE 16 January 2. Paid cash for supplies, $165.00. Check No. 1. Supplies 165.00 Cash 165.00 Lesson 3-1 LO3 2. 2.Write the title of the account debited in the Account Title column. Write the debit amount in the Debit column. 1. 1.Write the date in the Date column. 3. 3.On the next line, indented about one centimeter, write the title of the account credited in the Account Title column. Write the credit amount in the Credit column. 4. 4.Write the source document number in the Doc. No. column. 1 1 Date 4 4 Source Document 2 2 Debit Credit 3 3

17

© 2014 Cengage Learning. All Rights Reserved. Lesson 3-1 Audit Your Understanding 1.In what order are transactions recorded in a journal? SLIDE 17 ANSWER By date Lesson 3-1

18

© 2014 Cengage Learning. All Rights Reserved. Lesson 3-1 Audit Your Understanding 2.Why are source documents important? SLIDE 18 ANSWER Source documents are one way to verify the accuracy of a specific journal entry. Lesson 3-1

19

© 2014 Cengage Learning. All Rights Reserved. Lesson 3-1 Audit Your Understanding 3.List the four parts of a journal entry. SLIDE 19 ANSWER Date Debit Credit Source document Lesson 3-1

20

© 2014 Cengage Learning. All Rights Reserved. Learning Targets © 2014 Cengage Learning. All Rights Reserved. Lesson 3-2 Transactions Affecting Prepaid Insurance and Supplies What: Journalizing Transactions

21

© 2014 Cengage Learning. All Rights Reserved. Learning Targets © 2014 Cengage Learning. All Rights Reserved. To understand different types of source documents and the journalizing process. STEP 2 of the Accounting Cycle Why:

22

© 2014 Cengage Learning. All Rights Reserved. Learning Targets © 2014 Cengage Learning. All Rights Reserved. How: LT4Analyze and record cash transactions using source documents. LT5 Analyze and record transactions for buying and paying on account. Use your Aplia “Work Together” and “On Your Own” to verify concept accuracy.

24

© 2014 Cengage Learning. All Rights Reserved. Paid Cash for Insurance SLIDE 24 LO4 Lesson 3-2 January 3. Paid cash for insurance, $900.00. Check No. 2. Prepaid Insurance 900.00 Cash 900.00 2. 2.Write the title of the account debited in the Account Title column. Write the debit amount in the Debit column. 1. 1.Write the date in the Date column. 3. 3.On the next line, indented about one centimeter, write the title of the account credited in the Account Title column. Write the credit amount in the Credit column. 4. 4.Write the source document number in the Doc. No. column. 1 1 Date 4 4 Source Document 2 2 Debit Credit 3 3

25

© 2014 Cengage Learning. All Rights Reserved. Bought Supplies on Account SLIDE 25 LO5 Lesson 3-2 January 5. Bought supplies on account from Canyon Office Supplies, $220.00. Memorandum No. 1. Supplies 220.00 Accounts Payable—Canyon Office Supplies 220.00 2. 2.Write the title of the account debited in the Account Title column. Write the debit amount in the Debit column. 1. 1.Write the date in the Date column. 3. 3.On the next line, indented about one centimeter, write the title of the account credited in the Account Title column. Write the credit amount in the Credit column. 4. 4.Write the source document number in the Doc. No. column. 1 1 Date 4 4 Source Document 2 2 Debit Credit 3 3

26

© 2014 Cengage Learning. All Rights Reserved. 2. 2.Write the abbreviated title of the account debited in the Account Title column. Write the debit amount in the Debit column. 1. 1.Write the date in the Date column. 3. 3.On the next line, indented about one centimeter, write the title of the account credited in the Account Title column. Write the credit amount in the Credit column. 4. 4.Write the source document number in the Doc. No. column. 1 1 Date 4 4 Source Document 2 2 Debit Credit 3 3 Paid Cash on Account SLIDE 26 January 9. Paid cash on account to Canyon Office Supplies, $100.00. Check No. 3. 100.00 Accounts Payable—Canyon Office Supplies Cash 100.00 LO5 Lesson 3-2

27

© 2014 Cengage Learning. All Rights Reserved. Lesson 3-2 Audit Your Understanding 1.When cash is paid for insurance, which account is listed on the first line of the entry? SLIDE 27 ANSWER Prepaid Insurance Lesson 3-2

28

© 2014 Cengage Learning. All Rights Reserved. Lesson 3-2 Audit Your Understanding 2.When supplies are bought on account, which account is listed on the first line of the entry? SLIDE 28 ANSWER Supplies Lesson 3-2

29

© 2014 Cengage Learning. All Rights Reserved. Lesson 3-2 Audit Your Understanding 3.When supplies are bought on account, which account is listed on the second line of the entry? SLIDE 29 ANSWER Accounts Payable Lesson 3-2

30

© 2014 Cengage Learning. All Rights Reserved. Lesson 3-2 Audit Your Understanding 4.When cash is paid on account, which account is listed on the second line of the entry? SLIDE 30 ANSWER Cash Lesson 3-2

31

© 2014 Cengage Learning. All Rights Reserved. Learning Targets © 2014 Cengage Learning. All Rights Reserved. Lesson 3-3 Transactions Affecting Owner’s Equity and Asset Accounts What: Journalizing Transactions

32

© 2014 Cengage Learning. All Rights Reserved. Learning Targets © 2014 Cengage Learning. All Rights Reserved. To understand different types of source documents and the journalizing process. STEP 2 of the Accounting Cycle Why:

33

© 2014 Cengage Learning. All Rights Reserved. Learning Targets © 2014 Cengage Learning. All Rights Reserved. How: LT6Analyze and record transactions that affect owner’s equity. LT7 Analyze and record sales and receipt of cash on account. Use your Aplia “Work Together” and “On Your Own” to verify concept accuracy.

35

© 2014 Cengage Learning. All Rights Reserved. Received Cash from Sales SLIDE 35 LO6 Lesson 3-3 January 10. Received cash from sales, $1,100.00. Calculator Tape No. 10. Cash 1,100.00 Sales 1,100.00 2. 2.Write the title of the account debited in the Account Title column. Write the debit amount in the Debit column. 1. 1.Write the date in the Date column. 3. 3.On the next line, indented about one centimeter, write the title of the account credited in the Account Title column. Write the credit amount in the Credit column. 4. 4.Write the source document number in the Doc. No. column. 1 1 Date 4 4 Source Document 2 2 Debit Credit 3 3

36

© 2014 Cengage Learning. All Rights Reserved. Source Document 4 4 Sold Services on Account SLIDE 36 January 12. Sold services on account to Main Street Services, $500.00. Sales Invoice No. 1. 500.00 Accounts Rec.—Main Street Services LO7 Lesson 3-3 2. 2.Write the abbreviated title of the account debited in the Account Title column. Write the debit amount in the Debit column. 1. 1.Write the date in the Date column. 3. 3.On the next line, indented about one centimeter, write the title of the account credited in the Account Title column. Write the credit amount in the Credit column. 4. 4.Write the source document number in the Doc. No. column. 1 1 Date 2 2 Debit Credit 3 3 500.00 Sales

37

© 2014 Cengage Learning. All Rights Reserved. 4 4 Source Document Paid Cash for an Expense SLIDE 37 January 12. Paid cash for communications bill including cell phone and Internet service, $80.00. Check No. 4. 80.00 Communications Expense Cash 80.00 LO7 Lesson 3-3 2. 2.Write the title of the account debited. Write the debit amount. 1. 1.Write the date in the Date column. 3. 3.On the next line, write the title of the account credited. Write the credit amount. 4. 4.Write the source document number in the Doc. No. column. 1 1 Date 2 2 Debit Credit 3 3

38

© 2014 Cengage Learning. All Rights Reserved. Paid Cash for an Expense SLIDE 38 January 15. Paid cash for equipment rental, $400.00. Check No. 5. 400.00 Equipment Rental Expense Cash 400.00 LO7 Lesson 3-3 4 4 Source Document 2. 2.Write the title of the account debited. Write the debit amount. 1. 1.Write the date in the Date column. 3. 3.On the next line, write the title of the account credited. Write the credit amount. 4. 4.Write the source document number in the Doc. No. column. 1 1 Date 2 2 Debit Credit 3 3

39

© 2014 Cengage Learning. All Rights Reserved. January 16. Received cash on account from Main Street Services, $200.00. Receipt No. 2. Received Cash on Account SLIDE 39 Cash 200.00 Accts Rec.—Main Street Services 200.00 LO7 Lesson 3-3 2. 2.Write the title of the account debited. Write the debit amount. 1. 1.Write the date in the Date column. 3. 3.On the next line, indented about one centimeter, write the title of the account credited. Write the credit amount. 4. 4.Write the source document number in the Doc. No. column. 1 1 Date 2 2 Debit Credit 3 3 4 4 Source Document

40

© 2014 Cengage Learning. All Rights Reserved. 4 4 Source Document Paid Cash to Owner as Withdrawal of Equity SLIDE 40 January 16. Paid cash to owner for a withdrawal of equity, $350.00. Check No. 6. 350.00 Michael Delgado, Drawing Cash 350.00 LO7 Lesson 3-3 2. 2.Write the title of the account debited. Write the debit amount. 1. 1.Write the date in the Date column. 3. 3.On the next line, indented about one centimeter, write the title of the account credited. Write the credit amount. 4. 4.Write the source document number in the Doc. No. column. 1 1 Date 2 2 Debit Credit 3 3

41

© 2014 Cengage Learning. All Rights Reserved. Lesson 3-3 Audit Your Understanding 1.When cash is received from sales, which account is listed on the first line of the entry? SLIDE 41 ANSWER Cash Lesson 3-3

42

© 2014 Cengage Learning. All Rights Reserved. Lesson 3-3 Audit Your Understanding 2.When cash is received from sales, which account is listed on the second line of the entry? SLIDE 42 ANSWER Sales Lesson 3-3

43

© 2014 Cengage Learning. All Rights Reserved. Lesson 3-3 Audit Your Understanding 3.When services are sold on account, which account is listed on the second line of the entry? SLIDE 43 ANSWER Sales Lesson 3-3

44

© 2014 Cengage Learning. All Rights Reserved. Lesson 3-3 Audit Your Understanding 4.When cash is paid for any reason, what abbreviation is used for the source document? SLIDE 44 ANSWER C (for check) Lesson 3-3

Lesson 3-3.")

45

© 2014 Cengage Learning. All Rights Reserved. Lesson 3-3 Audit Your Understanding 5.When cash is received on account, what abbreviation is used for the source document? SLIDE 45 ANSWER R (for receipt) Lesson 3-3

Lesson 3-3.")

46

© 2014 Cengage Learning. All Rights Reserved. Learning Targets © 2014 Cengage Learning. All Rights Reserved. Lesson 3-4 Starting a New Journal Page What: Journalizing Transactions

47

© 2014 Cengage Learning. All Rights Reserved. Learning Targets © 2014 Cengage Learning. All Rights Reserved. To understand different types of source documents and the journalizing process. STEP 2 of the Accounting Cycle Why:

48

© 2014 Cengage Learning. All Rights Reserved. Learning Targets © 2014 Cengage Learning. All Rights Reserved. How: LT8Demonstrate when to end and how to start a new journal page. LT9 Identify and correct errors using standard accounting practices. Use your Aplia “Work Together” and “On Your Own” to verify concept accuracy.

50

© 2014 Cengage Learning. All Rights Reserved. A Completed Journal Page SLIDE 50 Lesson 3-4 LO8

51

© 2014 Cengage Learning. All Rights Reserved. Starting a New General Journal Page ●A new page is started by writing the page number in the space provided in the journal heading. SLIDE 51 Lesson 3-4 LO8 Page number

52

© 2014 Cengage Learning. All Rights Reserved. Correcting Errors in Journal Entries SLIDE 52 Lesson 3-4 LO9 1. 1. Sometimes an entire entry is incorrect and is discovered before the next entry is journalized. Draw neat lines through all parts of the incorrect entry. Journalize the entry correctly on the next blank line as shown on lines 9 through 12. 1 1

53

© 2014 Cengage Learning. All Rights Reserved. Correcting Errors in Journal Entries SLIDE 53 Lesson 3-4 LO9 2. 2.If an error is recorded, cancel the error by neatly drawing a line through the incorrect item. Write the correct item immediately above the canceled item as shown on lines 13 and 14. 2 2 1 1

54

© 2014 Cengage Learning. All Rights Reserved. Correcting Errors in Journal Entries SLIDE 54 Lesson 3-4 LO9 3. 3.Sometimes several correct entries are recorded after an incorrect entry is made. The next blank lines are several entries later. Draw neat lines through all incorrect parts of the entry. Record the correct items on the same lines as the incorrect items, directly above the canceled parts as shown on line 16. 3 3 1 1 2 2

55

© 2014 Cengage Learning. All Rights Reserved. Lesson 3-4 Audit Your Understanding 1.When is a general journal page complete? SLIDE 55 ANSWER When there is insufficient space to record any more entries. Lesson 3-4

56

© 2014 Cengage Learning. All Rights Reserved. Lesson 3-4 Audit Your Understanding 2.If an entire entry is incorrect and is discovered before the next entry is journalized, how should the incorrect entry be corrected? SLIDE 56 ANSWER Draw neat lines through all parts of the incorrect entry. Journalize the entry correctly on the next blank line. Lesson 3-4

57

© 2014 Cengage Learning. All Rights Reserved. Lesson 3-4 Audit Your Understanding 3.If several correct entries are recorded after an incorrect entry is made, how should the incorrect entry be corrected? SLIDE 57 ANSWER Draw neat lines through all incorrect parts. Record the correct items on the same lines as the incorrect items, directly above the canceled parts. Lesson 3-4

Similar presentations