Download presentation

Presentation is loading. Please wait.

1

Chapter 16 Dividend Policy

2

Slide Contents Learning Objectives Principles Used in This Chapter

How Do Firms Distribute Cash to their Shareholders? Does Dividend Policy Matter? Cash Distribution Policies in Practice Key Terms

3

Learning Objectives Distinguish between the use of cash dividends and share repurchases. Understand the tax treatments of dividends and capital gains, and stock dividends and stock splits.

4

Learning Objectives (cont.)

Discuss the conditions under which dividend policy is an important determinant of stock price. Describe corporate dividend policies that are commonly used in practice.

5

Principles Used in This Chapter

Principle 1: Money Has a Time Value. Principle 3: Cash Flows Are the Source of Value. Principle 4: Market Prices Reflect Information.

6

Introduction When a firm generates cash from operations, what can the firm do with the cash? Use the cash to fund new investments, Use the cash to pay off some of its debt, and/or Distribute the cash back to the firm’s shareholders either as a cash dividend or as stock repurchases.

7

Introduction (cont.) This chapter provides answers to three questions regarding a firm’s dividend policy: What are the pros and cons of the methods the firm can use to distribute cash? Why should the firm’s shareholders care about the firm’s dividend policy given that they can generate cash when they need it by selling some of their shares? What cash distribution policies do most firms use in practice?

8

16.1 How Do Firms Distribute Cash to their Shareholders?

9

How Do Firms Distribute Cash to their Shareholders?

Cash distributions can take two basic forms: Cash dividend Share repurchase

10

How Do Firms Distribute Cash to their Shareholders? (cont.)

With cash dividend, cash is paid directly to the shareholders. With a share repurchase, a company uses cash to buy back its own shares from the market place, thereby reducing the number of outstanding shares.

11

How Do Firms Distribute Cash to their Shareholders? (cont.)

The impact on the balance sheet will be as follows: On the Assets side, cash will be reduced due to cash dividend or share repurchase. On the Equity side, there will be a corresponding decrease.

12

Figure 16.1 (Cont.)

")

13

Figure 16.1 (Cont.)

")

14

Cash Dividends A firm’s dividend policy determines how much cash it will distribute to its shareholders and when these distributions will be made. Dividends are generally described in terms of dividend payout ratio, which indicates the amount of dividends paid relative to the company’s earnings.

15

Dividend Payment Procedures

Generally, companies pay dividends on a quarterly basis. There are several dates that are important with regard to dividend payment: (a) Announcement date: It is the date on which dividend is formally declared by the board of directors.

Announcement date: It is the date on which dividend is formally declared by the board of directors.")

16

Dividend Payment Procedures (cont.)

(b) Date of record: Investors who own stock on this date receive the dividend. However, this date was pushed forward two days to ex-dividend date. (c) Ex-dividend date: This is two days before the date of record and any investor who buys shares after the ex-dividend date is not entitled to dividend.

Date of record: Investors who own stock on this date receive the dividend. However, this date was pushed forward two days to ex-dividend date. (c) Ex-dividend date: This is two days before the date of record and any investor who buys shares after the ex-dividend date is not entitled to dividend.")

17

Dividend Payment Procedures (cont.)

(d) Payment date: This is the date on which dividend checks are mailed to the investors.

Payment date: This is the date on which dividend checks are mailed to the investors.")

18

Dividend Payment Procedures (cont.)

Date Explanation Calendar Date Announcement Date Dividend is declared. March 15 Ex-Dividend Date Shares begin trading ex-dividend. May 17 Record Date Dividend will be paid to shareholders who own the stock on this date. May 19 Payment Date Dividends are distributed to the shareholders of record on the record date. May 27

19

Stock Repurchases (Stock Buyback)

Stock repurchase is when a firm uses its cash to repurchase some of its own stock. This results in a reduction in the firm’s cash balance as well as the number of shares of stock outstanding. Firms use one of three methods to purchase the shares: Open market repurchase, tender offer, and direct purchase.

20

How do Firms Repurchase Their Shares?

Open Market Repurchase Here the firm acquires the stock on the market, often buying a relatively small number of shares everyday. This will put upward pressure on share prices. This is the most widely used method for stock repurchase.

21

How do Firms Repurchase Their Shares? (cont.)

Tender Offer A company uses this method when it wants to buy a relatively large number of shares very quickly. The company makes a formal offer to buy a specified number of shares at a stated price. The price is set above the market price to attract sellers.

22

How do Firms Repurchase Their Shares? (cont.)

Direct Purchase from a large investor Here the firm purchases the stock from one or more major stockholders on a negotiated basis. This method is not used frequently.

23

Personal Tax Considerations – Dividend Versus Capital Gains Income

Historically, tax laws have favored capital gains income over dividend income. However, the 2006 Tax Act lowered the tax rate on dividends and long-term capital gains (stock held for more than 1 year) to 15% for most people.

to 15% for most people.")

24

Personal Tax Considerations – Dividend Versus Capital Gains Income (cont.)

To qualify for the lower tax rate on dividends, the stock must be held for more than 60 days during the 120-day period that begins 60 days before the ex-dividend date. If not, dividends will be taxed as ordinary income.

25

Non-Cash Distributions: Stock Dividends and Stock Splits

A stock dividend is a pro-rata distribution of additional shares of stock to the firm’s current stockholders. These distributions are generally defined in terms of a fraction paid per share. For example, a firm might pay a stock dividend of .20 shares of stock per share or 2 shares for every 10 held.

26

Non-Cash Distributions: Stock Dividends and Stock Splits (cont.)

Stock split is essentially a very large stock dividend. For example, a 2-for-1 split would entail receiving two new shares for every old share currently held. With a 2-for-1 split, the number of shares will double and the share price will drop in half.

27

Rationale for a Stock Dividend or Stock Split

One rationale for splits and stock dividends is that there is an optimal price range for the firm’s stock. Also, beyond a certain price range, there might be lower demand for shares from investors. If the price exceeds that optimal range, it can be brought back to the optimal range by doing a stock split or paying stock dividend.

28

16.2 Does Dividend Policy Matter?

29

Does Dividend Policy Matter?

Modigiliani and Miller suggest that without taxes and transaction costs, cash dividends and share repurchases are equivalent and the timing of the distribution is unimportant. This is known as the Modigiliani and Miller dividend irrelevancy proposition.

30

The Irrelevance of the Distribution Choice

The distribution choice is irrelevant under the following assumptions: There are no taxes. No transaction costs are incurred in either buying or selling shares of stock. The firm’s operating and investment policies are fixed.

31

The Irrelevance of the Distribution Choice (cont.)

The dividend irrelevancy proposition can be illustrated in two ways: Timing of dividend distributions does not affect firm value. In the absence of taxes and transaction costs, a cash dividend is equivalent to a share repurchase.

32

The Timing of Dividend is Irrelevant

Figure 16.2 (Cont.)

")

33

Figure 16.2 (Cont.)

")

34

The Timing of Dividend is Irrelevant (cont.)

Figure 16-2 considers two alternatives: Pay $35 million now and $135 million in one year Pay $52.5 million now and $ million in one year In both cases, the value of share remains the same at $15.24 per share.

35

Checkpoint 16.1 Stock Price and the Timing of Dividend Payments

After operating for more than 50 years, the owners of the Northwest Wire and Cable Company decided that it was time to shut down the firm’s business at the end of the year. However, the firm has $4 million in cash available for distribution to its shareholders today and expects to have $30 million at the end of the year to pay as a liquidating dividend. Northwest has 3 million shares outstanding today and is contemplating one of two cash distribution policies. The first (Alternative #1) involves simply paying cash dividends equal to the firm’s cash flow both today and at the end of the year. Alternative #2 involves paying a much larger dividend today of $12 million and issuing new shares of stock to raise the $8 million in additional funds needed to fund the dividend. The company’s stockholders require a 12% rate of return on the firm’s shares. What is the value of the firm’s equity in total and per share under the two dividend payment plans where the firm has 1 million shares of stock outstanding before issuing any new shares?

involves simply paying cash dividends equal to the firm’s cash flow both today and at the end of the year. Alternative #2 involves paying a much larger dividend today of $12 million and issuing new shares of stock to raise the $8 million in additional funds needed to fund the dividend. The company’s stockholders require a 12% rate of return on the firm’s shares. What is the value of the firm’s equity in total and per share under the two dividend payment plans where the firm has 1 million shares of stock outstanding before issuing any new shares")

36

Checkpoint 16.1

37

Checkpoint 16.1

38

Checkpoint 16.1

39

Checkpoint 16.1: Check Yourself

Consider Alternative #3 in which Northwest Wire and Cable decides to increase its current period dividend to only $8 million. Show that the firm’s equity under this scenario would be $30.79 million.

40

Step 1: Picture the Problem

The firm is considering two alternatives: Pay $4 million today and $30 in year 1 as liquidating dividend; or Pay $8 million today and pay $25.52 in year 1 ($30 million - $4million*1.12 paid to new shareholders)

")

41

Step 2: Decide on a Solution Strategy

The value of Northwest Wire and Cable company’s equity is equal to the present value of the firm’s expected cash dividends. We can estimate the value using equation 16-1.

42

Step 3: Solve Value – Alternative 1

Value = $4 million + $25.52 million /(1.12)1 = $30.79 million

1. = $30.79 million.")

43

Step 3: Solve (cont.) Value – Alternative 2

Value = $8 million + $30 million /(1.12)1 = $30.79 million

1. = $30.79 million.")

44

Step 4: Analyze This example illustrates that the timing of dividend payment does not affect the value of the firm. This was true because we held constant the firm’s investment cash flows. We also assumed that the new shares could be issued under the same terms as the existing shares.

45

The form of Payment (Cash Dividend Versus Share Repurchase) is Irrelevant

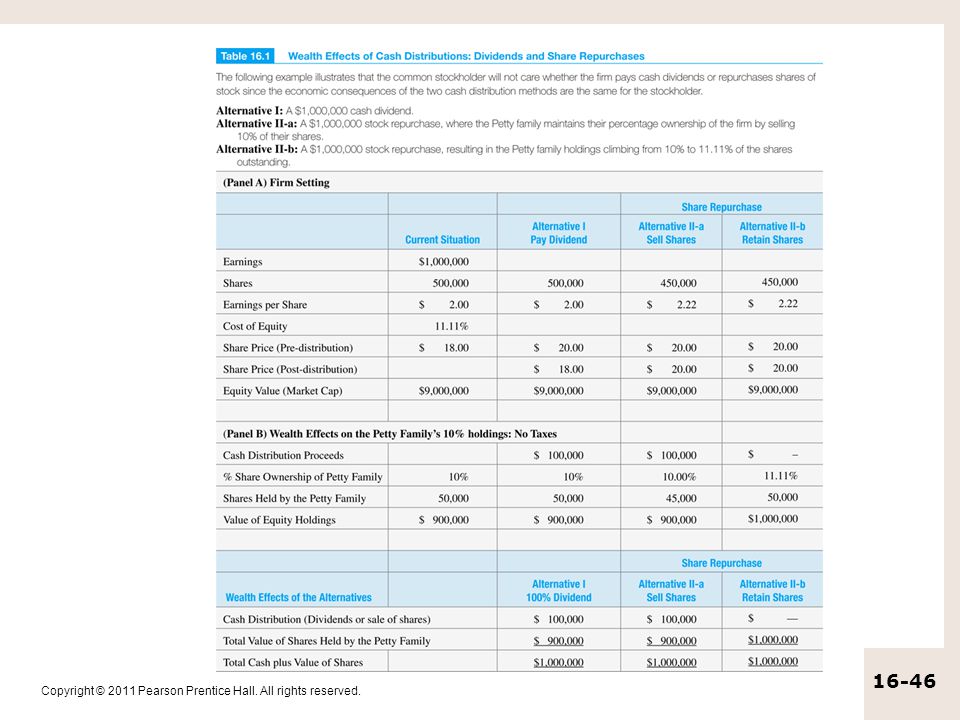

Table 16-1 illustrates two possibilities for the use of $1,000,000 in cash flows: A $1,000,000 cash dividend A $1,000,000 stock repurchase It is observed that the value is the same so an investor will be indifferent between the two options.

47

Individual Investor Wealth Effects – Personal Taxes

What are the tax rules with regard to dividends and share repurchases? 100% of cash dividends are taxable in the year in which they are received. When individuals sell shares, tax is assessed only on the capital gain (i.e. price appreciation of stock).

.")

48

Individual Wealth Effects – Personal Taxes (cont.)

If an individual decides not to sell his or her share back to the company making the stock repurchase, they will not incur any taxes.

49

Individual Wealth Effects – Personal Taxes (cont.)

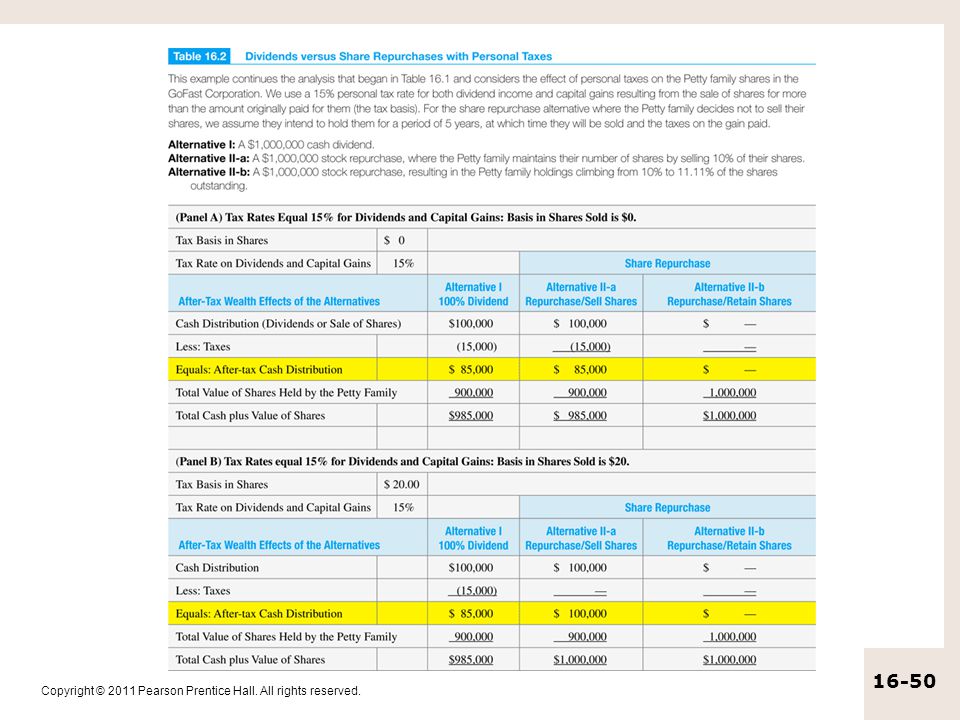

Table 16-2 shows the cash flow consequences of the alternative methods for distributing cash to the shareholders that were introduced in Table 16-1. It is assumed that both dividends and capital gains are taxed at 15%.

51

Why Dividend Policy is Important?

Transactions are costly Since taxes are incurred when dividends are received and transactions costs are incurred when buying and selling shares, investors will prefer to select companies whose dividend policy match up with their own preferences. Because firms with different dividends attract different dividend clienteles, it is important that dividend policy remain somewhat stable.

52

Why Dividend Policy is Important? (cont.)

The Information Conveyed by Dividend and Share Repurchase Announcement Investors and stock market are constantly trying to decipher the information released by firms to better understand what they imply about firm values. Firms tend to increase their dividends when dividends can be sustained in the future. In such cases, dividend increase is clearly good news.

53

Why Dividend Policy is Important? (cont.)

Share repurchases are also viewed very favorably as it reveals that the firm has generated more money than it currently needs. Share repurchases may also reveal that the equity is currently underpriced. The empirical evidence indicates that dividends and share repurchases do in fact convey favorable information to investors.

54

Why Dividend Policy is Important? (cont.)

The Information Conveyed by Stock Dividends and Stock Splits The announcement of stock dividends and stock splits also tend to generate positive stock returns. This increase is harder to explain as stock dividends and stock splits do not affect firm’s cash flows. Some researchers have suggested that firms have a preferred trading range and stock splits help bring stock prices to that trading range.

55

Why Dividend Policy is Important? (cont.)

A second possibility is that stock splits and stock dividends tend to attract attention. Naturally, firm would like to attract attention only when the prospects are favorable. Thus even though there is no direct effect on cash flows, the market reacts favorably.

56

16.3 Cash Distribution Policies in Practice

57

Cash Distribution Policies in Practice

Stable Payout In a survey of CEOs, most CEOs recognized the importance of maintaining consistency and stability in dividend policy. See figure 16-3, panel a and b.

58

Figure 16.3 (Cont.)

")

59

Figure 16.3 (Cont.)

")

60

Stock Repurchase Decisions

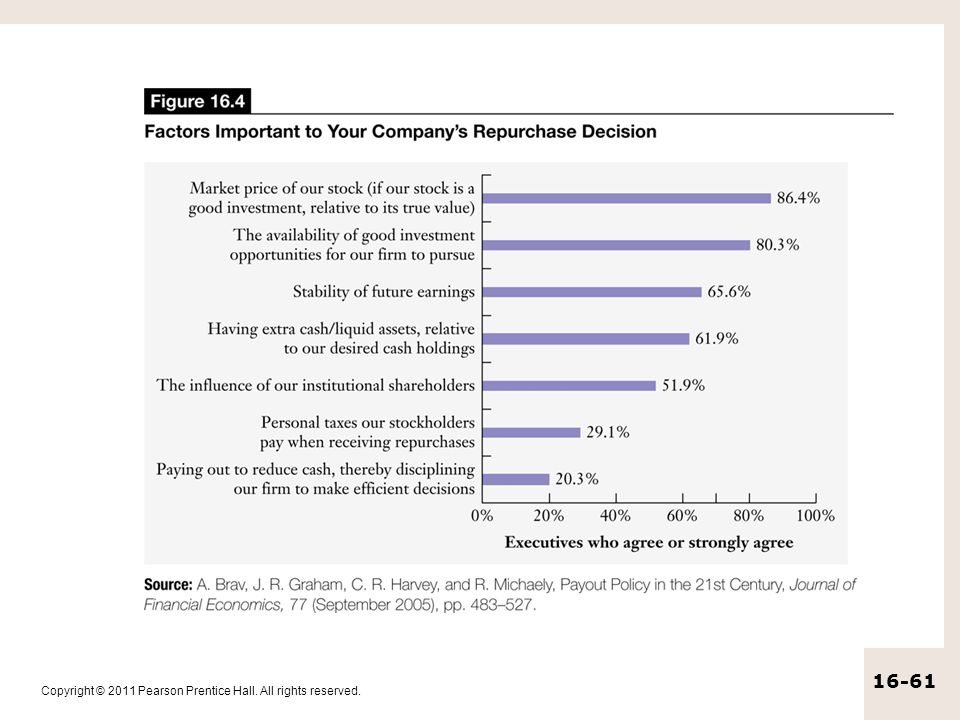

Figure 16-4 reveals that stock repurchase decisions are driven by executive’s feeling that the stock is a good investment relative to its true value and that there are a lack of good investment opportunities to invest in.

62

Dividends versus Repurchases

Table 16-3 provides a summary of factors influencing the payout policy. Flexibility emerges as a major factor in the choice of repurchases as opposed to dividends.

64

Residual Dividend Policy

With a residual dividend policy, the firm first finances its investments using its own earnings. Dividends are paid out of the residual earnings that are not needed to finance new investment opportunities. While this policy minimizes the cost of financing, it can lead to unstable dividends for shareholders.

65

Other Factors Playing a Role in How Much to Distribute

Liquidity Position Because dividend payments and stock repurchases are made with cash, and not with retained earnings, the firm must have cash available for payouts to be made.

66

Other Factors Playing a Role in How Much to Distribute (cont.)

Lack of Other Sources of Financing Many small or new companies may not have access to the capital markets, and must depend upon internally generated funds to fund their investment opportunities. As a result, the dividend pay out ratio for such firms is generally lower.

67

Other Factors Playing a Role in How Much to Distribute (cont.)

Earnings Predictability A company’s payout ratio depends to some extent on the predictability of a firm’s profits over time. Firms with stable earnings will typically pay out a larger portion of its earnings.

68

Key Terms Cash dividend Date of record Declaration date

Dividend clienteles Dividend payout ratio Dividend policy Ex-dividend date

69

Key Terms (cont.) Open market repurchases Payment date

Residual dividend payout policy Stock dividend Stock repurchase Stock split Tender offer

Similar presentations

>")