Download presentation

Presentation is loading. Please wait.

1

Accounting for Rural Transits

Presented by The Ohio Department of Transportation Office of Transit Office of External Audits

2

Please turn phones to vibrate

Housekeeping Restrooms Smoking Area Cafeteria Details Please turn phones to vibrate

3

Training Focus County Transit Boards Governmental Units

City County Municipalities Villages Private Nonprofit Corporations Regional Transit Authorities

4

Topics - AM Roles & Responsibilities Accrual Accounting

Supporting Documentation/Proper Documentation Invoicing Revenue Classification Reporting

5

Topics - PM Expenses Cost Allocation Plans/Overhead

Eligible/Ineligible Adjustments/Offsets Operating vs. Capital (No double dipping) Vehicle Operation Maintenance Non-Vehicle Operation Maintenance Cost Allocation Plans/Overhead Common Audit Findings

Vehicle Operation Maintenance. Non-Vehicle Operation Maintenance. Cost Allocation Plans/Overhead. Common Audit Findings.")

6

Roles & Responsibilities

7

Roles & Responsibilities

Ohio Department of Transportation (ODOT)

")

8

ODOT’s Role & Responsibilities

State agencies (ODOT) are responsible for: providing oversight of Federal and State funds ensuring that funds are used appropriately ensuring compliance with Federal and State guidance ensuring compliance with the terms of the contract

are responsible for: providing oversight of Federal and State funds. ensuring that funds are used appropriately. ensuring compliance with Federal and State guidance. ensuring compliance with the terms of the contract.")

9

ODOT Roles & Responsibilities

Two primary methods: Desk Inspections Audits (On-site)

")

10

ODOT’s Roles & Responsibilities

Desk Inspections Review audit reports issued by Auditor of State and Independent Public Accountants (IPAs) Reconcile Schedule of Expenditures of Federal Awards Confirm receipt /recognition of federal funds Identify and follow-up on audit findings & issues Bring significant or material issues to attention of the Office of Transit

Reconcile Schedule of Expenditures of Federal Awards. Confirm receipt /recognition of federal funds. Identify and follow-up on audit findings & issues. Bring significant or material issues to attention of the Office of Transit.")

11

ODOT Roles & Responsibilities

Audits Conducted on-site (4 – 5 days) Cover a specific period of time (years) Up to 3 years after final payment Formal Entrance & Exit conference Request documents in advance of on-site Review, reconcile and verify Financial statements to General Ledger ODOT invoices to Transit source documents Sample of transaction (revenue and expense) Issue audit report Findings for recovery Corrective Action Plan

Cover a specific period of time (years) Up to 3 years after final payment. Formal Entrance & Exit conference. Request documents in advance of on-site. Review, reconcile and verify. Financial statements to General Ledger. ODOT invoices to Transit source documents. Sample of transaction (revenue and expense) Issue audit report. Findings for recovery. Corrective Action Plan.")

12

How is a Transit selected for Audit?

Risk Assessment performed annually Combination of financial and programmatic criteria Input from Office of Transit Includes, but not limited to: Federal Funding/federal sources Prior audit findings (AOS) Prior QAR findings Accuracy of invoicing

Prior QAR findings. Accuracy of invoicing.")

13

Additional Oversight Methods

Produce annual report to assist Transits with Federal Reporting AKA “Pink Book” Available on ODOT – Audits website for Transits Review Cost Allocation Plans Review Charge Rates (Central Garage) Provide training and technical assistance

Provide training and technical assistance.")

14

Roles & Responsibilities

Transits

15

Transit Responsibilities

Follow Federal and State guidance Office of Management and Budget (OMB) Guidance (See chart) Ohio Revised Code GAAP (Generally Accepted Accounting Principles) FTA Guidance ODOT Rural Transit Manual Comply with terms of contract Requires the use of accrual accounting

Guidance (See chart) Ohio Revised Code. GAAP (Generally Accepted Accounting Principles) FTA Guidance. ODOT Rural Transit Manual. Comply with terms of contract. Requires the use of accrual accounting.")

16

Federal Guidance Available at

17

Transit – General Requirements

Must use accrual accounting when invoicing ODOT. Must provide supporting documentation for revenue and expense. Must provide detail to support cost allocation and overhead rates charged

19

Accrual Accounting

20

Accrual Accounting Fundamental concept of GAAP Accrual Accounting matches revenues and expenses to the period earned or incurred

21

Accounting Basics are necessary

To understand Accrual Accounting Accounting Basics are necessary

22

What is a debit or a credit?

This is commonly referred to as a “T” account. Left Side Right Side

23

Assets = Liabilities + Equity

Accounting Equation Assets = Liabilities + Equity

24

What is the “normal balance”?

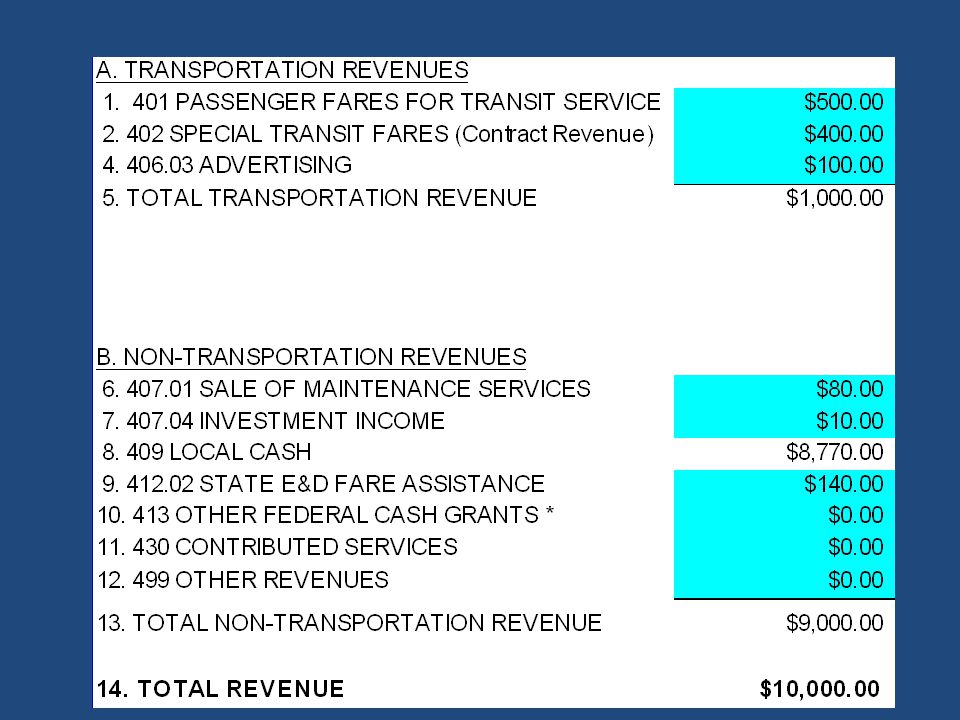

The normal balance is the side of the T-account that represents an increase. This is the side the balance should be on.

25

Normal Balances

26

What is the Difference between Cash and Accrual Accounting?

Revenue when received Expense when paid Disregards matching / timing (revenue in one month – expense in a different month) Application: Personal Household Revenue when earned Expense when incurred Matches revenue & expense to period (month, quarter, year) Application: Company

Application: Personal Household. Revenue when earned. Expense when incurred. Matches revenue & expense to period (month, quarter, year) Application: Company.")

27

Benefits of Accrual Accounting with Transit Grant

Perfect match to grant budget Whereas costs are applied over 12 months True cost of business is reflected Allows for better projections for future years Allows for better management of Transit organization finances

29

Accrual Accounting Transit Examples Revenue Liability Expense

30

An example of an accrual – contract revenue

Transit Services (rides) provided in January. Invoice in the amount of $5,000 sent to provider in February. Provider pays $5,000 invoice in March When does the Transit record the revenue?

provided in January. Invoice in the amount of $5,000 sent to provider in February. Provider pays $5,000 invoice in March. When does the Transit record the revenue")

31

An example of an accrual – contract revenue

When does the Transit record the revenue? Revenue must be recorded in the time period earned, which would be January for this example. Before accounting records are closed for January, the entry must be recorded. What is the accounting entry?

32

Adjusting Journal Entry to record revenue earned

There is no exchange of cash – only the recording of the revenue and amount due.

33

T-Account entries

34

Journal Entry to Record Cash Receipt in March

35

T-Account entries

36

Accrual Accounting - Revenues

Revenues earned during the period but no cash payment has been received: Contract revenue Advertising revenue Maintenance Revenue May be billed and payment not received May not be billed

37

What does the transit record?

Insurance Liability Transit receives invoice for insurance - $12,000 for the current year in January. Transit pays $12,000 invoice in January. When does the Transit record the expense? What does the transit record?

38

An example of an accrual – Insurance Expense

When does the Transit record the expense? What does the transit record? Expense must be recorded in the time period incurred, which would be January – December for this example. $1,000 insurance expense will be recognized each month. A prepaid expense is recorded initially. What is the accounting entry?

39

Journal Entries Entries would also be made for April - November

40

What does the transit record?

Insurance Liability Transit receives invoice for insurance - $12,000 for the current year in January. Transit pays $3,000 quarterly. When does the Transit record the expense? What does the transit record?

41

An example of an accrual – Insurance expense

When does the Transit record the expense? What does the transit record? Expense must be recorded in the time period incurred, which would be January – December for this example. $1,000 insurance expense will be recognized each month. A prepaid expense is recorded initially. What is the accounting entry for the quarterly payment and the monthly accrual?

43

An example of an accrual – Utility Services

Utilities Services provided to Transit in January. Invoice received in February for January services in the amount of $1,000. Transit pays $1,000 invoice in March. When does the Transit record the Expense?

44

An example of an accrual – Utility Expense

When does the Transit record the expense? Expenses must be recorded in the time period incurred, which would be January for this example. Before accounting records are closed for January, the entry must be recorded. What is the accounting entry?

45

Adjusting Journal Entry to record expense

No payment of cash, just the accrual of utility expense – (can be a reasonable estimate.)

")

46

T-Account entries

47

Journal Entry to Record Cash Payment in March

48

T-Account entries

49

Overall Effect to Accounts

51

Accrual Accounting - Expenses

Expenses incurred during the period, but no cash payment has yet been made: Utility expenses incurred but not yet paid Repair services and/or parts received, but not yet paid Advertising Payroll Fuel Considers any good or service received, for which payment has not yet been made.

52

True or False 1. GAAP allows cash basis accounting. FALSE

53

True or False Accrual accounting requires matching of revenues and expenses in the same period. TRUE

54

True or False Accounts receivable and accounts payable entries are necessary with cash basis accounting. FALSE

56

Supporting Documentation

57

Grant – Common Rule 49 CFR 18.20 Pursuant to the Standards for financial management systems, a transit is responsible for meeting the standards provided for: Financial reporting Accounting Records Internal Control Budget Control Allowable Costs Source Documentation Cash Management Transit bears the burden to support all claims of revenue and expense.

58

As seen in…. Jerry Maguire 1996

59

Supporting Documentation

Revenues and Expenses invoiced to ODOT Must be supported by General Ledger Listing of transactions from your accounting system Must be able to reconcile amounts if multiple accounts are tied to one line item on the ODOT invoice Must be supported by actual deposits or invoices or accrued journal entries If payments are made to vendors by statement, individual invoices with detail must be provided Examples provided later in Training

60

Transit Process Invoice Receipt Review and Approve Process for Payment

Retain documentation

61

ODOT Process ODOT Quarterly Invoice

Verify to General Ledger & Financials Verify to actual invoices (not statements)

")

62

True or False Monthly credit card statements are sufficient documentation for quarterly expenses charged to ODOT. FALSE

63

True or False A paid invoice represents a valid Transit expense that can be charged to ODOT. FALSE

64

True or False When reviewing transactions selected for audit, if the supporting documentation cannot be provided, the cost may be ineligible for ODOT reimbursement. TRUE

66

Revenue

67

49 CFR – Program Income Grantees are encouraged to earn income to defray program costs. Maintenance Service Advertising Income

68

Revenue Classification

Drives the amount of reimbursement provided by ODOT Incorrect classification can result in: Loss of reimbursement if not found prior to project close-out. Requirement of payback for over –payment due to revenue misclassification

70

$4,750 (1/2 of $9,500 operating expenses are eligible for Federal Assistance after offsets from Passenger Fares. The other half ($4,750) will be considered for Non-Federal Assistance. Passenger Fares (Farebox Revenue) is applied to expenses total allowable expenses prior to consideration of Federal Assistance.

is applied to expenses total allowable expenses prior to consideration of Federal Assistance.")

71

Non-Federal Share begins with 50% left from 50% Federal Assistance.

$4,750 was eligible for Federal funding in the previous slide - The remaining $4,750 is considered eligible for non-Federal share. After local revenue and State E&D Fare Assistance is applied, the remaining non-Federal share is available for State Assistance.

72

What affect does reporting Contract revenue as Farebox revenue have on Federal Reimbursement?

Earned $80,000 in contract Revenue Earned $20,000 in Fare box Revenue Total Eligible Expenses = $206,600

73

What affect does reporting Contract revenue as Farebox revenue have on Federal Reimbursement?

Reported both contract and farebox revenue as farebox revenue: Reported revenue correctly: Transit would have lost the opportunity to be reimbursed for $40,000

74

What affect does reporting Farebox revenue as Contract revenue have on Federal Reimbursement?

Reported both contract and farebox revenue as contract revenue: Reported revenue correctly: Transit would have been overpaid $7,000 originally, but will eventually be required to pay the amount back to the Office of Transit. $100,000 is contract max.

75

Transportation Revenue

401 Passenger Fares Regular and discounted cash fares Pre-purchased tickets or tokens even when purchased by a contract provider if sold at fare box price Fare price dictates record, not purchaser Cash contributions or donations from passengers This includes tips 402 Special Transit Fares Contract Revenues Must be fully allocated cost* Not general fare rate Non-Contract Special Service Fares Donations from others for providing service for a special event Fares are not guaranteed on a contractual basis

76

Transportation Revenue

Advertising Revenues Revenues received for selling advertising space on the interior or exterior of Operating vehicles Determining amount to charge Sale of Maintenance Services Revenues received for performing maintenance services on vehicles and equipment owned by other agencies, organizations and individuals. Profits can be used as local matching Losses not eligible for Federal & State funding Cannot charge other for services and also charge to Transit Grant

77

Non-Transportation Revenue

Investment Income Interest earned on deposited public transportation funds Should be recorded even when in City, County, or Agency Cash on deposit 409 Local Cash Grants & Reimbursements Funds obtained from local government units that assist in defraying costs for public transportation. Includes funding from City or County Populates automatically on invoice

78

Non-Transportation Revenue

State Senior Citizens Fare Assistance Revenues received from the Ohio Elderly & Disabled (E & D) Transit Fare Assistance Program 413 “Other” Federal Cash Grants & Reimbursements Includes funds received from the Federal Government that help defray the costs of providing public transportation services. Originally set up for some other program CDBG, CSBG HUD, Local Assistance Federal direct payments are not included

Transit Fare Assistance Program. 413 Other Federal Cash Grants & Reimbursements. Includes funds received from the Federal Government that help defray the costs of providing public transportation services. Originally set up for some other program CDBG, CSBG HUD, Local Assistance. Federal direct payments are not included.")

79

Non-Transportation Revenue

430 Contributed Services In-kind services received from another agency, organization, or individual in which the grantee is under no obligation to pay for the services. Must be approved by Office of Transit prior to claiming. Must be matched by offsetting costs in expense accounts. All in-kind expenses and revenues must be documented Can be difficult to value and document. Third parties can provide contributed services - may include associations, but not Federal , State or Local governmental agencies. Must be performed during period to which matching requirement applies. Cannot claim expense twice – for two different grants, or used as matching for other grants. Must be verifiable

80

An Example of great supporting Revenue detail from an Audited Transit

81

Example of Invoice Detail

279,315.35 $ Example of Transit GL Detail

82

Although this is listed as Other Revenue, this should be in Investment Income. However great match of dollars to GL.

83

Revenue Review *Dependent on Available Contract Award

84

How do I set up a Capital Replacement fund?

Program must be approved by Office of Transit prior to implementation Applicable to Transit Agencies providing contract operating services. (Rides only) Charge an additional rate per mile or hour on contract Average .10 to .13 cents per mile Office of Transit can provide a spreadsheet for calculating Helps offset local share Applied to Capital invoice, not operating invoice Need to establish a separate bank account for the restricted funds Money cannot be used for other items such as operating matching Cash from vehicles sold must go back to Transit Program Recommend the cash goes to capital replacement Whether there is a capital replacement fund or not Transit must track funds from vehicles sold Cannot set money aside from operating for capital replacement

Charge an additional rate per mile or hour on contract. Average .10 to .13 cents per mile. Office of Transit can provide a spreadsheet for calculating. Helps offset local share. Applied to Capital invoice, not operating invoice. Need to establish a separate bank account for the restricted funds. Money cannot be used for other items such as operating matching. Cash from vehicles sold must go back to Transit Program. Recommend the cash goes to capital replacement. Whether there is a capital replacement fund or not. Transit must track funds from vehicles sold. Cannot set money aside from operating for capital replacement.")

85

True or false

86

True or False In claiming contract revenue as fare box revenue, the eligible amount for Federal reimbursement is negatively impacted. TRUE

87

True or False 2. A rural transit agency should have interest income to report on the ODOT operating invoice each quarter. TRUE

88

True or False 3. When a Transit Maintenance garage sells services to other non-Transit departments, or to external customers, these revenues should be reflected on the ODOT invoice. TRUE

90

Eligible Expenses

91

Eligible Expenses per A-87 (city, state) per A-122 (non-profit)

To be allowable under Federal awards, costs must be: Necessary and reasonable for proper and efficient performance and administration of Federal awards. May not be included as a cost or used to meet cost sharing or matching requirements of any other Federal award. Must be able to withstand public scrutiny Allocable to Federal Awards A-87 - (2 CFR part 225) A-122 (2 CFR part 230) In accordance with GAAP Authorized or not prohibited under State or local laws or regulations Be the net of all applicable credits Be adequately documented

A-122 (2 CFR part 230) In accordance with GAAP. Authorized or not prohibited under State or local laws or regulations. Be the net of all applicable credits. Be adequately documented.")

92

Eligible Expenses Per USOA:

For transit agencies providing more than one mode of service, it is necessary to further identify and classify labor compensation by each mode of service. In most multi-mode systems, some labor is directly associated with each mode and some labor jointly serves more than one mode. Demand Response vs. Fixed Route Uniform System of Accounts (for Transits)

")

93

Reporting expenses Report all Transit expenses, even if ineligible

Provides true cost of providing service. Provides transparency to all elements of expense Total cost of eligible + ineligible should reconcile to the general ledger/financials for the Transit.

94

ODOT invoice - Which column to use?

95

Invoice Expense Headings

96

Vehicle Operations and Vehicle Maintenance

Supervising station and terminal transportation activities; clerical support for transportation administration activities, operators report, standby, instructor operators, inspecting operator performance, reporting accidents, representing union, selecting runs during sign-up, administering sign-ups.

97

Vehicle Operations and Vehicle Maintenance

Providing supervision and clerical support for the administration of vehicle maintenance, preparing and updating vehicle maintenance records, accumulating and computing vehicle performance data, (e.g., mileage, fuel and oil consumption), providing technical training to vehicle maintenance personnel….

, providing technical training to vehicle maintenance personnel….")

98

Non-vehicle maintenance

Providing supervision and clerical support for the administration of transit way and structures maintenance and other buildings, grounds and equipment maintenance; preparing and updating transit way and structures maintenance records and other buildings, grounds and equipment maintenance personnel….

99

General Administration

101

ODOt invoice - Which ROW to use?

102

Which ROW to use?

103

ODOT Invoice Snapshot – Salary and Wages

104

Examples of Eligible Expenses

Operator’s Salaries and Wages Cost of labor for transit agency’s employees who are classified as revenue vehicle operators. Wages for performing revenue vehicle operations (stand-by time, inspection, maintenance of revenue vehicles, servicing revenue vehicles, and customer service) DOES NOT include operator’s wages for performing non-vehicle maintenance functions Labor – Other Salaries and Wages Labor of employees of the transit agency who are not classified as revenue vehicle operators Wages for maintenance workers, administrative staff and transit managers Salaries & Wages (in general) Payments to employees arising from the performance of work, Shift differentials Overtime Premiums Minimum Guarantees Other non-fringe benefit labor costs

DOES NOT include operator’s wages for performing non-vehicle maintenance functions. Labor – Other Salaries and Wages. Labor of employees of the transit agency who are not classified as revenue vehicle operators. Wages for maintenance workers, administrative staff and transit managers. Salaries & Wages (in general) Payments to employees arising from the performance of work, Shift differentials. Overtime Premiums. Minimum Guarantees. Other non-fringe benefit labor costs.")

105

ODOT Invoice Snapshot – Fringe Benefits

106

Fringe Benefits All payments and accruals to others (insurance, government) on behalf of employees of the Transit agency. Payments to employee for leave. Payments arise from the employment relationship, but are over and above “labor” costs. FICA Pension Plans Medical Plans Dental Plans Life Insurance Plans Disability Plans Unemployment Insurance Workers Compensation Sick Leave, Holiday, Vacation Other paid absence (military duty, jury duty, and bereavement)

")

107

Eligible Expense – Separate Accounts

Can cash be transferred to a separate account for transit employees’ vacation payouts? Assume this is related to an employee - separation from service. It depends – By-laws, Board of Directors, agency policies. Transit has an obligation to pay employee for leave payout at some point in the future = Liability. Governmental Accounting Standards Board - Statement No. 16 Accounting for Compensated Absences (Issued 11/92) Vacation leave and other compensated absences with similar characteristics should be accrued as a liability as the benefits are earned by the employees if the leave is attributable to past service and it is probable that the employer will compensate the employees for the benefits through paid time off or some other means, such as cash payments at termination or retirement. Statement of Financial Accounting Standards No. 43 "Accounting for Compensated Absences“ Issued in November 1980

Vacation leave and other compensated absences with similar characteristics should be accrued as a liability as the benefits are earned by the employees if the leave is attributable to past service and it is probable that the employer will compensate the employees for the benefits through paid time off or some other means, such as cash payments at termination or retirement. Statement of Financial Accounting Standards No. 43 Accounting for Compensated Absences Issued in November")

108

Examples of Eligible Expenses

Management Service Fees Compensation for Personal Services Per Cost Principles - Includes but is not limited to salaries, wages, director’s and executive’ committee member’s fees, fringe benefits, pension plan costs….to the extent that: Compensation to individual employee is reasonable for the services rendered rather than a distribution of earnings in excess of costs.

109

Examples of Eligible Expenses

Advertising Fees When incurred for the purpose of: recruitment of personnel procurement t of goods and services disposal of surplus materials acquired in the performance of a Federal award.

110

Examples of Eligible Expenses

Professional/Technical Services Per Cost Principles - When rendered by persons who are members of a particular profession or possess a special skill and who are not officers or employees of the organization. Consideration must be made to whether the service can be performed more economically by direct employment Attorneys, Accountants, Auditors, Investment Bankers, Computer Service Companies, Engineering Firms, Management Consultants and Transit Industry Consultants

111

Examples of Eligible Expenses

Temporary Help When incurred for the sole purpose of Transit Activities Work in the capacity of a transit agency employee under the supervision of transit agency personnel. Indirect salaries & Wages

112

Examples of Eligible Expenses

Contract Maintenance Services Per Cost Principles - When Incurred for necessary maintenance, repair or upkeep of Transit equipment Provided by external supplier Includes Central Garage for city/county Must be charged at actual cost, net of applicable credits Parts and supplies from general stores or stockrooms should be charged at their actual net cost. Upcharge cannot be applied to costs billed to grant

113

Examples of Eligible Expenses

Custodial Services – performance of janitorial services under contract or on a single job basis with an outside organization. Other Services – Services not included previously Drug testing

114

Invoice Snapshot – Materials & Supplies

115

Examples of Eligible Expenses

Fuels & Lubricants Less fuel tax rebate (discussed later with offsets) Tires & Tubes For Transit vehicles Other Materials and Supplies Issued from inventory or purchased for immediate consumption Vehicle maintenance parts Cleaning supplies Office forms

Tires & Tubes. For Transit vehicles. Other Materials and Supplies. Issued from inventory or purchased for immediate consumption. Vehicle maintenance parts. Cleaning supplies. Office forms.")

116

ODOT Invoice Snapshot –Utilities

117

Examples of Eligible Expenses

Utilities other than Non-Propulsion Electric Natural Gas Water & Sewer Trash collections Telephone Transit having separate building – full cost is charged to Transit. Transit using shared area – only pro-rata share to be applied Cost Allocation Plan is necessary

118

ODOT Invoice Snapshot – Casualty & Liability Costs

119

Examples of Eligible Expenses

Casualty & Liability Costs Costs for the protection of the transit agency from loss through insurance program, compensation of others for their losses due to incidents for which the transit is liable. Premiums for Physical Damage To insure against loss through damage caused by collision, fire, theft, flood earthquakes and other types of losses. Recoveries of PD From Insurance companies or 3rd parties involved in accident Need to be entered as a negative amount on invoice. Credits discussed later in offsets.

120

ODOT Invoice Snapshot – Taxes

121

Examples of Eligible Expenses

Property Taxes Based upon valuation of property owned by Transit Vehicle Licensing and Registration Fees Only Transit Vehicles Non-Profits would need to include on invoice to ODOT

122

ODOT Invoice Snapshot – Purchased Transportation Services

123

Examples of Eligible Expenses

Purchased Transportation Services Third Party Service Provider – ODOT Office of Transit must approve contract.

124

ODOT Invoice Snapshot – Miscellaneous

125

Examples of Eligible Expenses

Dues & Subscriptions Lobbying costs are unallowable Transit Related Fees for Membership in industry organizations Membership must be in name of grantee organization and not in the name of an individual Subscriptions to periodicals Subscription to local newspaper is not an eligible expense.

126

Examples of Eligible Expenses

Travel & Meetings Per Conus Rates Cannot claim expenses covered by scholarship awards on invoice

127

Miscellaneous Expenses

Bridge, tunnel, and highway tolls Bad Debt Expense Costs are ineligible Report in Non-Eligible column to reflect true costs

128

Miscellaneous Expenses

Other Miscellaneous Expenses Costs that were not detailed in other categories defined. Parking fees, copying, Staff recognition based upon performance Includes: Per cost principle: Staff recognition – to include employee morale and health and welfare costs. Certificate for years of service Attendance bonus - $25 savings bond

129

Miscellaneous Expenses

Other Miscellaneous Expenses Does not Include: Retirement Gifts Flowers or gifts of any kind Food, coffee, pop, gift cards, hams, turkeys, tickets to games or events, company picnics, outings, etc. Office pool – coffee/pop

130

ODOT Invoice Snapshot – Interest Expense

131

Examples of Eligible Expenses

Interest Expense On long term debt for capital assets Sales & Rentals All lease agreements require prior approval from the Office of Transit Applies to vehicles, facilities, & other capital items.

132

Leases and Rentals

133

Depreciation & Amortization

134

Examples of Eligible Expenses

Depreciation expense on assets – to include only those assets purchased with no portion of federal funding. OMB Circular A-122 Attachment B; Section 11 (Depreciation and use allowances); Subpart C provides that the calculation of depreciation will exclude: (1) Any portion of the cost of buildings and equipment borne by or donated by the Federal Government irrespective of where title was originally vested or where it presently resides. (2) Any portion of the cost of buildings and equipment contributed by or for the non-profit organization in satisfaction of a statutory matching requirement.

; Subpart C provides that the calculation of depreciation will exclude: (1) Any portion of the cost of buildings and equipment borne by or donated by the Federal Government irrespective of where title was originally vested or where it presently resides. (2) Any portion of the cost of buildings and equipment contributed by or for the non-profit organization in satisfaction of a statutory matching requirement.")

135

Examples of Eligible Expenses

Depreciation expense on assets – to include only those assets purchased with no portion of federal funding. OMB Circular A-87 (2 CFR 225) Attachment B; Section 11 (Depreciation and use allowances); Subpart C provides that the calculation of depreciation will exclude: (1) Any portion of the cost of buildings and equipment borne by or donated by the Federal Government irrespective of where title was originally vested or where it presently resides; and (2) Any portion of the cost of buildings and equipment contributed by or for the governmental unit, or a related donor organization, in satisfaction of a matching requirement.

Attachment B; Section 11 (Depreciation and use allowances); Subpart C provides that the calculation of depreciation will exclude: (1) Any portion of the cost of buildings and equipment borne by or donated by the Federal Government irrespective of where title was originally vested or where it presently resides; and. (2) Any portion of the cost of buildings and equipment contributed by or for the governmental unit, or a related donor organization, in satisfaction of a matching requirement.")

136

ODOT Invoice Snapshot – Other Costs

137

Other Costs Costs that do not fit into any other category.

Allocated Indirect costs (CAP) As directed by ODOT Office of Transit

As directed by ODOT Office of Transit.")

138

A good Example of supporting Expense detail from a Transit

140

From ODOT Invoice: From Transit GL/Financials: Need to apply $25 credit to expense.

141

Example of Invoice Detail

$58,002 Example of Transit GL Detail $13,614

142

Expenses must be net of all applicable credits

143

General Principles for determining Allowable Costs per A-87

Entity is responsible for efficient and effective administration of Federal awards through the application of sound management practices. Employing whatever management techniques may be necessary for proper and efficient administration of awards. Complying with terms and conditions of Federal Awards Purchases less applicable credits

144

Applicable Credits per A-87

“to the extent that such credits accruing to or received by the governmental unit relate to allowable costs, they shall be credited to the Federal Award either as a cost reduction….”

145

Expense Offset Accident claims Warranty Reimbursements - Vehicles

Vendor invoice to repair vehicle Insurance reimbursement paid to transit for repairs Warranty Reimbursements - Vehicles Warranty Rebate for service completed Sales Tax credit Rebates Purchase printer that has a rebate offer Fuel Tax Rebate Processed quarterly The offset reduces the actual expense incurred by the transit ODOT invoice must reflect the credit.

146

Insurance reimbursements

147

What is cost to be billed on ODOT invoice?

Insurance Payments A vehicle incurs $10,000 damage in an accident. Insurance Company Reimburses $10,000 for vehicle damage. Local body shop completes repairs to vehicle at a cost of $9,000. Transit completes additional repairs to vehicle at a cost of $1,000. What is cost to be billed on ODOT invoice?

148

Insurance Payments What is cost to be billed on ODOT invoice? Costs would be included on ODOT invoice, but there is no expense - nets to zero. Salaries/Wages Expense $1,000 Contract Maintenance Expense $9,000 Recoveries of PD $10,000 Show transaction – need transparency to the event

149

Fuel tax rebates

150

Who is eligible for rebate?

XT Excise Tax Division Information Release - Revised Definition of Transit Buses – February 12, 2004 The transit bus must be operated for public transit or para-transit service on a regular and continuing basis within the state by or for a county, a municipal corporation, a county transit board, or a regional transit authority or commission. DOES NOT include shared-ride taxi service, carpools, vanpools, jitney service, school bus transportation, or charter or sightseeing services. DOES NOT include vehicles used for service/maintenance or general administration. EVERY RURAL TRANSIT IS ELIGIBLE

151

Fuel Tax Rebate Requirements

Claim must be filed within 365 days from the date of fuel purchase. Must report gallons, rather than dollars. Documentation - must keep separate reporting for fuel usage.

152

What is the state motor fuel tax rate?

July 1993 through June 2003 $0.22 July 2003 through June 2004 $0.24 July 2004 through June 2005 $0.26 Beginning July 1, 2005 $0.28

153

Minimum Rebate Requirement

No refund shall be authorized under Ohio Revised Code Section for any single refund claim for less than 100 gallons. All motor fuel listed must be rounded to the nearest whole gallon.

154

Purchase Documentation

Submitted to the Ohio Department of Taxation Evidence of fuel purchases fuel invoices cash receipts credit card receipts or any other document Document must contain the name and address of the seller name of the purchaser date of purchase type of fuel, the number of gallons purchased the purchase price

155

Fuel Usage Documentation

Fuel available (inventory) Fuel sold to others Consumed in vehicles other than qualified transit buses (i.e., Service Vehicles & General Administration) Consumed in a non-qualifying manner Consumed off the highway Consumed in qualified transit Buses

Fuel sold to others. Consumed in vehicles other than qualified transit buses (i.e., Service Vehicles & General Administration) Consumed in a non-qualifying manner. Consumed off the highway. Consumed in qualified transit Buses.")

156

Invoice Requirements ODOT

Fuel expense to line item – Fuel & Lube Record fuel tax credit as a negative amount on line – Fuel & Lube taxes (only for operations) Quarterly operating invoice TAXATION Minimum of 100 gallons Can file monthly (if meet minimum consumption) Must file claim within 365 days of fuel purchase

Quarterly operating invoice. TAXATION. Minimum of 100 gallons. Can file monthly (if meet minimum consumption) Must file claim within 365 days. of fuel purchase.")

157

What is billed on the ODOT invoice?

Fuel Tax Rebates Fuel Cost - $50,000 Tax Rebate $8,000 What is billed on the ODOT invoice?

158

What is cost to be billed on ODOT invoice?

Fuel Tax Rebates Fuel Cost - $50,000 Tax Rebate $8,000 What is cost to be billed on ODOT invoice? Fuel cost of $50,000 recorded on quarterly invoice line Fuel & Lubricants for the appropriate column only. Rebate of $8,000 recorded as a credit (negative amount) on quarterly invoice line – Fuel/Lube taxes only available for the Operations column.

on quarterly invoice. line – Fuel/Lube taxes. only available for the Operations column.")

159

Motor Fuel Tax Rebate - Effective

Must begin 3rd quarter of State Fiscal Year (January - March 2012) Must keep documentation necessary to support rebate requirements All Transits must include the rebate as a credit (negative amount) to line item fuel/lube tax Note: The Transit’s failure to seek the rebate does not negate the requirement to recognize the credit to the fuel taxes.

Must keep documentation necessary to support rebate requirements. All Transits must include the rebate as a credit (negative amount) to line item fuel/lube tax. Note: The Transit’s failure to seek the rebate does not negate the requirement to recognize the credit to the fuel taxes.")

160

Implementation Determine if the transit is actually incurring and paying the state taxes. If not incurring the tax, no additional reporting requirements. Retain documentation to support tax position.

161

Sales tax

162

Sales Tax Credits Many Transits are exempt from sales tax.

If exempt, the transit must report expenses net of the sales tax, even if not taken.

163

Sales Tax Credits - Example

Mechanic makes a purchase at the local auto parts store and charges it to the transit account. The sales receipt provided to the mechanic erroneously includes sales taxes. The Transit A/P employee identifies the error and contacts the auto parts store and has the sales tax removed. Transit processes payment of the invoice less the sales tax.

164

Sales Tax Credits - Example

What happens if the A/P employee does not identify the error and pays the sales tax? What is the effect on ODOT quarterly operating invoice? Tax amount is recorded in the non-eligible column on the ODOT invoice.

166

Cost allocation plan (CAP) Overhead rates

IT Support Storage CEO Office Space Utilities

167

Cost Allocation Plans Indirect Costs - defined

“Incurred for a common or joint purpose benefiting more than one cost objective, and not readily assignable to the cost objectives specifically benefitted, without disproportionate to the results achieved.” Note: Assigned based on use/consumption – not ability of a division, area, or program’s ability to pay.

168

Cost Allocation Plans Indirect Costs - Examples

Building occupancy costs rent, utilities, telephone Computer/IT data processing, data storage, software maintenance Payroll paychecks processed Accounting A/R, A/P, financial & budgeting Centralized Services

169

Cost Allocation Plans Formal process to allocate indirect costs to all departments, divisions, or offices. Prepared annually (same basis as financials) Two approved methods Simplified - Each agency’s departments benefit from indirect costs to approximately the same degree. Multiple-rate – Agency’s indirect costs benefit its major functions (departments) in varying degrees. Multiple- rate: when more definitive costing and should be used when operating differences between divisions or bureaus result in material differences in the use of resources and in costs.

Two approved methods. Simplified - Each agency’s departments benefit from indirect costs to approximately the same degree. Multiple-rate – Agency’s indirect costs benefit its major functions (departments) in varying degrees. Multiple- rate: when more definitive costing and should be used when operating differences between divisions or bureaus result in material differences in the use of resources and in costs.")

170

Steps Involved in Calculating a Rate Under the Simplified Method

Cost Allocation Plans Steps Involved in Calculating a Rate Under the Simplified Method 1. Adjust indirect costs for the period by eliminating any costs directly reimbursed through a Federal award awarded specifically for that purpose. remove administrative salaries included in the pool that were funded as direct in a grant. Remove unallowable costs and capital expenditures. 2. Adjust direct costs by eliminating flow-through funds and capital expenditures. Compute and add use allowances. 3. Divide the total allowable indirect costs (net of applicable credits) by an equitable direct cost base (e.g. salaries and wages or modified total direct costs).

by an equitable direct cost base (e.g. salaries and wages or modified total direct costs).")

171

Steps Involved in Calculating a Rate Under the Multiple Rate Method

Cost Allocation Plans Steps Involved in Calculating a Rate Under the Multiple Rate Method 1. Classify departmental indirect costs into functional cost groupings (cost pools) which benefit divisions of the agency in significantly different proportions. 2. Select appropriate basis for distribution of each classified pool of indirect costs. 3. Distribute each classified pool to the benefitting division. 4. Calculate an indirect cost rate for each division of the agency by relating the total indirect costs allocated to that division to that unit’s direct cost base. Rates must be calculated annually

which benefit divisions of the agency in significantly different proportions. 2. Select appropriate basis for distribution of each classified pool of indirect costs. 3. Distribute each classified pool to the benefitting division. 4. Calculate an indirect cost rate for each division of the agency by relating the total indirect costs allocated to that division to that unit’s direct cost base. Rates must be calculated annually.")

173

Cost Allocation Plans Agency certification required

Based upon auditable historical costs Must demonstrate that all unallowable costs have been excluded Supported by formal accounting and other records Required annually, within six months of fiscal year

174

CAP Support Must be accompanied by An organization chart

A copy of the Comprehensive Annual Financial Report (CAFR) Brief description of the service – who provides who receives Items of expense include in the cost of the service The method used to distribute the cost of the service to benefitted agencies Time-tracking source documents

Brief description of the service – who provides. who receives. Items of expense include in the cost of the service. The method used to distribute the cost of the service to benefitted agencies. Time-tracking source documents.")

175

CAP Guidance ASMB C-10 Cost Principles and Procedures for developing cost allocation plans and indirect cost rates for agreements with the Federal government Implementation guide for Circular A-87 Developed by US Department of Health and Human Services As of April 8, 1997

177

Common Audit Findings

178

Common Audit Findings Double dipping – claiming the same cost on both the operating and capital invoices. Depreciation on Federal funded assets. Misclassified Revenue Lack of supporting documentation. Math errors Incomplete or inaccurate fixed asset inventory listing. Unallowable expenses Lack of support for cost allocations or charge rates. Inaccurate, out-dated or unapproved cost-allocation plans

179

Common Audit Findings Farebox issues abound Segregation of duties

Internal controls Safeguarding/security of cash, tokens Tokens – Inventory, record keeping Outstanding tokens – what is the liability Chain of custody Matching payments to manifest

180

Common Audit Findings Unallowable/Ineligible costs – Report in ineligible column Executive Director costs Late fees Penalties on credit cards (over limit) Credits due but not taken Bad debt expense Contracts – (Please work with the Office of Transit to address) Not charging fully allocated costs Not charging actual trips/mileage to contracts Lack of succession planning – training, manuals, policies and procedures Lack of documentation – current financial policies and procedures Others have policies and procedures, but are not following them.

Credits due but not taken. Bad debt expense. Contracts – (Please work with the Office of Transit to address) Not charging fully allocated costs. Not charging actual trips/mileage to contracts. Lack of succession planning – training, manuals, policies and procedures. Lack of documentation – current financial policies and procedures. Others have policies and procedures, but are not following them.")

181

Common Audit Findings Charge rates for mechanics labor/central garage must be supported/documented based upon actual incurred costs. Must be able to provide evidence for time-tracking of resources. Operate on break-even basis, no profit motive when charged to Federal Programs cannot mark-up labor cannot mark-up parts Entity must have a reliable work order system capable of tracking labor, materials and supplies for each vehicle.

183

Contact Information Stephanie Wagenschein (614) Jana Cassidy (614)

")

Similar presentations

>")