Download presentation

Presentation is loading. Please wait.

1

Chapter 9: Factor pricing models

2

Contents Introduction CAPM ICAPM Comments on the CAPM and ICAPM APT

APT vs. ICAPM

3

Brief introduction

4

Brief introduction More directly, the essence of asset pricing is that there are special states of the world in which investors are especially concerned that their portfolios not do badly. The factors are variables that indicate that these “bad states” have occurred. Any variable that forecasts asset returns (“changes in the investment opportunity set”) or macroeconomic variables is a candidate factor. Such as :term premium, dividend/price ratio, stock returns

or macroeconomic variables is a candidate factor. Such as :term premium, dividend/price ratio, stock returns.")

5

Should factors be unpredictable over time?

Factors that proxy for marginal utility growth, though they don’t have to be totally unpredictable, should not be highly predictable. If one chooses highly predictable factors, the model will counterfactually predict large interest rate variation. In practice, this consideration means that one should choose the right units: Use GNP growth rather than level, portfolio returns rather than prices or price/dividend ratios, etc.

6

The derivations of factor pricing model

Determine one particular list of factors that can proxy for marginal utility growth Prove that the relation should be linear. Remark: all factor models are derived as specializations of the consumption-based model.

7

guard against fishing One should call for better theories or derivations, more carefully aimed at limiting the list of potential factors and describing the fundamental macroeconomic sources of risk, and thus providing more discipline for empirical work.

8

Capital Asset Pricing Model (CAPM)

wealth portfolio return. In expected return / beta language, CAPM can be derived from consumption-based model by different assumption.

9

Different assumption 1) two-period quadratic utility

2) exponential utility and normal returns, 3) Infinite horizon, quadratic utility and i.i.d. returns 4) Log utility. Same assumption: no labor income

exponential utility and normal returns, 3) Infinite horizon, quadratic utility and i.i.d. returns. 4) Log utility. Same assumption: no labor income.")

10

Two-period quadratic utility,no labor income

Investors have quadratic preferences and only live two periods, marginal rate of substitution is thus

11

the budget constraint is

12

Just as

13

Exponential utility, normal distributions, no labor income

If consumption only in the last period and is normally distributed, we have a is the coefficient of absolute risk aversion.

14

the budget constraint is

16

Quadratic value function, dynamic programming

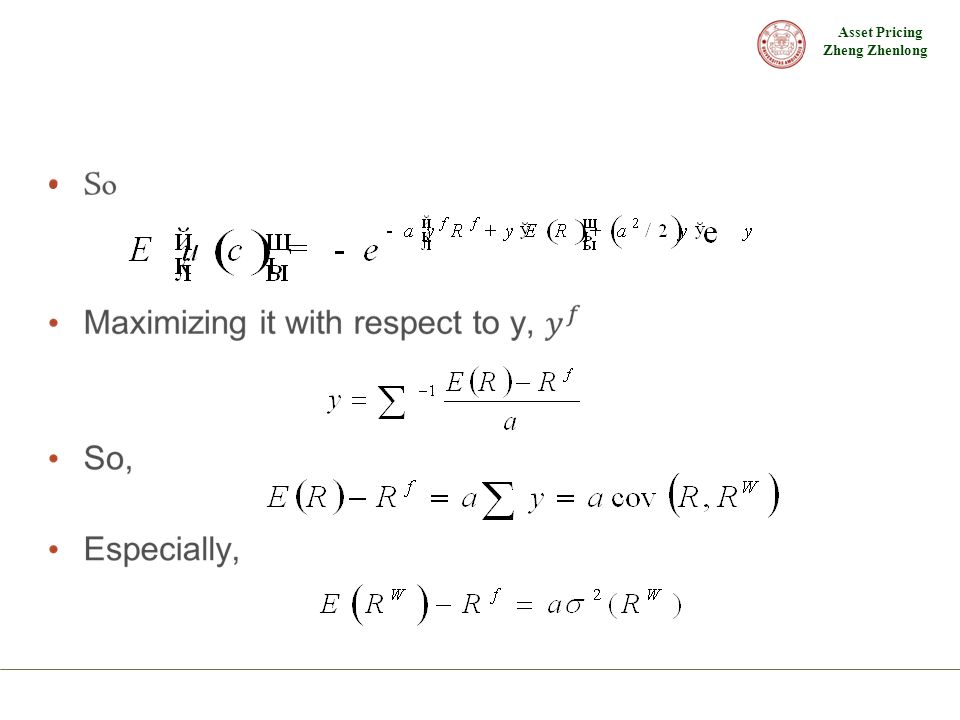

first order condition So,

17

suppose the value function were quadratic,

Then, Some addition assumptions: The value function only depends on wealth. The value function is quadratic. It needs the following assumptions: the interest rate is constant, returns are iid, no labor income.

18

the existence of value function (Proof )

Suppose investors last forever, and have the standard sort of utility function Define the value function as the maximized value of the utility function in this environment.

19

Value functions allow you to express an infinite period problem as a two period problem

20

Why is the value function quadratic?

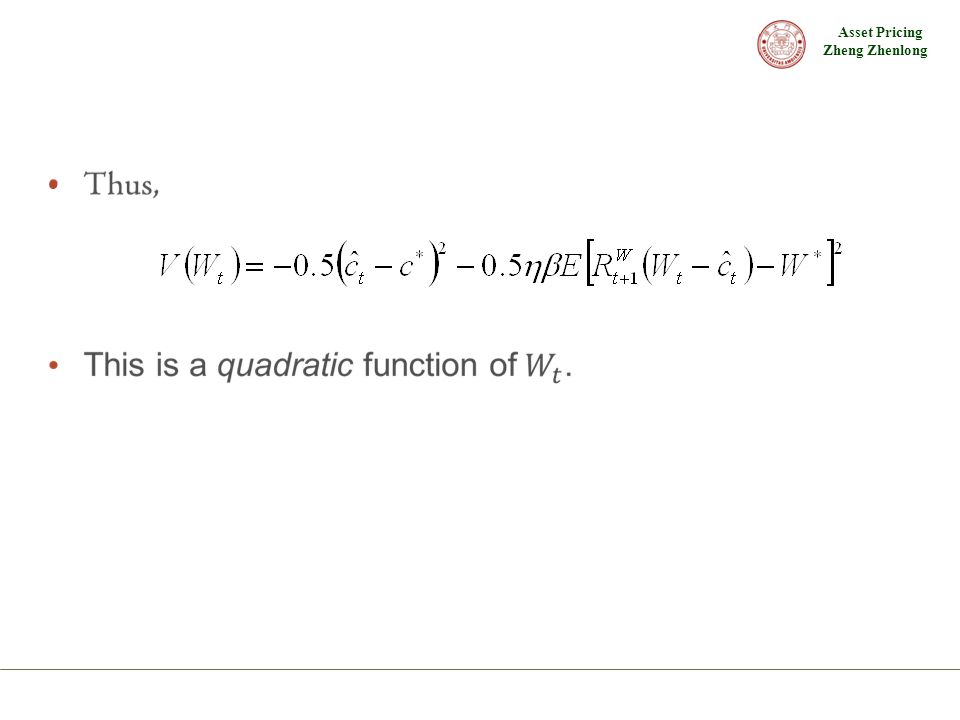

Remark: quadratic utility function leads to a quadratic value function in this environment Specify: Guess: Thus,

23

Log utility, no labor income

24

Log utility has a special property that “income effects offset substitution effects,” or in an asset pricing context that “discount rate effects offset cash flow effects.”

25

How to linearize the model?

The twin goals of a linear factor model derivation are to derive what variables derive the discount factor, and to derive a linear relation between the discount factor and these variables. This section covers three tricks that are used to obtain a linear functional form. Taylor approximation the continuous time limit normal distribution

26

Taylor approximation The most obvious way to linearize the model is by a Taylor approximation

27

Continuous time limit If the discrete time is short enough, we can apply the continuous time result as an approximation For a short discrete time interval,

28

Normal distribution in discrete time

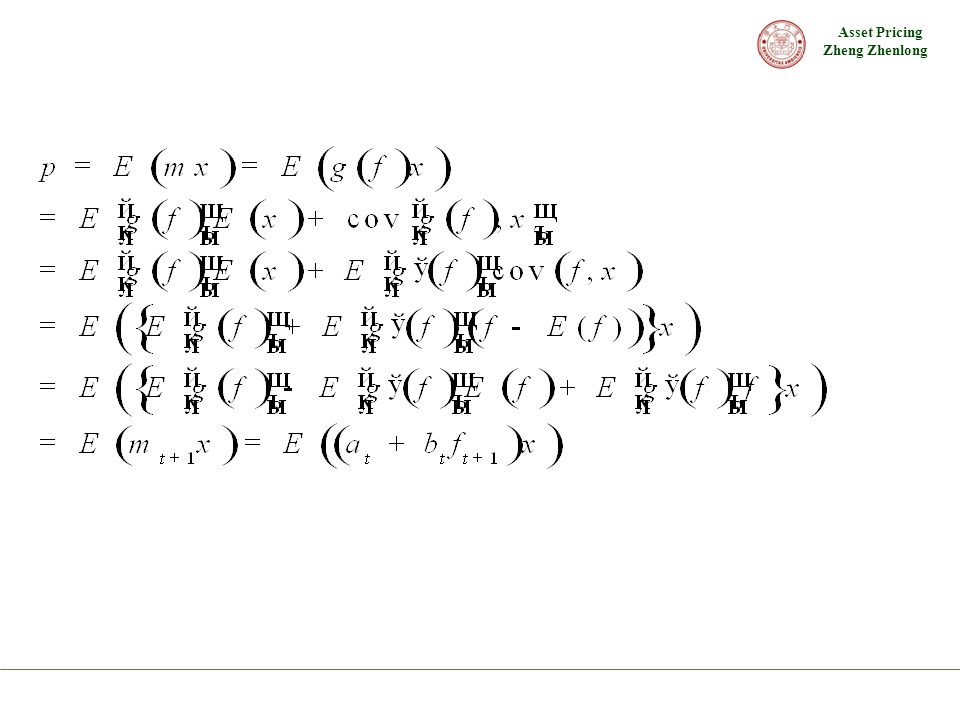

Stein’s lemma : If f and R are bivariate normal, g(f) is differentiable and ,then

is differentiable and ,then.")

29

Remark: If m=g(f), if f and a set of the payoffs priced by m are normally distributed returns, and if , then there is a linear model m=a+bf that prices the normally distributed returns.

, if f and a set of the payoffs priced by m are normally distributed returns, and if , then there is a linear model m=a+bf that prices the normally distributed returns.")

31

Similar,it allows us to derive an expected return-beta model using the factors

32

Two period CAPM Stein’s lemma allows us to substitute a normal distribution assumption for the quadratic assumption in the two period CAPM. Assuming RWand Ri are normally distributed, we have:

33

Log utility CAPM Stein’s lemma cannot be applied to the log utility CAPM because the market return cannot be normally distributed. For log utility CAPM, g(f)=1/RW, so If RW is normally distributed, E(1/RW2) does not exist. The Stein’s lemma condition is violated.

=1/RW, so. If RW is normally distributed, E(1/RW2) does not exist. The Stein’s lemma condition is violated.")

34

Intertemporal Capital Asset Pricing Model (ICAPM)

The ICAPM generates linear discount factor models in which the factors are “state variables” for the investor’s consumption-portfolio decision.

35

the value function depends on the state variables

so we can write

36

Start from We have

37

Define the coefficient of relative risk aversion,

Then we obtain the ICAPM,

38

Thus, in discrete time

39

9.3 Comments on the CAPM and ICAPM

40

Is the CAPM conditional or unconditional?

42

The log utility CAPM expressed with the inverse market return is a beautiful model, since it holds both conditionally and unconditionally. There are no free parameters that can change with conditioning information. Finally it requires no specification of the investment opportunity set, or no specification of technology. However, the expectations in the linearized log utility CAPM are conditional.

43

Should the CAPM price options?

the quadratic utility CAPM and the nonlinear log utility CAPM should apply to all payoffs: stocks, bonds, options, contingent claims, etc. However, if we assume normal return distributions to obtain a linear CAPM, we can no longer hope to price options, since option returns are non-normally distributed

44

Why bother linearizing a model?

45

What about the wealth portfolio?

To own a (share of) the consumption stream, you have to own not only all stocks,but all bonds, real estate, privately held capital, publicly held capital (roads, parks, etc.), and human capital. Clearly, the CAPM is a poor defense of common proxies such as the value-weighted NYSE portfolio.

the consumption stream, you have to own not only all stocks,but all bonds, real estate, privately held capital, publicly held capital (roads, parks, etc.), and human capital. Clearly, the CAPM is a poor defense of common proxies such as the value-weighted NYSE portfolio.")

46

Implicit consumption-based models

47

The log utility model also allows us for the first time to look at what moves returns ex-post as well as ex-ante. Aggregate consumption and asset returns are likely to be de-linked at high frequencies, but how high (quarterly?) and by what mechanism are important questions to be answered. In sum, the poor performance of the consumption- based model is an important nut to chew on, not just a blind alley or failed attempt that we can safely disregard and go on about our business.

and by what mechanism are important questions to be answered. In sum, the poor performance of the consumption- based model is an important nut to chew on, not just a blind alley or failed attempt that we can safely disregard and go on about our business.")

48

Identity of state variables

The ICAPM does not tell us the identity of the state variables zt , leading Fama (1991) to characterize the ICAPM as a ‘‘fishing license.’’ The ICAPM 并非全无道理。关键是要在选择变量时要遵 守纪律.

to characterize the ICAPM as a ‘‘fishing license.’’ The ICAPM 并非全无道理。关键是要在选择变量时要遵 守纪律.")

49

Portfolio Intuition and Recession State Variables

The covariance (or beta) of 𝑅 𝑖 with 𝑅 𝑊 measures how much a marginal increase in 𝑅 𝑖 affects the portfolio variance. Modern asset pricing starts when we realize that investors care about portfolio returns, not about the behavior of specific assets. That is the central insight in CAPM. The ICAPM adds long investment horizons and time-varying investment opportunities to this picture. People are unhappy when news comes that future returns are lower, they will thus prefer stocks that do well on such news. Most current theorizing and empirical work, while citing the ICAPM, really considers another source of additional risk factors: Investors have jobs. Or they own houses and shares of small businesses. People with jobs will prefer stocks that don’t fall in recessions.

of 𝑅 𝑖 with 𝑅 𝑊 measures how much a marginal increase in 𝑅 𝑖 affects the portfolio variance. Modern asset pricing starts when we realize that investors care about portfolio returns, not about the behavior of specific assets. That is the central insight in CAPM. The ICAPM adds long investment horizons and time-varying investment opportunities to this picture. People are unhappy when news comes that future returns are lower, they will thus prefer stocks that do well on such news. Most current theorizing and empirical work, while citing the ICAPM, really considers another source of additional risk factors: Investors have jobs. Or they own houses and shares of small businesses. People with jobs will prefer stocks that don’t fall in recessions.")

50

Arbitrage Pricing Theory (APT)

The intuition behind the APT is that the completely idiosyncratic movements in asset returns should not carry any risk prices, since investors can diversify them away by holding portfolios. Therefore, risk prices or expected returns on a security should be related to the security’s covariance with the common components or “factors” only.

51

The APT models the tendency of asset payoffs (returns) to move together via a statistical factor decomposition Define So,

53

Thus, with N= number of securities, the N(N-1)/2 elements of a variance-covariance matrix are described by N betas, and N+1 variances. With multiple (orthogonalized) factors, we obtain

factors, we obtain.")

54

If we know the factors we want to use ahead of time, we can estimate a factor structure by running regressions. If we don’t, we use factor analysis to estimate the factor model.

55

Exact factor pricing

56

Approximate APT using the law of one price

There is some idiosyncratic or residual risk; we cannot exactly replicate the return of a given stock with a portfolio of a few large factor portfolios. However, the idiosyncratic risks are often small. There is reason to hope that the APT holds approximately, especially for reasonably large portfolios.

57

Suppose Again take prices of both sides,

59

Limiting arguments

60

These two theorems can be interpreted to say that the APT holds approximately (in the usual limiting sense) for either portfolios that naturally have high R2, or well-diversified portfolios in large enough markets.

for either portfolios that naturally have high R2, or well-diversified portfolios in large enough markets.")

61

Law of one price arguments fail

62

Remark: the effort to extend prices from an original set of securities (f in this case) to new payoffs that are not exactly spanned by the original set of securities, using only the law of one price, is fundamentally doomed. To extend a pricing function, you need to add some restrictions beyond the law of one price.

63

the law of one price: arbitrage and Sharpe ratios

The approximate APT based on the law of one price fell apart because we could always choose a discount factor sufficiently “far out” to generate an arbitrarily large price for an arbitrarily small residual. But those discount factors are surely “unreasonable.” Surely, we can rule them out.

65

Theorem

66

APT vs. ICAPM In the ICAPM there is no presumption that factors f in a pricing model 𝑚= 𝑏 ′ 𝑓 describe the covariance matrix of returns. The factors do not have to be orthogonal or i.i.d. either. High 𝑅 2 in time-series regressions of the returns on the factors may imply factor pricing (APT), but again are not necessary (ICAPM). Factors such as industry may describe large parts of returns’ variances but not contribute to the explanation of average returns. The biggest difference between APT and ICAPM for empirical work is in the inspiration for factors. The APT suggests that one start with a statistical analysis of the covariance matrix of returns and find portfolios that characterize common movement. The ICAPM suggests that one start by thinking about state variables that describe the conditional distribution of future asset returns.

, but again are not necessary (ICAPM). Factors such as industry may describe large parts of returns’ variances but not contribute to the explanation of average returns. The biggest difference between APT and ICAPM for empirical work is in the inspiration for factors. The APT suggests that one start with a statistical analysis of the covariance matrix of returns and find portfolios that characterize common movement. The ICAPM suggests that one start by thinking about state variables that describe the conditional distribution of future asset returns.")

Similar presentations

Single-Factor APT Model Multi-Factor APT Models Arbitrage Opportunities Disequilibrium in APT Is APT.>")

have on asset demands and asset prices?>")

: Finish Sharpe’s Chapter 4. Highly relevant for Hand-In #2, which has now posted. Fri Apr 24 (8-(if need be)12): Sharpe’s.>")