Download presentation

Presentation is loading. Please wait.

1

Convergence of Government Bond Yields in the Euro Zone: The Role of Policy Harmonization Denise Côté and Christopher Graham International Department 28 April 2006

2

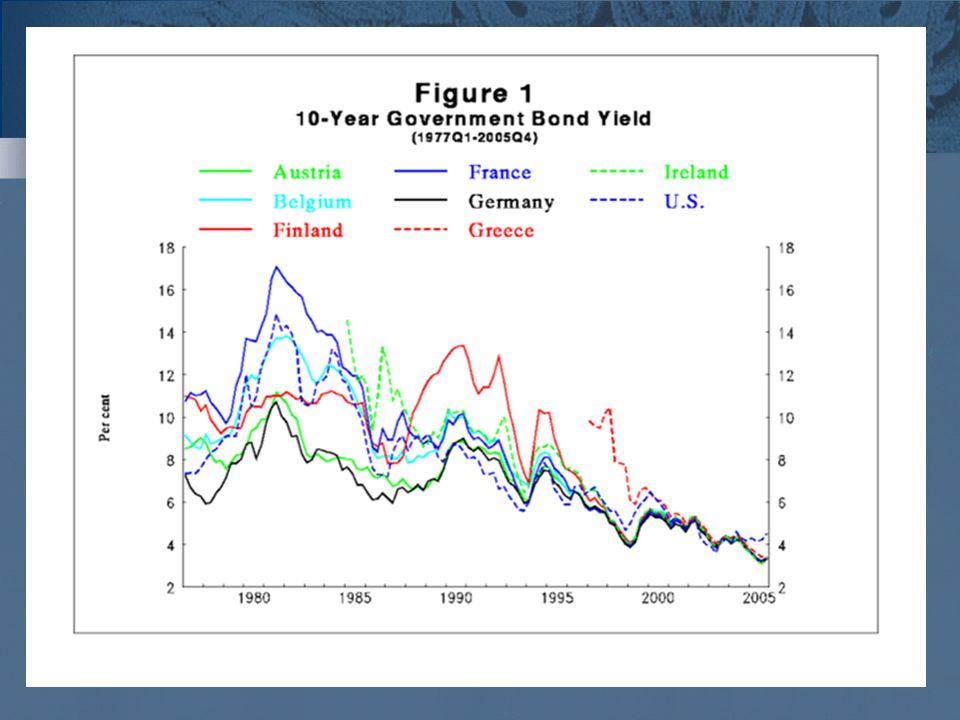

Motivation By the time the euro was introduced in January 1999, bond yields across the euro zone countries had largely converged to that of Germany (the euro zone's largest economy) Since the early 1980s, long-term government bond yields in the euro zone have declined, in line with those in other industrialized countries

Since the early 1980s, long-term government bond yields in the euro zone have declined, in line with those in other industrialized countries")

8

Motivation Why does convergence of national yields to a stable level with reduced risk matter? Reduces various risks => less uncertainty regarding the value of funds over time Contributes to financial stability Stimulates investment and output within converging countries Cheaper access to debt financing

9

Motivation What factors can drive convergence of long-term bond yields to a stable level with reduced risk and maintain it over the long term? One explanation, by the ECB: –Convergence driven by anticipation of the introduction of the euro and corresponding elimination of exchange rate risk (ECB Monthly Bulletin November 2003)

.")

10

Motivation Our goal: To examine how monetary and fiscal policies adopted on the path to EMU, including the introduction of the euro, contributed to the convergence of national long-term government bond yields in the euro zone

11

Outline 1. Institutional Background 5. Policy Implications 3. Empirical Analysis Panel analysis Currency risk 2. Our Approach 4. Conclusions

12

Institutional Background Maastricht Convergence Criteria (1993): 1) General government deficit to GDP ≤ 3% 2) Gross general government debt to GDP ≤ 60% 3) Inflation ≤ 1.5 ppt above average of 3 best performing countries in terms of price stability 4) Long-term interest rate ≤ 2 ppt above average of 3 best performing countries in terms of price stability 5) Exchange Rate Mechanism respected for at least 2 years prior to adoption of euro (±15%)

: 1) General government deficit to GDP ≤ 3% 2) Gross general government debt to GDP ≤ 60% 3) Inflation ≤ 1.5 ppt above average of 3 best performing countries in terms of price stability 4) Long-term interest rate ≤ 2 ppt above average of 3 best performing countries in terms of price stability 5) Exchange Rate Mechanism respected for at least 2 years prior to adoption of euro (±15%)")

13

Our Approach Assess convergence of long-term government bond yields resulting from: Increased harmonization of monetary and fiscal policies on the road to EMU The introduction of the common currency itself

14

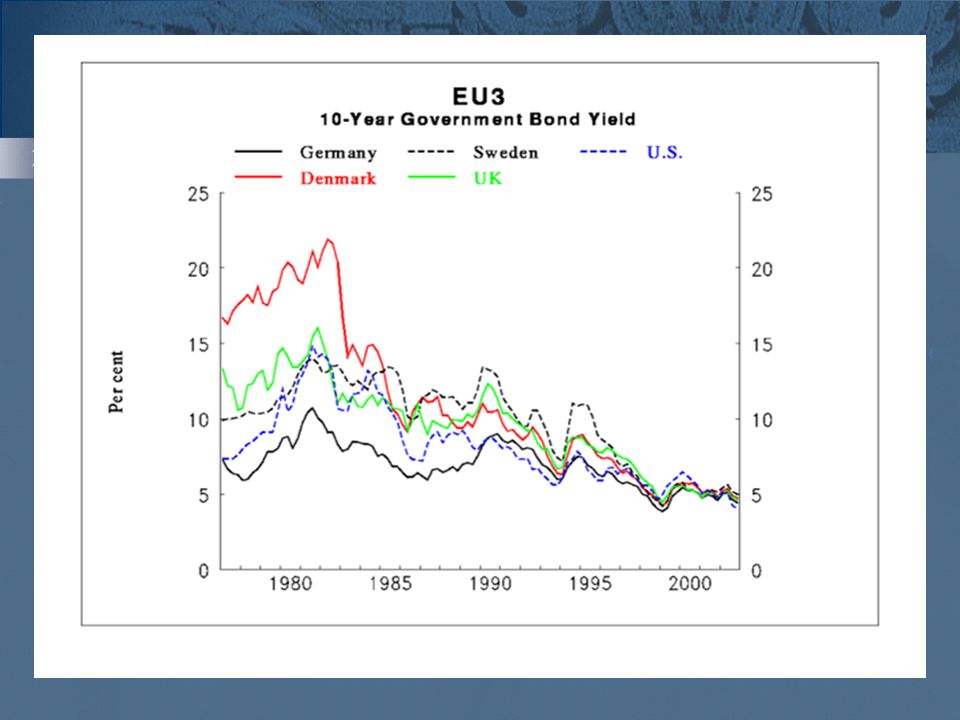

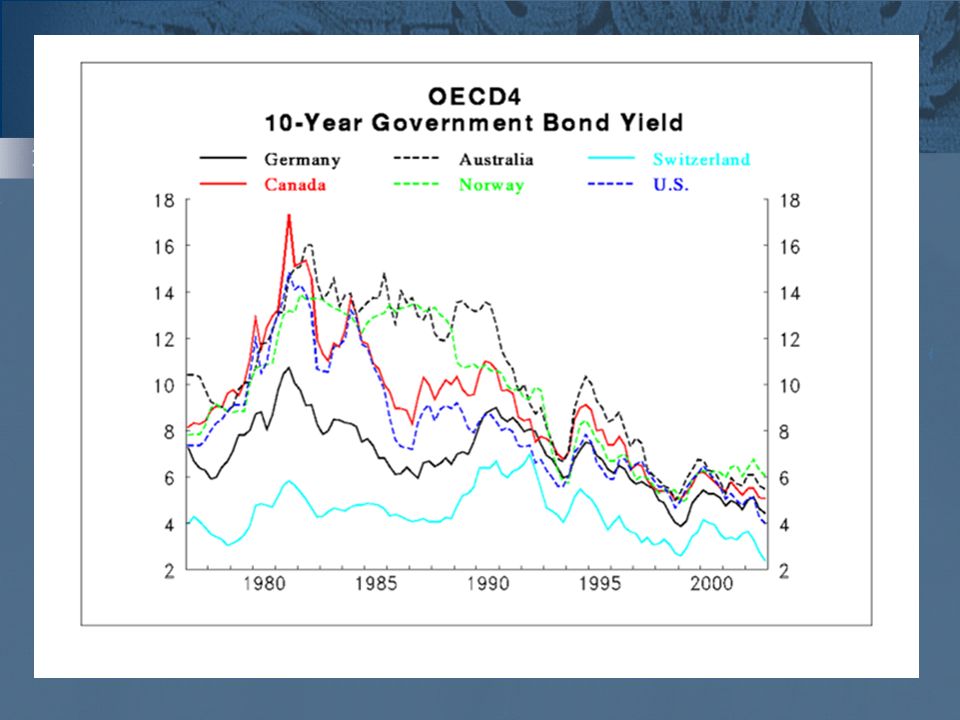

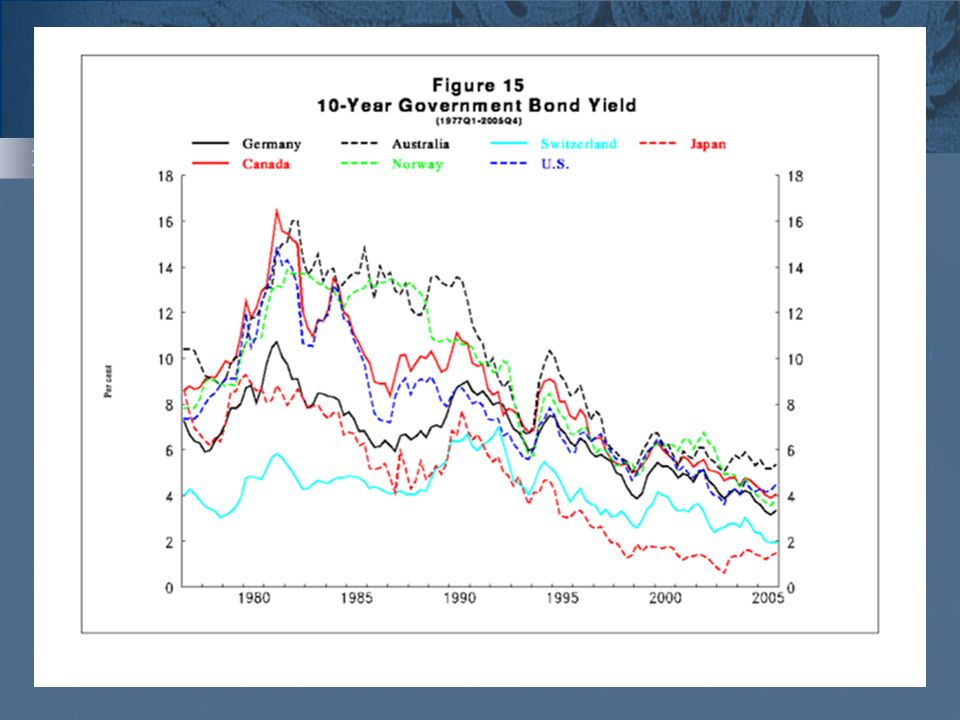

Analytical Approach Empirical Analysis: Cointegration and panel estimation techniques applied over 1980Q1 - 2002Q4 Estimate 10-year government bond yields using a set of long-term determinants: expected inflation, government balance, government debt and world interest rate Apply to a pool of nine EMU countries Compare to 2 control-groups: EU3 (UK, Denmark and Sweden) and OECD4 (Australia, Canada, Norway and Switzerland)

and OECD4 (Australia, Canada, Norway and Switzerland)")

15

Euro zone Estimates Parameter German Yield as World Yield US Yield As World Yield Expected Inflation 0.83 Fiscal Balance (% of GDP) -0.18-0.17 World Interest Rate 0.720.23 Adjustment Speed (ECM) -0.080 (6.09) -0.060 (5.00) All estimated parameters are of the expected sign, except the debt-to-GDP ratio Parameter on world interest rate three times larger when real German yield is used (Knot & de Haan [1995]) Speed of convergence to long- run equilibrium is faster when using the German yield Fiscal balance parameter consistent with Orr, Edey & Kennedy (1995), Brook (2003)

![Euro zone Estimates Parameter German Yield as World Yield US Yield As World Yield Expected Inflation 0.83 Fiscal Balance (% of GDP) World Interest Rate Adjustment Speed (ECM) (6.09) (5.00) All estimated parameters are of the expected sign, except the debt-to-GDP ratio Parameter on world interest rate three times larger when real German yield is used (Knot & de Haan [1995]) Speed of convergence to long- run equilibrium is faster when using the German yield Fiscal balance parameter consistent with Orr, Edey & Kennedy (1995), Brook (2003)](http://images.slideplayer.com/31/9673088/slides/slide_15.jpg "Euro zone Estimates Parameter German Yield as World Yield US Yield As World Yield Expected Inflation 0.83 Fiscal Balance (% of GDP) World Interest Rate Adjustment Speed (ECM) (6.09) (5.00) All estimated parameters are of the expected sign, except the debt-to-GDP ratio Parameter on world interest rate three times larger when real German yield is used (Knot & de Haan [1995]) Speed of convergence to long- run equilibrium is faster when using the German yield Fiscal balance parameter consistent with Orr, Edey & Kennedy (1995), Brook (2003)")

16

EU3 Estimates Parameter German Yield as World Yield US Yield As World Yield Expected Inflation 0.760.85 Fiscal Balance (% of GDP) -0.23-0.11 Fiscal Debt (% of GDP) 0.050.04 World Interest Rate 0.820.36 Adjustment Speed (ECM) -0.059 (2.82) -0.042 (2.01) Parameters qualitatively the same as for the euro zone Debt ratio is now of expected sign Adjustment slower than for euro zone countries

Fiscal Debt (% of GDP) World Interest Rate Adjustment Speed (ECM) (2.82) (2.01) Parameters qualitatively the same as for the euro zone Debt ratio is now of expected sign Adjustment slower than for euro zone countries")

17

OECD4 Estimates Parameters qualitatively similar to those for euro zone and EU3 Impact of fiscal balance slightly reduced Adjustment slower than for euro zone, but similar to EU3 Parameter German Yield as World Yield US Yield As World Yield Expected Inflation 0.870.91 Fiscal Balance (% of GDP) -0.06-0.05 World Interest Rate 0.490. 33 Adjustment Speed (ECM) -0.048 (3.10) -0.037 (2.48) Debt ratio not significant

(3.10) (2.48) Debt ratio not significant.")

18

Summary of Panel Results Summary of results for euro zone, EU3 and OECD4 In the long-run, 10-year bond yields driven by: Expected inflation Developments in larger country's bond yields To a lesser extent, effects of persistent changes in general government fiscal balances (debt ratio for EU3) Results robust (expected inflation, ECM lags & Y-gap)

Results robust (expected inflation, ECM lags & Y-gap)")

19

Summary of Panel Results Results suggest: Convergence driven by policy harmonization (especially monetary policy) Not confined to members of the common currency or common market

Not confined to members of the common currency or common market")

20

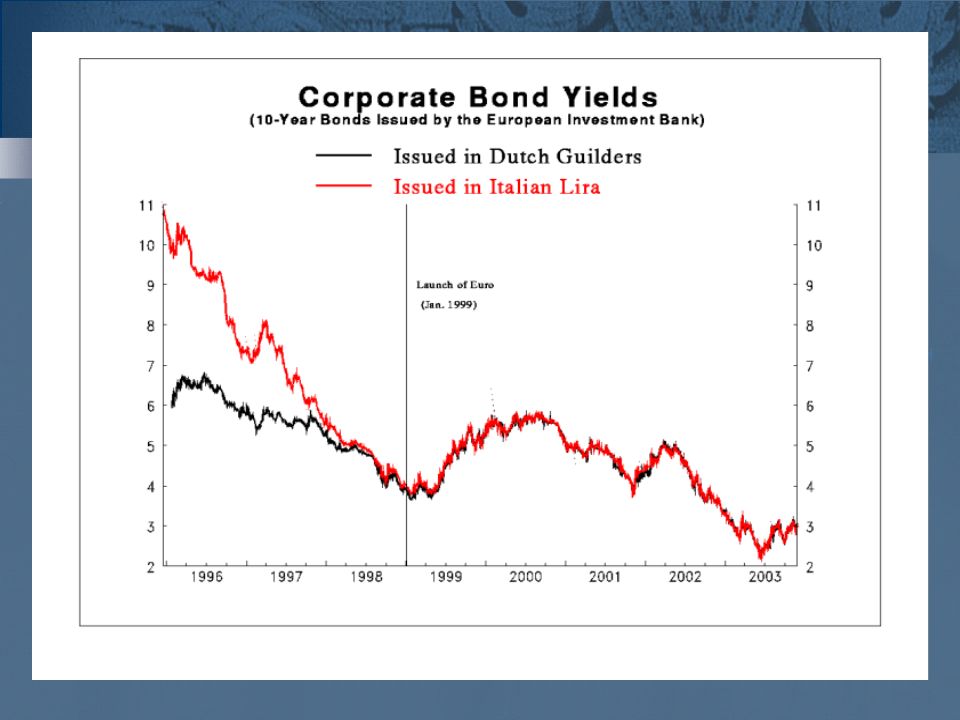

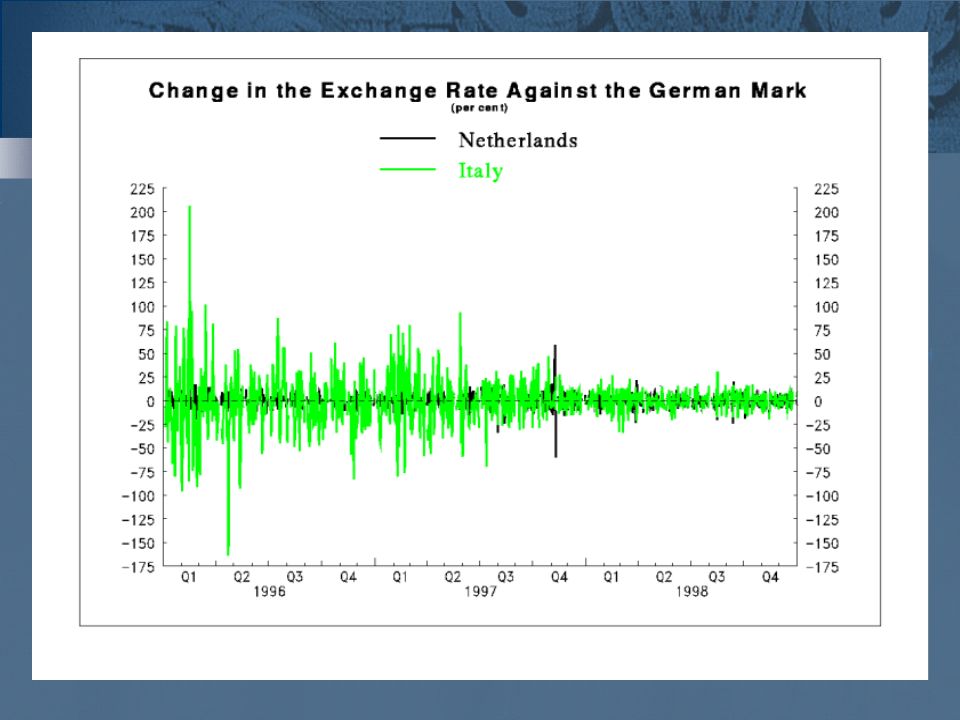

Currency Risk Plot two corporate bonds –Same issuer same default risk –Different countries different currency and liquidity risks Currency risk declined gradually and had essentially disappeared before adoption of euro Liquidity risk remains and is very small

22

Conclusions Harmonization of monetary and fiscal policies greatly contributed to convergence of long-term government bond yields in the euro zone by prompting convergence of their long-run determinants Convergence in the euro zone cannot be attributed primarily to the strict introduction of the euro, since EU3 and OECD4 also experienced a similar convergence

24

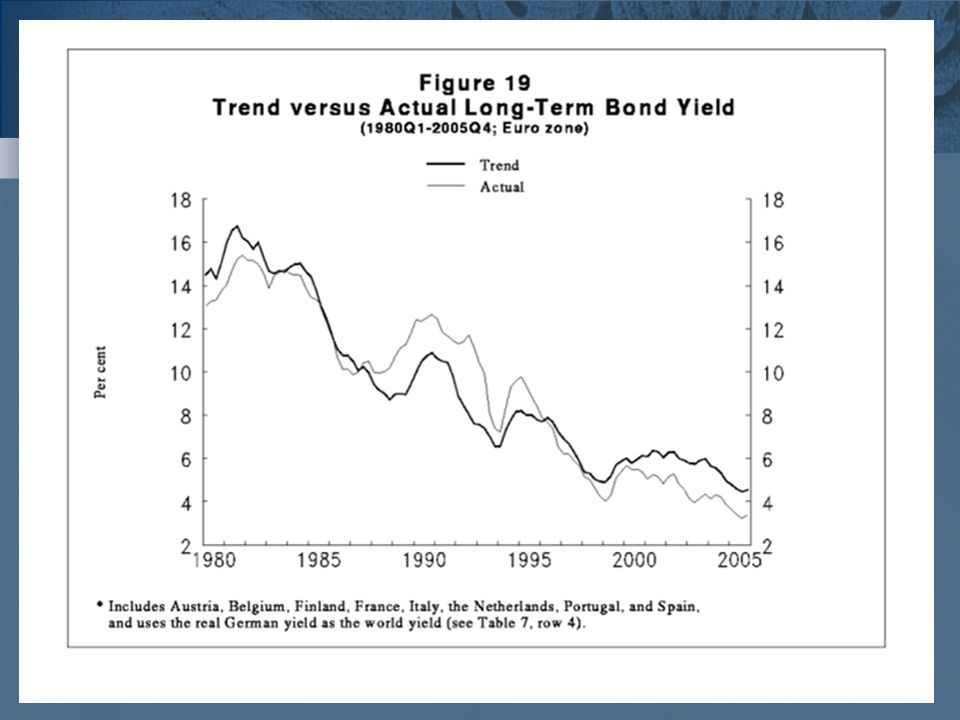

Policy Implications Current average yield is below trend for cyclical reasons Given current policy, trend should remain low Mitigates financial risk Long-term estimates imply decreasing trend for euro zone yields

25

Convergence of Government Bond Yields in the Euro Area: The Role of Policy Harmonization Denise Côté and Christopher Graham International Department 28 April 2006

26

Empirical Analysis General long-run specification, based on theory: RL t = 1 ecpi t + 2 gbal t + 3 gdebt t + 4 rrlw t + t (1) ecpi = expected inflation gbal = General government fiscal balance as % of nominal GDP (“+”=surplus, “-”=deficit) gdebt = Gross general government debt as % of nominal GDP rrlw = U.S. or German 10-year government real bond yield (measure of the world real yield)

.")

27

Estimation of Panel Error Correction Model -0.0804 (6.09).02 +.83ecpi -.18gbal +.72rrlgy (6.49) (64.09) (11.04) (14.08) -0.0811 (6.04).02 +.81ecpi -.21gbal -.01gdebt +.70rrlgy (6.83) (52.73) (10.66) (2.90) (13.74) -0.0596 (5.00).04 +.83ecpi -.17gbal +.23rrlus (23.98) (61.87) (10.02) (7.25) -0.0606 (5.02).04 +.81ecpi -.21gbal -.01gdebt +.23rrlus (18.54) (52.24) (10.26) (3.54) (7.09) 2nd Step: Estimation of Error-Correction Models, Error-Correction Term ( ) First Step: Estimates of Long-Run Relationship Sample: 1980Q1-2002Q4, 9 countries, 819 Observations Euro zone Countries

ecpi -.18gbal +.72rrlgy (6.49) (64.09) (11.04) (14.08) (6.04) ecpi -.21gbal -.01gdebt +.70rrlgy (6.83) (52.73) (10.66) (2.90) (13.74) (5.00) ecpi -.17gbal +.23rrlus (23.98) (61.87) (10.02) (7.25) (5.02) ecpi -.21gbal -.01gdebt +.23rrlus (18.54) (52.24) (10.26) (3.54) (7.09) 2nd Step: Estimation of Error-Correction Models, Error-Correction Term ( ) First Step: Estimates of Long-Run Relationship Sample: 1980Q1-2002Q4, 9 countries, 819 Observations Euro zone Countries")

28

Estimation of Panel Error Correction Model -0.0585 (2.82) -.01 +.76ecpi -.23gbal +.05gdebt +.82rrlgy (1.50) (20.07) (6.32) (4.70) (8.24) -0.0416 (2.01).01 +.85ecpi -.11gbal +.04gdebt +.36rrlus (1.80) (22.16) (3.09) (3.01) (5.80) Error-Correction Term ( ) Estimates of Long-Run Relationship using panel data Sample: 1980Q1-2002Q4, 3 countries, 273 Observations EU3 Countries

ecpi -.23gbal +.05gdebt +.82rrlgy (1.50) (20.07) (6.32) (4.70) (8.24) (2.01) ecpi -.11gbal +.04gdebt +.36rrlus (1.80) (22.16) (3.09) (3.01) (5.80) Error-Correction Term ( ) Estimates of Long-Run Relationship using panel data Sample: 1980Q1-2002Q4, 3 countries, 273 Observations EU3 Countries")

29

Estimation of Panel Error Correction Model -0.0483 (3.10).02 +.87ecpi -.06gbal +.01gdebt +.49rrlgy (4.51) (24.65) (2.72) (1.01) (5.83) -0.0371 (2.48).03 +.91ecpi -.05gbal +.01gdebt +.33rrlus (6.97) (26.18) (1.97) (1.25) (6.34) Error-Correction Term ( ) Estimates of Long-Run Relationship using panel data Sample: 1980Q1-2002Q4, 4 countries, 364 Observations OECD4 Countries

ecpi -.06gbal +.01gdebt +.49rrlgy (4.51) (24.65) (2.72) (1.01) (5.83) (2.48) ecpi -.05gbal +.01gdebt +.33rrlus (6.97) (26.18) (1.97) (1.25) (6.34) Error-Correction Term ( ) Estimates of Long-Run Relationship using panel data Sample: 1980Q1-2002Q4, 4 countries, 364 Observations OECD4 Countries")

Similar presentations

Presentation by Nigel Nagarajan Faculty Orientation for the 2009 Euro Challenge New York, November 25 th 2008 The 2009.>")

Presentation by Nigel Nagarajan Student Orientation – 2009 Euro Challenge Miami-Florida European Union Center of Excellence.>")

Tomislav Ridzak & Mirna Dumicic Financial Stability Department.>")