Download presentation

Presentation is loading. Please wait.

1

1 Engineering Economics

2

Money has a time value because it can earn more money over time (earning power). Money has a time value because its purchasing power changes over time (inflation). Time value of money is measured in terms of market interest rate which reflects both earning and purchasing power in the financial market.

. Time value of money is measured in terms of market interest rate which reflects both earning and purchasing power in the financial market..")

3

Interest is the cost of money—a cost to the borrower and an earning to the lender. Elements of Transactions Involving Interest: Principal Interest rate Interest period Total number of interest periods A plan for receipts or disbursements A future amount of money

4

◦ INVESTMENT INTEREST = VALUE NOW - ORIGINAL AMOUNT ◦ LOAN INTEREST = TOTAL OWED NOW - ORIGINAL AMOUNT 4

5

5 Example You borrowed $10,000 for one full year. Must pay back $10,700 at the end of one year, find the interest amount and the interest rate: Solution Interest Amount (I) = $10,700 - $10,000 Interest Amount = $700 for the year Interest rate (i) = 700/$10,000 = 7%/Yr

= $10,700 - $10,000 Interest Amount = $700 for the year Interest rate (i) = 700/$10,000 = 7%/Yr.")

6

6 Notations I = the interest amount in $ i = the interest rate (%/interest period) N = No. of interest periods (1 for this problem) P = The actual borrowed amount or the principal ($10,000 in this problem)

P = The actual borrowed amount or the principal ($10,000 in this problem).")

7

7 If you borrow $20,000 for 1 year at 9% interest per year calculate the total amount of money that you will pay by the end of that year. Solution P= $20,000 i = 0.09 per year and N = 1 Year Interest Amt (I) = i*P*N =(0.09)($20,000) = $1,800 Total Amt Paid after one year (Future amount of money)= P + I = $21,800 Create an Excel Sheet

= i*P*N =(0.09)($20,000) = $1,800 Total Amt Paid after one year (Future amount of money)= P + I = $21,800 Create an Excel Sheet.")

8

8 On the other hand if you invest $20,000 for one year in a venture that will return to you, 9% per year. At the end of one year, you will have: Original $20,000 back Plus…….. The 9% return on $20,000 = $1,800 We say that you earned 9%/year on the investment! This is your RATE of RETURN on the investment

9

9 Where a country’s currency becomes worth less over time thus requiring more of the currency to purchase the same amount of goods or services in a time period

10

10 Inflation impacts: Purchasing Power (reduces) Operating Costs (increases) Rate of Returns on Investments (reduces)

Operating Costs (increases) Rate of Returns on Investments (reduces)")

11

11 Taxes represent a significant negative cash flow A realistic economic analysis must assess the impact of taxes Called an AFTER-TAX cash flow analysis Not considering taxes is called a BEFORE- TAX Cash Flow analysis

12

Cash Flows ◦ Inflows (Receipts) =====> Revenues or Benefits (+ positive) ◦ Outflows (Disbursements) =====> Costs (- negative) T=0t = 1 Yr Positive + Negative - $20,000 is received here $21,800 paid back here

=====> Revenues or Benefits (+ positive) ◦ Outflows (Disbursements) =====> Costs (- negative) T=0t = 1 Yr Positive + Negative - $20,000 is received here $21,800 paid back here")

13

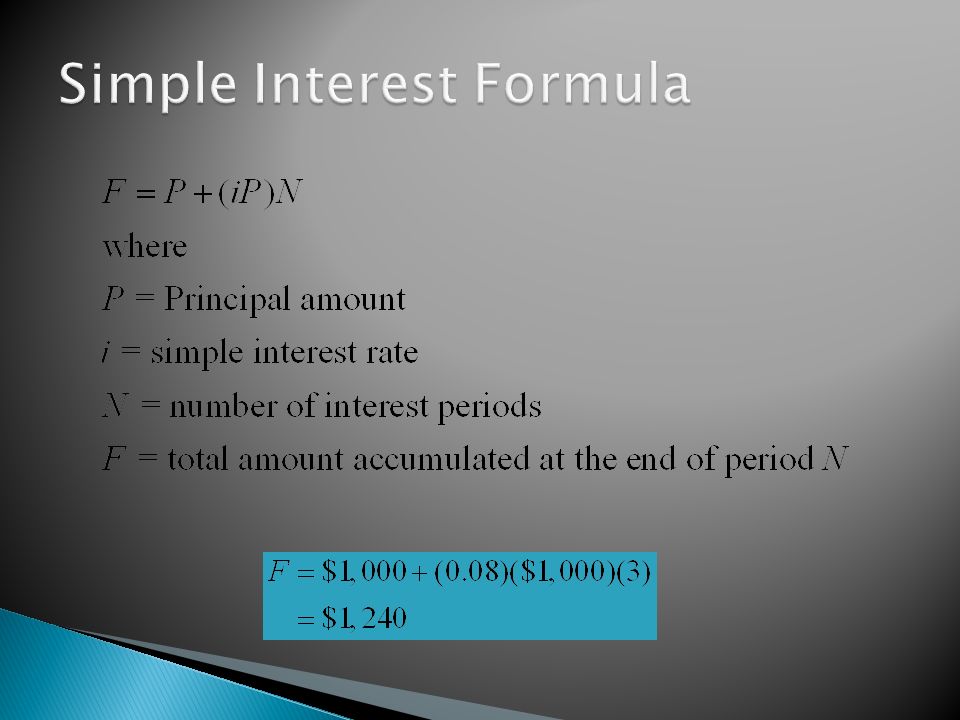

Methods of Calculating Interest Simple interest: the practice of charging an interest rate only to an initial sum (principal amount). Compound interest: the practice of charging an interest rate to an initial sum and to any previously accumulated interest that has not been withdrawn.

14

Simple Interest P = Principal amount i = Interest rate N = Number of interest periods Example: P = $1,000 i = 8% N = 3 years End of Year Beginnin g Balance Interest earned Ending Balance 0$1,000 1 $80$1,080 2 $80$1,160 3 $80$1,240

16

Compound Interest Compound interest: the practice of charging an interest rate to an initial sum and to any previously accumulated interest that has not been withdrawn.

17

Compound Interest P = Principal amount i = Interest rate N = Number of interest periods Example: P = $1,000 i = 8% N = 3 years End of Year Beginning Balance Interest earned Ending Balance 0$1,000 1 $80$1,080 2 $86.40$1,166.40 3 $93.31$1,259.71

18

$1,000 $1,080 $1,166.40 $1,259.71 0 1 2 3

19

n = 0: P n = 1: F 1 = P(1+i) n = 2: F 2 = F 1 (1+i)= P(1+i) 2. n = N: F N = P(1+i) N

n = 2: F 2 = F 1 (1+i)= P(1+i) 2. n = N: F N = P(1+i) N")

20

0 $1,000 $1,259.71 1 2 3 $1,259.71 in three years is the economic equivalence of $1,000 now with interest rate 8% with compound calculation

21

Example You travel at 68 miles per hour Equivalent to 110 kilometers per hour Thus: 68 mph is equivalent to 110 kph Using two measuring scales Miles and Kilometers

22

Is “68” equal to “110”? No, not in terms of absolute numbers But they are “equivalent” in terms of the two measuring scales Miles Kilometers

23

Economic Equivalence Two sums of money at two different points in time can be made economically equivalent if: We consider an interest rate and, Number of Time periods between the two sums Equality in terms of Economic Value

24

Returning to the Example from previous slides Diagram the loan (Cash Flow Diagram) The company’s perspective is shown T=0t = 1 Yr $20,000 is received here $21,800 paid back here $20,000 now is economically equivalent to $21,800 one year from now IF the interest rate is set to equal 9%/year

The company’s perspective is shown T=0t = 1 Yr $20,000 is received here $21,800 paid back here $20,000 now is economically equivalent to $21,800 one year from now IF the interest rate is set to equal 9%/year")

25

$20,000 now is not equal in magnitude to $21,800 1 year from now But, $20,000 now is economically equivalent to $21,800 one year from now if the interest rate in 9% per year.

26

To have economic equivalence you must specify: Timing of the cash flows An interest rate (i% per interest period) Number of interest periods (N)

Number of interest periods (N)")

27

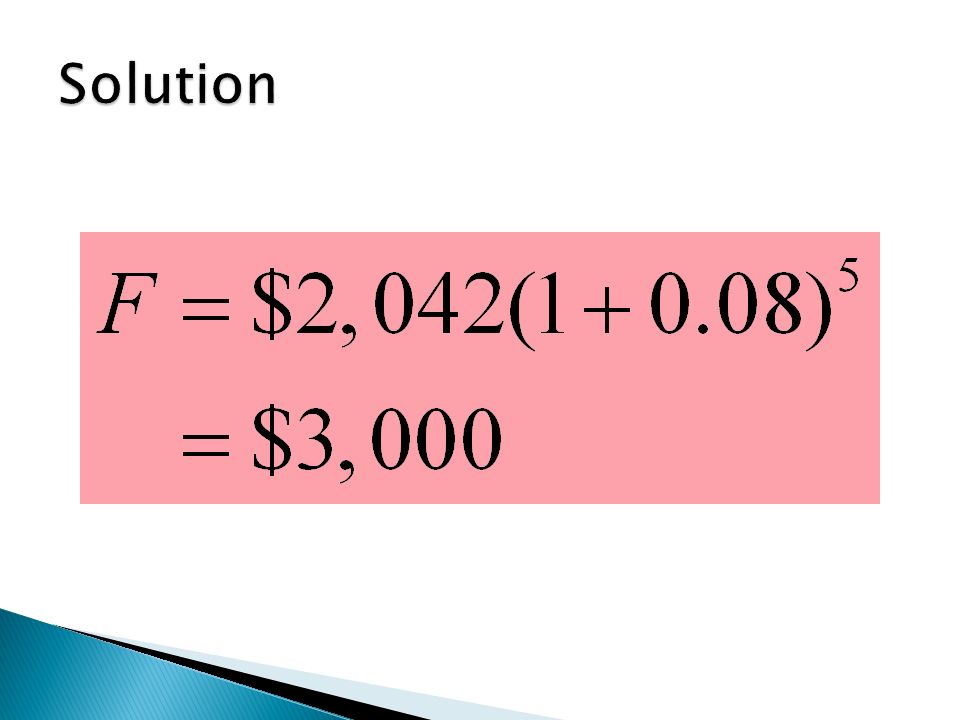

012 3 345 $2,042 5 F 0 At 8% interest, what is the equivalent worth of $2,042 now 5 years from now? If you deposit $2,042 today in a savings account that pays 8% interest annually. how much would you have at the end of 5 years? =

29

$3,289$2,042 50 At what interest rate would these two amounts be equivalent in 5 years period of time? i = ?

30

Equivalence Between Two Cash Flows Step 1: Determine the base period, say, year 5. Step 2: Identify the interest rate to use. Step 3: Calculate equivalence value. $3,289$2,042 50

31

Find the present dollar amount that will be economically equivalent to $5,877.32 in 5 years, given an interest rate of 8%. 0 1 2 3 4 5 P F $4,000 $5877.32 $4,320 $4,665.6 $5,441.96 $5,038.85

32

EXAMPLE OF EQUIVALENT CASH FLOWS $2,042 today was equivalent to receiving $3,000 in five years, at an interest rate of 8%. Are these two cash flows are also equivalent at the end of year 3? Equivalent cash flows are equivalent at any common point in time, as long as we use the same interest rate (8%, in our example).

..")

33

PRACTICE PROBLEM Compute the equivalent value of the cash flow series at n = 3, using i = 10%. Solution: Contemporary Engineering Economics, 5th edition, © 2010 012 3 4 5 $100 $80 $120 $150 $200 $100 V3V3

34

How many years would it take an investment to double at 10% annual interest? P 2P2P 0 N = ?

35

P 2P2P 0

36

Approximating how long it will take for a sum of money to double

38

Single payment compound amount factor (growth factor) P F N 0

P F N 0")

39

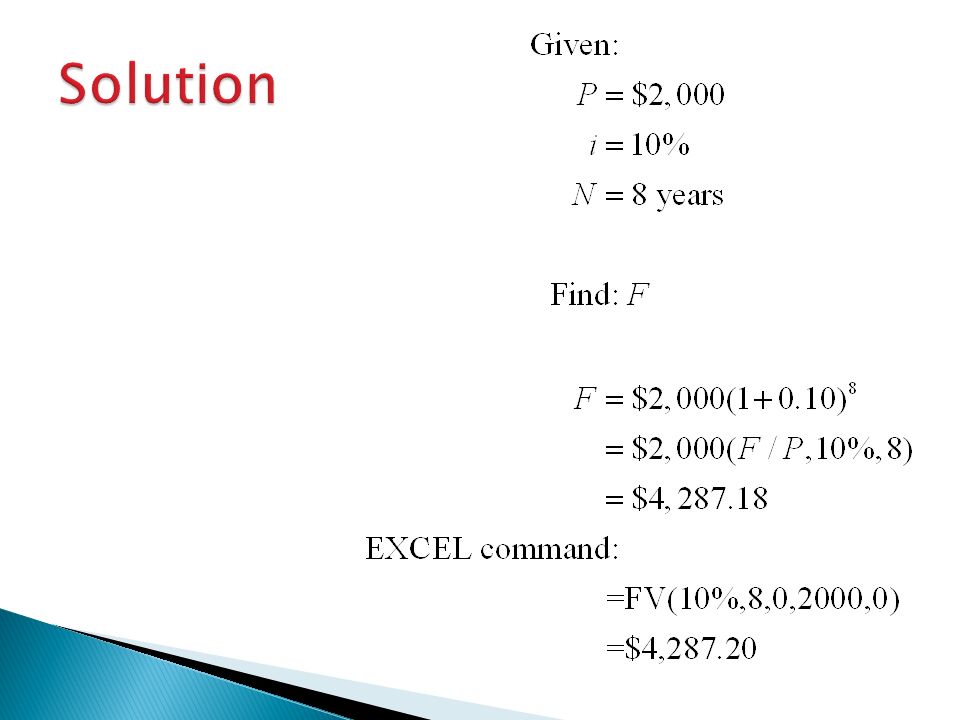

Practice Problem If you had $2,000 now and invested it at 10%, how much would it be worth in 8 years? $2,000 F = ? 8 0 i = 10%

41

Single Cash Flow Formula Single payment present worth factor (discount factor) Given: Find: P F N 0

Given: Find: P F N 0")

42

You want to set aside a lump sum amount today in a savings account that earns 7% annual interest to meet a future expense in the amount of $10,000 to be incurred in 6 years. How much do you need to deposit today?

43

0 6 $10,000 P

44

How much do you need to deposit today (P) to withdraw $25,000 at n =1, $3,000 at n = 2, and $5,000 at n =4, if your account earns 10% annual interest? 0 1 2 3 4 $25,000 $3,000 $5,000 P

45

0 1 2 3 4 $25,000 $3,000 $5,000 P 0 1 2 3 4 $25,000 P1P1 0 1 2 3 4 $3,000 P2P2 0 1 2 3 4 $5,000 P3 ++ Uneven Payment Series

46

01234 Beginning Balance 028,6226,484.204,132.624,545.88 Interest Earned (10%) 02,862648.42413.26454.59 Payment+28,622-25,000-3,0000-5,000 Ending Balance $28,6226,484.204,132.624,545.880.47 Rounding error

02, Payment+28,622-25,000-3,0000-5,000 Ending Balance $28,6226, , , Rounding error")

47

P = value or amount of money at a time designated as the present or time 0. Also P is referred to as present worth (PW), present value (PV), net present value (NPV), discounted cash flow (DCF), and capitalized cost (CC); dollars

, present value (PV), net present value (NPV), discounted cash flow (DCF), and capitalized cost (CC); dollars.")

48

F = value or amount of money at some future time. Also F is called future worth (FW) and future value (FV); dollars

and future value (FV); dollars.")

49

A = series of consecutive, equal, end ‑ of ‑ period amounts of money. Also A is called the annual worth (AW) and equivalent uniform annual worth (EUAW); dollars per year, dollars per month n = number of interest periods; years, months, days

and equivalent uniform annual worth (EUAW); dollars per year, dollars per month n = number of interest periods; years, months, days.")

50

i = interest rate or rate of return per time period; percent per year, percent per month t = time, stated in periods; years, months, days, etc

Similar presentations

2002 Contemporary Engineering Economics 1 Chapter 4 Time Is Money Interest: The Cost of Money Economic Equivalence Development of Interest Formulas.>")

2002 Contemporary Engineering Economics>")