Download presentation

Presentation is loading. Please wait.

1

Unit III: Costs of Production and Perfect Competition

2

Accountants vs. Economists

Accountants look at only EXPLICIT COSTS Explicit costs (out of pocket costs) are payments paid by firms for using the resources of others. Example: Rent, Wages, Materials, Electricity Bills Economists examine both the EXPLICIT COSTS and the IMPLICIT COSTS Implicit costs are the opportunity costs that firms “pay” for using their own resources Example: Forgone Wage, Forgone Rent, Time

are payments paid by firms for using the resources of others. Example: Rent, Wages, Materials, Electricity Bills. Economists examine both the EXPLICIT COSTS and the IMPLICIT COSTS. Implicit costs are the opportunity costs that firms pay for using their own resources. Example: Forgone Wage, Forgone Rent, Time.")

3

Analyzing Production

4

Inputs and Outputs To earn profit, firms must make products (output)

Inputs (FACTORS) are the resources used to make outputs. Total Physical Product (TP)- total output or quantity produced Marginal Product (MP)- the additional output generated by additional inputs (workers). Marginal Product = Change in Total Product Change in Inputs

are the resources used to make outputs. Total Physical Product (TP)- total output or quantity produced. Marginal Product (MP)- the additional output generated by additional inputs (workers). Marginal Product = Change in Total Product. Change in Inputs.")

5

What is the general relationship between inputs and outputs?

To earn profit, firms must make something (output) Inputs are the resources used to produce outputs. Input resources are also called FACTORS. Total Physical Product (TP)- total output or quantity produced What is the general relationship between inputs and outputs? Marginal Product (MP)- the additional output generated by additional inputs. Marginal Product = Change in Total Product Change in Labor Input Average Product (AP)- the output per unit of input Average Product = Total Product Units of Labor

Inputs are the resources used to produce outputs. Input resources are also called FACTORS. Total Physical Product (TP)- total output or quantity produced. What is the general relationship between inputs and outputs Marginal Product (MP)- the additional output generated by additional inputs. Marginal Product = Change in Total Product. Change in Labor Input. Average Product (AP)- the output per unit of input. Average Product = Total Product. Units of Labor.")

6

Total Product(TP) PIZZAS

Calculate the MP, identify the three stages, and explain why each stage occurs # of Workers (Input) Total Product(TP) PIZZAS Marginal Product(MP) 1 10 2 25 3 45 4 60 5 70 6 75 7 8

Total Product(TP) PIZZAS. Marginal Product(MP)")

7

Total Product(TP) PIZZAS

Calculate the MP, identify the three stages, and explain why each stage occurs # of Workers (Input) Total Product(TP) PIZZAS Marginal Product(MP) - 1 10 2 25 15 3 45 20 4 60 5 70 6 75 7 8 -5

Total Product(TP) PIZZAS. Marginal Product(MP)")

8

Total Product(TP) PIZZAS

Calculate the MP, identify the three stages, and explain why each stage occurs # of Workers (Input) Total Product(TP) PIZZAS Marginal Product(MP) - 1 10 2 25 15 3 45 20 4 60 5 70 6 75 7 8 -5

Total Product(TP) PIZZAS. Marginal Product(MP)")

9

Why does MP start to fall? Too many cooks in the kitchen!

The Law of Diminishing Marginal Returns As successive units of variable resources (workers) are added to fixed resources (machinery, tool, etc.), the additional output produced from each new worker will eventually fall. Too many cooks in the kitchen!

are added to fixed resources (machinery, tool, etc.), the additional output produced from each new worker will eventually fall. Too many cooks in the kitchen!")

10

Law of Diminishing Returns

There are three stages of returns. Total Product Total Product, TP Stage I: Increasing Marginal Returns Quantity of Labor Average Product, AP, and Marginal Product, MP Average Product Quantity of Labor Marginal Product

11

Law of Diminishing Returns

There are three stages of returns. Total Product Total Product, TP Stage II: Diminishing Marginal Returns Quantity of Labor Average Product, AP, and Marginal Product, MP Average Product Quantity of Labor Marginal Product

12

Law of Diminishing Returns

There are three stages of returns. Total Product Total Product, TP Stage III: Negative Marginal Returns Quantity of Labor Average Product, AP, and Marginal Product, MP Average Product Quantity of Labor Marginal Product

13

Short-Run Production Costs

14

Definitions Fixed Costs

Fixed costs (costs for fixed resources) DON’T change with the amount produced Ex: Rent, Insurance, Managers salaries, etc. Average Fixed Costs = Fixed Costs Quantity Variable Costs Variable costs (costs for variable resources) change as more or less is produced Ex: raw materials, labor, electricity, etc. Average Variable Costs = Variable Costs Quantity

DON’T change with the amount produced. Ex: Rent, Insurance, Managers salaries, etc. Average Fixed Costs = Fixed Costs. Quantity. Variable Costs. Variable costs (costs for variable resources) change as more or less is produced. Ex: raw materials, labor, electricity, etc. Average Variable Costs = Variable Costs. Quantity.")

15

Definitions Total Cost Sum of Fixed and Variable Costs Total Costs

Average Total Cost = Total Costs Quantity Marginal Cost Additional costs of and additional output. Ex: If the production of another output increases total cost from $100 to $120, the MC is $20. Marginal Cost = Change in Total Costs Change in Quantity

16

Calculating TC, VC, FC, ATC, AFC, and MC

TP VC FC TC MC AVC AFC ATC 100 - 1 10 2 16 3 21 4 26 5 30 6 36 7 46

17

Calculating TC, VC, FC, ATC, AFC, and MC

TP VC FC TC MC AVC AFC ATC 100 - 1 10 110 2 16 116 3 21 121 4 26 126 5 30 130 6 36 136 7 46 146

18

Calculating TC, VC, FC, ATC, AFC, and MC

TP VC FC TC MC AVC AFC ATC 100 - 1 10 110 2 16 116 6 3 21 121 5 4 26 126 30 130 36 136 7 46 146

19

Calculating TC, VC, FC, ATC, AFC, and MC

TP VC FC TC MC AVC AFC ATC 100 - 1 10 110 2 16 116 6 8 58 3 21 121 5 33.3 40.3 4 26 126 6.5 25 31.5 30 130 36 136 16.67 22.67 7 46 146 6.6 14.3 20.9

20

Calculating TC, VC, FC, ATC, AFC, and MC

TP VC FC TC MC AVC AFC ATC 100 - 1 10 110 2 16 116 6 8 50 58 3 21 121 5 7 33.3 40.3 4 26 126 6.5 25 31.5 30 130 20 36 136 16.67 22.67 46 146 6.6 14.3 20.9

21

Calculating TC, VC, FC, ATC, AFC, and MC

TP VC FC TC MC AVC AFC ATC 100 - 1 10 110 2 16 116 6 8 50 58 3 21 121 5 7 33.3 40.3 4 26 126 6.5 25 31.5 30 130 20 36 136 16.67 22.67 46 146 6.6 14.3 20.9

22

Per-Unit Costs (Average and Marginal)

ATC and AVC get closer and closer but NEVER touch MC 12 11 10 9 8 7 6 5 4 3 2 1 ATC AVC Costs (dollars) Average Fixed Cost AFC Quantity

Average Fixed Cost. AFC Quantity.")

23

Converting Average to Total At output Q, what area represents:

TC VC FC 0CDQ 0BEQ 0AFQ or BCDE

24

Why is the MC curve U-shaped?

12 11 10 9 8 7 6 5 4 3 2 1 Why is the MC curve U-shaped? Costs (dollars) Quantity

Quantity.")

25

Why is the MC curve U-shaped?

The MC curve falls and then rises because of diminishing marginal returns The additional cost of the first units produced fall when workers have increasing marginal returns. As production continues, each worker adds less and less to production so the marginal cost for each unit increases.

26

1. 2.

27

3. 4.

28

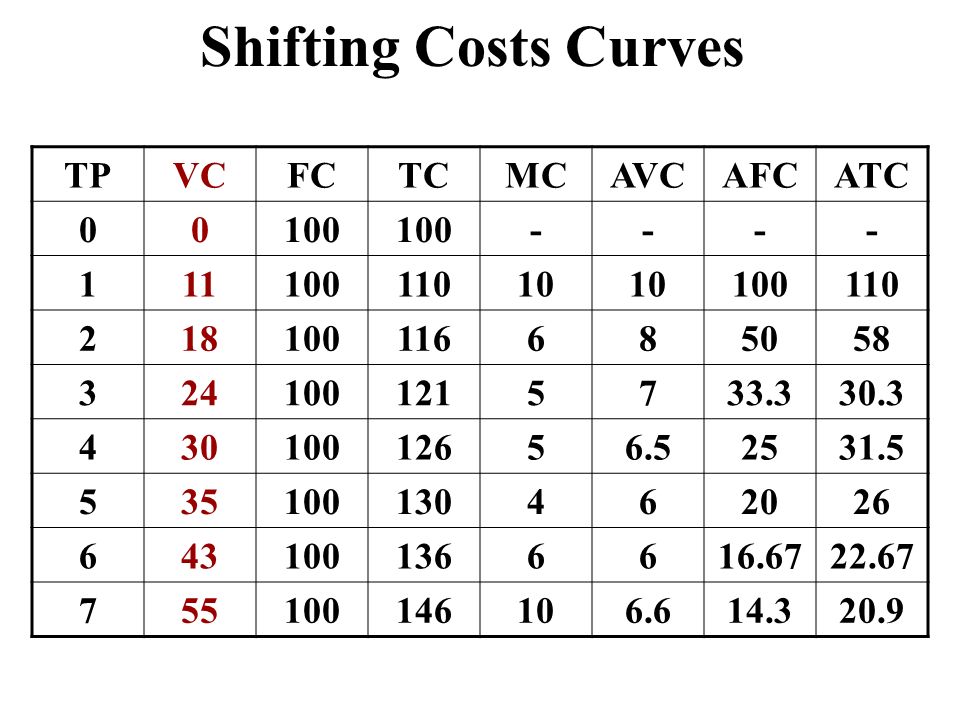

Shifting Cost Curves

29

What if Fixed Costs increase to $200

Shifting Costs Curves TP VC FC TC MC AVC AFC ATC 100 - 1 10 110 2 16 116 6 8 50 58 3 21 121 5 7 33.3 30.3 4 26 126 6.5 25 31.5 30 130 20 36 136 16.67 22.67 46 146 6.6 14.3 20.9 What if Fixed Costs increase to $200

30

Shifting Costs Curves TP VC FC TC MC AVC AFC ATC 100 - 1 10 110 2 16

100 - 1 10 110 2 16 116 6 8 50 58 3 21 121 5 7 33.3 30.3 4 26 126 6.5 25 31.5 30 130 20 36 136 16.67 22.67 46 146 6.6 14.3 20.9

31

Shifting Costs Curves TP VC FC TC MC AVC AFC ATC 200 100 - 1 10 110 2

200 100 - 1 10 110 2 16 116 6 8 50 58 3 21 121 5 7 33.3 30.3 4 26 126 6.5 25 31.5 30 130 20 36 136 16.67 22.67 46 146 6.6 14.3 20.9

32

Which Per Unit Cost Curves Change?

Shifting Costs Curves TP VC FC TC MC AVC AFC ATC 200 - 1 10 210 100 110 2 16 216 6 8 50 58 3 21 221 5 7 33.3 30.3 4 26 226 6.5 25 31.5 30 230 20 36 236 16.67 22.67 46 246 6.6 14.3 20.9 Which Per Unit Cost Curves Change?

33

ONLY AFC and ATC Increase!

Shifting Costs Curves TP VC FC TC MC AVC AFC ATC 200 - 1 10 210 100 110 2 16 216 6 8 50 58 3 21 221 5 7 33.3 30.3 4 26 226 6.5 25 31.5 30 230 20 36 236 16.67 22.67 46 246 6.6 14.3 20.9 ONLY AFC and ATC Increase!

34

ONLY AFC and ATC Increase!

Shifting Costs Curves TP VC FC TC MC AVC AFC ATC 200 - 1 10 210 110 2 16 216 6 8 100 58 3 21 221 5 7 66.6 30.3 4 26 226 6.5 50 31.5 30 230 40 36 236 33.3 22.67 46 246 6.6 28.6 20.9 ONLY AFC and ATC Increase!

35

If fixed costs change ONLY AFC and ATC Change!

Shifting Costs Curves If fixed costs change ONLY AFC and ATC Change! TP VC FC TC MC AVC AFC ATC 200 - 1 10 210 2 16 216 6 8 100 108 3 21 221 5 7 66.6 73.6 4 26 226 6.5 50 56.5 30 230 40 46 36 236 33.3 39.3 246 6.6 28.6 35.2 MC and AVC DON’T change!

36

Shift from an increase in a Fixed Cost

MC ATC1 ATC AVC Costs (dollars) AFC1 AFC Quantity

AFC1. AFC. Quantity.")

37

Shift from an increase in a Fixed Cost

MC ATC1 AVC Costs (dollars) AFC1 Quantity

AFC1. Quantity.")

38

What if the cost for variable resources increase

Shifting Costs Curves TP VC FC TC MC AVC AFC ATC 100 - 1 10 110 2 16 116 6 8 50 58 3 21 121 5 7 33.3 30.3 4 26 126 6.5 25 31.5 30 130 20 36 136 16.67 22.67 46 146 6.6 14.3 20.9 What if the cost for variable resources increase

39

Shifting Costs Curves TP VC FC TC MC AVC AFC ATC 100 - 1 10 110 2 16

100 - 1 10 110 2 16 116 6 8 50 58 3 21 121 5 7 33.3 30.3 4 26 126 6.5 25 31.5 30 130 20 36 136 16.67 22.67 46 146 6.6 14.3 20.9

40

Shifting Costs Curves TP VC FC TC MC AVC AFC ATC 100 - 1 11 110 10 2

100 - 1 11 110 10 2 18 116 6 8 50 58 3 24 121 5 7 33.3 30.3 4 30 126 6.5 25 31.5 35 130 20 26 43 136 16.67 22.67 55 146 6.6 14.3 20.9

41

Which Per Unit Cost Curves Change?

Shifting Costs Curves TP VC FC TC MC AVC AFC ATC 100 - 1 11 111 10 110 2 18 118 6 8 50 58 3 24 124 5 7 33.3 30.3 4 30 130 6.5 25 31.5 35 135 20 26 43 143 16.67 22.67 55 155 6.6 14.3 20.9 Which Per Unit Cost Curves Change?

42

Shifting Costs Curves TP VC FC TC MC AVC AFC ATC 100 - 1 11 111 10 110

100 - 1 11 111 10 110 2 18 118 7 8 50 58 3 24 124 6 33.3 30.3 4 30 130 6.5 25 31.5 5 35 135 20 26 43 143 16.67 22.67 55 155 12 6.6 14.3 20.9 MC, AVC, and ATC Change!

43

Shifting Costs Curves TP VC FC TC MC AVC AFC ATC 100 - 1 11 111 110 2

100 - 1 11 111 110 2 18 118 7 9 50 58 3 24 124 6 8 33.3 30.3 4 30 130 7.5 25 31.5 5 35 135 20 26 43 143 7.16 16.67 22.67 55 155 12 7.8 14.3 20.9 MC, AVC, and ATC Change!

44

If variable costs change MC, AVC, and ATC Change!

Shifting Costs Curves If variable costs change MC, AVC, and ATC Change! TP VC FC TC MC AVC AFC ATC 100 - 1 11 111 2 18 118 7 9 50 59 3 24 124 6 8 33.3 41.3 4 30 130 7.5 25 32.5 5 35 135 20 27 43 143 7.16 16.67 23.83 55 155 12 7.8 14.3 22.1

45

Shift from an increase in a Variable Costs

MC1 MC ATC1 AVC1 ATC AVC Costs (dollars) AFC Quantity

AFC. Quantity.")

46

Shift from an increase in a Variable Costs

MC1 ATC1 AVC1 Costs (dollars) AFC Quantity

AFC. Quantity.")

47

Long-Run Cost Curves

48

Short-Run vs. Long-Run The short-run is a period in which at least one resource is fixed. Plant capacity/size is NOT changeable In the long-run ALL resources are variable NO fixed resources Plant capacity/size is changeable

49

Long Run ATC What happens to the average total costs of a product when a firm increases its plant capacity? Example of various plant sizes: I make looms out of my garage with one saw I rent out building, buy 5 saws, hire 3 workers I rent a factory, buy 20 saws and hire 40 workers I build my own plant and use robots to build looms. I create plants in every major city in the U.S. Long Run ATC curve is made up of all the different short run ATC curves of various plant sizes.

50

5 Various Plant Capacities

Long Run ATC 5 Various Plant Capacities Unit Costs Output

51

The long-run ATC is the result of all of the short-run ATC curves.

Unit Costs Output

52

Why is LRATC U Shaped? The law of diminishing marginal returns doesn’t apply in the long run because all resources are variable. LRATC Unit Costs Output

53

Three Areas on the LRATC Curve

Economies of Scale- LRATC is falling as mass production techniques can be utilized. Economies of scale Unit Costs long-run ATC Output

54

Three Areas on the LRATC Curve

Constant Returns to Scale- The average total cost is as low as it can get. Economies of scale Constant returns to scale Unit Costs long-run ATC Output

55

Three Areas on the LRATC Curve

Diseconomies of Scale- The LRATC is increasing as the firm gets too big and difficult to manage. Economies of scale Constant returns to scale Diseconomies of scale Unit Costs long-run ATC Output

56

Perfect Competition

57

FOUR MARKET MODELS Characteristics of Pure Competition:

Many small firms Identical products (perfect substitutes) Firms are “Price Takers” Easy for firms to enter and exit the industry No control over price. No need to advertise Examples: Corn or Avocado farmers, TJ hammocks Pure Competition Monopolistic Competition Pure Monopoly Oligopoly Market Structure Continuum

Firms are Price Takers Easy for firms to enter and exit the industry. No control over price. No need to advertise. Examples: Corn or Avocado farmers, TJ hammocks. Pure. Competition. Monopolistic. Competition. Pure. Monopoly. Oligopoly. Market Structure Continuum.")

58

Demand for Perfectly Competitive Firms (A Horizontal straight line)

Why are they Price Takers? If a firm charges above the market price, NO ONE will buy. They will go to other firms There is no reason to price low because consumers will buy just as much at the market price. Since the price is the same at all quantities demanded, the demand curve and MR for each firm is… Perfectly Elastic (A Horizontal straight line)

")

59

Maximizing PROFIT

60

Profit Maximizing Rule

MR = MC Maximizing PROFIT

61

Draw a FIRM making a profit

62

Draw a FIRM making a profit

MC ATC MR Profit Price P Q Quantity

63

Draw a FIRM making a loss

64

Draw a FIRM making a loss

MC ATC Price P Loss MR Q Quantity

65

Don’t forget that averages show PER UNIT COSTS

How much output should be produced? How much is Total Revenue? How much is Total Cost? Is there profit or loss? How much? $9 8 7 6 5 4 3 2 1 MC MR=Price Cost and Revenue Profit = $18 ATC AVC Don’t forget that averages show PER UNIT COSTS Total Cost=$45 Total Revenue =$63

66

the MR=MC rule still applies

Loss Minimization Position What would happen if the price is lowered from $7 to $5… the MR=MC rule still applies …but the output changes.

67

How much output should be produced?

How much is Total Revenue? How much is Total Cost? Is there profit or loss? How much? MC $9 8 7 6 5 4 3 2 1 ATC Cost and Revenue AVC Loss =$7 MR=Price Total Cost = $42 Total Revenue=$35

68

What would happen if the price is lowered from $5 to $4…

…the firm must SHUT-Down A firm should continue to produce as long as the price is above the AVC. Even though they are losing money, they are still paying some of their fixed costs. When the price falls below AVC then the firm should minimize its losses by shutting down. This is called the… Shutdown Point

69

Minimum AVC is shut down point

SHUT DOWN! Produce Zero MC $9 8 7 6 5 4 3 2 1 ATC Cost and Revenue AVC Minimum AVC is shut down point

70

Producing nothing is cheaper than staying open.

SHUT DOWN! Producing nothing is cheaper than staying open. MC $9 8 7 6 5 4 3 2 1 ATC Cost and Revenue AVC Fixed Costs MR=Price Total Cost Total Revenue

72

Supply Revisited

73

Marginal Cost & Supply Break-even Point (No Economic Profit) MR5

MC P5 MR5 ATC MR4 P4 Cost and Revenue, (dollars) AVC P3 MR3 P2 MR2 MR1 P1 Do not Produce – Below AVC Q2 Q3 Q4 Q5 Quantity Supplied

AVC. P3. MR3. P2. MR2. MR1. P1. Do not. Produce – Below AVC. Q2. Q3. Q4. Q5. Quantity Supplied.")

74

Supply = Marginal Cost above AVC

Marginal Cost & Supply Supply = Marginal Cost above AVC This is the Supply Curve Supply= MC P5 MR5 MR4 P4 Cost and Revenue, (dollars) P3 MR3 P2 MR2 MR1 P1 Q2 Q3 Q4 Q5 Quantity Supplied

P3. MR3. P2. MR2. MR1. P1. Q2. Q3. Q4. Q5. Quantity Supplied.")

75

What if variable costs increase?

Marginal Cost & Short-Run Supply MC2 S2 Cost and Revenue, (dollars) MC1 AVC1 Quantity Supplied S1 AVC2 What if variable costs increase? Supply Curve shifts to the Left

MC1. AVC1. Quantity Supplied. S1. AVC2. What if variable costs increase Supply Curve shifts to the Left.")

76

Marginal Cost & Short-Run Supply

Cost and Revenue, (dollars) MC1 AVC1 Quantity Supplied S1 Lower Costs Move the Supply Curve to the Right MC2 S2 AVC2

MC1. AVC1. Quantity Supplied. S1. Lower Costs Move. the Supply Curve. to the Right. MC2. S2. AVC2.")

77

Perfect Competition in the Long-Run

78

(No Economic Profit=Normal Profit)

In the Long-run… Firms will enter if there is profit Firms will leave if there is loss All firms break even, they make NO economic profit (No Economic Profit=Normal Profit) In long run equilibrium the firm is efficient. (Price = Minimum ATC)

In long run equilibrium the firm is efficient. (Price = Minimum ATC)")

79

Firm making a normal profit

LONG-RUN EQUILIBRIUM FOR A COMPETITIVE FIRM MC ATC Price P MR Price = MC = Minimum ATC Firm making a normal profit Q Quantity

80

What happens when there is a change in price?

LONG-RUN EQUILIBRIUM FOR A COMPETITIVE FIRM What happens when there is a change in price? MC ATC Price P MR When at Long-Run Equilibrium, there is no incentive to enter or leave the industry. Q Quantity

81

Changes in the long-run equilibrium

PROFIT MAXIMIZATION IN THE LONG RUN Changes in the long-run equilibrium S1 P Q 100 100,000 Industry Firm (price taker) $60 50 40 MC ATC MR D1

$ MC. ATC. MR. D1.")

82

What happens when demand increases?

PROFIT MAXIMIZATION IN THE LONG RUN What happens when demand increases? Economic Profits S1 P Q 100 100,000 Industry Firm (price taker) $60 50 40 MC ATC MR D2 D1

$ MC. ATC. MR. D2. D1.")

83

PROFIT MAXIMIZATION IN THE LONG RUN

New competitors enter. This increases supply and lowers price back to equilibrium. Zero Economic Profits S1 P Q 100 100,000 Industry Firm (price taker) $60 50 40 S2 MC ATC MR D2 D1

$ S2. MC. ATC. MR. D2. D1.")

84

Firm Industry Result is Long-Run Equilibrium Again.

The ONLY change is the industry’s output Zero Economic Profits S1 P Q 100 100,000 Industry Firm (price taker) $60 50 40 S2 MC ATC MR D2 D1

$ S2. MC. ATC. MR. D2. D1.")

85

Firm Industry Decreases in demand, losses, and the

PROFIT MAXIMIZATION IN THE LONG RUN Decreases in demand, losses, and the reestablishment of long-run equilibrium S1 P Q 100 100,000 Industry Firm (price taker) $60 50 40 MC ATC MR D1

$ MC. ATC. MR. D1.")

86

Firm Industry A decrease in demand creates losses… Economic Losses P Q

PROFIT MAXIMIZATION IN THE LONG RUN A decrease in demand creates losses… Economic Losses S1 P Q 100 100,000 Industry Firm (price taker) $60 50 40 MC ATC MR D1 D2

$ MC. ATC. MR. D1. D2.")

87

Firm Industry Competitors with losses leave, decrease supply, and

PROFIT MAXIMIZATION IN THE LONG RUN Competitors with losses leave, decrease supply, and prices return to zero economic profits. S3 Return to Zero Economic Profits S1 P Q 100 100,000 Industry Firm (price taker) $60 50 40 MC ATC MR D1 D2

$ MC. ATC. MR. D1. D2.")

88

Firm Industry Result is Long-Run Equilibrium Again. Zero Economic P

PROFIT MAXIMIZATION IN THE LONG RUN Result is Long-Run Equilibrium Again. Zero Economic Profits S1 P Q 100 100,000 Industry Firm (price taker) $60 50 40 S2 MC ATC MR D2 D1

$ S2. MC. ATC. MR. D2. D1.")

90

Efficiency

91

1. Productive Efficiency 2. Allocative Efficiency

PURE COMPETITION AND EFFICIENCY In general, efficiency is the optimal use of societies scarce resources Perfect Competition forces producers to use limited resources to their fullest. Inefficient firms have higher costs and are the first to leave the industry. Perfectly competitive industries are extremely efficient There are two kinds of efficiency: 1. Productive Efficiency 2. Allocative Efficiency

92

Price = Minimum ATC Productive Efficiency

PURE COMPETITION AND EFFICIENCY Productive Efficiency The production of a good in a least costly way. (Minimum amount of resources are being used) Graphically it is where… Price = Minimum ATC

Graphically it is where… Price = Minimum ATC.")

93

Allocative Efficiency

PURE COMPETITION AND EFFICIENCY Allocative Efficiency The distribution of resources towards the production of products most wanted by society. Graphically it is where… Price(Marginal Benefit) = MC

= MC.")

94

Productive Efficiency in the Long-Run Optimal amount being produced

Long-Run Equilibrium MC ATC MR P Price The marginal benefit to society (as measured by the price) equals the marginal cost. Q Optimal amount being produced Quantity

equals the marginal cost. Q. Optimal amount being produced. Quantity.")

95

equilibrium perfectly competitive firms have

Long-Run Equilibrium In long run equilibrium perfectly competitive firms have both productive and allocative efficiency MC ATC Price MR P P = Minimum ATC = MC Q Quantity

Similar presentations