Download presentation

Presentation is loading. Please wait.

1

12-1 Chapter Twelve Financial Considerations

2

12-2 Chapter learning objectives 12.1 Appreciate the potential benefits of accounting and financial analysis in an event management context 12.2 Understand what records a business is required to keep for taxation purposes 12.3 Explain the accounting process and the double- entry method 12.4 Understand how to develop a trial balance and explain its value and use 12.5 Understand how to develop a balance sheet and explain its value and use

3

12-3 Chapter learning objectives 12.6 Understand how to develop a profit and loss statement and explain its value and use 12.7 Understand how to develop a range of financial ratios and explain their use 12.8 Appreciate the value and importance of financial analysis in the event management context. 12.9 Understand key issues associated with the management of finance.

4

12-4 Units of Competence and Elements BSBFIM601A Manage finances 1.Plan for financial management 2.Establish budgets and allocate funds 3. Implement budgets 4.Report on finances

5

Introduction and potential benefits of accounting and financial analysis Profit is based on customer satisfaction. Why accounting information is important: –For taxation purposes –Shows: how a business is performing what a business is worth how financial performance can be improved –For making informed business decisions. 12-5

6

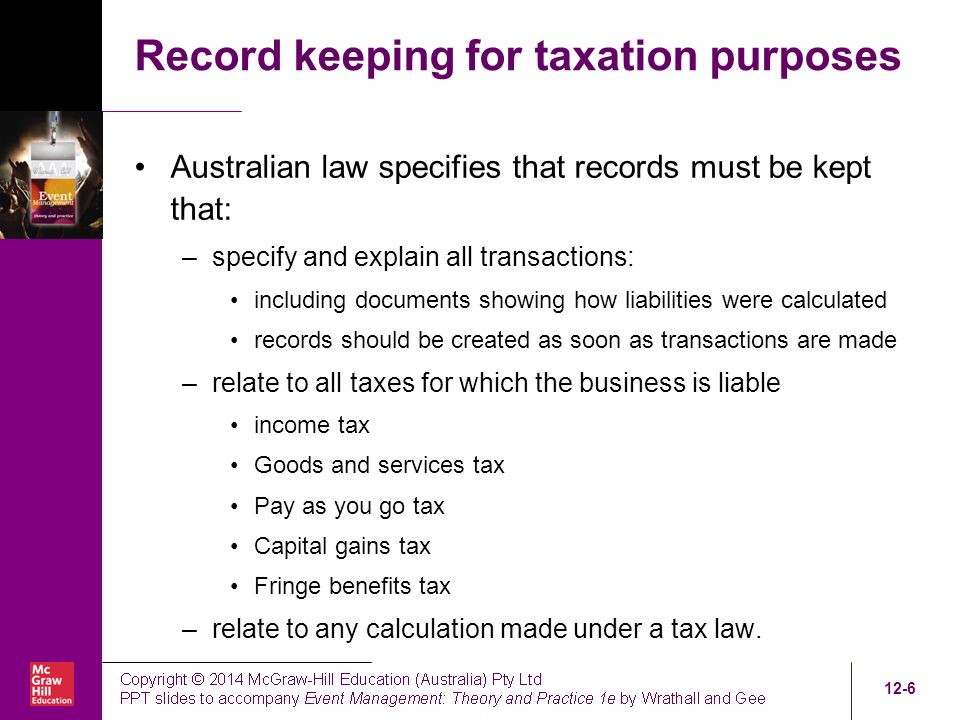

Record keeping for taxation purposes Australian law specifies that records must be kept that: –specify and explain all transactions: including documents showing how liabilities were calculated records should be created as soon as transactions are made –relate to all taxes for which the business is liable income tax Goods and services tax Pay as you go tax Capital gains tax Fringe benefits tax –relate to any calculation made under a tax law. 12-6

7

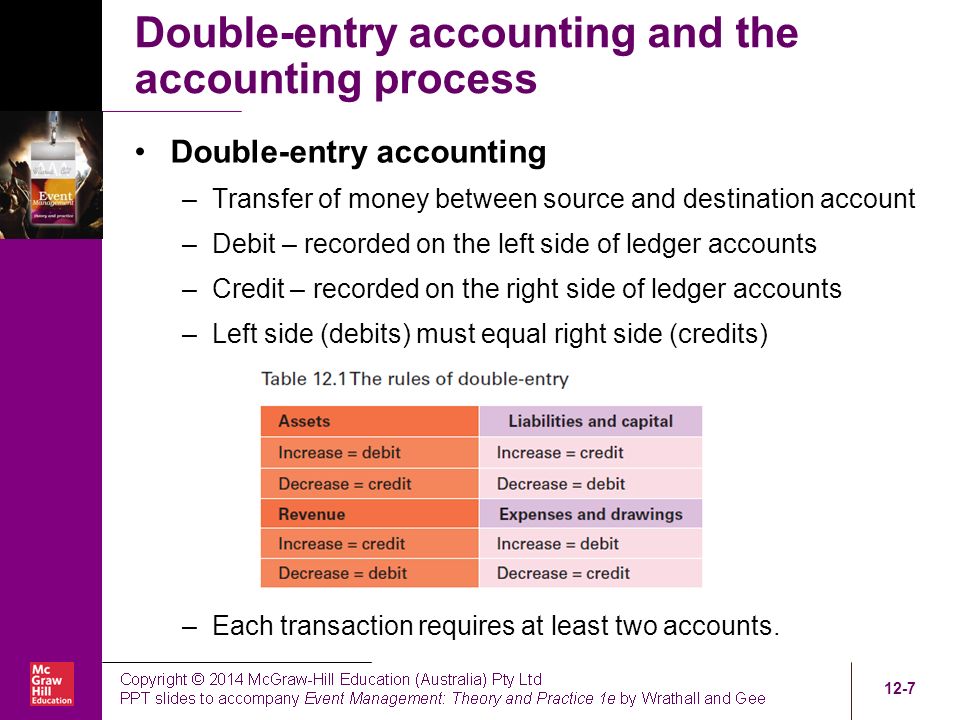

Double-entry accounting and the accounting process Double-entry accounting –Transfer of money between source and destination account –Debit – recorded on the left side of ledger accounts –Credit – recorded on the right side of ledger accounts –Left side (debits) must equal right side (credits) –Each transaction requires at least two accounts. 12-7

8

Double-entry accounting and the accounting process The accounting process –Transactions Involve an exchange Internal – within an organisation External – between businesses –Source documents Produced each time a transaction occurs –Journals and ledgers Journals record all transactions impacting on the business Tallied at the end of the month to provide summary General journals are the simplest forms Transferred or posted to ledger accounts. 12-8

9

Double entry accounting and the accounting process 12-9 Table 12.3 (a)

")

10

Double-entry accounting and the accounting process 12-10 Part of Table 12.4

11

Development and use of a trial balance A list of all of the ledger accounts. Debits must equal credits. Errors can be found here before moving to other financial documents. Insert table 12.5 12-11

12

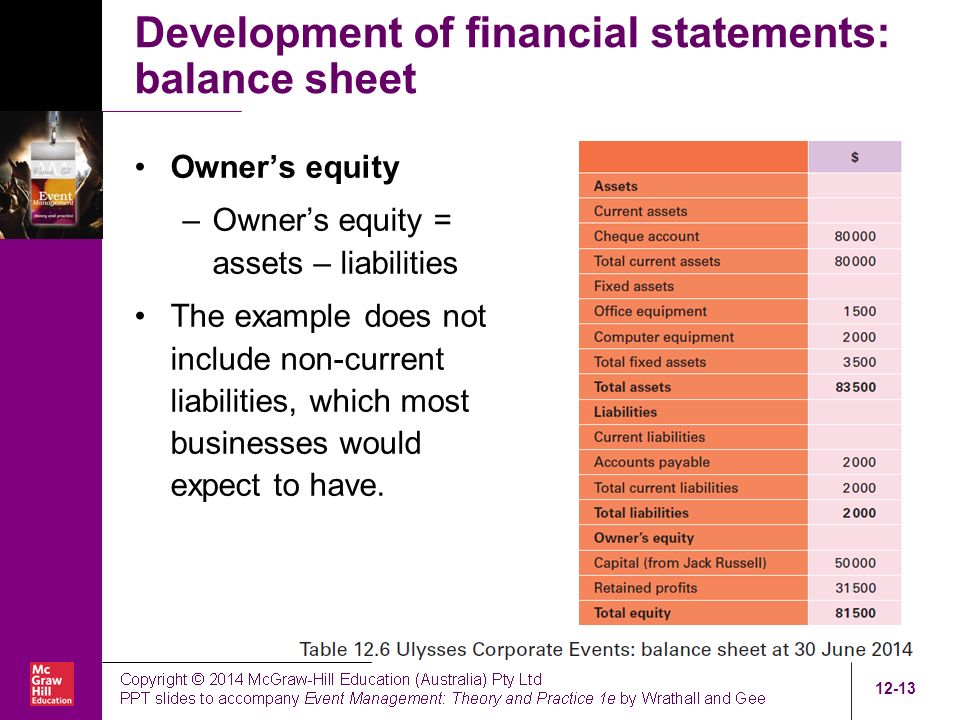

Development of financial statements: balance sheet Provides a summary of the current worth or financial position of the business at a point in time. Owner’s equity = assets – liabilities. Assets –Current assets –Fixed assets –Intangible assets Liabilities –Current liabilities –Non-current liabilities 12-12

13

Development of financial statements: balance sheet Owner’s equity –Owner’s equity = assets – liabilities The example does not include non-current liabilities, which most businesses would expect to have. 12-13

14

Development of financial statements: the profit and loss statement Reports on the net profit recorded over a period of time. Net profit = revenue – expenses. Revenue – income earned by the business. Expenses – costs incurred by a business to earn revenue. Net profit becomes retained earnings in the balance sheet. 12-14

15

Development of financial statements: cash flow statement Also called a statement of cash flows or funds flow statement. Profits do not mean there are no cash flow problems. Cash flow statement shows a business’s liquidity. Reports inflows and outflows of cash related to: –operating activities –investing activities –financing activities. Cash flows are produced over short periods to highlight issues, e.g. monthly. 12-15

16

Development of financial statements: cash flow statement 12-16

17

Financial ratios Measures of liquidity –Current ratio Measures ability to meet creditor demands –Net working capital Alternative measure of liquidity Net working capital = current assets – current liabilities Needs to be positive 12-17 Current ratio= current assets current liabilities

18

Financial ratios Leverage measures –Debt–equity ratio Relative amount of funds provided through debt The higher the ratio, the higher the risk of defaulting Measures of profitability –Net profit margin Rate of profit from total revenue 12-18 Debt–equity ratio = long-term debt equity Net profit margin = net profit total revenues

19

Financial ratios –Return on assets (ROA) –Return on equity (ROE) Measure of overall profitability of a business 12-19 return on assets = net profit total assets return on equity = net profit equity

–Return on equity (ROE) Measure of overall profitability of a business return on assets = net profit total assets return on equity = net profit equity")

20

The value of financial analysis in making business decisions Business decisions always have financial implications. The ability to interpret financial information is critical. Measures of liquidity can show cash flow problems, and control measures can be implemented. Leverage measures can show too much debt is being carried, and reduction of debt is required. Measures of profitability can show comparisons with other similar businesses. 12-20

21

Managing event finances In order to ensure financial viability: –Continuously monitor liquidity If liquidity problems begin to emerge take corrective action to increase cash inflows and reduce cash outflows –Monitor levels of debt If debt levels rise significantly consider actions that may reduce reliance on debt –Measure profitability and ROA, and analyse recent trends Reductions in levels of profitability may highlight the need to look for new sources of revenue or seek ways of reducing costs 12-21

22

Chapter summary The accounting process starts with a transaction. These transactions needs to be followed through to posts in journals, then transferred to ledgers. At the end of the financial year, trial balances, balance sheets, profit and loss statements and cash flow statements should be prepared. Key financial ratios can then be calculated to monitor the state of the business and its ability to maintain operations and aid in the decision-making process. 12-22

Similar presentations