Download presentation

Presentation is loading. Please wait.

2

Credit Depth in Latin America In Latin America, credit is scarce... Note: Simple average within regions. Mean Value for the 1990s. Source: World Bank data.

3

Credit Depth in Latin America... especially in continental Latin America, even controlling for the level of development

4

Interest Rate Margin Credit in Latin America is costly. Note: Simple average within regions. Mean Value for the 1990s. Source: IMF data.

5

Interest Rate Margin Low financial development is associated with high spreads.

6

Credit Volatility And credit is also highly volatile

7

Credit Volatility...credit volatility is related with an underdeveloped financial sector.

8

Recurring Banking Crises LAC is the region of the world with the highest banking crisis recurrence

9

Banking Credit in Latin America No wonder, lack of credit is firms’ concern number 1No wonder, lack of credit is firms’ concern number 1 restrictedMoreover, access to credit is restricted for certain groups, in particular SMEs limitThese characteristics of credit limit economic performance and poverty alleviation.

10

This Report... Explores these characteristics of banking credit from three perspectives –The effects of crises, their resolution and prevention –The impact of changes in the structure of the banking sector –The role played by the institutions supporting credit markets

11

Crisis and Volatility The volatility of the banking sector reflects a history of macroeconomic imbalances In many countries dollarization is high...

12

Crisis and Volatility... as well as public sector debt holdings.

13

Crisis and Volatility: Sudden Stops Despite contagion in capital markets, the probability of a sudden stop depends on the interaction between openness and the degree of dollarization

14

Crisis and Volatility: Twin Crises This is highly relevant considering that sudden stops and banking crises are another set of twins (75% in dollarized countries)

")

15

Crisis and Volatility: Balance Sheets Abrupt changes in relative prices lead to government’s and non tradable firm’s bankruptcies.

16

Crisis Prevention and Resolution In contrast to developed countries, inadequate resolution of crises in LAC (where depositors pay for the crises) has increased the volatility of deposits.

has increased the volatility of deposits.")

17

Crisis Prevention and Resolution Faulty financial safety nets have also increased volatility –They induced excessive risk taking by banks and low depositor market discipline. –Weak regulation and supervision generated incorrect risk valuation and poor banking practices.

18

Crisis Prevention and Resolution The degree of compliance of Basel Core Principles in LAC is very low

19

Banking System Structure: Consolidation Following the banking crises of the 1980’s and 1990’s, and financial liberalization, there was consolidation of the banking industry Concentration has not reduced competition. (evidence that higher concentration reduces NIM and overhead costs). Concentration has reduced credit volatility, increased access to credit, and eased supervision.

. Concentration has reduced credit volatility, increased access to credit, and eased supervision..")

20

Banking System Structure: Foreign Banks – –There was a drastic change in bank ownership in favor of foreign banking. More than 50% in Argentina, Chile, Mexico and Peru

21

Banking System Structure: Foreign Banks Foreign banking has: –Increased efficiency (lower interest rate margins) –But has had mixed results in other areas: Credit access has not increased, particualrly that of SMEs Has made credit less vulnerable to liquidity shocks, but more vulnerable to productivity shocks

–But has had mixed results in other areas: Credit access has not increased, particualrly that of SMEs Has made credit less vulnerable to liquidity shocks, but more vulnerable to productivity shocks")

22

Banking System Structure: Public Banking Public banks have reduced their participation in LAC

23

Banking System Structure: Public Banking Although public banking has decreased, it remains an important share of total banking Public banks enjoy strong political support...... but they are inefficient (significantly higher operating costs),... do not lend more to SMEs nor to sectors with greater funding needs They have low deposit rates because they offer an implicit government guarantee (implying a hidden fiscal liability). However, their performance should be measured against their social mandate.

,... do not lend more to SMEs nor to sectors with greater funding needs They have low deposit rates because they offer an implicit government guarantee (implying a hidden fiscal liability). However, their performance should be measured against their social mandate..")

24

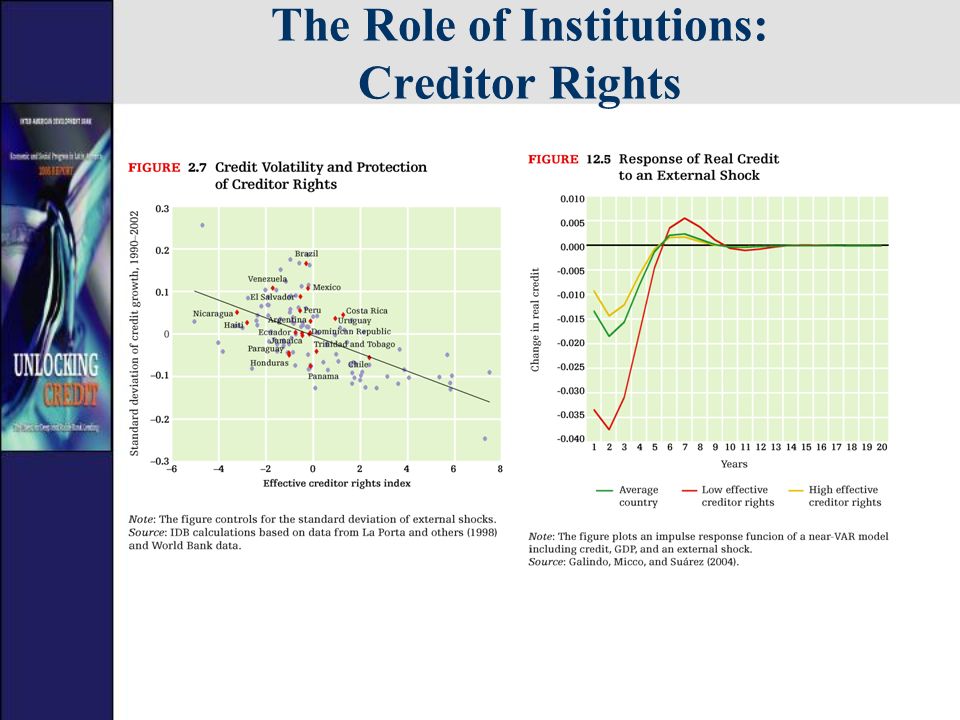

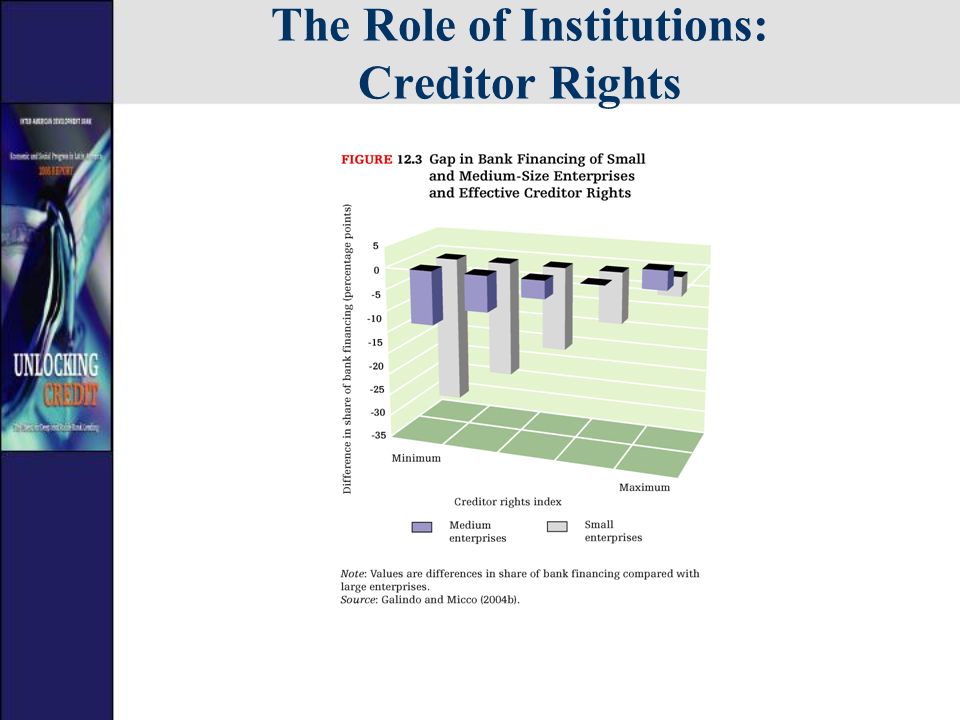

The Role of Institutions: Weak Creditor Rights in LAC

25

The Role of Institutions: Creditor Rights Creditor rights in LAC are weak. – –Regulations are tilted in favor of debtors during bankruptcy procedures. – –Courts are highly inefficient (a typical bankruptcy procedure lasts 4 years) – –Too many obstacles to recovering collateral Improving creditor rights can: – –increase financial depth (by 15% of GDP) – –reduce credit volatility by nearly half... – –and increase access to credit by SMEs by at least 15%. However, reform may be difficult to implement. A critical constituency is needed

– –Too many obstacles to recovering collateral Improving creditor rights can: – –increase financial depth (by 15% of GDP) – –reduce credit volatility by nearly half... – –and increase access to credit by SMEs by at least 15%. However, reform may be difficult to implement. A critical constituency is needed.")

26

The Role of Institutions: Creditor Rights

29

Future Challenges: Basel II Basel II tries to improve risk valuation and strengthen the link between risk and capital requirements and provisions Adopting Basel II is not a trivial matter: –Low compliance of Basel I –Scarce development of rating agencies –Actual levels of capitalization and difficulty to increase them –Low availability of information –Mixed degree of technical sophistication of banks and supervisors

30

Future Challenges: Money Laundering Money laundering is a global problem, but has a high incidence in Latin America. Money laundering is strongly related to: –weak government institutions, in particular legal entities –weak corporate governance of firms –weak bank regulation and supervision –underdeveloped financial systems

31

Policy Agenda Plan ahead to avoid crisis –Reducing the likelihood of twin crises requires dealing with domestic liability dollarization (currency mismatches) via regulation in the banking system and/or the creation of hedging markets. –Reducing liability dollarization calls for increasing central bank independence (low inflation volatility and the reduction of fiscal pressures) introducing sound alternatives to dollar assets, such as CPI- indexed instruments. –Facing sudden stops with a pre-announced monetary policy that reduces uncertainty.

introducing sound alternatives to dollar assets, such as CPI- indexed instruments. –Facing sudden stops with a pre-announced monetary policy that reduces uncertainty..")

32

Policy Agenda Pay for your sins: –Crisis resolution processes must ensure that the parties that took higher risk bear the brunt of the costs. Play safe: –Financial regulation needs to appropriately measure credit risks (including the treatment of dollar loans and government debt) to determine safe levels of capital- adequacy ratios and provisions. –Basel I remains a challenge for the region, and the adoption of Basel II requires caution.

to determine safe levels of capital- adequacy ratios and provisions. –Basel I remains a challenge for the region, and the adoption of Basel II requires caution..")

33

Policy Agenda Define the government’s business: –The role of government in commercial banking needs to be redefined by specifying their social mandate and ensuring cost effectiveness. Design the right environment: –Increasing creditor protection requires a serious reform of secured transaction laws. A first step is the creation of specialized courts to deal with collateral claims. –Establish a regulatory framework for proper information sharing to increase credit access and enhance supervision.

Similar presentations