Download presentation

Presentation is loading. Please wait.

1

FINANCIAL ACCOUNTING A USER PERSPECTIVE Hoskin Fizzell Davidson Second Canadian Edition

2

Long-term Liabilities Chapter Ten

3

Bonds Companies may raise long-term funds through: –Equity (stock) market –Debt market Borrow money from a commercial bank Sell bonds to investors

market –Debt market Borrow money from a commercial bank Sell bonds to investors")

4

Bond Characteristics Formal agreement Specifies –How the money is to be paid back –Conditions that must be met during the period of the loan Stated in the indenture agreement May include restrictions (bond covenants)

")

5

Bond Characteristics Bonds traded in public markets are standardized, stating –Face value: $1,000 Specifies the cash payment to be made at maturity –Semi-annual interest payments –Bond interest rate Stated as an annual percentage

6

Bond Characteristics Mortgage bond –Has real property as collateral Collateral trust bond –Provides shares and bonds of other companies as collateral Debenture bond –Carries no specific collateral

7

Bond Characteristics Some bonds have special provisions –Convertible bonds Convertible to a specified number of common shares

8

Public Bond Issues Investment banker –Helps design the bond issue –Responsible for the initial sale of the issue to its investor clients Underwriters –Investment bankers jointly responsible for selling the issue

9

Bond Pricing Market price of bonds is determined by discounting future cash flows Example: –A company issues a $1,000 bond with two years to maturity –Interest is 10% paid semi-annually

10

Bond Pricing The company expects the investor to demand a return of 8% compounded semi-annually from this type of investment What price can the company expect to get from this offering?

11

Bond Pricing The cash flows must be discounted using the yield rate of 8%. (Often called the discount rate or market rate)

.")

12

Bond Pricing Assumptions Face value$1,000 Bond interest rate10% Time to maturity2 years Yield rate8%

13

Bond Pricing Calculation Number of periods = Time to maturity x 2 = 2 years x 2 = 4 Yield rate per period= Yield rate / 2 = 8% / 2 = 4% Interest payments= Face amount x bond interest rate x 1/2 = $1,000 x 10% x 1/2 = $50

14

Bond Pricing

15

Calculate present value of future cash flows

16

Bond Pricing Alternative calculation: Interest payments (treated as an annuity) $50 x 3.6299 (present value for 4 periods at 4%) + ($1,000 x 0.8548) = $181.50 + $854.80 = $1,036.30

$50 x (present value for 4 periods at 4%) + ($1,000 x ) = $ $ = $1,036.30")

17

Bond Pricing If the buyers demand a 12% return on their investment: PV of bond = PV of interest payments + PV of maturity payment = PV of annuity of $50 for 4 periods at 6% (Table 4) + PV of $1,000 for 4 periods at 6% (Table 2) = ($50 x 3.4651) + ($1,000 x 0.7921) = $965.35

+ PV of $1,000 for 4 periods at 6% (Table 2) = ($50 x ) + ($1,000 x ) = $965.35")

18

Bond Pricing Selling price: –Higher than face value –Lower than face value –Equals face value Bond issued at: Premium Discount At Par

19

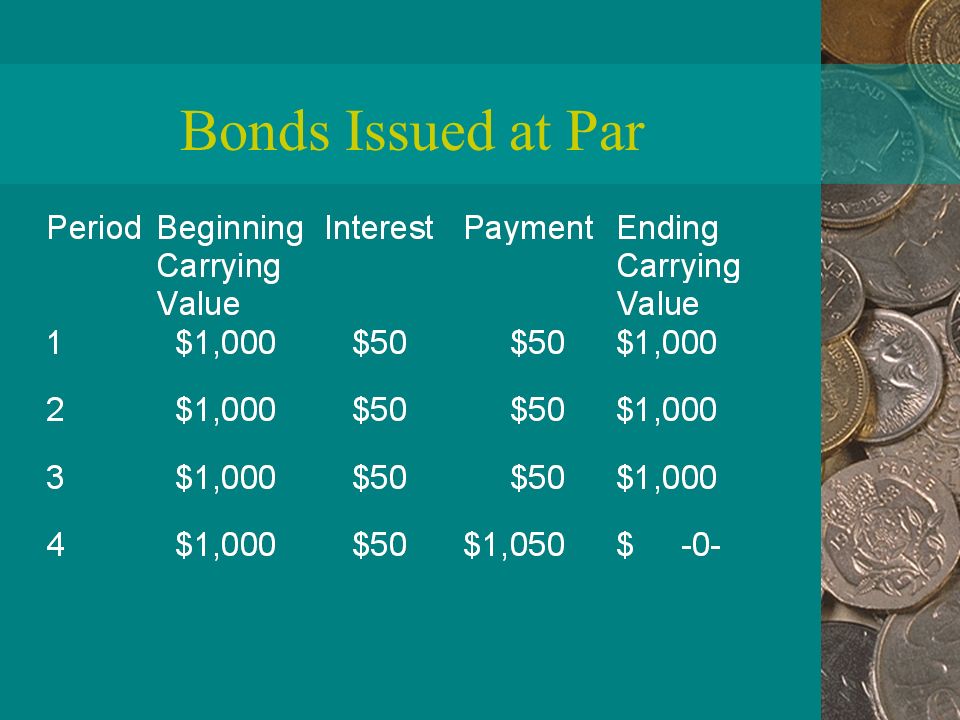

Bonds Issued at Par Bond issued at par are said to be issued at 100. A-Cash1,000 L-Bond Payable1,000 No interest is recognized on the date of issuance, because interest accrues as time passes

20

Bonds Issued at Par Recognition of interest: –Accrue the interest expense and the amount payable to the bondholders Interest expense = Carrying value x Yield rate x Time = $1,000 x 10% x 6/12 = $50 Interest payable = Face Amount x Bond interest rate x Time = $1,000 x 10% x 6/12 = $50

21

Bonds Issued at Par Recognition of interest: SE-Interest Expense50 L-Interest Payable50 –Record the cash payment made L-Interest payable50 A-Cash50

22

Bonds Issued at Par Calculations: –Interest payable amount will be the same in all our interest periods over the life of the bond –Interest expense in each period will depend on the carrying value of the bond at the beginning of each period.

23

Bonds Issued at Par Calculations: Carrying value (ending) = Carrying value )beginning) + Interest expense - Interest payments = $1,000 + 50 - 50 = $1,000 Final payment L-Bond Payable1,000 A-Cash1,000

= Carrying value )beginning) + Interest expense - Interest payments = $1, = $1,000 Final payment L-Bond Payable1,000 A-Cash1,000")

24

Bonds Issued at Par

26

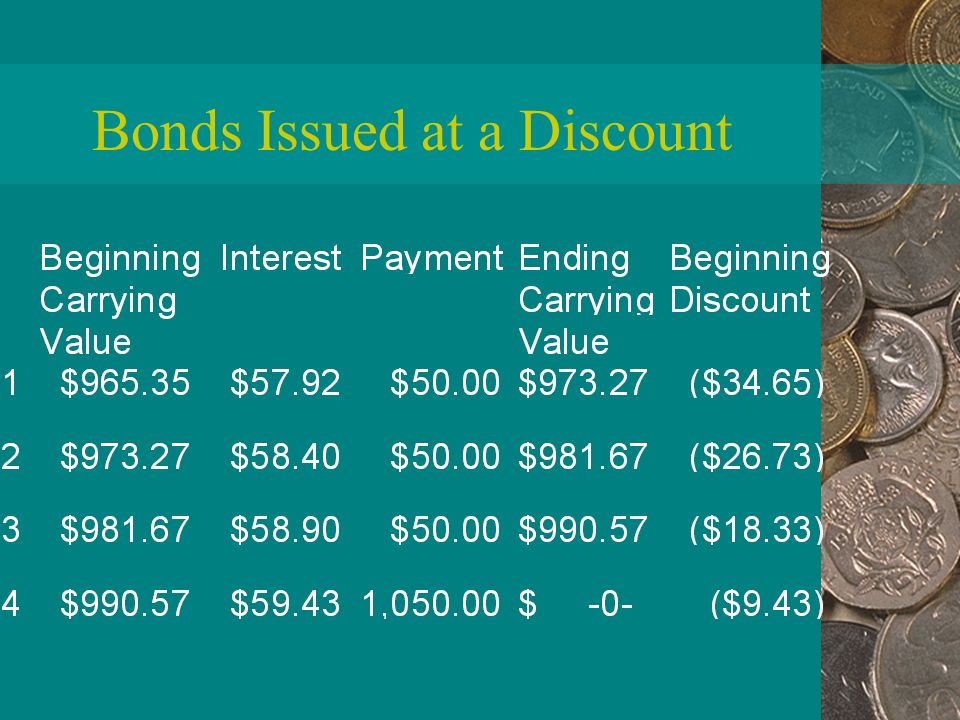

Bonds Issued at a Discount Assume investors demanded a 12 % return The bond would be issued at a price of $965.35 The bond sold at 96.535 A-Cash 965.35 XL-Discount on Bond Payable 34.65 L-Bond Payable 1,000.00

27

Bonds Issued at a Discount Interest entries: Interest expense = Carrying value x Yield rate x Time = $965.35 x 12% x 6/12 = $57.92 Interest payable = Face Amount x Bond interest rate x Time = $1,000 x 10% x 6/12 = $50.00

28

Bonds Issued at a Discount Effective interest method –Difference between interest expense and interest payable decreases (amortizes) the balance of the discount

the balance of the discount")

29

Bonds Issued at a Discount Interest entries: SE-Interest Expense57.92 XL-Discount on Bond Payable 7.92 L-Interest Payable50.00 L-Interest payable50.00 A-Cash50.00

30

Bonds Issued at a Discount Calculations: –Interest payable amount will be the same in all our interest periods over the life of the bond –Interest expense in each period will depend on the carrying value of the bond at the beginning of each period.

31

Bonds Issued at a Discount Calculations: Carrying value (ending) = Carrying value (beginning) + Interest expense - Interest payments = $965.35 + 57.92 - 50.00 = $973.27 Final payment L-Bond Payable1,000.00 A-Cash1,000.00

= Carrying value (beginning) + Interest expense - Interest payments = $ = $ Final payment L-Bond Payable1, A-Cash1,000.00")

32

Bonds Issued at a Discount

34

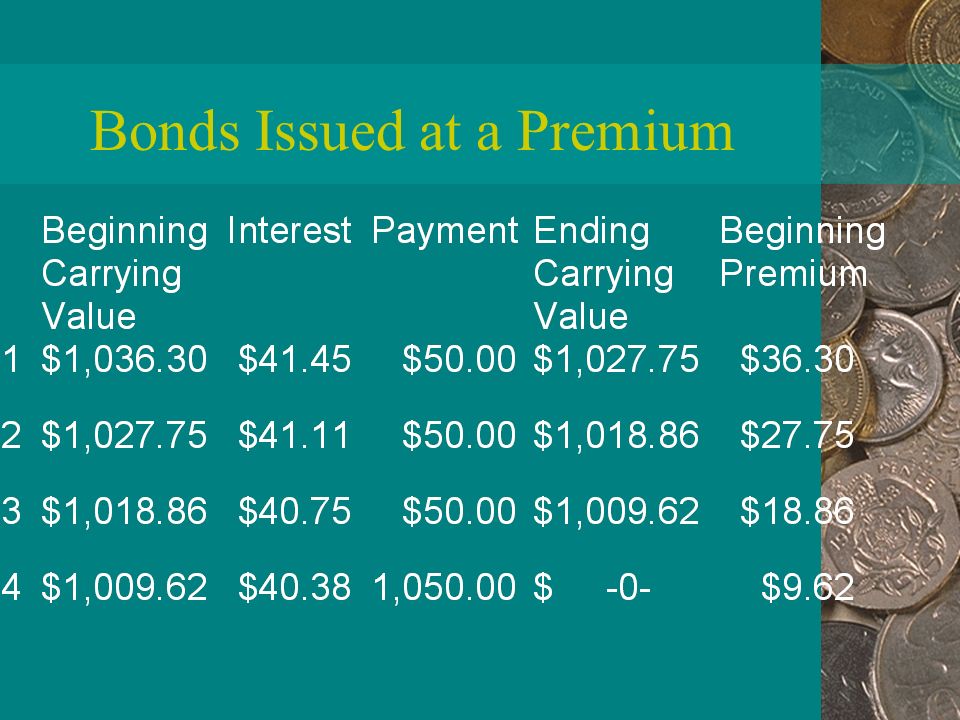

Bonds Issued at a Premium Assume investors demanded 8 % return The bond would be issued at a price of $1,036.30 The bond sold at 103.63 A-Cash 1,036.30 XL-Premium on Bond Payable 36.30 L-Bond Payable 1,000.00

35

Bonds Issued at a Premium Interest entries: Interest expense = Carrying value x Yield rate x Time = $1,036.30 x 8% x 6/12 = $41.45 Interest payable = Face Amount x Bond interest rate x Time = $1,000 x 10% x 6/12 = $50.00

36

Bonds Issued at a Premium Effective interest method –Difference between interest expense and interest payable decreases (amortizes) the balance of the premium

the balance of the premium")

37

Bonds Issued at a Premium Interest entries: SE-Interest Expense41.45 XL-Premium on Bond Payable 8.55 L-Interest Payable50.00 L-Interest payable50.00 A-Cash50.00

38

Bonds Issued at a Premium Calculations: –Interest payable amount will be the same in all our interest periods over the life of the bond –Interest expense in each period will depend on the carrying value of the bond at the beginning of each period.

39

Bonds Issued at a Premium Calculations: Carrying value (ending) = Carrying value (beginning) + Interest expense - Interest payments = $1,036.30 + 41.45 - 50.00 = $1,027.75 Final payment L-Bond Payable1,000.00 A-Cash1,000.00

= Carrying value (beginning) + Interest expense - Interest payments = $1, = $1, Final payment L-Bond Payable1, A-Cash1,000.00")

40

Bonds Issued at a Premium

42

Early Retirement of Debt Retire by buying the bonds on the bond market or by calling the bonds L-Bond Payable1,000.00 L-Premium on Bond Payable 18.86 A-Cash 981.67 SE-Gain on Early Retirement of Bond 37.19

43

Leasing Lease agreement for an asset –A lessor buys the asset and the lessee makes periodic payments in exchange for the use of the asset over the lease term

44

Capital Lease A lease qualifies as a capital lease if one of the following criteria is met: –Title passes at the end of the term –Term = or > useful life of the asset –PV of payments > 90% of the fair value of the asset

45

Operating Lease If none of the capital lease criteria is met, the lease is an operating lease

46

Leases Example: –Asset is leased for 5 years –Quarterly lease payments of $2,000, payable in advance –Title does not pass –No purchase option –Interest rate is 12%

47

Operating Lease If the lease qualifies as an operating lease: SE-Rent expense (Lease expense)2,000 A-Cash2,000

2,000 A-Cash2,000")

48

Capital Lease If the lease qualifies as a capital lease, Both the asset and the obligation would be recorded at the present value of the lease payments The asset is accounted for as if it had been purchased

49

Capital Lease Present value of the lease payments: = First payment + PV of 19 payments at 3% (quarterly rate based on the 12% annual rate) = $2,000 + ($2,000 x 14.32380) = $2,000 = $28,647.60 = $30,647.60

= $2,000 + ($2,000 x ) = $2,000 = $28, = $30,647.60")

50

Capital Lease At date of signing, record the purchase of the asset A-Asset under capital lease 30,647.60 L-Obligation under capital lease 30,647.60

51

Capital Lease On the first day of each quarter, record the payment entry: L-Obligation under capital lease 2,000.00 A-Cash 2,000.00 On the last day of the quarter, record the expense entry: SE-Interest expense 859.43 L-Obligation under capital lease 859.43

52

Capital Lease On the last day of the quarter, record the amortization expense for the asset: SE-Amortization expense 1,532.38 XA-Accumulated amortization (on lease assets) 1,532.38 (Assumes straight-line amortization over 20 quarters)

1, (Assumes straight-line amortization over 20 quarters)")

53

Lease Disclosure In Canada, companies are required to disclose significant future lease payments to be made in total and for each of the next five years

54

Pensions Agreements between employers and employees that provide employees with specified benefits (income) upon retirement Represent an estimated future obligation

upon retirement Represent an estimated future obligation")

55

Pensions Defined contribution plans –Employer agrees to make a set (defined) contribution to a retirement fund for the employee Defined benefit plans –Employee is guaranteed a certain amount of money during each year of retirement

contribution to a retirement fund for the employee Defined benefit plans –Employee is guaranteed a certain amount of money during each year of retirement")

56

Debt/Equity Ratio Total liabilities Total liabilities + Shareholders’ equity =

57

Times Interest Earned Ratio Times interest earned Income before interest and taxes Interest = = Net income + taxes + interest Interest

Similar presentations