Download presentation

Presentation is loading. Please wait.

1

Presentation by Shaun Farrell Secretary & Chief Executive Church of England Pensions Board Pensions and Retirement Housing

2

1927 Clergy Pension Measures Prior to 1927 no pension as of right Pensions Board created Guaranteed Pensions paid at age 70 Funded by (a) Money from Ecclesiastical Commissioners (b) Church Assembly grant (c) Incumbent contribution 3% of stipend

Money from Ecclesiastical Commissioners (b) Church Assembly grant (c) Incumbent contribution 3% of stipend")

3

1954 Clergy Pensions Measure Church Commissioners took on full responsibility for all pension costs Member contributions ceased Church Commissioners took over assets of the fund then £8m Note Church Commissioners pension liabilities 2006 £1.8bn

4

1980 “The Three Aspirations” to improve pensions Pensions = 2/3rds stipend at 65 for 37 years service (£12,400 p.a.) Lump sum = 3x pension (£37,200) Widow(er)s pension = 2/3 rd of member’s pension (£8,266 p.a.) All achieved by late 1980’s BUT

Lump sum = 3x pension (£37,200) Widow(er)s pension = 2/3 rd of member’s pension (£8,266 p.a.) All achieved by late 1980’s BUT")

5

1992 re-evaluation showed that Church Commissioners had:- Taken on far more expenditure commitments than their assets could support so Financial support to dioceses reduced by £45m p.a. 1992 – 1997 Clergy Pensions Measure 1997 established current funded scheme which takes over all pension commitments from 1998 Church Commissioners remain responsible all for pension benefits earned up to 1997

6

Funded clergy scheme 1998 – Scheme set up Initial contribution set at 21.9% of stipend (£2,900 per person - £27m for Church as a whole) 2000 - First actuarial valuation Contribution rate rises to 29.1% (£4,668 per person - £47m for Church)

First actuarial valuation Contribution rate rises to 29.1% (£4,668 per person - £47m for Church)")

7

Funded clergy scheme (cont.) 2003 - Second actuarial valuation Contribution rate rises to 33.8% (£5,925 per person - £57m for Church) End of 2006 – Third actuarial valuation to be carried out

Second actuarial valuation Contribution rate rises to 33.8% (£5,925 per person - £57m for Church) End of 2006 – Third actuarial valuation to be carried out")

8

Long term investment returns are lower Life expectancy increasing Government regulations Why are costs rising?

9

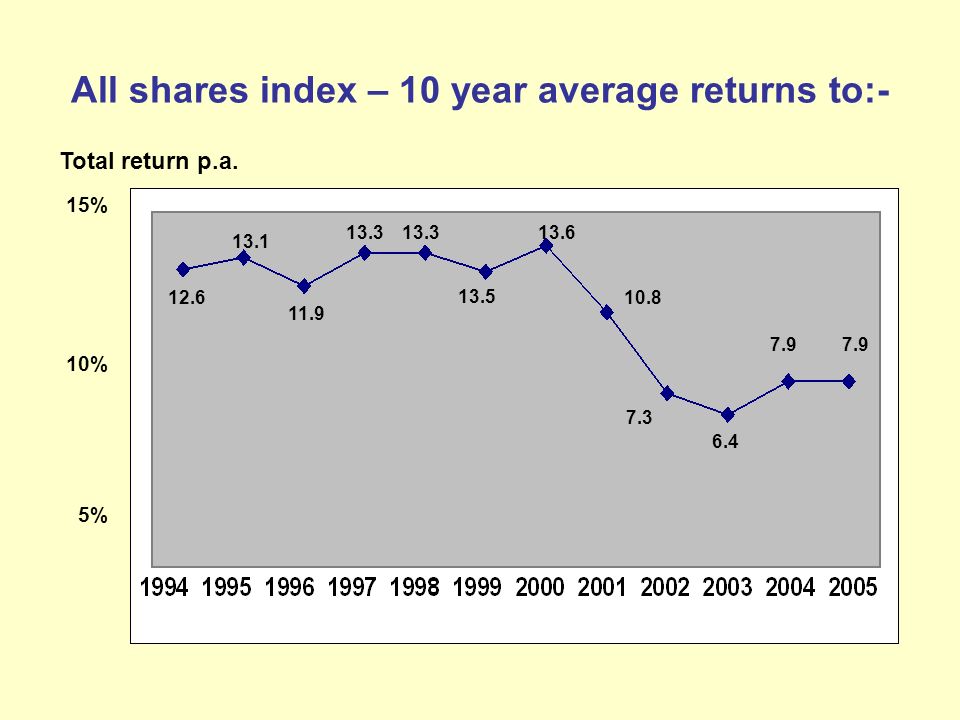

All shares index – 10 year average returns to:- 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 10% 5% 15% Total return p.a. 12.6 13.1 11.9 13.3 13.5 13.6 10.8 7.3 6.4 7.9

10

Average life expectancy at birth Age (Years) (Est) 68.2 70.8 75.4 77.0 84.0 47.3

(Est)")

11

Remaining life expectancy at 65 Years (Est) 13.9 15.2 17.2 18 20?

")

12

Types of Pension Scheme Defined Benefit/Final Salary Level of pension guaranteed Employer must pay whatever is required to meet benefits Funding risk all with ‘Employer’ Defined Contribution/Money Purchase Employer contribution defined Pension depends on how much goes into fund from contributions and investment returns achieved Risk lies with employee

13

Recent Developments Over 70% of all defined benefit schemes are now closed to new members or to all staff Many firms have switched to less expensive pension schemes

14

New Government regulations Designed to make schemes more secure for their members Scheme trustees encouraged to take cautious view about future investment returns (particularly from stocks and shares) Any scheme deficits should be made up over the shortest time possible But – extra caution comes at a cost

Any scheme deficits should be made up over the shortest time possible But – extra caution comes at a cost")

15

Events:- November 2005 : Pension Board’s actuaries provide update on financial position of the pensions scheme Indicates likelihood that costs will rise again (perhaps substantially) when 2006 valuation takes place Archbishops create Task Group to evaluate the situation – group first report published 1 March 2006 second report on 30 June 2006 Both available on website www.cofe.anglican. org

16

Report Findings:- Deficit on the scheme could rise from £91m (2003 valuation) to £170m+ Pension costs would have to rise again significantly if current benefits maintained Could mean annual contribution rising from £6,000 per person to over £8,000

to £170m+ Pension costs would have to rise again significantly if current benefits maintained Could mean annual contribution rising from £6,000 per person to over £8,000")

17

Could mean another £20m p.a. for the Church as a whole Church members unlikely to be able to find all the extra money required Scheme benefits will need to be reviewed Report Findings:-

18

Pensions Board raises pension contribution to 39.8% (£7,188 p.a.) for 2007 on an interim basis Second Task Group report makes some specific recommendations Two consultations carried out (a) dioceses (b) scheme members General Synod approves recommendations in July 2007 Subsequent Steps

for 2007 on an interim basis Second Task Group report makes some specific recommendations Two consultations carried out (a) dioceses (b) scheme members General Synod approves recommendations in July 2007 Subsequent Steps")

19

The changes 1.The ‘defined benefit’ scheme will be retained but modified to make it less expensive 2.Scheme changed as follows for all service from 1 January 2008:- (a)Increase from 37 to 40 years service needed to earn a full pension (b) Pensions, once in payment, to increase each year in line with price inflation (up to a max of 3.5%) not stipends

Increase from 37 to 40 years service needed to earn a full pension (b) Pensions, once in payment, to increase each year in line with price inflation (up to a max of 3.5%) not stipends")

20

Key points All pension rights earned up to the change are protected under law – can’t be taken away Increase to 40 years service only applies to current active clergy (i.e. not those already retired) All service up to change ‘banked’ on basis of 37 year accrual period Clergy can still retire at 65

All service up to change ‘banked’ on basis of 37 year accrual period Clergy can still retire at 65.")

21

Key points (cont) Does not mean all existing clergy having to work an extra 3 years to get full pension Examples 30 years current service – 7 months extra 20 years current service – 1 year 5 months extra 10 years current service – 2 years 3 months extra

Does not mean all existing clergy having to work an extra 3 years to get full pension Examples 30 years current service – 7 months extra 20 years current service – 1 year 5 months extra 10 years current service – 2 years 3 months extra")

22

Key points (cont) Pension benefits ‘earned’ up to 1 January 2008 are increased in line with RPI up to 5% p.a. Pension benefits ‘earned’ after change are increased in line with RPI up to 3.5% p.a.

23

2006 Actuarial Review Pensions Board sets new contribution rate for period 2008 – 2010 at 39.7% i.e. no more than interim rate for 2007 Without the changes approved by General Synod rate would have been 45%+

24

The CHARM Scheme Church’s Housing Assistance for the Retired Ministry Clergy with some capital to invest are granted mortgage loans by the Pensions Board (mostly financed by Commissioners) to enable them to purchase property Those without sufficient resources are able to occupy a property owned by the Board (mostly financed by the Commissioners)

to enable them to purchase property Those without sufficient resources are able to occupy a property owned by the Board (mostly financed by the Commissioners)")

25

The CHARM Scheme (Cont.) On mortgage loans, pensioner pays interest only at 4% p.a. rising each year (in line with index of stipend and price inflation growth) On rented properties, occupiers pay occupation charge to cover interest and other property costs (around £300-400 per month at current rates) Subsidy of £3m p.a. paid into the scheme by dioceses so that no pensioner pays more than 30% of his/her total gross income on housing costs

On rented properties, occupiers pay occupation charge to cover interest and other property costs (around £ per month at current rates) Subsidy of £3m p.a. paid into the scheme by dioceses so that no pensioner pays more than 30% of his/her total gross income on housing costs.")

26

The CHARM Scheme (Cont.) Approx one third of clergy use scheme Mortgage loans are value linked so that the increase in the value of the properties is split between the Commissioners and the pensioners (or his/her estate) in line with the initial capital contributions Maximum loan of £125,000 recently increased to £150,000 Maximum purchase price on ‘rental’ scheme recently increased from £150,000 to £200,000 (£225,000 in SE Counties)

Approx one third of clergy use scheme Mortgage loans are value linked so that the increase in the value of the properties is split between the Commissioners and the pensioners (or his/her estate) in line with the initial capital contributions Maximum loan of £125,000 recently increased to £150,000 Maximum purchase price on ‘rental’ scheme recently increased from £150,000 to £200,000 (£225,000 in SE Counties)")

27

Review of retirement housing Review group set up to look at additional options to assist clergy Due to report back to General Synod in July 2008

Similar presentations

Plan Annuity Defined-Benefit Plan Defined- Contribution Plan Employer- Sponsored Retirement.>")

ALTERNATIVE FOR EMPLOYEES>")