Download presentation

Presentation is loading. Please wait.

1

Copyright © 2005 John Wiley & Sons, Inc. All rights reserved. The Accounting Information System Chapter 3 Prepared by Carol A. Hartley Providence College Principles of Accounting Kimmel Weygandt Kieso

2

Copyright © 2005 John Wiley & Sons, Inc. All rights reserved. Study Objectives 1.Analyze the effect of business transactions on the basic accounting equation. 2.Explain what an account is and how it helps in the recording process. 3.Define debits and credits and explain how they are used to record business transactions. 4.Identify the basic steps in the recording process.

3

Copyright © 2005 John Wiley & Sons, Inc. All rights reserved. Study Objectives 5.Explain what a journal is and how it helps in the recording process. 6.Explain what a ledger is and how it helps in the recording process. 7.Explain what posting is and how it helps in the recording process. 8.Explain the purposes of a trial balance.

4

Copyright © 2005 John Wiley & Sons, Inc. All rights reserved. 5 Accounting Information System The system of collecting and processing transaction data and communicating financial information to interested parties.

5

Copyright © 2005 John Wiley & Sons, Inc. All rights reserved. Chapter Overview

6

Copyright © 2005 John Wiley & Sons, Inc. All rights reserved. # 1 Analyze the Effect of Business Transactions on the Basic Accounting Equation. Assets = Liabilities + Stockholders’ Equity Recall: must always balance!

7

Copyright © 2005 John Wiley & Sons, Inc. All rights reserved. Accounting Transactions Accounting Transactions: economic events that must be recorded in the financial statements.Accounting Transactions: economic events that must be recorded in the financial statements. Event must affect assets, liabilities or stockholders’ equityEvent must affect assets, liabilities or stockholders’ equity

8

Copyright © 2005 John Wiley & Sons, Inc. All rights reserved. Accounting Transactions? Purchase computer Is the financial position (assets, liabilities or stockholders’ equity changed? YES!

9

Copyright © 2005 John Wiley & Sons, Inc. All rights reserved. Accounting Transactions? Discuss product design with customer Is the financial position (assets, liabilities or stockholders’ equity changed? NO!

10

Copyright © 2005 John Wiley & Sons, Inc. All rights reserved. Accounting Transactions? Pay rent Is the financial position (assets, liabilities or stockholders’ equity changed? YES!

11

Copyright © 2005 John Wiley & Sons, Inc. All rights reserved. Transaction Analysis Transaction Analysis:the process of identifying the specific effects of economic events on the accounting equation.Transaction Analysis: the process of identifying the specific effects of economic events on the accounting equation. Each transaction has a dual (double-sided) effectEach transaction has a dual (double-sided) effect

effectEach transaction has a dual (double-sided) effect.")

12

Copyright © 2005 John Wiley & Sons, Inc. All rights reserved. Transaction Analysis If an individual asset is increased, there must be a corresponding:If an individual asset is increased, there must be a corresponding: – Decrease in another asset, or – Increase in a specific liability, or – Increase in stockholders’ equity

13

Copyright © 2005 John Wiley & Sons, Inc. All rights reserved. Transaction Analysis Two or more items can be affectedTwo or more items can be affected Example: purchase computer for $10,000 by paying $6,000 in cash and signing a note for $4,000Example: purchase computer for $10,000 by paying $6,000 in cash and signing a note for $4,000

14

Copyright © 2005 John Wiley & Sons, Inc. All rights reserved. Let’s Practice! Let’s practice transaction analysis with Sierra Corporation...

15

Copyright © 2005 John Wiley & Sons, Inc. All rights reserved. Event 1 – Investment of Cash by Stockholders Oct. 1 - Owner invested $10,000 Cash in business in exchange for $10,000 of Sierra Corporation Common Stock

16

Copyright © 2005 John Wiley & Sons, Inc. All rights reserved. Event 2 – Note Issued in Exchange for Cash Oct. 1 – Sierra issued a 3-month, 12%, $5,000 Note Payable to Castle Bank.

17

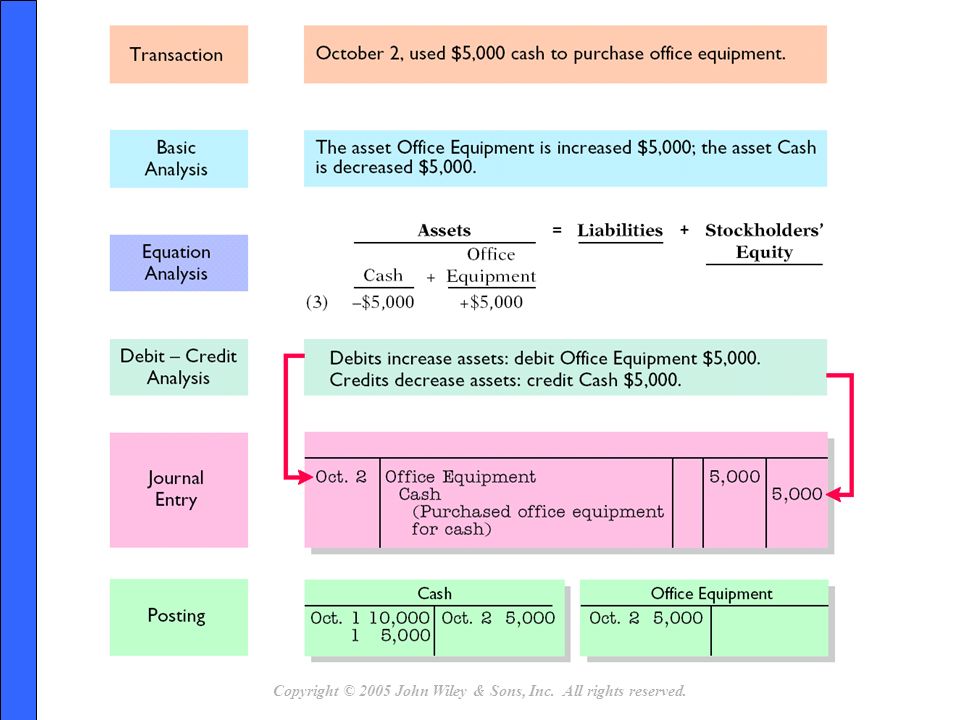

Copyright © 2005 John Wiley & Sons, Inc. All rights reserved. Event 3 – Purchase of Office Equipment for Cash Oct. 2 – Sierra acquired office equipment by paying $5,000 cash to Superior Sales Co.

18

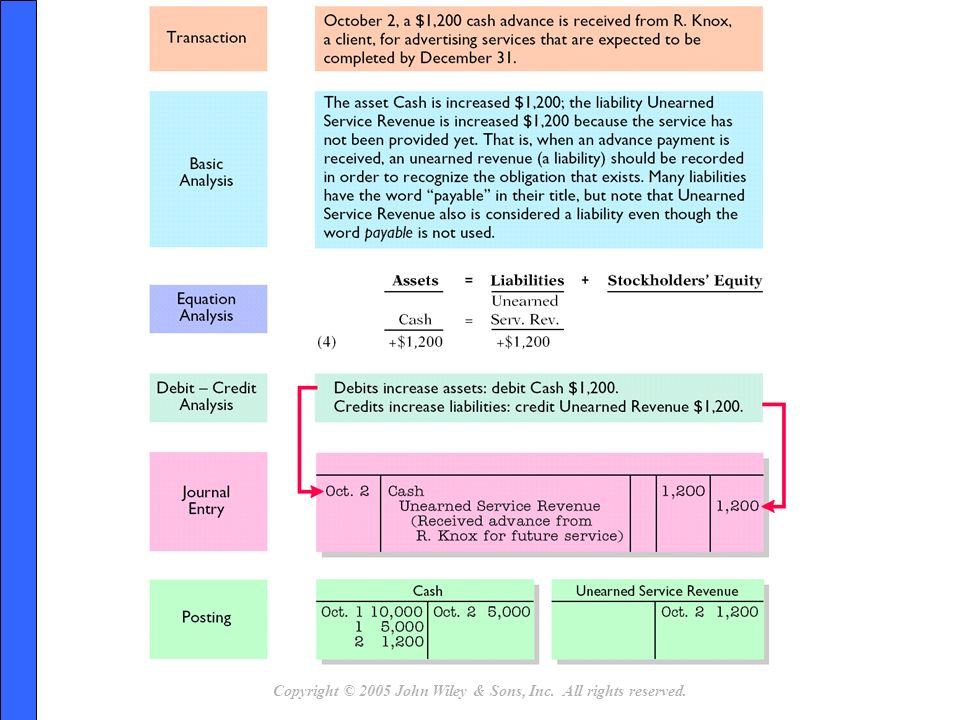

Copyright © 2005 John Wiley & Sons, Inc. All rights reserved. Event 4 – Receipt of Cash in Advance from Customer Oct. 2 – Sierra received a $1,200 cash advance from R. Knox, a client.

19

Copyright © 2005 John Wiley & Sons, Inc. All rights reserved. Event 5 – Services Rendered for Cash Oct. 3 – Sierra received $10,000 in cash from Copa Co. for advertising services performed

20

Copyright © 2005 John Wiley & Sons, Inc. All rights reserved. Event 5 – Services Rendered, WHAT IF these were performed “on account”? Later, when $10,000 is collected from customer…

21

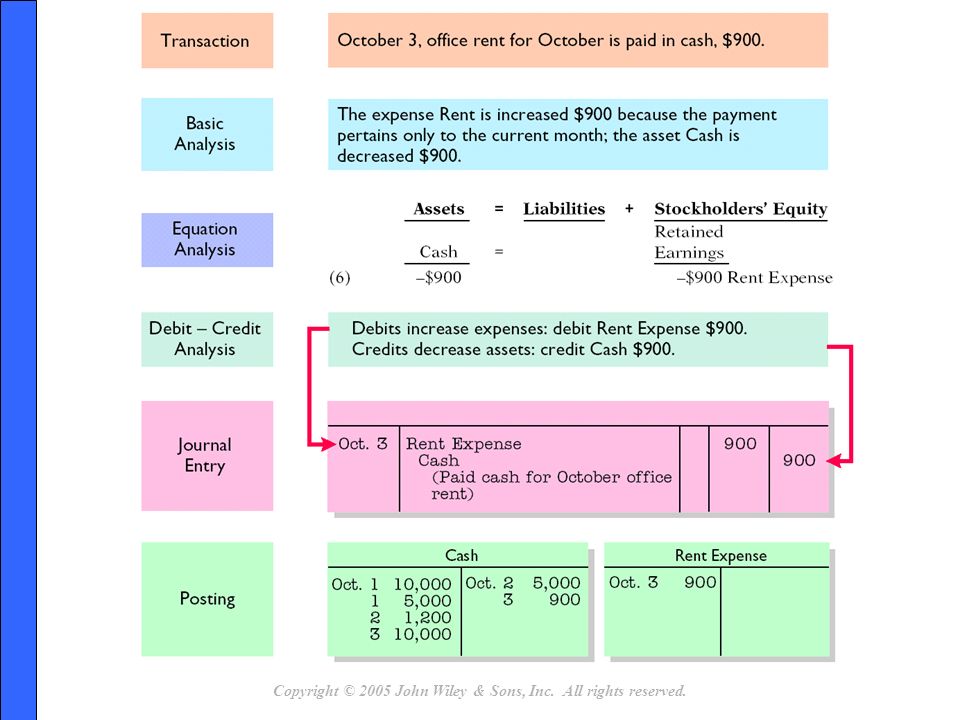

Copyright © 2005 John Wiley & Sons, Inc. All rights reserved. Event 6 – Payment of Rent Oct. 3 – Sierra paid its office rent for the month of October in cash, $900.

22

Copyright © 2005 John Wiley & Sons, Inc. All rights reserved. Event 7 – Purchase of Insurance Policy with Cash Oct. 4 – Sierra paid $600 for a one-year insurance policy that will expire next year on Sept. 30.

23

Copyright © 2005 John Wiley & Sons, Inc. All rights reserved. Event 8 – Purchase of Supplies on Credit Oct. 5 – Sierra purchases a three-month supply of advertising materials on account from Aero Supply for $2,500.

24

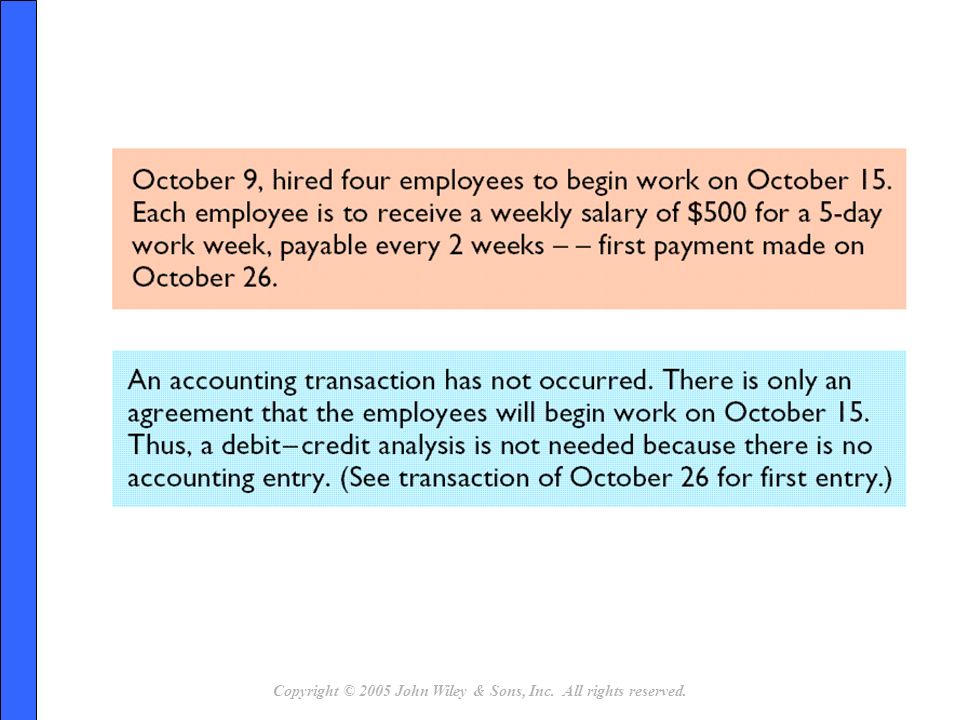

Copyright © 2005 John Wiley & Sons, Inc. All rights reserved. Event 9 – Hiring of New Employees Oct. 9 – Sierra hired four new employees to begin work on Oct. 15. Accounting transaction has NOT occurred!

25

Copyright © 2005 John Wiley & Sons, Inc. All rights reserved. Event 10 – Payment of Dividend Oct. 20 – Sierra paid a $500 dividend.

26

Copyright © 2005 John Wiley & Sons, Inc. All rights reserved. Event 11 – Payment of Cash for Employee Salaries Oct. 26 – Paid employees working two weeks, who have earned $4,000 in salaries.

27

Copyright © 2005 John Wiley & Sons, Inc. All rights reserved. Summary of Transactions Assets = Liabilities + Equity

28

Copyright © 2005 John Wiley & Sons, Inc. All rights reserved. # 2 Explain what an account is and how it helps in the recording process. Account: individual accounting record of increases and decreases in a specific Asset, Liability, or Stockholders’ Equity item. Account: individual accounting record of increases and decreases in a specific Asset, Liability, or Stockholders’ Equity item.

29

Copyright © 2005 John Wiley & Sons, Inc. All rights reserved. Account Consists of three parts:Consists of three parts: –Title of the account –Left side, the debit side, Dr. –Right side, the credit side, Cr. We call this the T - accountWe call this the T - account

30

Copyright © 2005 John Wiley & Sons, Inc. All rights reserved. The T Account

31

Copyright © 2005 John Wiley & Sons, Inc. All rights reserved. # 3 Define debits and credits and explain how they are used to record business transactions. Recall Debit means left Recall Debit means left thus, entry on left side is debiting thus, entry on left side is debiting Recall Credit means right Recall Credit means right thus, entry on right side is crediting thus, entry on right side is crediting

32

Copyright © 2005 John Wiley & Sons, Inc. All rights reserved. Examples

33

52 Total the Balances on T-Account Debit Title of Account Credit Total Debits > Credits, then you have a Debit Balance!

34

Copyright © 2005 John Wiley & Sons, Inc. All rights reserved. 52 Total the Balances on T-Account Debit Title of Account Credit Total Credits > Debits, then you have a Credit Balance!

35

Copyright © 2005 John Wiley & Sons, Inc. All rights reserved. Normal Balances for Assets and Liabilities

36

Copyright © 2005 John Wiley & Sons, Inc. All rights reserved. Normal Balances for Stockholders’ Equity

37

Copyright © 2005 John Wiley & Sons, Inc. All rights reserved. Normal Balances for Expenses and Revenues

38

Copyright © 2005 John Wiley & Sons, Inc. All rights reserved. 52 Debits Increase assets and expenses Decrease liabilities, common stock, revenues

39

Copyright © 2005 John Wiley & Sons, Inc. All rights reserved. 53 Credits Decrease assets and expenses Increase liabilities, common stock, revenues

40

Copyright © 2005 John Wiley & Sons, Inc. All rights reserved. Expansion of Basic Equation

41

Copyright © 2005 John Wiley & Sons, Inc. All rights reserved. Let’s Review What is the normal balance for the following accounts? Cash? Service Revenue? Accounts Receivable? Accounts Payable? Common Stock? Salaries Expense? Debit Credit Debit Credit Credit Debit

42

Copyright © 2005 John Wiley & Sons, Inc. All rights reserved. Let’s Review What is the normal balance for the following accounts? Dividends? Service Revenue? Taxes Payable? Building? Prepaid Insurance? Rent Expense? Debit Debit Credit Credit Debit Debit

43

Copyright © 2005 John Wiley & Sons, Inc. All rights reserved. 52 Let’s Review Using Sierra’s Transactions Oct. 1 - Owner invested $10,000 Cash in business in exchange for $10,000 of Sierra Corporation Common Stock Cash Common Stock 10,00010,000

44

Copyright © 2005 John Wiley & Sons, Inc. All rights reserved. 52 Let’s Review Using Sierra’s Transactions Cash Note Payable 5,0005,000 Oct. 1 – Sierra issued a 3-month, 12%, $5,000 Note Payable to Castle Bank.

45

Copyright © 2005 John Wiley & Sons, Inc. All rights reserved. 52 Let’s Review Using Sierra’s Transactions Office Equipment Cash 5,0005,000 Oct. 2 – Sierra acquired office equipment by paying $5,000 cash to Superior Sales Co. 5,000 10,000

46

Copyright © 2005 John Wiley & Sons, Inc. All rights reserved. # 4 Identify the Basic Steps in the Recording Process. 1.Analyze 2.Journalize 3.Post

47

Copyright © 2005 John Wiley & Sons, Inc. All rights reserved. Recording Process Step 1 Analyze each transaction and effect on accounts

48

Copyright © 2005 John Wiley & Sons, Inc. All rights reserved. Recording Process Step 2 Enter transaction information in a journal, a process called journalizing

49

Copyright © 2005 John Wiley & Sons, Inc. All rights reserved. Recording Process Step 3 Transfer (post) the journal information to the appropriate accounts in the ledger

the journal information to the appropriate accounts in the ledger.")

50

Copyright © 2005 John Wiley & Sons, Inc. All rights reserved. # 5 Explain what a journal is and how it helps in the recording process. An accounting record where the transactions are initially recorded in chronological order. An accounting record where the transactions are initially recorded in chronological order. For each transaction journal shows the debit and credit For each transaction journal shows the debit and credit

51

Copyright © 2005 John Wiley & Sons, Inc. All rights reserved. 58 Journals Help Recording Process Discloses in one place the complete effect of a transactionDiscloses in one place the complete effect of a transaction Provides a chronological record of transactionsProvides a chronological record of transactions Helps prevent or locate errors because debit and credit amounts can be readily comparedHelps prevent or locate errors because debit and credit amounts can be readily compared

52

Copyright © 2005 John Wiley & Sons, Inc. All rights reserved. 58 Computerized Systems Journals are kept as data filesJournals are kept as data files Accounts are recorded in computer databaseAccounts are recorded in computer database

53

Copyright © 2005 John Wiley & Sons, Inc. All rights reserved. Journalizing Complete entry consists of:Complete entry consists of: –Date of transaction –Accounts titles and dollar amounts to be debited and credited –Brief explanation Let’s use the first three Sierra transactions...Let’s use the first three Sierra transactions...

54

DateDebit Credit GENERAL JOURNAL Account Titles and Explanations 2005 Oct. 1 Cash 10,000 Common Stock 10,000 (Invested cash in business) 1 Cash 5,000 Notes Payable 5,000 (Issued 3-month, 12% note payable for cash) 2 Office Equipment 5,000 Cash 5,000 (Purchased office equipment for cash)

1 Cash 5,000 Notes Payable 5,000 (Issued 3-month, 12% note payable for cash) 2 Office Equipment 5,000 Cash 5,000 (Purchased office equipment for cash).")

55

Copyright © 2005 John Wiley & Sons, Inc. All rights reserved. # 6 Explain what a ledger is and how it helps in the recording process. Ledger is the entire group of accounts maintained by a company Ledger is the entire group of accounts maintained by a company Keeps all the information about current account balances and changes in specific account balancesKeeps all the information about current account balances and changes in specific account balances Ledger contains all the asset, liability, & stockholders’ equity accounts Ledger contains all the asset, liability, & stockholders’ equity accounts

56

Copyright © 2005 John Wiley & Sons, Inc. All rights reserved. General Ledger Most businesses computerize these files!

57

Copyright © 2005 John Wiley & Sons, Inc. All rights reserved. Chart of Accounts List of company accountsList of company accounts Number and type used depends upon size and complexity of businessNumber and type used depends upon size and complexity of business Small business might use 20 to 30 accountsSmall business might use 20 to 30 accounts Large business could use thousands worldwideLarge business could use thousands worldwide Computerized systems assign number sequence to each unique account and groupComputerized systems assign number sequence to each unique account and group

58

Copyright © 2005 John Wiley & Sons, Inc. All rights reserved. Chart of Accounts Note: In the Sierra examples we used the red accounts, in future chapters we will cover others in black

59

Copyright © 2005 John Wiley & Sons, Inc. All rights reserved. # 7 Explain what posting is and how it helps in the recording process. Procedure of transferring journal entries to ledger is called posting Procedure of transferring journal entries to ledger is called posting

60

Copyright © 2005 John Wiley & Sons, Inc. All rights reserved. Recall: Basic Steps in the Recording Process. Recall: Basic Steps in the Recording Process. 1.Analyze the transaction, identify the type of accounts involved? 2.Journalize, debit or credit what? 3.Post Let’s use some of Sierra’s data to demonstrate the recording process...

61

Copyright © 2005 John Wiley & Sons, Inc. All rights reserved.

62

Posting in Data File or Paper Files GENERAL JOURNAL Account Titles and Explanations 2005 Oct. 1 Cash 10,000 Common Stock 10,000 Balance Acct 1010 Account CASH Date Acct 3010 Account COMMON STOCK Dat e Balance debit credit debit credit re f Oct 1 GJ 1 10,000

63

Copyright © 2005 John Wiley & Sons, Inc. All rights reserved.

73

# 8 Explain the purposes of a trial balance. Lists all the accounts and their balances at a given time. Lists all the accounts and their balances at a given time. Proves mathematical equality of debits and credits after posting. Proves mathematical equality of debits and credits after posting. Useful in the preparation of financial statements. Useful in the preparation of financial statements. Does not tell you ledger is correct! Does not tell you ledger is correct!

74

Sierra Corporation Trial Balance October 31, 2005 Debit Credit Cash $15,200 Advertising Supplies 2,500 Prepaid Insurance 600 Office Equipment 5,000 Notes Payable $ 5,000 Accounts Payable 2,500 Unearned Service Revenue 1,200 Common Stock 10,000 Dividends 500 Service Revenue 10,000 Salaries Expense 4,000 Rent Expense 900 $28,700 $28,700

75

Copyright © 2005 John Wiley & Sons, Inc. All rights reserved. Copyright © 2005 John Wiley & Sons, Inc. All rights reserved. Reproduction or translation of this work beyond that named in Section 117 of the United States Copyright Act without the express written consent of the copyright owner is unlawful. Request for further information should be addressed to the Permissions Department, John Wiley & Sons, Inc. The purchaser may make back-up copies for his/her own use only and not for distribution or resale. The Publisher assumes no responsibility for errors, omissions, or damages, caused by the use of these programs or from the use of the information contained herein.

Similar presentations