Download presentation

Presentation is loading. Please wait.

1

Delivery mechanisms for cash and voucher programs MBRRR Training Session 5.1

2

Part I: Delivery mechanisms for cash transfers

3

Payment mechanisms in cash transfer programs DELIVERY AGENTS Aid agencies Banks Post offices Mobile phone companies Micro-finance companies Security companies Local traders (hawala) DELIVERY METHODS Direct delivery (“cash in envelopes”) Delivery through banking systems Smart cards Debit cards Mobile phones

DELIVERY METHODS Direct delivery ( cash in envelopes ) Delivery through banking systems Smart cards Debit cards Mobile phones")

4

Safe place for transfer (post office, school, meeting space, etc.) BeneficiariesCRS/Partner Cash transfers Beneficiary use of transfers Fee for service Food/ School fees Direct cash distributions Livelihoods Debt repayment

BeneficiariesCRS/Partner Cash transfers Beneficiary use of transfers Fee for service Food/ School fees Direct cash distributions Livelihoods Debt repayment")

5

Beneficiaries Bank CRS/ Partner Cash transfers Beneficiary use of transfers Fee for service Food/ School fees Cash payments using banks Livelihoods Debt repayment

6

Safe place for transfer Beneficiaries Trader/ Hawala agent CRS/ Partner Cash transfers Beneficiary use of transfers Fee for service Food/ School fees Cash payments using third- party distribution agents Livelihoods Debt repayment

7

Safe place for transfer Beneficiaries “MPESA” agent/ATM CRS/ Partner Cash transfers Beneficiary use of transfers Fee for service Electronic transfer (SMS) Food/ School fees Cash payments using mobile phones or debit cards Livelihoods Debt repayment

Food/ School fees Cash payments using mobile phones or debit cards Livelihoods Debt repayment")

8

Direct delivery to recipients STRENGTHS Can be delivered low-cost Can be delivered quickly Simple; does not require new skills on part of beneficiaries Not limited by presence of banks or other financial infrastructure Beneficiaries do not require bank accounts or assets (phones) Flexible if beneficiaries move locations WEAKNESSES Security and corruption risks Often labour intensive for staff Possibly long waiting lines at distributions Fixed distribution date and times Multiple distributions for frequent transfers

Flexible if beneficiaries move locations WEAKNESSES Security and corruption risks Often labour intensive for staff Possibly long waiting lines at distributions Fixed distribution date and times Multiple distributions for frequent transfers")

9

Delivery through bank accounts STRENGTHS Reduced workload for agency staff Corruption and security risks may be reduced if institutions have strong control systems Flexibility and convenience for recipients who can choose when to withdraw cash and avoid queues Access to financial system for previously unbanked recipients WEAKNESSES Timed needed to negotiate roles, contractual terms and establish systems Reluctance to set up accounts for small amounts of money Bank charges may be expensive Recipients may be unfamiliar with financial institutions and have some fears in dealing with them Possible exclusion of people without necessary documentation, e.g. women, IDPs, and children

10

Delivery through banks without accounts (checks) STRENGTHS Same as bank accounts but with less delays caused by having to verify transfers WEAKNESSES As bank accounts are not opened recipients do not gain access to the banking system

STRENGTHS Same as bank accounts but with less delays caused by having to verify transfers WEAKNESSES As bank accounts are not opened recipients do not gain access to the banking system")

11

Delivery by sub-contracted parties (traders, remittance companies) STRENGTHS Sub-contracted parties accept some responsibility for loss Security risks for agency reduced Remittance companies may have greater access than agencies to insecure areas Recipients may be familiar with these types of systems Flexibility and access – these systems may be near to where recipients live and may offer greater flexibility in receiving their cash WEAKNESSES The system may require greater monitoring for auditing purposes Transaction fees may be costly Reduced control over distribution time frame Credibility could be at risk if the transfer company cannot provide the money to the agreed time schedule Recipients may be more removed from aid agency and so less able to complain if things go wrong Risk of collusion between staff and traders/agents

STRENGTHS Sub-contracted parties accept some responsibility for loss Security risks for agency reduced Remittance companies may have greater access than agencies to insecure areas Recipients may be familiar with these types of systems Flexibility and access – these systems may be near to where recipients live and may offer greater flexibility in receiving their cash WEAKNESSES The system may require greater monitoring for auditing purposes Transaction fees may be costly Reduced control over distribution time frame Credibility could be at risk if the transfer company cannot provide the money to the agreed time schedule Recipients may be more removed from aid agency and so less able to complain if things go wrong Risk of collusion between staff and traders/agents")

12

Delivery via pre-paid cards or mobile phones STRENGTHS As with banks possible reduced corruption and security risks, reduced workload for agency staff, greater flexibility for recipients Greater flexibility in where cash can be collected (e.g. mobile points of sale, local traders) A mobile phone (individual or communal) can be provided at low cost to those who don’t already have them Automatic “topping up” of transfer values WEAKNESSES Systems may take time and be complex to establish Risks of agents or branches running out of money Costs and risks of new technology such as Smart Cards Requires financial infrastructure (ATMS) or Point of Service (POS) devices Recipients may be unfamiliar with new systems Form of identity may be required depending on local regulations which may exclude some people

A mobile phone (individual or communal) can be provided at low cost to those who don’t already have them Automatic topping up of transfer values WEAKNESSES Systems may take time and be complex to establish Risks of agents or branches running out of money Costs and risks of new technology such as Smart Cards Requires financial infrastructure (ATMS) or Point of Service (POS) devices Recipients may be unfamiliar with new systems Form of identity may be required depending on local regulations which may exclude some people.")

13

Group work In your country groups, complete the Delivery Mechanism Assessment matrix Identify all the feasible delivery mechanisms for a likely shock in your country Make a recommendation on an appropriate cash delivery mechanism for the context in which you are working

14

Part II: Payment mechanisms for voucher programs

15

Vendors at fair Beneficiaries CRS/Partner Flow of stocks Vouchers Cash Payment scheme for fairs

16

Shop-based vendors Beneficiaries CRS/Partner Flow of stocks Vouchers Checks/deposit Payment scheme for shops

17

Large Traders Small traders Beneficiaries CRS/Partner Flow of stocks Vouchers Cash Checks/deposit Payment scheme in weekly markets

18

Issues to consider Frequency of payment – Capacity of vendors to restock – Capacity of vendors to maintain credit – Staff capacity Method of payment – Cash – Checks – Bank deposit – Mobile transfers – Sub-contracted third parties (traders, microfinance organizations) How to pay small vendors – be creative! – Relationships with larger vendors – Payment to groups

19

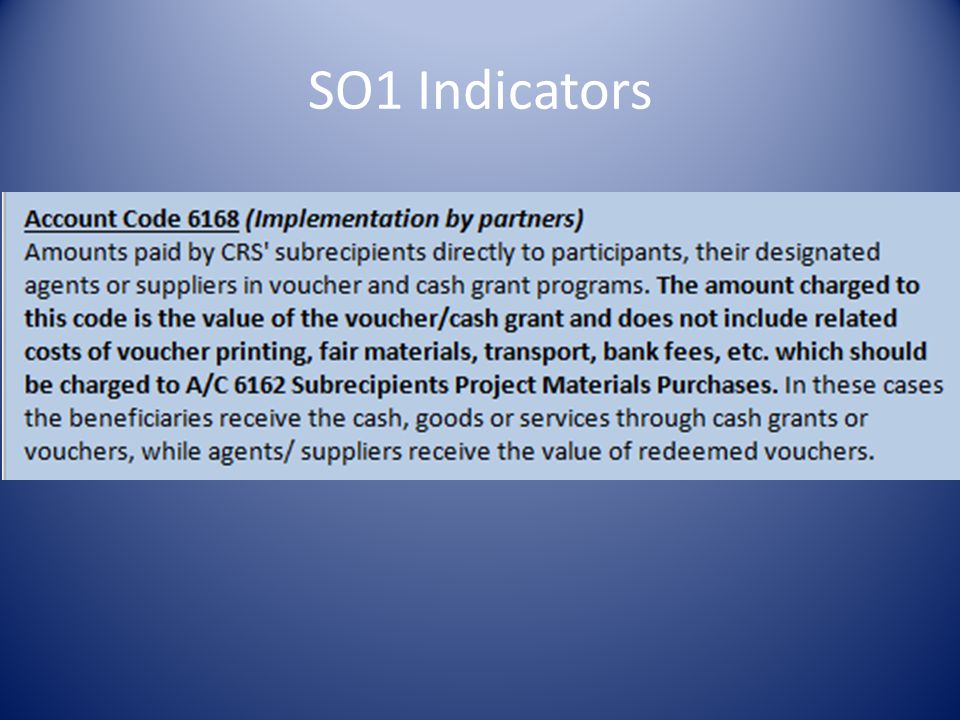

SO1 Indicators

21

Tools CRS cash and voucher SOPs CRS account codes CaLP “Delivering Money”

22

Key Messages Creativity may be necessary in designing good payment delivery mechanisms, especially in working with small traders Security is often a key concern, and the modality should be carefully considered – this doesn’t mean cash is the most dangerous. Financial audits are a key concern, but CRS has MQ SOPs to facilitate this.

Similar presentations

Advantages.>")

End time: ____ Please set phones to silent ring and answer outside of the room.>")

An Introduction Nick Hughes November 2005.>")