Download presentation

1

Chapter 8 Introduction

2

What is a Work Sheet? Is an informal business paper used to organize and plan the information for the financial statements Usually done in PENCIL Done on columnar bookkeeping paper

3

Why? Why use the Work Sheet?

Accountants prefer to use the work sheet, rather than rely solely on the trial balance sheet Organizes the accounts for a specific time period

4

Work Sheet 8 columns are used in the work sheet to allow accounts to make any adjustments required by certain GAAPs (look at in chapter 9) For this chapter we will be introduced to 6 columns

5

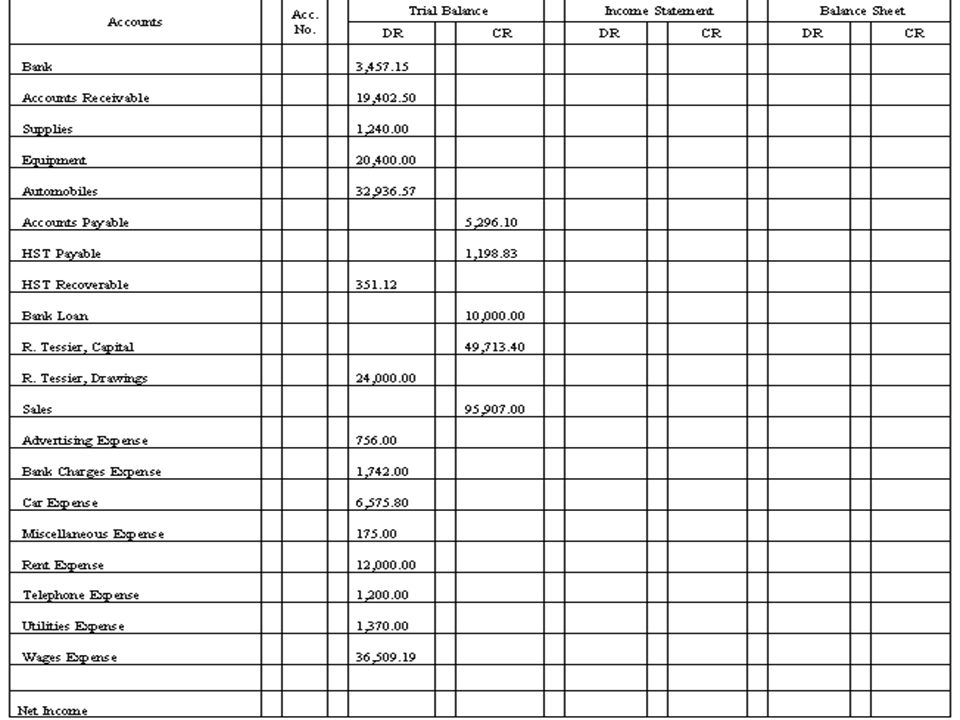

Example of a Work Sheet ALL ACOUNTS 6 Columns

6

Any changes? No longer have debtors’ names associated with Accounts Receivable No longer have creditors’ names associated with Accounts Payable

7

Control Accounts Accounts Receivable Control Account: the sum of the balances of all individual Accounts Receivable Accounts Payable Control Account: the sum of the balances of all individual Accounts Payable More efficient for preparing work sheets and provides a more efficient presentation on the balance sheet (kept in separate records, look at in chapter 11)

")

8

Steps in Preparation of a work sheet

Write the headings on columnar paper Company Name Vulcan Rentals Work Sheet Year Ended December 31, 2012 Business Form Period OR May Look Like this: Vulcan Rentalls Work Sheet Year Ended December 31, 2012

9

2. Record the trial balance on the work sheet

Enter ALL accounts with their balances in the first two columns (trial balance) Trial balance MUST balance before moving on DR = CR

Trial balance MUST balance before moving on. DR = CR.")

12

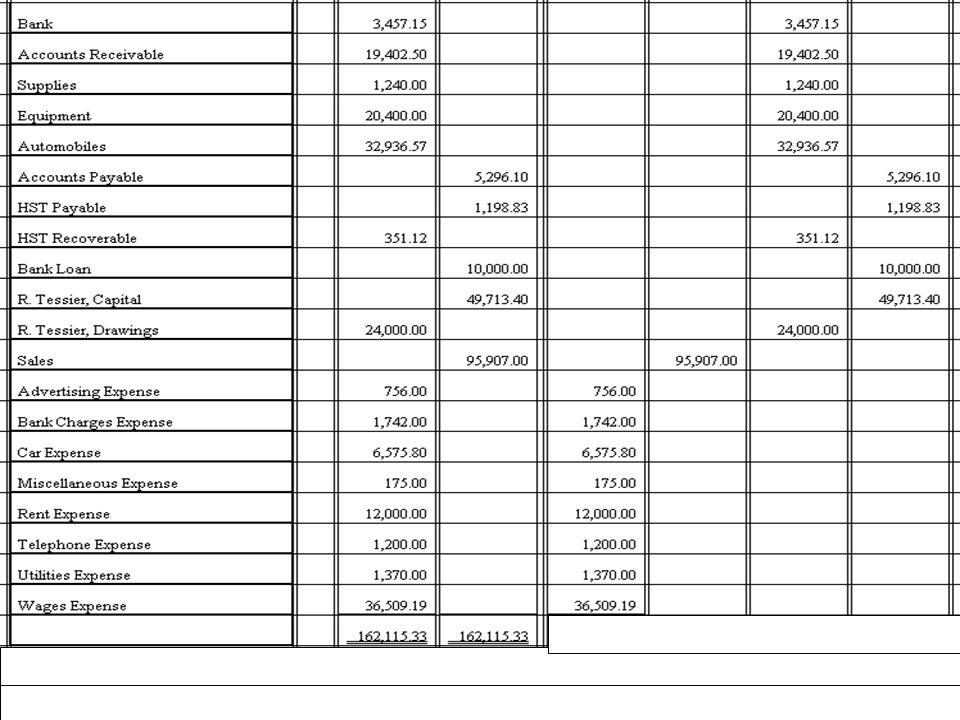

3. Extend each of the amounts

Extend each of the amounts from the trial balance columns into one of the four columns to the right Income Statement revenue & expenses (net income, net loss) Balance sheet assets, liabilities, capital & drawings **Be sure that each account balance is transferred only once & that no item is missing

Balance sheet assets, liabilities, capital & drawings. **Be sure that each account balance is transferred only once & that no item is missing.")

13

Expanding trial balance #s to correct financial statement

14

Total the four right-hand money columns

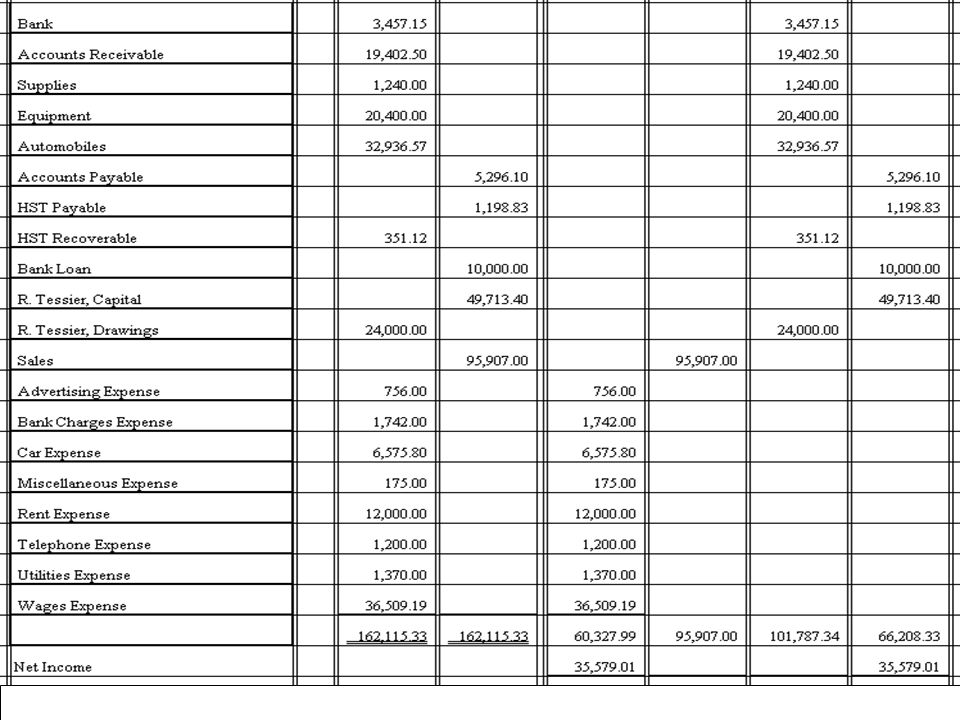

4. Balance the Work Sheet Total the four right-hand money columns

16

4. Balance the Work Sheet b) Make sure the difference between Income Statement columns is equal to the difference between the Balance sheet columns. Known as the BALANCING FIGURE

18

4. Balance the Work Sheet C) The work sheet MUST balance. If two figures do not agree, then one or more errors have been made ***YOU MAY NOT PROCEED to the preparation of the financial statements until the errors have been found & corrected!!!!

19

5. The balancing figures The work sheet tells the amount of the net income or net loss for the accounting period Net income = Revenue (credit column) > (greater than) Expense (debit column) Net Loss = Expense > (greater than) Revenue

> (greater than) Expense (debit column) Net Loss = Expense > (greater than) Revenue.")

20

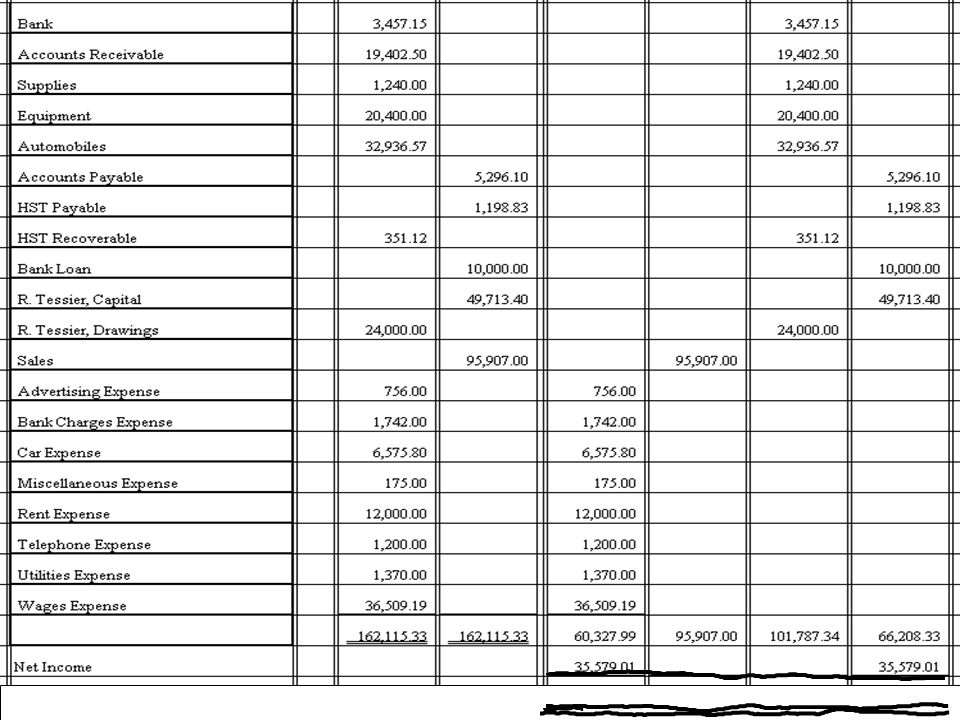

When there is a profit the balancing figure is placed in the 2 outside columns. When there is a loss, the balancing figure is placed in the 2 inside columns

21

Rule off the work sheet By drawing a single line under the net income totals and a DOUBLE line after the final four totals. USE A RULER!!!

23

The Accounting Cycle Step 1 Transaction Occurs (source documents)

Step 2 Journal Entry (daily record of transactions) Step 3 Posting to General Ledger (update all accounts) Step 4 Trial balance (DR=CR) Step 5 Worksheet (informal working doc, calc n/i, n/l) Step 6 Financial Statements (Income Statement & Balance sheet)

Step 3 Posting to General Ledger. (update all accounts) Step 4 Trial balance. (DR=CR) Step 5 Worksheet. (informal working doc, calc n/i, n/l) Step 6 Financial Statements. (Income Statement & Balance sheet)")

–Done 2.Post (To Ledger Accounts – which are also known as.>")