Download presentation

2

Learning Objectives 12.1 Describe the predominant economic systems and how they impact business. 12.2 Define scarcity and identify the problems posed by limited resources. 12.3 Explain how the economic concepts of supply and demand influence prices. 12.4 Identify the types of competition that exist within the free markets. 12.5 Understand the key economic indicators that determine how the economy is doing. 12.6 Describe how fiscal and monetary policy control the economy.

3

What are Economic Systems?

4

Economic Systems influence the creation of wealth, the quality of life, and the growth of business around the world. Popular economic systems of the world include: Capitalism Socialism Communism

5

Capitalism Capitalism – An economic system in which all or most of the factors of production and distribution are privately owned and operated for profit. It is the economic system of the US, England, Australia, Canada, and other industrialized nations. Capitalism creates a free market. Free Market – a system in which decisions about what to produce and in what quantities are made by the market. Capitalist systems grant people the right to own private property and live and work where they please.

6

Socialism Socialism – An economic system in which most businesses are owned by the government so profits can be evenly distributed among all people. It is the economic system of many countries in Europe (Sweden, Finland, Belgium) and Africa. Entrepreneurs may run small business, but are discouraged by a high level of taxation. Taxation in a socialist country helps to fund government programs for education, health care, retirement benefits, unemployment, and other social services. Workers in socialist countries tend to get longer vacations and work fewer hours, which accounts for slower growth. Businesses may also lack innovation, as there is no incentive or reward for creativity.

and Africa. Entrepreneurs may run small business, but are discouraged by a high level of taxation. Taxation in a socialist country helps to fund government programs for education, health care, retirement benefits, unemployment, and other social services. Workers in socialist countries tend to get longer vacations and work fewer hours, which accounts for slower growth. Businesses may also lack innovation, as there is no incentive or reward for creativity.")

7

Communism Communism – An economic system in which the government owns most businesses and limits the freedom of choice of its people. It is the economic system of North Korea, Vietnam, Cuba and part of the Soviet Union. The prices of goods and services are set by the government, thus, they do not reflect consumer choice. Shortages often occur and needs go unmet, as prices are not kept in line with supply and demand. Communism offers no incentive to work, so business growth is marginal.

8

What are Mixed Economies?

9

Mixed Economies are economic systems in which some allocation of resources is made by the market and some is made by the government. Mixed economies combine elements of capitalism (free market) with those of socialism and communism (government control) The trend is current capitalist countries are moving more toward socialism and socialist countries moving more toward capitalism.

with those of socialism and communism (government control) The trend is current capitalist countries are moving more toward socialism and socialist countries moving more toward capitalism.")

10

What is Economics?

11

Economics is the study of how individuals and society choose to use scarce resources to produce goods and services and distribute them for consumption. Economics has both a macro and micro focus Macroeconomics – the part of economics study that looks at the behavior of people and organizations in particular markets. Microeconomics – the part of economics study that looks at the behavior of people and organizations in particular markets.

12

What is Scarcity?

13

Scarcity is a basic economic problem that arises because people have unlimited wants, but resources are limited. Businesses often times various economic decisions must be made to allocate resources efficiently, sometimes referred to as opportunity costs. Opportunity Cost – refers to what you give up (your next best choice) in order to do or get something else (your chosen decision) Businesses can address scarcity through resource development. Resource Development – increasing resources or creating conditions that will make better use of resources.

in order to do or get something else (your chosen decision) Businesses can address scarcity through resource development. Resource Development – increasing resources or creating conditions that will make better use of resources.")

14

Supply and Demand

15

Market price is set when the quantity supplied and the quantity demanded reaches and equilibrium point. Supply – the quantity of products that manufacturers or owners are willing to sell at different prices at a specific time. Demand – the quantity of products that consumers are willing to buy at different prices at a specific time. The key factor in determining the quantities supplied and demanded is price. Proponents of a free market argue that, because supply and demand interactions determine prices, there is no need for government to set prices.

16

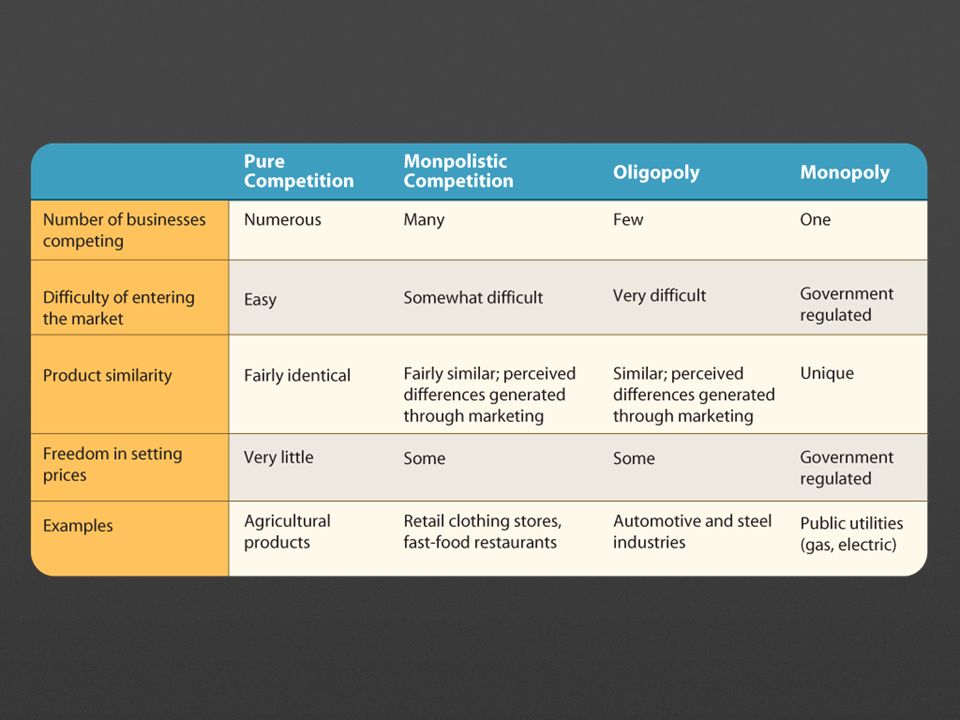

Types of Competition In free markets there are four types of competition: Perfect Competition – The degree of competition in which there are many sellers in a market and none is large enough to dictate the price of a product. Monopolistic Competition – The degree of competition in which a large number of sellers produce very similar products that buyers nevertheless perceive as different. Oligopoly – A degree of competition in which just a few sellers dominate the market. Monopoly – A degree of competition in which only one seller controls the total supply of a product or service and sets the price. The United States has laws in place the prohibit the creation of monopolies.

18

Key Indicators Economy is Doing?

What are some Key Indicators of how the Economy is Doing?

19

The major indicators of economic conditions are:

Gross domestic product (GDP) Unemployment rate Price indexes and inflation

Unemployment rate. Price indexes and inflation.")

20

Gross Domestic Product

Gross Domestic Product (GDP) - The total value of final goods and services produced in a country in a given year. Either a domestic or foreign-owned company may product the goods and services included in GDP, as long as the company is located within the measuring country’s boundaries. Another way to measure GDP is per capita, or per person. Gross National Product (GNP) - The value of goods and services produced by a country’s factors of production, regardless of where these factors are based. A major influence on the growth of the GDP is how productive the workforce is– how much output workers create for a given amount of input.

- The total value of final goods and services produced in a country in a given year. Either a domestic or foreign-owned company may product the goods and services included in GDP, as long as the company is located within the measuring country’s boundaries. Another way to measure GDP is per capita, or per person. Gross National Product (GNP) - The value of goods and services produced by a country’s factors of production, regardless of where these factors are based. A major influence on the growth of the GDP is how productive the workforce is– how much output workers create for a given amount of input.")

21

Recession, Depression, and Recovery

Recession – A period during which the GDP of a nation declines for to or more quarters. Depression – A severe recession. Recovery – A period following a recession during which an economy stabilizes and begins to grow again.

22

Unemployment Rate Unemployment Rate – The number of civilians 16 years of age and older who are unemployed and have tried to find a job within the prior four weeks. There are four type of unemployment: Cyclical – Not enough jobs for the people who want them, usually as a result of political or economic forces. Seasonal – Certain jobs can only take place during certain months of the year, and seasonal unemployment affects these workers. Frictional – A state wherein people are between jobs, such as a two-week period between ending one job and beginning another. Structural – A major shift in an industry causing people to lose their jobs.

23

Price Indexes Inflation – A general rise in the prices of goods and services over time. Some amount of inflation– about 2 percent per year– is considered normal. Stagflation – A situation where the economy is slowing but prices are rising. Many economist believe stagflation is a result of misguided fiscal and monetary policy by the federal government. Deflation – A general decline in the prices of goods and services over time. Price indexes are economic indicators that reveal the effects of inflation. Two widely used measures of inflation include: Consumer Price Index (CPI) – A set of monthly statistics that measures the price of inflation or deflation. Producer Price Index (PPI) – A set of monthly statistics that measures prices at the wholesale level.

– A set of monthly statistics that measures the price of inflation or deflation. Producer Price Index (PPI) – A set of monthly statistics that measures prices at the wholesale level.")

24

What is a Business Cycle?

25

Business Cycle – A pattern that consists of a period of rapid economic expansion alternating with a period of economic decline or contraction. During the expansion phase or prosperity, supply and demand grow. During the contraction phase or recession, supply and demand diminish. Dramatic swings in the economy cause disruptions to business. The government tries to minimize dramatic swings by using fiscal and monetary policy.

26

Fiscal Policy Fiscal Policy – The government’s efforts to keep the economy stable by increasing or decreasing taxes or government spending. Taxation High tax rates tend to slow the economy, while low tax rates tend to give the economy a boost. Government Spending Spending on highways, social programs, etc. Government spending affects that national deficit as well as the national debt. National Deficit – The amount of money the federal government spends beyond what is receives in taxes for a given fiscal year. National Debt – The sum of the government deficits over time.

27

Monetary Policy Monetary Policy – Management of the money supply and interest rates. In the US, this is accomplished by the Federal Reserve Bank (Fed). Interest Rates When the economy is booming interest rates are raised, making money more expensive to borrow. Businesses borrow less, thus helping to slow the economy. When the economy is in trouble interest rates are lowered, making it less expensive to borrow. Businesses borrow more, thus helping to grow the economy. Money Supply When the economy is booming the Fed lowers the money supply, and when it is in trouble, the Fed increases the money supply.

. Interest Rates. When the economy is booming interest rates are raised, making money more expensive to borrow. Businesses borrow less, thus helping to slow the economy. When the economy is in trouble interest rates are lowered, making it less expensive to borrow. Businesses borrow more, thus helping to grow the economy. Money Supply. When the economy is booming the Fed lowers the money supply, and when it is in trouble, the Fed increases the money supply.")