Download presentation

Presentation is loading. Please wait.

2

Economics

3

What is economics? It studies how we allocate the limited resources to satisfy unlimited wants

4

American Free Market System Introduction Challenges in a free market Supply and Demand Economic systems The U.S. economy Factors of Production Business organizations

6

The Circular flow of Economics Resources, goods and services and money flow continuously among households, businesses and the government in the U.S. economy.

7

The Circular flow of Economics Continued… Individual households own the resources used in production; sell the resources and use the income to purchase products. Businesses (producers) buy resources used in production; sell the resources and use the income to purchase products. Businesses provide households with income and goods and services. Governments use tax revenue from individuals and businesses to provide public goods and services.

buy resources used in production; sell the resources and use the income to purchase products. Businesses provide households with income and goods and services. Governments use tax revenue from individuals and businesses to provide public goods and services..")

8

Households supply businesses with labor (workforce) and payments for goods and services Businesses provides households with income and public goods and services. The government supplies businesses with public goods and services and payments for products purchased. Businesses provide the government with taxes and goods and services. The government provides households with income and public goods and services. Households provide the government with labor (workforce) and taxes

and taxes.")

9

Production, Consumption and Distribution Four Questions all Economic Systems must Address

10

Four Questions All Economic Systems must address… What is produced? *Production* Goods and services must satisfy the consumers wants and desires

11

Four Questions All Economic Systems must address… HOW should these goods be produced? *Factors of Production* 1.Capital 2.Entrepreneurship 3.Land 4.Labor Combine the factors of production to make or produce the goods and services

13

Four Questions All Economic Systems must address… For WHOM are the goods and services produced? *Distribution* Getting the goods and services from producer to consumer

15

Four Questions All Economic Systems must address… HOW MANY goods and services should be produced? *Consumption* Make enough to have a large profit and still have consumer demand. How many is determined by supply and demand.

17

Supply and Demand

18

Supply and Demand… Scarcity is the inability to satisfy all wants at the same time due to limited resources Choices must be made as to what to produce, how much to produce and who will receive what is produced. PRICE: Mechanism to decide who gets goods and services. The amount that satisfies both producers for profit and consumers for value.

19

Scarcity

20

Choices

21

Price

22

Supply and Demand determine price through their interaction DEMAND: is the amount of a good or service that consumers are willing and able to buy at a certain price SUPPLY: is the amount of a good or service that producers are willing and able to sell at a certain price.

23

LAW OF SUPPLY : Businesses will provide more products when they can sell them at higher prices LAW OF DEMAND: Buyers will demand more products when they can buy them at lower prices

24

Incentives Incite or motivate Change economic behavior Something that spurs someone into action: sale, coupons, etc.

25

Resources, Scarcity & Opportunity Cost

26

Good Anything that can be grown or manufactured (made) Food Clothes Cars

Food Clothes Cars")

27

Service Something a person does for someone else in exchange for money or value. Doctor Hairdresser waiter

28

Resources Natural Human Capital Combine to make goods and services

29

Our Basic Economic Problem…

30

People have Unlimited Wants Food Clothing Shelter Schools Hospitals Cars Transportation

31

But Resources are Limited Land Soil Minerals Fuels People Money Technology

32

Scarcity The inability to satisfy all wants at the same time; the NEEDS are greater than the RESOURCES

33

Since resources are LIMITED consumers and producers must make CHOICES CHOICE: selecting from a set of alternatives OPPORTUNITY COST: what is given up when the choice is made.

34

*Scarcity forces us to choose which needs and wants to satisfy with available resources. *Scarcity affects decisions concerning what and how much to produce, how goods and services will be produced and who will get what is produced

35

Production: (sellers) *Combining resources to make goods and services. *Available resources and consumer preference determine what is produced Consumption (buyers) *Using goods and services *Consumer preference and price determine what is purchased

*Using goods and services *Consumer preference and price determine what is purchased.")

36

SELLER Buyer

37

Challenges in a Free Market: Terms

38

Scarcity In English You can't have everything you want. Lessons for life Acceptance of scarcity will help you make more reasoned choices

40

Alternatives In English Different options from which you can choose Lessons for Life There are many different ways to allocate resources and to solve problems Yes….these are generic converse!

41

Choice In English Because you can't have everything you want, you have to make choices from a list of alternatives Lessons for life When policy-makers decide on a particular resource allocation, recognize that a choice had to be made due to scarcity. You may not like the alternative chosen, you may question the choice, but the villain is scarcity

42

Trade-off’s In English Choices involve giving up something to get something. All choices have consequences, both positive and negative Lessons for Life You are responsible for the consequences of your choices. Since you make choices, you can't be a victim.

43

Opportunity Cost In English What is given up when a choice is made Lessons for Life All choices have opportunity costs. A good idea is only a good idea if its value is greater than the value of its opportunity cost. Voters must always identify the opportunity cost of a particular policy

44

Types of Economies Traditional economy: –Economic decisions are based on custom and historical precedent. –People often perform the same type of work as their parents and grandparents, regardless of ability or potential.

45

Command Economy The central government makes decisions and determines how resources will be used. The central government owns property and resources. Businesses are not run for profit. No competition Lack of consumer choice The government sets the prices of goods and services. China, North Korea, Cuba

46

Economic Systems

48

Mixed Economy Most common type of economic system Government and individuals share the decision making process Individuals and businesses make decisions for the private sector Individuals own the means of production Government makes plans for the public sector Government guides and regulates production of goods and services offered. A greater government role than in a free market economy Most effective economy for providing goods and services U.S. and most Western European countries are mixed economies

50

Free Market Economy Also known as capitalism or free enterprise Private ownership of property and resources (owned by individuals) Individuals and businesses make profits Individuals and businesses compete Economic decisions are made by supply and demand Profit is a motivator for productivity No government involvement Consumer sovereignty: buyers determine what is produced

Individuals and businesses make profits Individuals and businesses compete Economic decisions are made by supply and demand Profit is a motivator for productivity No government involvement Consumer sovereignty: buyers determine what is produced")

51

The U.S. economy is a MIXED ECONOMY PRIVATE PROPERTY FREE MARKETS PROFIT COMPETITION CONSUMER SOVEREIGNTY Markets are allowed to operate without undue interference from the government. Money, goods and services flow continuously among individual households, businesses and the government Consumers determine what goods and services are produced by what they buy Money left over after all business expenses have been paid. Rivalry between businesses for the same customers; results in better quality Individuals can own the means of production & property without undue government interference

52

Competition We compete for the use of limited resources –2 ways of competition –Price competition –Non price competition e.g. waiting, examination, lucky draw, violence…

53

Factors of Production anything that goes into the making of a good or service

54

Factors of Production Capital Ex: tools, machinery, money and technology Entrepreneur Business owner and risk taker combines the factors of production

55

Factors of production cont… Land Natural Resources Labor Workers and their time and energy

56

Business Organizations The 15 million businesses in the U.S. fall into three categories: sole proprietorships, owned by a single individual, partnerships, with more than one owner sharing the risks and profits and corporations, owned by their stockholders.

57

Sole Proprietorship 1 owner The owner takes all the risks Supplies capital, hires help, pays taxes The owner makes all the profits The owner is solely responsible for losses

58

Partnership More than one owner (2+) Risks are shared amongst the owners Profits are shared amongst the owners Often more successful than sole proprietorships Responsibilities are shared

Risks are shared amongst the owners Profits are shared amongst the owners Often more successful than sole proprietorships Responsibilities are shared")

59

Corporation Owned by stockholders Authorized to act as a legal person regardless of the number of owners Owners share the profits Liability is limited to investment (you can only loose as much as you put in) Raise money by selling stocks No one is responsible for corporation’s debt if it fails

Raise money by selling stocks No one is responsible for corporation’s debt if it fails")

60

Making choices Which restaurant will you go for lunch? What would you like to study at university? What will you buy with $100? CD or dress ? Which girl (boy) will you marry?

will you marry .")

62

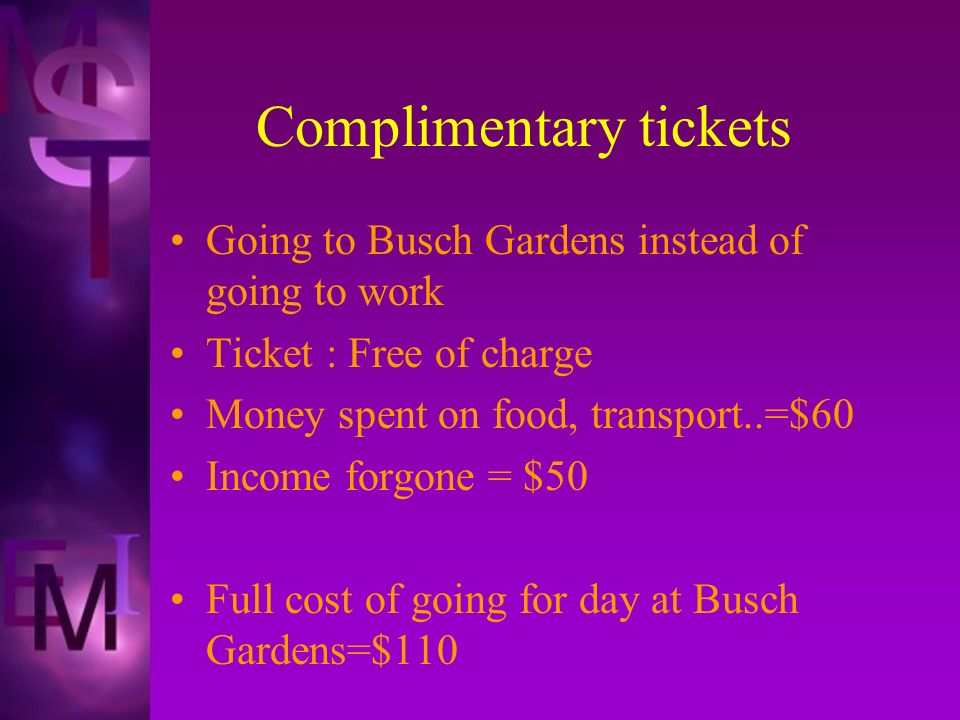

Complimentary tickets Going to Busch Gardens instead of going to work Ticket : Free of charge Money spent on food, transport..=$60 Income forgone = $50 Full cost of going for day at Busch Gardens=$110

63

Choosing a Career Cost-Benefit Analysis Cost: Education Benefit: Higher paying job Example: Cost of college for 4 years averages $36,000.

64

Average Annual Earnings— Different Levels of Education Professional Degree $109,600 Doctoral Degree $89,400 Master's Degree $62,300 Bachelor's Degree $52,200 Associate's Degree $38,200 Some College $36,800 High School Graduate $30,400 Some High School $23,400 Average Annual Earnings— Different Levels of Education. Source: U.S. Census Bureau, Current Population Surveys, March 1998, 1999, and 2000.

65

Taxation Definition of taxation: In economic terms, wealth transfer from businesses or households to the government occurs by use of taxation. Let us now look at the four main purposes of taxation which are: 1. Revenue: to raise money to spend on hospitals & schools, roads and government functions like justice system. 2. Redistribution: Transfer of wealth from richer sections of society to poorer sections. This is controversial. 3. Repricing: Taxes are imposed to influence society; taxation on tobacco to discourage smoking. 4. Representation: direct taxation results in higher degree of accountability & better governance.

66

Types of Taxes Income Sales Self-employed businessperson or independent Contractor Business Real estate Utility Lodging/Restaurant Personal property

67

Personal Finances No one will make your life but you! You cannot build a house without a hammer. You cannot build a lifestyle without money.

68

Definitions Personal finance: the process of planning your spending, financing, and investing to optimize your financial situation Personal financial plan: a plan of your financial goals and describes the spending, financing, and investing plans that are intended to achieve those goals

69

How You Benefit From An Understanding of Personal Finance Make your own financial decisions –Every spending decision has an opportunity cost Judge the advice of financial advisors –Make informed decisions

70

Components of a Financial Plan Budgeting and tax planning Managing your cash Financing your large purchases Protecting your assets and income (insurance) Investing your money Planning your retirement and estate

Investing your money Planning your retirement and estate")

71

A Plan for Your Budgeting and Tax Planning Budget planning: The process of forecasting future expenses and savings Evaluate your current financial position –Assets: what you own (buying a house vs. renting) –Liabilities: what you owe –Net worth: the value of what you own minus the value of what you owe

–Liabilities: what you owe –Net worth: the value of what you own minus the value of what you owe.")

72

Budgeting Identify sources of income. Relate employee benefits to disposable income (Do you have to buy insurance?) Estimate income (gross pay versus net pay). Estimate expenses. Construct a budget/spending plan. – Fixed expenses (rent/mortgage, insurance, electricity, water, gas, automobile, phone, cable) – Variable expenses (groceries, entertainment, taxes, etc.)

Estimate income (gross pay versus net pay). Estimate expenses. Construct a budget/spending plan. – Fixed expenses (rent/mortgage, insurance, electricity, water, gas, automobile, phone, cable) – Variable expenses (groceries, entertainment, taxes, etc.).")

73

Budgeting and Tax Planning

74

A Plan to Manage Your Cash Credit management: decisions regarding how much credit to obtain to support your spending and which sources of credit to use –Credit cards-decrease credit score (score given people based on how you use credit and available to bankers) –Short term loans-increase credit score –Mortgages-increase credit score, tax-deductible, build equity (equity is value held by bank but available to you as cash when you sell your home)

–Short term loans-increase credit score –Mortgages-increase credit score, tax-deductible, build equity (equity is value held by bank but available to you as cash when you sell your home)")

75

Managing Your Cash

76

Banking Checking-check card, checks, cash machine –Easy access, but with service fee Savings –Less access, rarely a fee Certificate of Deposit (CD) –Little access, they pay you interest!

–Little access, they pay you interest!")

77

Developing the Financial Plan Step 1. Establish Your Financial Goals –Types of goals Car, home, college, wealth, charity –Set realistic goals Stronger likelihood of reaching goals –Timing of goals Short term (within one year) Intermediate (between 1–5 years) Long term (beyond five years)

Intermediate (between 1–5 years) Long term (beyond five years).")

78

Developing the Financial Plan Step 2. Consider Your Current Financial Position –How your future financial position is tied to your education Consider your skills, interests, and career paths –How your future financial position is tied to your career choice Choose a career that will be enjoyable and suit your skills, as well as one which helps you reach your financial goals

79

Integrating Key Concepts

80

A Plan for Your Financing Loans often needed for large expenditures –College tuition, car, house Managing loans –How much can you afford to borrow? –Determining maturity of the loan –Selecting a loan with a competitive interest rate

81

Financing Your Large Purchases

82

Insurance Property-against fire, casualty Liability-against lawsuit! Automobile-This is a state law. Health –medical costs are very expensive! Life-as gift to those you love

83

Investing Stocks Bonds Annuities Mutual Funds Property (Real Estate, Precious Metals, Art, etc.)

")

84

A Plan for Your Investing Funds not needed for cash can be invested All investments have some level of risk Risk: uncertainty surrounding the potential return on an investment

85

Retirement Employee Benefits-not as common as it used to be! Social Security-A political issue. Do you want to count on this? Personal Savings-Your best bet!

86

A Plan for Your Retirement and Estate This includes insurance planning, retirement planning, and estate planning –Retirement planning: determining how much money should be set aside each year for retirement and how those funds should be invested –Estate planning: determining how your wealth will be distributed before or upon your death Your will

87

How to stay out of financial trouble Maintain a record-keeping system for credit purchases Ensure safekeeping of credit and credit cards Avoid late payment and other penalties-pay attention to deadlines, bills, etc. Debt payment plans-BUDGET!! Warning signs of debt problems –Default, Notices, Repossessions, Collection agencies, Liens, Garnishment, Foreclosure, Repossession, Eviction Credit counseling Understanding bankruptcy: Chapter 7 (liquidation), Chapter 13 (repayment) Rebuilding credit -bank accounts-->credit cards-->short term loans-->mortgages

, Chapter 13 (repayment) Rebuilding credit -bank accounts-->credit cards-->short term loans-->mortgages.")

88

Miss Cheng could spend two hours at a concert or tutoring a student at $70 per hour. She could use the time on painting instead and earn a total of $170. If the price of the concert ticket is $250, what is the opportunity cost of her choice of going to the concert? A. $410 B. $420 C. $430 D $440

89

No. of coupons Gifts51520CupBagCamera Mary has accumulated 20 Coupons. What is the opportunity cost to her if she uses them to exchange for one camera? A.Cup B. Bag C. Cup and Bag D. Cup or Bag

90

Which of the following statements about scarcity is true? A. Once a choice is made, the problem of scarcity is solved. B. A good is scarce if not everyone has it. C. Scarcity means unlimited human wants. D. Both rich people and poor people face the problem of scarcity. Answer: D

91

Which of the following are opportunity costs of attending school? (1) Poor examination results (2) Income forgone (3) School fees (4) Expenditure on dinners A. (1) and (4) only B. (1) and (3) only C. (2) and (3) only D. (2) and (4) only Answer: C. (2) and (3) only

Poor examination results (2) Income forgone (3) School fees (4) Expenditure on dinners A. (1) and (4) only B. (1) and (3) only C. (2) and (3) only D. (2) and (4) only Answer: C. (2) and (3) only.")

Similar presentations

An Overview Of Financial Management.>")