Download presentation

Presentation is loading. Please wait.

1

School of the Built Environment Demand, Supply and Affordability: Review of The Numbers Professor Glen Bramley IPPR Seminar on South East

2

School of the Built Environment Outline of Contribution Overall household numbers - sources of growth - interpretation of recent trends - implications for planning South East Composition of demand and supply Locational strategy Market responses to planning changes Affordable housing need & supply - scale of problem - mix and cost of solutions

3

School of the Built Environment Household Growth in South East South East high growth region for a long time London transformed from declining to growing Greater S E taking up more of growth Recent reduction in S E growth a blip? Evidence of tightening land constraint

4

School of the Built Environment

5

Supply isnt Responding

6

School of the Built Environment Barkers Diagnosis Low and declining levels of housebuilding Weak response of supply to prices, -> high and volatile prices Long run real house price rise +2.4-2.7% p a Affordability worsening, wealth gap widening Labour mobility & econ growth restricted Loss of economic welfare (e.g. smaller houses) BUT To be weighed against environmental benefits of planning restrictions

BUT To be weighed against environmental benefits of planning restrictions.")

7

School of the Built Environment Taking Your Eye off the Ball

8

School of the Built Environment Migration Migration the dominant factor in S E growth Strong movement from London to S E Pressure in London from natural change & international migration S E now net exporter to surrounding regions Outflow from London increasing But more of this going to other regions Tight land constraint in S E diverting migrants elsewhere

9

School of the Built Environment

11

International Migration Big increase in net and gross inflows in 1990s Data remain problematic Many explanatory factors - easier travel - EU expansion & integration - favourable economy – past migrations - political instability - HE sector London dominant destination S E receiving 10k net, 57k gross pa (ave 10 yr) Indirect London pressure more important

Indirect London pressure more important")

12

School of the Built Environment Household Composition Growth mainly due to population numbers Most of net growth is single person households Caution about implications for dwelling size/type Private sector output polarised, but mainly larger Social sector builds more small & flats Arbitrary discounting of young singles questionable

13

School of the Built Environment

15

What Number to Plan For? SEERA consulting on range 25.5k-32k In my view more realistic figure would be 40k Straining credibility to see London building 48k (vs 15-19k recent actual); maybe 30k Realistic to assign half overspill to S E (32+9=41) Correcting recent underperformance gives 38k LAs own expectations are 38k Economically dynamic region: jobs:housing bal Barker affordability targets will require substantial increase in S E

; maybe 30k Realistic to assign half overspill to S E (32+9=41) Correcting recent underperformance gives 38k LAs own expectations are 38k Economically dynamic region: jobs:housing bal Barker affordability targets will require substantial increase in S E.")

16

School of the Built Environment Locational Strategy Existing SCP focuses on Bucks & Kent Strongest economic growth is to the west Mega-city region perspective also points this way Little apparent stomach for economic restraint Therefore a strong case for more planned growth in Oxfords, Berks, Hants, W Sussex

17

School of the Built Environment Market Simulation Model Releasing more land -> less than proportionate increase in output (e.g. 100% -> 45%) Implies more/larger sites built out more slowly To counter this needs direct delivery vehicles Large output increase gives moderate price falls (e.g. 45%->5% in this case – maybe more…) Concentrated in one area -> more net migration Difficult to meet affordability goal by this route alone

Implies more/larger sites built out more slowly To counter this needs direct delivery vehicles Large output increase gives moderate price falls (e.g. 45%->5% in this case – maybe more…) Concentrated in one area -> more net migration Difficult to meet affordability goal by this route alone.")

18

School of the Built Environment

19

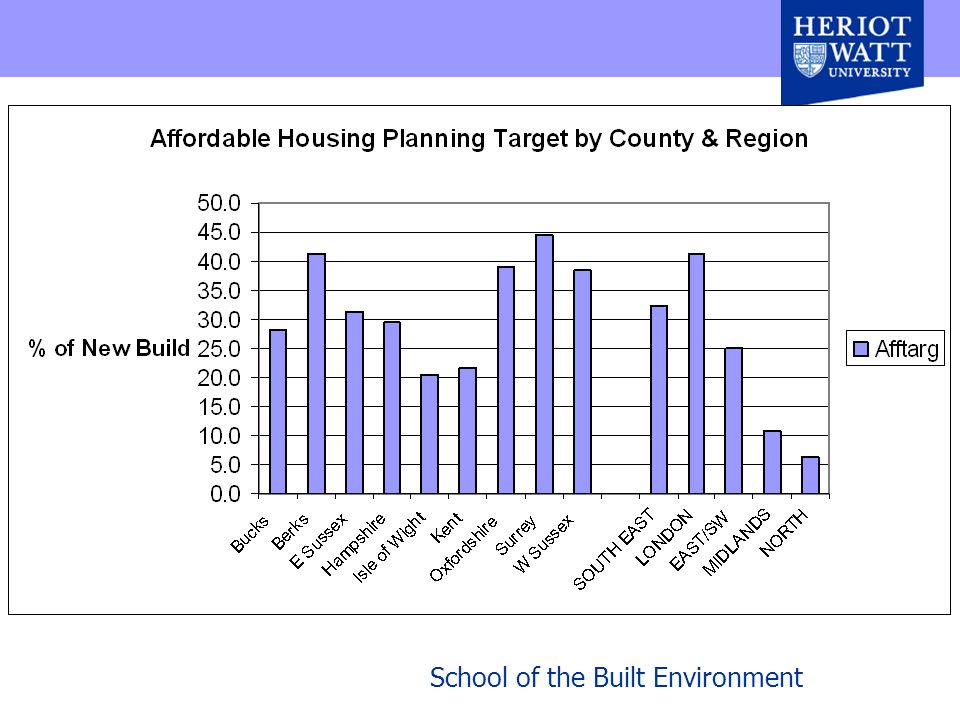

Affordability, Need & Supply Special run of affordability model (district level) Projection assumes some price correction Adjustment for wealth S E 2 nd worst after London; variation within reg Net new needs>feasible programme in S E & London (even maximising LCHO & planning) Current ADP<feasible prog, in south generally Net cost of prog for S E £660m, vs ADP of £300m Larger total build number would help bridge gap But backlog would remain

Projection assumes some price correction Adjustment for wealth S E 2 nd worst after London; variation within reg Net new needs>feasible programme in S E & London (even maximising LCHO & planning) Current ADP<feasible prog, in south generally Net cost of prog for S E £660m, vs ADP of £300m Larger total build number would help bridge gap But backlog would remain")

20

School of the Built Environment

24

Seminar Questions 1.40,000 a year + 2.Yes, but not 1:1; case for DDVs 3.(Yes, with adeq investment) 4.More in growth areas to west 5.(No comment) 6.Broad range of working and other households 7.Both, including intermediate LCHO; each strategy in isolation not enough.

4.More in growth areas to west 5.(No comment) 6.Broad range of working and other households 7.Both, including intermediate LCHO; each strategy in isolation not enough.")

Similar presentations