Download presentation

Presentation is loading. Please wait.

1

Ch 4 THE THEORY OF PRODUCTION

Production theory forms the foundation for the theory of supply Managerial decision making involves four types of production decisions: 1. Whether to produce or to shut down 2. How much output to produce 3. What input combination to use 4. What type of technology to use Ch 5 Ch 4

2

Production involves transformation of inputs such as capital, equipment, labor, and land into output - goods and services In this production process, the manager is concerned with efficiency in the use of the inputs - technical vs. economical efficiency

3

Two Concepts of Efficiency

Economic efficiency: occurs when the cost of producing a given output is as low as possible Technological efficiency: occurs when it is not possible to increase output without increasing inputs

4

The objective of efficiency will provide us with some basic rules about the manner in which firms should utilize inputs to produce goods and services

5

to maximize the output attainable with a given level of cost.

You will see that basic production theory is simply an application of constrained optimization: the firm attempts either to minimize the cost of producing a given level of output or to maximize the output attainable with a given level of cost. Both optimization problems lead to same rule for the allocation of inputs and choice of technology

6

Production Function A production function is a table or a mathematical equation showing the maximum amount of output that can be produced from any specified set of inputs, given the existing technology Q f2(x) f1(x) f0(x) Improvement of technology f0(x) - f2(x) Q = output x = inputs x

f1(x) f0(x) Improvement of technology. f0(x) - f2(x) Q = output. x = inputs. x.")

7

Production Function continued

Q = f(X1, X2, …, Xk) where Q = output X1, …, Xk = inputs For our current analysis, let’s reduce the inputs to two, capital (K) and labor (L): Q = f(L, K)

where. Q = output. X1, …, Xk = inputs. For our current analysis, let’s reduce the inputs to two, capital (K) and labor (L): Q = f(L, K)")

8

Production Table Same Q can be produced with different combinations of inputs, e.g. inputs are substitutable in some degree

9

All of these outputs are assumed to be technically efficient

But which one is economically efficient? That is the question facing the DM

10

Short-Run and Long-Run Production

In the short run some inputs are fixed and some variable e.g. the firm may be able to vary the amount of labor, but cannot change the amount of capital in the short run we can talk about factor productivity

11

In the long run all inputs become variable

e.g. the long run is the period in which a firm can adjust all inputs to changed conditions in the long run we can talk about returns to scale (compare latter with economies of scale, which is a cost related concept)

")

12

Short-Run Changes in Production Factor Productivity

How much does the quantity of Q change, when the quantity of L is increased?

13

Long-Run Changes in Production Returns to Scale

How much does the quantity of Q change, when the quantity of both L and K is increased?

14

Relationship Between Total, Average, and Marginal Product: Short-Run Analysis

Total Product (TP) = total quantity of output Average Product (AP) = total product per total input Marginal Product (MP) = change in quantity when one additional unit of input used

= total quantity of output. Average Product (AP) = total product per total input. Marginal Product (MP) = change in quantity when one additional unit of input used.")

15

The Marginal Product of Labor

The marginal product of labor is the increase in output obtained by adding 1 unit of labor but holding constant the inputs of all other factors Marginal Product of L: MPL= Q/L (holding K constant) = Q/L Average Product of L: APL= Q/L (holding K constant)

= Q/L. Average Product of L: APL= Q/L (holding K constant)")

16

Short-Run Analysis of Total, Average, and Marginal Product

If MP > AP then AP is rising If MP < AP then AP is falling MP = AP when AP is maximized TP maximized when MP = 0

17

Law of Diminishing Returns (Diminishing Marginal Product)

Holding all factors constant except one, the law of diminishing returns says that: As additional units of a variable input are combined with a fixed input, at some point the additional output (i.e., marginal product) starts to diminish e.g. trying to increase labor input without also increasing capital will bring diminishing returns Nothing says when diminishing returns will start to take effect, only that it will happen at some point All inputs added to the production process are exactly the same in individual productivity

starts to diminish. e.g. trying to increase labor input without also increasing capital will bring diminishing returns. Nothing says when diminishing returns will start to take effect, only that it will happen at some point. All inputs added to the production process are exactly the same in individual productivity.")

18

Three Stages of Production in Short Run

AP,MP Stage I Stage III Stage II APX X MPX Fixed input grossly underutilized; specialization and teamwork cause AP to increase when additional X is used Specialization and teamwork continue to result in greater output when additional X is used; fixed input being properly utilized Fixed input capacity is reached; additional X causes output to fall

19

How to Determine the Optimal Input Usage

We can find the answer to this from the concept of derived demand The firm must know how many units of output it could sell, the price of the product, and the monetary costs of employing various amounts of the input L Let us for now assume that the firm is operating in a perfectly competitive market for its output and its input

20

Example 1: Note: P = Product Price = $2

W = Cost per unit of labor = $10000 TRP = TP x P, MRP = MP x P TLC = X x W MLC = TLC / X

21

Optimal Decision Rule:

A profit maximizing firm operating in perfectly competitive output and input markets will be using optimal amount of an input at the point at which the monetary value of the input’s marginal product is equal to the additional cost of using that input (L) - in other words, when MRP = MLC

- in other words, when MRP = MLC.")

22

Production in the Long-Run

All inputs are now considered to be variable (both L and K in our case) How to determine the optimal combination of inputs? To illustrate this case we will use production isoquants. An isoquant is a curve showing all possible combinations of inputs physically capable of producing a given fixed level of output.

How to determine the optimal combination of inputs To illustrate this case we will use production isoquants. An isoquant is a curve showing all possible combinations of inputs physically capable of producing a given fixed level of output.")

23

Example 2 Production Table

Units of K Employed Isoquant

24

An Isoquant

25

Substituting Inputs There exists some degree of substitutability between inputs. Different degrees of substitution: Corn syrup Natural flavoring Capital K1 K2 K K4 Q Q Sugar All other ingredients Labor L1 L2 L L4 a) Perfect substitution b) Perfect complementarity c) Imperfect substitution

Perfect substitution. b) Perfect complementarity. c) Imperfect substitution.")

26

Substituting Inputs continued

In case the two inputs are imperfectly substitutable, the optimal combination of inputs depends on the degree of substitutability and on the relative prices of the inputs

27

Substituting Inputs continued

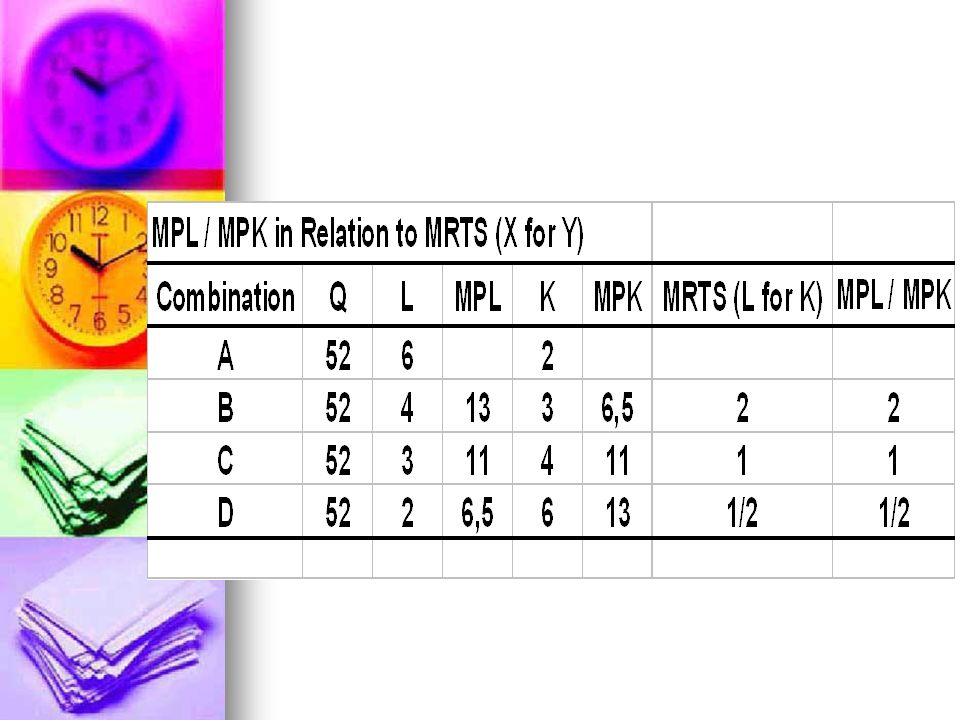

The degree of imperfection in substitutability is measured with marginal rate of technical substitution (MRTS): MRTS = L/K (in this MRTS some of L is removed from the production and substituted by K to maintain the same level of output)

: MRTS = L/K. (in this MRTS some of L is removed from the production and substituted by K to maintain the same level of output)")

28

Law of Diminishing Marginal Rate of Technical Substitution:

29

Law of Diminishing Marginal Rate of Technical Substitution continued

Y =- 2 B C X = 1 Y = -1 D E X = 1 Y = -1 X = 2

30

MRTS = L/K = - MPL/MPK

Similar presentations

where R is revenue, C is cost, P is price,>")