Download presentation

Presentation is loading. Please wait.

1

1 Bruce Bowhill University of Portsmouth ISBN: 978-0-470-06177-0 © 2008 John Wiley & Sons Ltd. www.wileyeurope.com/college/bowhill

2

Chapter 5 Traditional Approaches to Full Costing © 2008 John Wiley & Sons Ltd. www.wileyeurope.com/college/bowhill

3

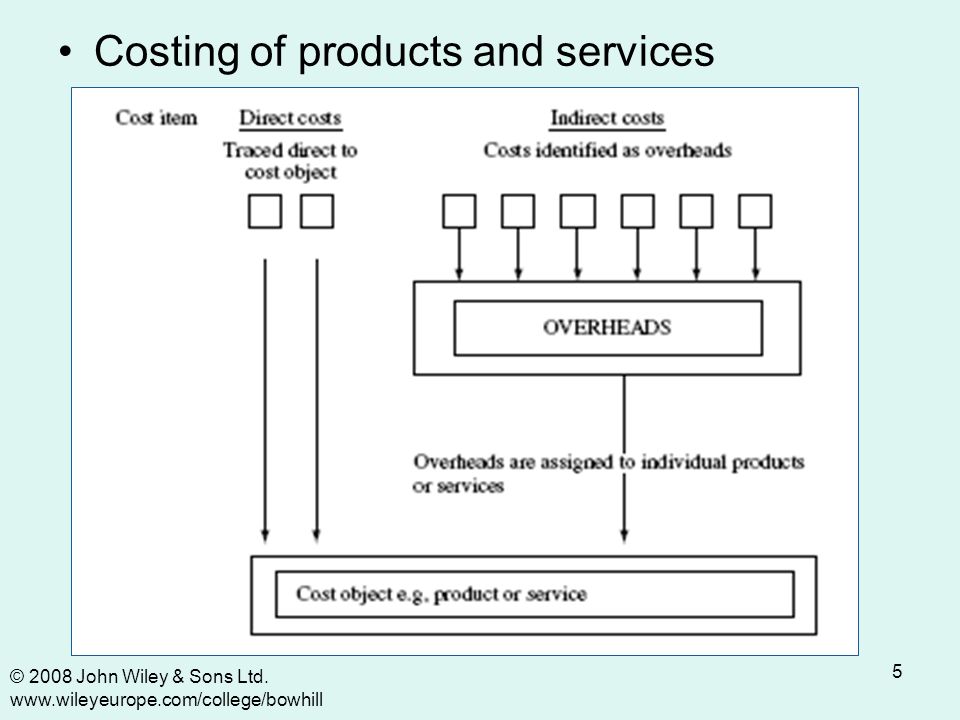

3 COST RECORDING AND CLASSIFICATION Direct costs are those costs that can be exclusively identified with a particular cost object. A cost object is any activity for which a separate measurement of cost is desired. This could be a range of entities such as a product, a service or a department. Indirect costs or overheads are those costs that cannot be exclusively identified with a particular cost object © 2008 John Wiley & Sons Ltd. www.wileyeurope.com/college/bowhill

4

4 Purposes of full/total costing To calculate the full cost of a single product or service: i) Identify the direct costs. ii) Assign a proportion of the indirect costs to each product or service. Three main possible reasons for undertaking this activity: 1) Profit determination. A proportion of the overheads should be included in the cost of those goods or services. 2) Pricing. Some organisations use the full cost of a product or service as a basis for pricing. 3) Inventory valuation. Inventories should be valued at the lower of full manufacturing cost or the net sales value. (Statement of Standard Accounting Practice 9) © 2008 John Wiley & Sons Ltd. www.wileyeurope.com/college/bowhill

Assign a proportion of the indirect costs to each product or service. Three main possible reasons for undertaking this activity: 1) Profit determination. A proportion of the overheads should be included in the cost of those goods or services. 2) Pricing. Some organisations use the full cost of a product or service as a basis for pricing. 3) Inventory valuation. Inventories should be valued at the lower of full manufacturing cost or the net sales value. (Statement of Standard Accounting Practice 9) © 2008 John Wiley & Sons Ltd.")

5

5 Costing of products and services © 2008 John Wiley & Sons Ltd. www.wileyeurope.com/college/bowhill

6

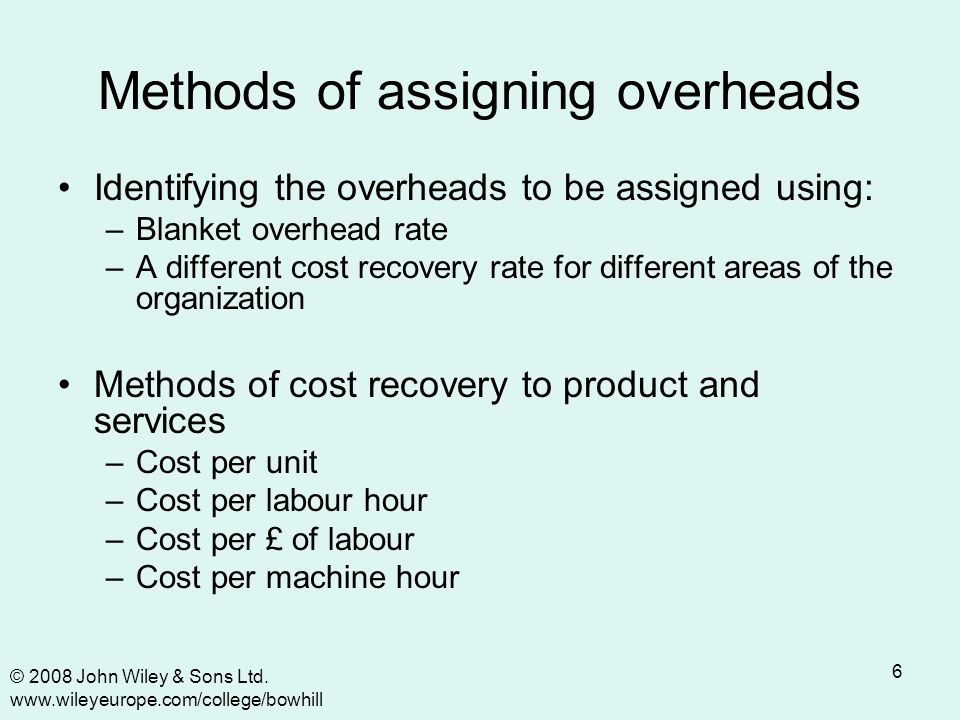

6 Methods of assigning overheads Identifying the overheads to be assigned using: –Blanket overhead rate –A different cost recovery rate for different areas of the organization Methods of cost recovery to product and services –Cost per unit –Cost per labour hour –Cost per £ of labour –Cost per machine hour © 2008 John Wiley & Sons Ltd. www.wileyeurope.com/college/bowhill

7

7 © 2008 John Wiley & Sons Ltd. www.wileyeurope.com/college/bowhill

8

8 Step 1. Calculating the departmental overhead rate CostBasis of apportioning costs to cost centres Canteen costsNumber of employees Rent /Heating and lightingFloor area InsuranceCost of assets in the department © 2008 John Wiley & Sons Ltd. www.wileyeurope.com/college/bowhill

9

9 Step 2 Costs of service departments need to be reallocated to the ‘production’ departments Step 3 A separate overhead rate needs to be calculated for each ‘production’ department. E.g. if a labour hour rate: Overhead £10,000 = £10 / hour Budget labour hours 1,000 Step 4. An overhead rate can be assigned to each product or service. E.g. 1.5 hours at £10 an hour = £15. © 2008 John Wiley & Sons Ltd. www.wileyeurope.com/college/bowhill

10

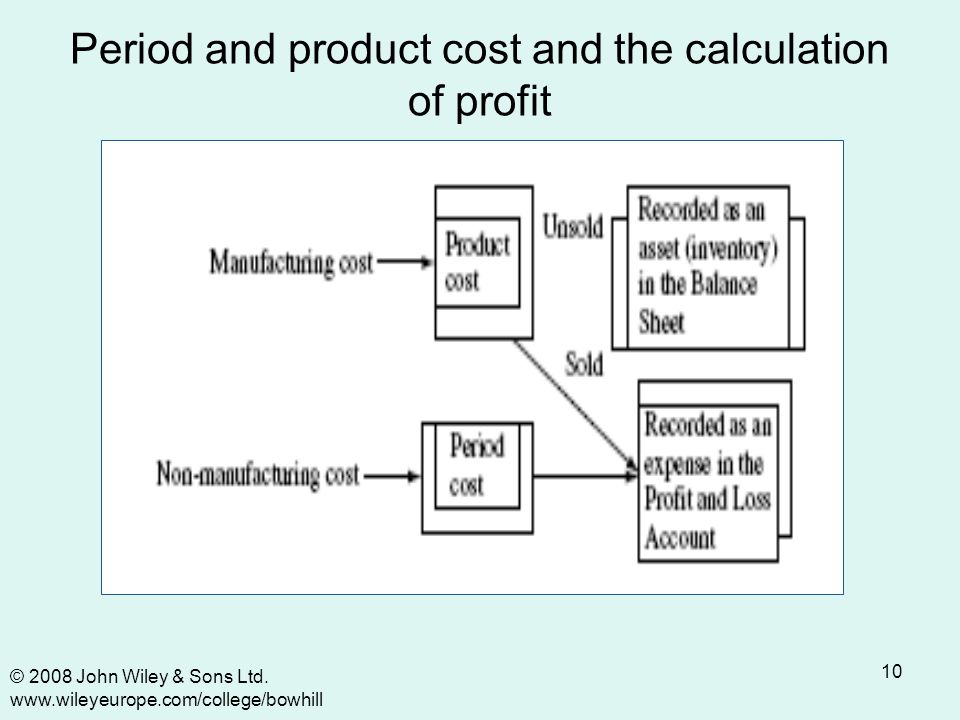

10 Period and product cost and the calculation of profit © 2008 John Wiley & Sons Ltd. www.wileyeurope.com/college/bowhill

11

11 a) 1,500 units sold at £10 each £ Sales 15,000 Less Cost of Sales (Note 1) 10,500 Gross Profit 4,500 Less Administration expenses 500 Net profit 4,000 Note 1 The cost of sales is calculated by multiplying the budgeted manufacturing cost per unit of £7 by budgeted sales of 1,500 units. Prepared the Profit and Loss Account and Balance Sheet for 600 units. © 2008 John Wiley & Sons Ltd. www.wileyeurope.com/college/bowhill

12

12 600 units sold at £10 each. 1,500 units manufactured, so 900 units are in inventory at the end of the month. £ Sales 6,000 Less Cost of Sales (Note 1) 4,200 Gross Profit 1,800 Less Administration expenses 500 Net profit 1,300 Note 1 - 600 units sold at £7 per unit. 900 units. 900 units of stock are unsold and these are also valued at £7 per unit, which is £6,300 © 2008 John Wiley & Sons Ltd. www.wileyeurope.com/college/bowhill

4,200 Gross Profit 1,800 Less Administration expenses 500 Net profit 1,300 Note units sold at £7 per unit. 900 units. 900 units of stock are unsold and these are also valued at £7 per unit, which is £6,300 © 2008 John Wiley & Sons Ltd.")

13

13 Contract costing The contract price to manufacture a cargo ship is £12 million; budgeted cost is £10 million; contract is expected to last 2 years. At the end of the first year: £million Certified work completed is valued at 7.0. Costs to date 6.0 Profit 1.0 Profit on the work certified to date is £1.0 million. At the end of the second year. £million Certified work completed is valued at 12.0. Costs to date 10.5 Profit 1.5 Profit in second year = £1.5 million - £1.0 million = £500,000. © 2008 John Wiley & Sons Ltd. www.wileyeurope.com/college/bowhill

14

14 Process costing Ellesmere chemicals produces a chemical product Step 1 – calculate the equivalent number of litres processed in a period i) 4,000 litres are completed in the month. ii) 300 litres of partly completed chemical (25% complete) were available at the beginning of the month. This is equivalent to 300 x 25% = 75 completed units. iii) 500 litres of partly completed chemical (50% complete) were available at the end of the month. This is equivalent to 500 x 50% = 250 completed units. © 2008 John Wiley & Sons Ltd. www.wileyeurope.com/college/bowhill

300 litres of partly completed chemical (25% complete) were available at the beginning of the month. This is equivalent to 300 x 25% = 75 completed units. iii) 500 litres of partly completed chemical (50% complete) were available at the end of the month. This is equivalent to 500 x 50% = 250 completed units. © 2008 John Wiley & Sons Ltd.")

15

15 The equivalent completed units are therefore: Litres Competed units 4000 Add equivalent completed units at end of month 250 4,250 Less equivalent completed units at beginning of month 75 Equivalent completed units in month 4,175 Step 2 – identify the costs in the month The costs of production were £41,750 in the month. Step 3 – identify the cost per litre. The cost per litre of chemical is £41,750 =£10. 4,175 litres © 2008 John Wiley & Sons Ltd. www.wileyeurope.com/college/bowhill

Similar presentations

Customers.>")