Download presentation

Presentation is loading. Please wait.

1

c. 2014 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, or posted to a publicly accessible website, in whole or in part. Current Liabilities and Payroll Chapter 11

2

Learning Objectives 1. Describe and illustrate current liabilities related to accounts payable, current portion of long-term debt, and notes payable. 2. Determine employer liabilities for payroll, including liabilities arising from employee earnings and deductions from earnings. 3. Describe payroll accounting systems that use a payroll register, employee earnings records, and a general journal.

3

Learning Objectives 4. Journalize entries for employee fringe benefits, including vacation pay and pensions. 5. Describe the accounting treatment for contingent liabilities and journalize entries for product warranties. 6. Describe and illustrate the use of the quick ratio in analyzing a company’s ability to pay its current liabilities.

4

c. 2014 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, or posted to a publicly accessible website, in whole or in part. Learning Objective Describe and illustrate current liabilities related to accounts payable, current portion of long- term debt, and notes payable 1

5

Current Liabilities o When a company or a bank advances credit, it is making a loan. o The company or bank is called a creditor (or lender). o The individuals or companies receiving the loans are called debtors (or borrowers).

. o The individuals or companies receiving the loans are called debtors (or borrowers)..")

6

Current Liabilities o Long-term liabilities are debts due beyond one year. o Current Liabilities are debts that will be paid out of current assets and are due within one year.

7

Accounts Payable o Accounts payable transactions arise from purchasing goods or services for use in a company’s operations or from purchasing merchandise for resale.

8

A CCOUNTS P AYABLE

9

Current Portion of Long-Term Debt o Long-term liabilities are often paid back in periodic payments, called installments. Installments that are due within the coming year must be classified as a current liability. The installments due after the coming year are classified as a long-term liability.

10

Short-Term Notes Payable o Nature’s Sunshine Company issues a 90-day, 12% note for $1,000, dated August 1, 2011 to Murray Co. for a $1,000 overdue account.

11

Interest Expense appears on the income statement as an “Other Expense.” Short-Term Notes Payable o When the note matures, the entry to record the payment of $1,000 plus $30 interest ($1,000 x 12% x 90/360) is as follows:

is as follows:")

12

Short-Term Notes Payable o On May 1, Bowden Co. (borrower) purchased merchandise on account from Coker Co. (creditor), $10,000, 2/10, n/30. The merchandise cost Coker Co. $7,500.

purchased merchandise on account from Coker Co. (creditor), $10,000, 2/10, n/30. The merchandise cost Coker Co. $7,500..")

13

Description DebitCredit Bowden Co. (Borrower) Mdse. Inventory10,000 Accounts Payable10,000 Coker Co. (Creditor) Description DebitCredit Accounts Receivable10,000 Sales10,000 Cost of Mdse. Sold7,500 Mdse. Inventory7,500 S HORT -T ERM N OTES P AYABLE

Description DebitCredit Accounts Receivable10,000 Sales10,000 Cost of Mdse. Sold7,500 Mdse. Inventory7,500 S HORT -T ERM N OTES P AYABLE.")

14

Short-Term Notes Payable o On May 31, Bowden Co. issued a 60-day, 12% note for $10,000 to Coker Co. on account.

15

Accounts Payable10,000 Notes Payable10,000 DescriptionDebitCredit Bowden Co. (Borrower) Notes Receivable10,000 Accounts Receivable10,000 Coker Co. (Creditor) DescriptionDebitCredit S HORT -T ERM N OTES P AYABLE

Notes Receivable10,000 Accounts Receivable10,000 Coker Co. (Creditor) DescriptionDebitCredit S HORT -T ERM N OTES P AYABLE.")

16

Short-Term Notes Payable o On July 30, Bowden Co. paid Coker Co. the amount due on the note of May 31, the face amount of $10,000 plus interest of $200 ($10,000 x 12% x 60/360).

..")

17

Notes Payable10,000 Interest Expense200 Cash10,200 DescriptionDebitCredit Bowden Co. (Borrower) Cash10,200 Interest Revenue 200 Notes Receivable10,000 Coker Co. (Creditor) DescriptionDebitCredit S HORT -T ERM N OTES P AYABLE

Cash10,200 Interest Revenue 200 Notes Receivable10,000 Coker Co. (Creditor) DescriptionDebitCredit S HORT -T ERM N OTES P AYABLE.")

18

Short-Term Notes Payable o On September 19, Iceburg Company borrowed cash from First National Bank by issuing a $4,000, 90-day, 15% note to the bank.

19

Short-Term Notes Payable o On December 18, Iceburg Company paid First National Bank $4,000 plus interest of $150 ($4,000 x 15% x 90/360).

.")

20

Short-Term Notes Payable o A discounted note has the following characteristics: The interest rate on the note is called the discount rate. The amount of interest on the note, called the discount, is computed by multiplying the discount rate times the face amount of the note. The debtor (borrower) receives the face amount of the note less the discount, called the proceeds. The debtor must repay the face amount of the note on the due date.

receives the face amount of the note less the discount, called the proceeds. The debtor must repay the face amount of the note on the due date..")

21

proceeds Short-Term Notes Payable o On August 10, Cary Company issues a $20,000, 90-day discounted note to Western National Bank. The discount rate is 15%, and the amount of the discount is $750 ($20,000 x 15% x 90/360).

..")

22

Short-Term Notes Payable o The entry when Cary Company pays the discounted note on November 8 is as follows:

23

c. 2014 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, or posted to a publicly accessible website, in whole or in part. Learning Objective Determine employer liabilities for payroll, including liabilities arising from employee earnings and deductions from earnings. 2

24

Payroll and Payroll Taxes o In accounting, payroll refers to the amount paid to employees for services they provided during the period. A company’s payroll is important for the following reasons: Payroll and related payroll taxes significantly affect the net income of most companies. Payroll is subject to federal and state regulations. Good employee morale requires payroll to be paid timely and accurately.

25

Liability for Employee Earnings o Salary usually refers to payment for managerial and administrative services. Salary is normally expressed in terms of a month or a year.

26

(concluded) Liability for Employee Earnings o Wages usually refers to payment for employee manual labor. The rate of wages is normally stated on an hourly or weekly basis.

27

Earnings at regular rate (40 x $34)$1,360 Earnings at overtime rate (2 x $51) 102 Total earnings$1,462 Liability for Employee Earnings o John T. McGrath is employed by McDermott Supply Co. at the rate of $34 per hour, plus 1.5 times the normal hourly rate for hours over 40 per week. For the week ended December 27, McGrath worked 42 hours. His earnings are computed as follows:

28

Deductions from Employee Earnings o The total earnings of an employee for a payroll period, including any overtime pay, are called gross pay. o From this amount is subtracted one or more deductions to arrive at the net pay.

29

D EDUCTIONS FROM E MPLOYEE E ARNINGS

30

Deductions from Employee Earnings o John T. McGrath made $1,462 for the week ending December 27. McGrath’s W-4 (previous slide) claims one withholding allowance of $70. Thus, the wages used to determine McGrath’s withholding bracket in Exhibit 3 (next slide) are $1,392 ($1,462 – $70).

claims one withholding allowance of $70. Thus, the wages used to determine McGrath’s withholding bracket in Exhibit 3 (next slide) are $1,392 ($1,462 – $70)..")

31

D EDUCTIONS FROM E MPLOYEE E ARNINGS

32

Deductions from Employee Earnings o The Federal Insurance Contributions Act (FICA) tax withheld contributes to the following two federal programs. Social security, which provides payments for retirees, survivors, and disability insurance. (Assume 6% on all earnings.) Medicare, which provides health insurance benefits for senior citizens. (Assume 1.5% on all earnings.)

Medicare, which provides health insurance benefits for senior citizens. (Assume 1.5% on all earnings.).")

33

Deductions from Employee Earnings o John T. McGrath’s earnings for the week ending December 27 are $1,462. Total FICA tax to be withheld is calculated as follows: Earnings subject to 6% social security tax $1,462 Social security tax rate x 6% Social security tax $ 87.72 Earnings subject to 1.5% Medicare tax $1,462 Medicare tax rate x 1.5% Medicare tax 21.93 Total FICA tax$109.65

34

Computing Employee Net Pay o John T. McGrath’s Net Pay

35

Liability for Employer’s Payroll Taxes o Employers are subject to the following payroll taxes for amounts paid their employees: FICA Tax Federal Unemployment Compensation Tax (FUTA) State Unemployment Compensation Tax (SUTA)

State Unemployment Compensation Tax (SUTA)")

36

L IABILITY FOR E MPLOYER ’ S P AYROLL T AXES

37

c. 2014 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, or posted to a publicly accessible website, in whole or in part. Learning Objective Describe payroll accounting systems that use a payroll register, employee earnings records, and a general journal. 3

38

Accounting Systems for Payroll and Payroll Taxes Accounting Systems for Payroll and Payroll Taxes o Payroll systems should be designed to: Pay employees accurately and timely. Meet regulatory requirements of federal, state, and local agencies. Provide useful data for management decision- making needs.

39

Payroll Register o The payroll register is a multicolumn report used for summarizing the data for each payroll period. Exhibit 5 illustrates a payroll register for McDermott Supply Co.

40

(left side, continued) P AYROLL R EGISTER

P AYROLL R EGISTER")

41

(right side) P AYROLL R EGISTER

P AYROLL R EGISTER")

42

R ECORDING E MPLOYEES ’ E ARNINGS

43

Social security tax$ 834.12($13,902 x 6%) Medicare tax208.53($13,902 x 1.5%) SUTA146.34($2,710 x 5.4%) FUTA 21.68($2,710 x 0.8%) Total payroll taxes$1,210.67 Recording and Paying Payroll Taxes o Employers must match the employee’s social security and Medicare tax contributions. In addition, the employer must pay SUTA tax of 5.4% and FUTA tax of 0.8% (assume on $2,710). For McDermott Supply’s payroll of December 27, these payroll taxes are computed as follows:

. For McDermott Supply’s payroll of December 27, these payroll taxes are computed as follows:.")

44

Recording and Paying Payroll Taxes o The entry to journalize the payroll tax expense for Exhibit 5 is shown below.

45

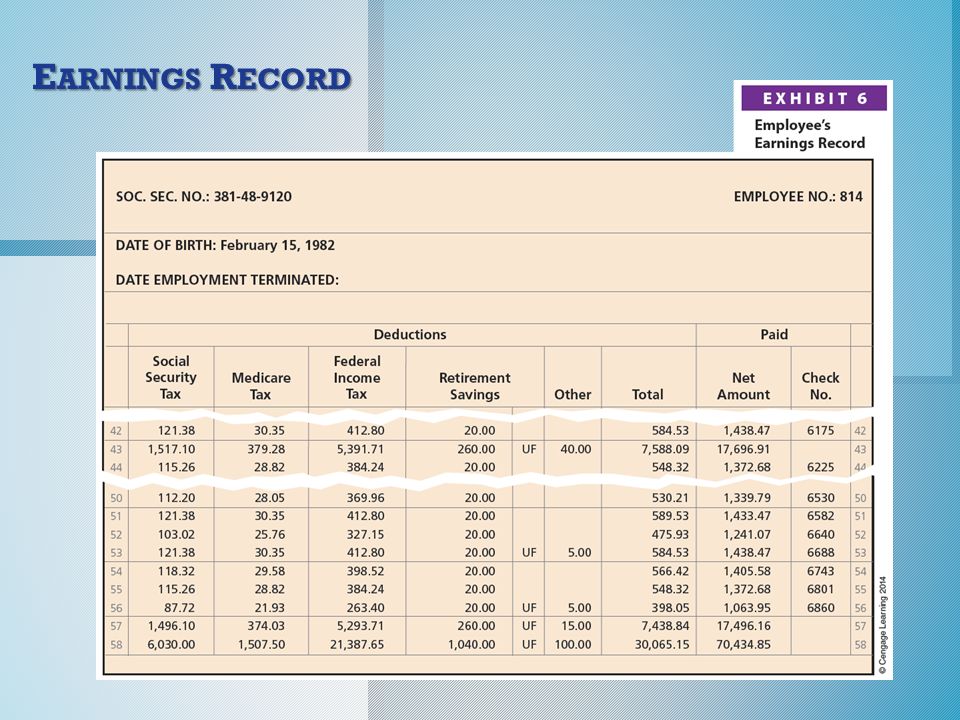

Employee’s Earnings Record o A detailed payroll record must be kept for each employee. This record is called an employee’s earnings record. Exhibit 6 (next two slides) shows a portion of John T. McGrath’s employee’s earnings record.

shows a portion of John T. McGrath’s employee’s earnings record..")

46

E ARNINGS R ECORD

48

E MPLOYEE ’ S E ARNINGS R ECORD

49

Payroll Checks o At the end of each payroll period, payroll checks are prepared. Each check includes a detachable statement showing the details of how the net pay was computed.

50

P AYROLL C HECK

51

Payroll System Design o The inputs into a payroll system may be classified as: Constants, which are data that remain unchanged from payroll to payroll. Employee names Employee names Social security numbers Social security numbers Variables, which are data that change from payroll to payroll. Number of hours or days worked Number of hours or days worked Accrued sick leave Accrued sick leave

52

Internal Controls for Payroll Systems o Some examples of payroll controls include the following: If a check-signing machine is used, blank payroll checks and access to the machine should be restricted to prevent their theft or misuse. The hiring and firing of employees should be properly authorized and approved in writing. (continued)

.")

53

Internal Controls for Payroll Systems All changes in pay rates should be properly authorized and approved in writing. Employees should be observed when arriving for work to verify that employees are “checking in” for work only once and only for themselves. Payroll checks should be distributed by someone other than employee supervisors. A special payroll bank account should be used.

54

c. 2014 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, or posted to a publicly accessible website, in whole or in part. Learning Objective Journalize entries for employee fringe benefits, including vacation pay and pensions. 4

55

Employees’ Fringe Benefits o Many companies provide their employees benefits in addition to salary and wages earned. Such fringe benefits may include: Vacation pay (sometimes called compensated absences) Medical benefits Retirement benefits

Medical benefits Retirement benefits.")

56

Vacation Pay o Assume that employees earn one day of vacation for each month worked. The estimated vacation pay for the year ending December 31 is $325,000. The adjusting entry for the accrued vacation is shown below.

57

Pensions o A pension is a cash payment to retired employees. Pension rights are accrued by employees as they work, based on the employer’s pension plan. Two types of pension plans are: Defined contribution plan Defined benefit plan

58

Pensions o In a defined contribution plan, the company invests contributions on behalf of the employee during the employee’s working years. Normally, the employee and employer contribute to the plan. The employee’s pension depends on the total contributions and the investment returns earned on those contributions.

59

Pensions o Heaven Scent Perfumes Company contributes 10% of employee monthly salaries to an employee 401K plan. Assuming $500,000 of monthly salaries, the journal entry to record the monthly contribution is shown below.

60

Pensions o In a defined benefit plan, the employer is obligated to pay for (fund) the employee’s future pension benefits. Many companies are replacing their defined benefit plans with defined contribution plans. A retired employee receives a specific amount based on his or her salary history and years of service.

61

Pensions o The defined benefit plan of Hinkle Co. requires an annual pension cost of $80,000. The annual contribution is based on estimates of Hinkle’s future pension liability. On December 31, Hinkle Co. pays $60,000 to the pension fund. The entry to record the payment and unfunded liability is shown below.

62

Postretirement Benefits Other than Pensions o Employees may earn rights to other postretirement benefits, such as dental care, eye care, medical care, life insurance, tuition assistance, tax services, and legal services.

63

C URRENT L IABILITIES ON THE B ALANCE S HEET

64

c. 2014 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, or posted to a publicly accessible website, in whole or in part. Learning Objective Describe the accounting treatment for contingent liabilities and journalize entries for product warranties. 5

65

Contingent Liabilities o Some liabilities may arise from past transactions if certain events occur in the future. These potential obligations are called contingent liabilities. The accounting for contingent liabilities depends on the following two factors: Likelihood of occurring: Probable, reasonably possible, or remote Measurement: Estimable or not estimable

66

Contingent Liabilities o During June, a company sold a product for $60,000 that includes a 36-month warranty for repairs. The average cost of repairs over the warranty period is 5% of the sales price. The entry to record the estimated product warranty expense for June is shown below.

67

Contingent Liabilities o If a $200 part is replaced under warranty on August 16, the entry is as follows:

68

C ONTINGENT L IABILITIES

69

c. 2014 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, or posted to a publicly accessible website, in whole or in part. Learning Objective Describe and illustrate the use of the quick ratio in analyzing a company’s ability to pay its current liabilities. 6

70

Quick Ratio o Current position analysis helps creditors evaluate a company’s ability to pay its current liabilities. It is based on: Working capital, the excess of current assets over current liabilities Current ratio, determined by dividing the current assets by the current liabilities Quick ratio, an indicator of a company’s short-term liquidity

71

Quick Ratio o The quick ratio measures the “instant” debt- paying ability of a company and is computed as follows: o Quick assets are cash and other current assets that can be easily converted to cash. Quick Ratio = Quick Assets Current Liabilities

72

c. 2014 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, or posted to a publicly accessible website, in whole or in part. Current Liabilities and Payroll The End

Similar presentations