Download presentation

Presentation is loading. Please wait.

1

More on Nonprofit Financial Statements Webinar 2

2

Today’s Session Topics Cash and accrual basis of accounting Fiduciary and financial reporting requirements for restricted resources Review of Pilgrim Services Society financial statements

3

3 Cash vs. Accrual Accounting Cash basis recognizes: – Revenues when cash received – Expenses when cash is paid Used by individuals, some small businesses and nonprofits Benefits – Easy to implement – Easy for a third party to verify Costs – Can misrepresent the financial condition, activities and cash flows of an organization Cash basis of accounting is not permitted under GAAP.

4

What’s Wrong with the Cash Basis – An Example The Situation: Ann has a new job with a salary of $50K: she bought a new car for $20K with an auto loan: and used her new credit cards to cover all her expenses ($25K) except her rent ($20K) which she paid for the year.

except her rent ($20K) which she paid for the year.")

5

5 Revenue Recognition – Accrual Basis Under accrual accounting, revenue is recognized when two key criteria are met: –Revenue is EARNED The critical event in process of earning revenue has taken place – a service is performed, goods are provided, ownership is transferred, etc. –Revenue is MEASURABLE Amount to be collected is reasonably assured and can be measured with a fair degree of reliability “Net realizable value”

6

6 Expense Recognition – Accrual Accounting Under the accrual basis –Recognize expenses when “incurred” and “measurable” when benefit has been received or liability incurred Work has been performed by employees Food has been ordered and received for cafeteria –Matching principle applies – expenses are recognized when related revenue is recognized

7

Accrual Basis of Accounting Required under GAAP Cash can be received before or after revenue and expense is recorded Benefits –Reflects ultimate financial performance and position irrespective of cash payments or receipts Cons –More difficult and costly to maintain –Relies heavily on estimations and judgments Modified Accrual basis is a compromise for small, international or developing NGOs 7

8

Practical Compromise Size or development stage of nonprofits may limit ability to fully implement accrual accounting – particularly international NGOs Cash basis of accounting is used by some NGOs in developing countries Modified accrual basis of accounting is a reasonable compromise: – Cash basis of accounting used for monthly or internal reporting – Conversion to accrual basis done for audit, or for monthly/quarterly/annual financials – External accountant used for accrual adjustments Restricted funds must be separately accounted for in all cases.

9

9 Asset in Accrual Accounting Accounts Receivable - revenue recognized in advance of cash being received Prepaid Expenses - advance payments Inventory - supplies acquired before use Fixed assets - purchase that will benefit multiple future periods for buildings, equipment Depreciation expense – annual “use” of fixed assets

10

10 Liabilities in Accrual Accounting Accounts payable to reflect expenses not yet paid for Deferred revenue to reflect revenue received but not yet earned Notes payable - borrowings that must be repaid Long term obligations - pension

11

Revenues, Expenses, Assets or Liabilities???? Purchase of supplies to be used in next year Payment of salaries for current month Receipt of subscriptions for a magazine for 3 years Receipt of unrestricted gift 11

12

Valuation Concepts – Assets and Liabilities Assets are generally recorded at the lower of cost or market value – or net realizable values Investments are recorded at market value Fixed assets are recorded at cost less depreciation Accounts receivable (and pledges) are recorded at net realizable value (net of allowance for uncollectible accounts) Liabilities are recorded at amounts expected to be paid Assets and liabilities are periodically adjusted to reflect changes in values due to: – New circumstances (market values, sales) – Use in the operations (fixed assets, deferred revenue) 12

are recorded at net realizable value (net of allowance for uncollectible accounts) Liabilities are recorded at amounts expected to be paid Assets and liabilities are periodically adjusted to reflect changes in values due to: – New circumstances (market values, sales) – Use in the operations (fixed assets, deferred revenue) 12")

13

13 Capitalization vs. Expense A Cost can be expensed immediately or deemed an asset. If an asset, it is stored on the balance sheet until it is expensed or used up. To recognize/capitalize an asset, it must meet two criteria: 1. Rights Acquired Rights to future benefits have been acquired in a transaction 2. Measurable Benefits are in the future and can be estimated with reasonable certainty

14

14 Purchasing a Computer A computer is purchased for $10K today that will be used for 5 years – Right Now Fixed Asset is recorded– this resource will benefit the future (Asset increase) Cash is reduced (Asset decreased) – As asset is used over time Expense is recognized for $2K in each year of use (Expense Increased) The value of the fixed asset is “depreciated” (Asset decreased) Fixed assets show net undepreciated or remaining value – Generally Costs to maintain an asset’s benefits are expensed Costs to increase an asset’s benefits are capitalized

Cash is reduced (Asset decreased) – As asset is used over time Expense is recognized for $2K in each year of use (Expense Increased) The value of the fixed asset is depreciated (Asset decreased) Fixed assets show net undepreciated or remaining value – Generally Costs to maintain an asset’s benefits are expensed Costs to increase an asset’s benefits are capitalized")

15

Fixed Asset Accounting YearFixed Asset (original cost) Accumulated Depreciation (annual accumulation) Net Fixed Asset (Balance Sheet) Depreciation Expense (Activity Statement 110000200080002000 210000400060002000 310000600040002000 41000080002000 510000 02000

Accumulated Depreciation (annual accumulation) Net Fixed Asset (Balance Sheet) Depreciation Expense (Activity Statement")

16

Accounting for Debt Debt includes two components: – Principal = amount borrowed less payments to date – Interest = annual expense to reflect cost of borrowing at stated rate applied to principal balance Accounting for Payments: – Principal payments reduce liability – Interest payments increase expense (cost of borrowing)

")

17

Accounting for Debt Year Cash Activity Balance Sheet Debt Activity Balance Sheet Debt Balance Balance Sheet Interest Expense Activity Statement 1 4500050000 5000 2(14000)(10000)400004000 3(13000)(10000)300003000 4(12000)(10000)200002000 5(11000)(10000)100001000 6(10000) -- Net Impact $15k less cash net 50k Borrowed$50k Repaid $15k cost of borrowing

(10000) (13000)(10000) (12000)(10000) (11000)(10000) (10000) -- Net Impact $15k less cash net 50k Borrowed$50k Repaid $15k cost of borrowing")

18

18 Importance of Estimates Assets and liabilities recorded at expected ultimate realizable value Major areas of estimation in nonprofit organizations: – Accounts receivable – Pledges receivable – Investments (next class) Judgments are required to reflect appropriate values in financial statements

Judgments are required to reflect appropriate values in financial statements")

19

19 A Telemarketing Campaign As a result of a telemarketing campaign, 1,000 people promise to contribute $50 each to an NFP in February. Historically 4% of donors fail to pay. NFP records revenue now for: – $50K as a receivable (asset and revenue increase) – Less uncollectible bad debt of $2K (reduction of asset and an increase to expense)

– Less uncollectible bad debt of $2K (reduction of asset and an increase to expense).")

20

Patient Accounts Receivable Services to patients total $100K which have not yet been collected Assessment of age and payment source shows 25% uncollectible experience Receivable and revenue recorded for $100K Allowance for uncollectibles of $25K is recorded to reduce receivable to net collectible amount with bad debt expense of $25K 20

21

Importance of Footnotes Notes to Financial Statements add critical data and insight: – Details accounting policies and practices – “GAAP summary” – Detail on financial statement components – investments, fixed assets, debt – Highlight financial matters not included in the numbers – uncertainties, contingencies, estimates Audited financial statements are required to contain such disclosures

22

New Resource – Khan Academy You Tube Educational Videos – Thousands of Topics Try these (listed under “Finance” category: – Cash Accounting – Accrual Accounting – Comparing Cash and Accrual Accounting – Balance Sheet and Income Statement Relationship – Basic Cash Flow Statement 22

23

Accounting for Restricted Resources Gifts or resources are provided which contain restrictions as to use NFPs have a fiduciary responsibility to record and account for these resources through “fund accounting” – identifying revenues, expenses, and net assets separately in the accounting records Financial statements must disclose nature and activity of net asset categories (“funds”) Three types of funds (net assets): – Unrestricted net assets – Temporarily restricted net assets – Permanently restricted net asssets 23

Three types of funds (net assets): – Unrestricted net assets – Temporarily restricted net assets – Permanently restricted net asssets 23")

24

Unrestricted Net Assets Unrestricted net assets are the resources available for use in accordance with the general purposes of the NFP Also called: – Operating funds – General fund Board designated funds are unrestricted funds which have been designated by the board for a specific purpose – Whatever a board designates, it can undesignate 24

25

Temporarily Restricted Funds Temporarily restricted funds are resources given to the NFP which contain either time or use restrictions Temporarily restricted funds include: Restricted grants and contracts Funds for specific purposes Pledges receivable which are due in more than one year – an implicit time restriction When restrictions are met, amounts are released through a transfer to unrestricted funds 25

26

Permanently Restricted Funds 26 Permanently restricted funds are resources given to a NFP which require that the principal (corpus) be invested in perpetuity with the income used for restricted or unrestricted purposes Permanently restricted funds – Are also called Endowment Funds – Realized and unrealized gains are usually classified as temporarily restricted funds or unrestricted funds – depending upon state legislation

be invested in perpetuity with the income used for restricted or unrestricted purposes Permanently restricted funds – Are also called Endowment Funds – Realized and unrealized gains are usually classified as temporarily restricted funds or unrestricted funds – depending upon state legislation")

27

27

28

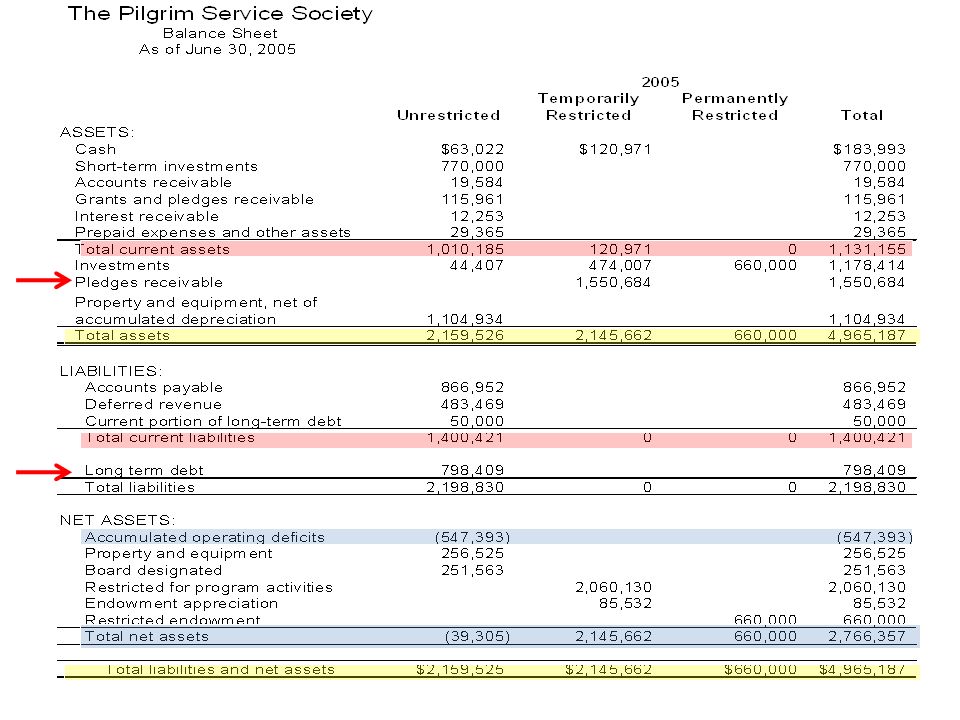

Pilgrim Services Society “Road Map” Gain further understanding of financial statement information Realize importance of “Notes to Financial Statements” Begin analysis of financial information

30

30

31

31

32

Other Questions? Growing vibrant organization? Dependence or risk on certain revenues? Overall capital structure? Other risks? What else would you want to look at before you gave PSS a grant or a loan? 32

Similar presentations