Download presentation

Presentation is loading. Please wait.

1

Shelby County Down Payment Assistance Program NACCED Presentation September 2011

2

Shelby County Down Payment Assistance Program Created in late 2006 as a revolving loan pool through a partnership between Shelby County Government and the State of Tennessee. Created in late 2006 as a revolving loan pool through a partnership between Shelby County Government and the State of Tennessee. Specifically the Department of Housing and the Tennessee Housing Development Agency (THDA) Specifically the Department of Housing and the Tennessee Housing Development Agency (THDA)

Specifically the Department of Housing and the Tennessee Housing Development Agency (THDA).")

3

Shelby County Down Payment Assistance Program The original funding pool came from interest paid on old bonds issued by Shelby County and the State in 1990’s. The original funding pool came from interest paid on old bonds issued by Shelby County and the State in 1990’s. 70% of the pool provided by the State 70% of the pool provided by the State 30% of the pool provided by Shelby County 30% of the pool provided by Shelby County

4

Shelby County Down Payment Assistance Program In addition to the original pool, fees were established and collected on permits issued by Shelby County Code Enforcement. In addition to the original pool, fees were established and collected on permits issued by Shelby County Code Enforcement. Funds generated are used to operate the program and build on the revolving loan fund. Funds generated are used to operate the program and build on the revolving loan fund.

5

Shelby County Down Payment Assistance Program Permit Fees consist of: Permit Fees consist of: $1 for each residential permit issued. $1 for each residential permit issued. $5 for each commercial permit issued. $5 for each commercial permit issued. $5 for each sign permit issued/renewed. $5 for each sign permit issued/renewed. Average generated per year from fees $114,300.00 Average generated per year from fees $114,300.00

6

Shelby County Down Payment Assistance Program Original available loan pool: $ 3.3 Million Original available loan pool: $ 3.3 Million (in 2006) Current Available loan pool: $ 2.3 Million Current Available loan pool: $ 2.3 Million (in 2011) (in 2011) Total Loans Made: $ 2.3 Million Total Loans Made: $ 2.3 Million (2006-2011) (2006-2011)

Current Available loan pool: $ 2.3 Million Current Available loan pool: $ 2.3 Million (in 2011) (in 2011) Total Loans Made: $ 2.3 Million Total Loans Made: $ 2.3 Million ( ) ( )")

7

Type of Assistance Provided Assistance is in the form of a 5% loan for down payment and closing costs associated with the purchase of a home. Assistance is in the form of a 5% loan for down payment and closing costs associated with the purchase of a home. Loan amount:Up to $ 3,500.00 Loan amount:Up to $ 3,500.00 Term:Up to 10 years/120 months Term:Up to 10 years/120 months Monthly Payment:$ 37.12 for 120 months* Monthly Payment:$ 37.12 for 120 months* * for maximum loan.

8

Eligibility Requirements Unit purchased must be located in Shelby County and be the primary residence. Unit purchased must be located in Shelby County and be the primary residence. Unit may be either existing or a newly constructed unit Unit may be either existing or a newly constructed unit Homebuyer must qualify for a THDA, FHA, VA, or Conventional Mortgage. Homebuyer must qualify for a THDA, FHA, VA, or Conventional Mortgage.

9

Eligibility Requirements Homebuyer(s) must invest a minimum of $500 of their own savings for closing. Homebuyer(s) must invest a minimum of $500 of their own savings for closing. Homebuyer(s) must attend a homebuyer counseling class. Homebuyer(s) must attend a homebuyer counseling class. The purchase price of the unit must be less than $200,160.00. The purchase price of the unit must be less than $200,160.00.

must invest a minimum of $500 of their own savings for closing. Homebuyer(s) must attend a homebuyer counseling class. Homebuyer(s) must attend a homebuyer counseling class. The purchase price of the unit must be less than $200, The purchase price of the unit must be less than $200,")

10

Eligibility Requirements Ratio for Approval of DPA funds: Ratio for Approval of DPA funds: Front end: Cannot exceed 33% Front end: Cannot exceed 33% (Monthly housing expense/stable income) Back end: Cannot exceed 43% Back end: Cannot exceed 43% (Monthly housing expense + debt/stable income) (Monthly housing expense + debt/stable income)

Back end: Cannot exceed 43% Back end: Cannot exceed 43% (Monthly housing expense + debt/stable income) (Monthly housing expense + debt/stable income)")

11

Eligibility Requirements Household Income Levels: Household Income Levels: 1 to 2 Person Household 1 to 2 Person Household Minimum $ 26,100.00 Minimum $ 26,100.00 Maximum $ 68,439.00 Maximum $ 68,439.00 3 or More person Household 3 or More person Household Minimum $ 26,100.00 Minimum $ 26,100.00 Maximum $ 78,704.00 Maximum $ 78,704.00

12

Eligibility Requirements Purchaser must agree to a Deed of Trust Restriction being recorded on the home at closing. Purchaser must agree to a Deed of Trust Restriction being recorded on the home at closing. Purchaser may not at any time lease the property and such language must be included in all loan documents. Purchaser may not at any time lease the property and such language must be included in all loan documents. Purchaser must sign to a Promissory Note which also incorporates all requirements of the loan. Purchaser must sign to a Promissory Note which also incorporates all requirements of the loan.

13

Eligible Closing Costs 1. Origination Fee (1%) 2. One repair inspection 3. One lender inspection 4. Compliance/Final Inspection 5. Engineer’s Certificate 6. Pest Inspection 7. Closing/Settlement, Deed of Trust, Note Preparation 8. Amortization Schedule 9. Title Examination 10. Title Insurance 11. Credit Report 12. Survey 13. Recording 14. Notary 15. Attorney’s fee not to exceed $200 16. Allowable Pre-pays 17. Insurance

14

Resale Provision All loans contain a resale provision which requires payoff of the unpaid balance when the property is: All loans contain a resale provision which requires payoff of the unpaid balance when the property is: Sold, Sold, Transferred, or Transferred, or Leased. Leased.

15

Prepayment Loan balances may be paid off at any time. There is no penalty for the prepayment of the DPA loan prior to the maturity date. There is no penalty for the prepayment of the DPA loan prior to the maturity date.

16

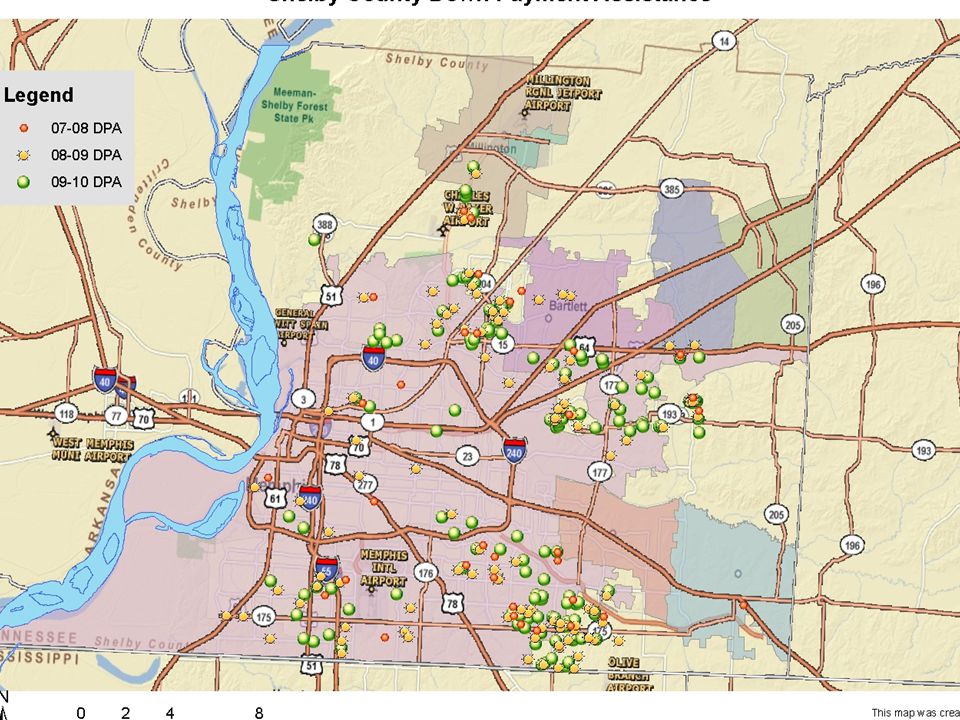

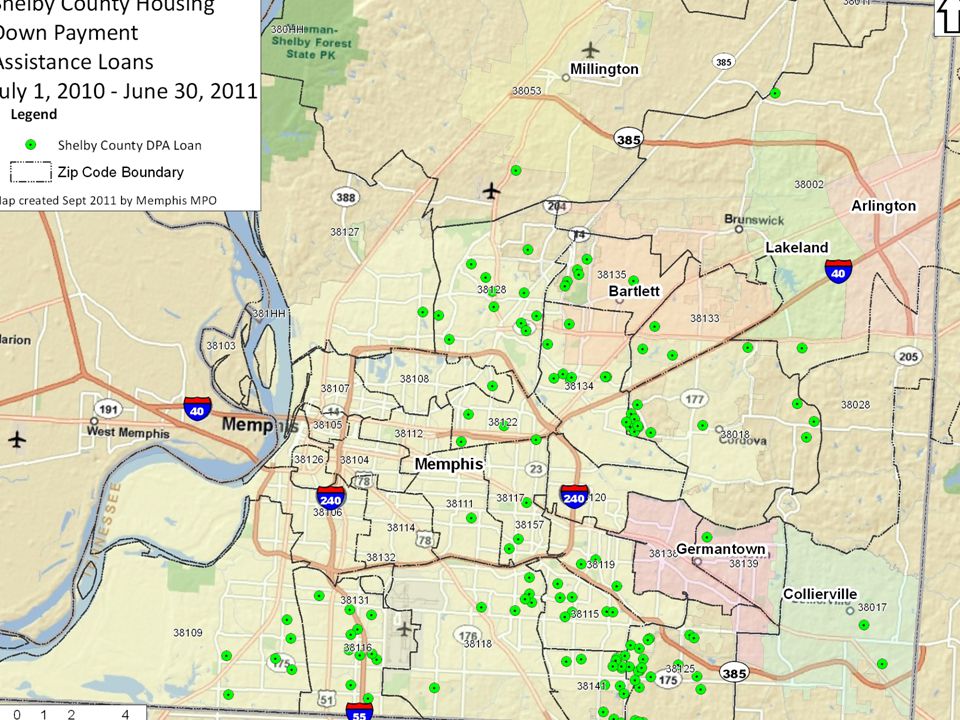

Loans By Fiscal Year # of loans Dollars Loans Average Loan # of loans Dollars Loans Average Loan 2006:18$ 57,658 $ 3,203 2006:18$ 57,658 $ 3,203 2007:18$ 57,020$ 3,168 2007:18$ 57,020$ 3,168 2008:39$ 124,588$ 3,195 2008:39$ 124,588$ 3,195 2009:153$ 505,047$ 3,301 2009:153$ 505,047$ 3,301 2010:311$ 1,018,646$ 3,275 2010:311$ 1,018,646$ 3,275 2011:153$ 483,447$ 3,160 2011:153$ 483,447$ 3,160 692$ 2,246,406$ 3,246

19

Average Tax Rates (January 1, 2006 – 6/30/2011) Annual Property Tax Rates: Shelby County$4.02 (Memphis) $4.06 (Non-Memphis) Municipalities* Municipalities* Memphis$3.19 Arlington$1.00 Bartlett$1.49 Collierville$1.43 Germantown$1.48 Millington$1.23 * Overall Average Municipal Rate: $1.63

Annual Property Tax Rates: Shelby County$4.02 (Memphis) $4.06 (Non-Memphis) Municipalities* Municipalities* Memphis$3.19 Arlington$1.00 Bartlett$1.49 Collierville$1.43 Germantown$1.48 Millington$1.23 * Overall Average Municipal Rate: $1.63")

20

Estimated Taxes Generated (Since January 2006) Average Mortgage Loan: $ 94,698.00 Shelby County Taxes:$ 1,511,331.36 City/Municipal Taxes:$ 612,809.20 Total in Shelby County:$ 2,124,140.56

Average Mortgage Loan: $ 94, Shelby County Taxes:$ 1,511, City/Municipal Taxes:$ 612, Total in Shelby County:$ 2,124,140.56")

21

Annual DPA Income Loans & Fees MonthlyAnnually Average repayments$13,370$160,440 Average from permit fees$ 9,525$114,300 Total revenue collected*$ 22,895$274,740 * Average as of 6/30/2011

22

Obstacles In Implementing Household Income Limits Household Income Limits Slow start due to income qualifications. Slow start due to income qualifications. Originally, the program was set up to mirror income by household size under the federal guidelines which resulted a high volume of non-qualifying applicants. (Buyers were pigeonholed.) Because no Federal funds are involved, a change to State household limits resolved this issue by freeing up the restricted income levels and provided a wider income range. Because no Federal funds are involved, a change to State household limits resolved this issue by freeing up the restricted income levels and provided a wider income range.

Because no Federal funds are involved, a change to State household limits resolved this issue by freeing up the restricted income levels and provided a wider income range. Because no Federal funds are involved, a change to State household limits resolved this issue by freeing up the restricted income levels and provided a wider income range..")

23

Obstacles In Implementing Shelby County’s Finance Department Shelby County’s Finance Department How to issue/cut Down Payment Checks? How to issue/cut Down Payment Checks? Originally, Finance wanted W-9’s and Vendor numbers for each Homeowner receiving assistance. Originally, Finance wanted W-9’s and Vendor numbers for each Homeowner receiving assistance. Finally, resolved by agreeing that the lender had to be set up as a Shelby County vendor and the check was cut to the closing attorney on behalf of the buyer. Finally, resolved by agreeing that the lender had to be set up as a Shelby County vendor and the check was cut to the closing attorney on behalf of the buyer.

24

Obstacles In Implementing Shelby County Finance Department Shelby County Finance Department Time line for issuing checks and method. Time line for issuing checks and method. County policy required checks to be mailed (no County employee can handle the check) and turnaround time was set at 30 days. County policy required checks to be mailed (no County employee can handle the check) and turnaround time was set at 30 days. Negotiated a system whereby checks could be walked through in 10 days and picked up and delivered by a Dept. of Housing staff person. Negotiated a system whereby checks could be walked through in 10 days and picked up and delivered by a Dept. of Housing staff person.

and turnaround time was set at 30 days. County policy required checks to be mailed (no County employee can handle the check) and turnaround time was set at 30 days. Negotiated a system whereby checks could be walked through in 10 days and picked up and delivered by a Dept. of Housing staff person. Negotiated a system whereby checks could be walked through in 10 days and picked up and delivered by a Dept. of Housing staff person..")

25

Obstacles In Implementing Finding A Loan Servicing Agent: Finding A Loan Servicing Agent: Selection of a Loan Servicer to handle the loans. Selection of a Loan Servicer to handle the loans. We could not find anyone willing to service such a small loan portfolio at a reasonable cost. Issued numerous RFPs This was resolved when a Tallahassee, FL company made inquiry after seeing the RFP. They ended up securing licensing through the State of TN and ended up becoming The successful respondent. Cost of servicing is $8 per loan.

26

Contacts For More Information Jim Vazquez, Administrator901-379-7102 jim.vazquez@shelbycountytn.gov Israel Henry, Finance Manager 901-379-7116 israel.henry@shelbycountytn.gov Wanda Chambers, DPA Specialist901-379-7100 wanda.chambers@shelbycountytn.gov

Similar presentations

249-1800,>")

Orange County, Florida.>")

(adapted from AARP information)>")

Program Presented By: City of Decatur Community Development Department.>")