Download presentation

Presentation is loading. Please wait.

1

Year-End Closing of the Books 2013-2014

2

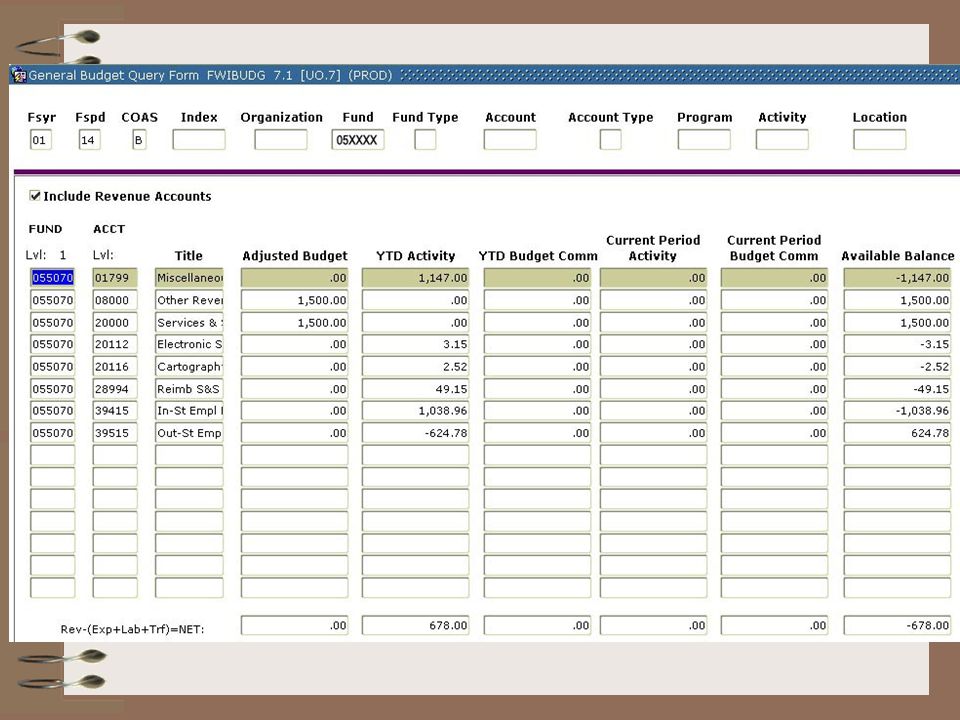

Overview of Closing: Why? GAAP – Generally Accepted Accounting Principles End of the business cycle: State sessions end in June UO activity begins with summer session (excluding Law) Federal (GASB) & State (OUS) requirements OUS has a number of mandated deadlines Snapshot in time YTD activity (FWIBUDG) and year-end balances (FGITBAL) are used to monitor, project, budget, evaluate performance, perform system audits, analyze anomalies, audit, compare and contrast with other years/funds/institutions etc…

Federal (GASB) & State (OUS) requirements OUS has a number of mandated deadlines Snapshot in time YTD activity (FWIBUDG) and year-end balances (FGITBAL) are used to monitor, project, budget, evaluate performance, perform system audits, analyze anomalies, audit, compare and contrast with other years/funds/institutions etc….")

3

Overview of Closing: Why? Annual reporting – internal & external Rolled into OUS and State financial statements Used by stakeholders such as general public, federal agencies, SBHE, federal F&A rate setters, accrediting agencies, NCAA, creditors and bond services, etc… Auditors – internal & external Test for accuracy, consistency, & reliability of systems including our policies & procedures Help us establish best practices Includes: OUS Internal Audit, DHHS, Naval Research, NCAA, Clifton Larson Allen (financial statement & A-133), Secretary of State, etc… Establish beginning balances for FY15

, Secretary of State, etc… Establish beginning balances for FY15.")

4

Overview of Closing What? Recording activity that takes place between: July 1, 2013 and June 30, 2014 Transactions must be recorded in the fiscal year that the event takes place, not when it is processed Includes accruals posted by July 22, 2014 Applies to all funds in FIS regardless of the source

5

Overview of Closing What? Close fiscal period 12 and open fiscal period 14 Fiscal period 12: Record June and remaining FY14 activity Fiscal period 14: Review and post necessary corrections/accruals Departments have first week BAO/BRP/SPS have additional week Close fiscal period 14 (FY14) OUS extracts our data & populates the HFM System UO reports any FY14 transactions to OUS through the date financial statements are issued in November

OUS extracts our data & populates the HFM System UO reports any FY14 transactions to OUS through the date financial statements are issued in November.")

6

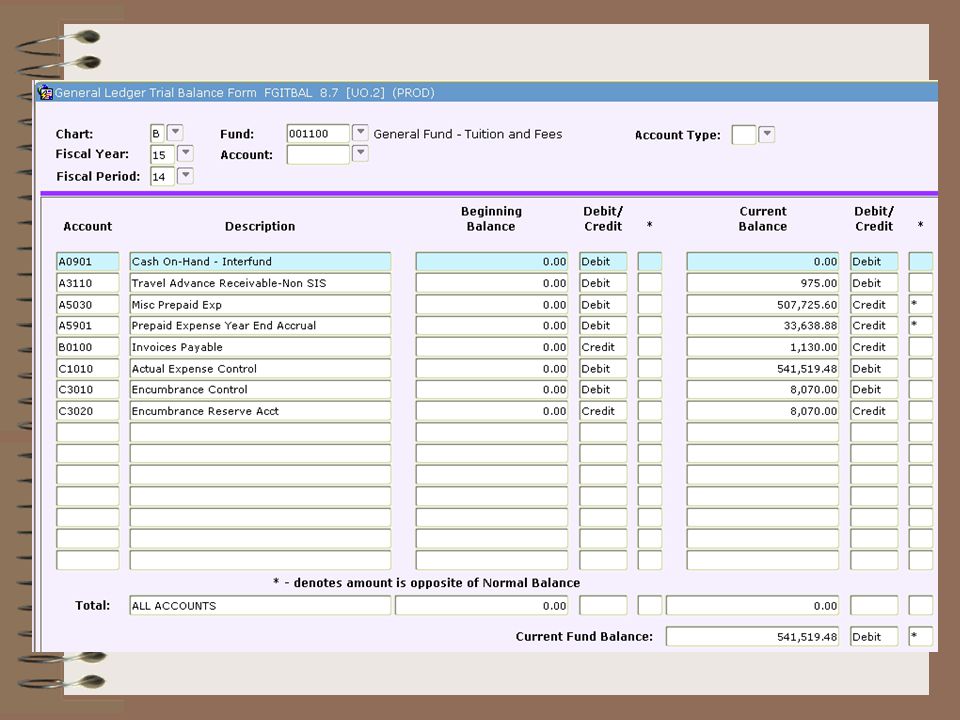

Balance Sheet Account Codes (FGITBAL – General Ledger) A = Assets B = Liabilities C = Control Accounts (Income Statement Totals) D = Fund Balance E = Fund Additions F = Fund Deletions When FP12 is closed and FP14 is opened, actual income/expense account balances from FY14 FP12 are closed into FY15 fund balance.

A = Assets B = Liabilities C = Control Accounts (Income Statement Totals) D = Fund Balance E = Fund Additions F = Fund Deletions When FP12 is closed and FP14 is opened, actual income/expense account balances from FY14 FP12 are closed into FY15 fund balance.")

7

Income Stmt/Balance Sheet FWIBUDGFGITBAL Income StmtBalance Sheet Revenue0XXXXC0010 Labor1XXXXC2010 General Expense 2XXXX- 8XXXX C1010 Transfers9XXXXC5010 Fund BalD0010

10

FY15 Beginning Balances Before period 14 is opened, FY15 balances only include FY15 transactions When period 14 is opened, FY14 period 12 ending balances become FY15 beginning balances (recorded in FP00) Then, each entry posted to FY14 during period14 has a mirror entry in FY15 FP00

Then, each entry posted to FY14 during period14 has a mirror entry in FY15 FP00")

12

Subsidiary Ledgers Provide a greater amount of detailed information FIS Examples – Student A/R, Grants Billing Module, Fixed Asset System, Accounts Payable Complimentary (shadow) systems are often used by departments as subsidiary ledgers (examples – QuickBooks, Excel, Access) Subsidiary ledgers must be reconciled to Banner FIS The FIS general ledger is the official source of financial information for the UO

systems are often used by departments as subsidiary ledgers (examples – QuickBooks, Excel, Access) Subsidiary ledgers must be reconciled to Banner FIS The FIS general ledger is the official source of financial information for the UO")

13

Subsidiary Ledger General ledger account codes require supporting detail schedules reconciled to Banner FIS. Commonly used accounts include: A3103 – Misc A/R A3106 – Sundry Receivable A3702 – AR from Affiliated Foundation A4002 – Organized Storeroom Inventories A5030 – Misc Prepaid Expense A5901 – Prepaid Expense Year End Accrual B0101 – Year End A/P Accrual B0190 – Received Items Payable B5802 – Misc Undistributed Income B5901 – Accrued Undistributed Income

14

Dates to Remember: June 6 June regular payroll deadline June 17 Contact BAO for help accruing department non-student accounts receivable June 30 Last day to submit student receivables June 30 Last day to deposit cash by 3:00 p.m. June 30 Goods and services must be received by this date to pay with FY14 funds July 2 Last day to submit payroll form (PAA) for FY14 July 7 Last day to direct input Inter-Institutional JVs (Charts B-K) for Period 12 **(Items input in July require a 30-JUN-2014 transaction date)**

for FY14 July 7 Last day to direct input Inter-Institutional JVs (Charts B-K) for Period 12 **(Items input in July require a 30-JUN-2014 transaction date)**.")

15

Dates to Remember: July 7 Last day to submit upload JVs for period 12 (Z documents through AppWorx) July 8 Last day to liquidate encumbrances that shouldn’t roll to FY15 July 8 Last day to submit budget changes for Period 12 July 8 Last day to input an invoice for Period 12 July 8 Last day to input JVs for Period 12 July 8 Period 12 Close (5:00 p.m.) July 9 Period 12 reports are available ** (Items input in July require a 30-JUN-2014 transaction date)**

July 8 Last day to liquidate encumbrances that shouldn’t roll to FY15 July 8 Last day to submit budget changes for Period 12 July 8 Last day to input an invoice for Period 12 July 8 Last day to input JVs for Period 12 July 8 Period 12 Close (5:00 p.m.) July 9 Period 12 reports are available ** (Items input in July require a 30-JUN-2014 transaction date)**")

16

Dates to Remember: July 8 Last day to direct input Inter-Institutional JVs (Charts B-K) for Period 14 July 15 Last day to input JVs for Period 14 July 15 Last day to input budget changes for Period 14 July 15 Last day to input an invoice for Period 14 July 15 Campus lock out (5:00 p.m.) For assistance with FY14 transactions after the lock-out, contact BAO General Accounting **(Items input in July require a 30-JUN-2014 transaction date)**

for Period 14 July 15 Last day to input JVs for Period 14 July 15 Last day to input budget changes for Period 14 July 15 Last day to input an invoice for Period 14 July 15 Campus lock out (5:00 p.m.) For assistance with FY14 transactions after the lock-out, contact BAO General Accounting **(Items input in July require a 30-JUN-2014 transaction date)**")

17

Dates to Remember: July 16 Detail and aging reports due for all non-SIS accounts receivable July 18 Last day to submit IIJVs to BAO July 22 Last day to submit year-end AP Reports July 22 Period 14 Close (FY14) July 23 Period 14 reports are available **(Items input in July require a 30-JUN-2014 transaction date)**

July 23 Period 14 reports are available **(Items input in July require a 30-JUN-2014 transaction date)**")

18

Expenditure Cut-Off Guidelines According to Generally Accepted Accounting Principles (GAAP), accrual accounting requires expenditures to be charged to the fiscal year and period in which goods are received or services are performed, regardless of when budget or cash is available. For goods and services received by June 30 for which vendor invoices have not been received as of July 22, fill out an AP Report and forward it to BAO Financial Services http://ba.uoregon.edu/sites/ba/files/forms/yearendap. pdfhttp://ba.uoregon.edu/sites/ba/files/forms/yearendap. pdf

19

Year End Accruals Prepaid Expense - A5901 Expenses for future fiscal years that are paid prior to June 30, 2014 should be coded to A5901. Post a reversing journal voucher with a transaction date in the future fiscal year and period that the goods or services will be received. This journal voucher may be processed at the same time, if the future period is open. For amounts posted as expense in FY14, that should be prepaid expenses for future years: Debit Department Index A5901 - Prepaid Expense Credit Department Index Expense Account Code - ex. 39515 Out-St Travel To remove the prepaid and recognize the expense in the future year: Debit Department Index Expense Account Code - ex. 39515 Out-St Travel Credit Department Index A5901 - Prepaid Expense

20

Year End Accruals Accrued Income - B5901 Revenue must be credited to the fiscal year that the goods or services will be provided. Revenue for future fiscal years that is received prior to June 30, 2014 should be coded to B5901. Post a reversing journal voucher with a transaction date in the future fiscal year and period that the goods or services will be provided. This journal voucher may be processed at the same time, if the future period is open. For amounts posted as revenue in FY14, that should be prepaid revenue for future years: Debit Department Index Revenue Account Code - ex. 01102 Nonresident Undergrad Tuition Credit Department Index B5901 - Accrued Undistr Income To remove the prepaid and recognize the revenue in the future year: Debit Department Index B5901 - Accrued Undistr Income Credit Department Index Revenue Account Code - ex. 01102 Nonresident Undergrad Tuition

21

Non-SIS Accounts Receivable Each department must submit a detail and aging report of their non-SIS accounts These reports must be reconciled to Banner as of period 14 (use FGITBAL) Includes all receivables from entities that are external to OUS institutions

Includes all receivables from entities that are external to OUS institutions")

22

Non-SIS Accounts Receivable

23

Dating FIS Documents After June 30 th, any document input for FY14 must have the transaction date changed to 30-JUN-2014 This includes: Budget changes Invoices JVs Travel reimbursements

24

Encumbrances All open encumbrances (except zero balance items) will be rolled into FY15 Banner FIS operating ledger Liquidate any encumbrances that you do not want to roll into FY15 before the close of period 12 (July 8th)

will be rolled into FY15 Banner FIS operating ledger Liquidate any encumbrances that you do not want to roll into FY15 before the close of period 12 (July 8th)")

25

Late FY14 and Subsequent Event Reporting Report FY14 activity and subsequent events to BAO Financial Services as follows: July 16 - 22 – for posting into Banner FIS during lock-out July 23 - September – to be included in OUS Financial Statements October - November – to be included in State of Oregon Financial Statements

26

Reporting Property Not Owned by the UO To provide required information for leased asset year-end reporting To provide adequate insurance coverage FWIFLST – Banner query form to review inventory records Leased Property (LE/LP) Loaned Property (LN)

Loaned Property (LN)")

27

Real Property Performed in conjunction with BAO and Capital Construction Department Capitalization of construction in progress (CIP) expenses Conversion of completed projects into the Banner FIS real property records Componentization of specified buildings used extensively for research

expenses Conversion of completed projects into the Banner FIS real property records Componentization of specified buildings used extensively for research")

28

FY15 Governance change UO will be separate entity with different tax identification number Adopting all FY14 policies IIJVs will no longer be utilized Internal revenue account codes will be only for UO departments Moving away from Oregon State Treasury Facilities and administrative rate proposal Additional Cognos IDR reporting available

29

BAO Financial Services Contacts Accounting and Financial Management Contacts http://ba.uoregon.edu/staff/actg-and-finl-mgmt-contacts Cost Accounting, Financial Analysis, and Reporting http://ba.uoregon.edu/staff/actg-and-finl-mgmt-contacts Accounts Payable (6-3143) http://ba.uoregon.edu/staff/ap-invoice-payment Travel (6-3158) http://ba.uoregon.edu/staff/travel

Travel (6-3158)")

30

Useful Links Year End COB Instructions and Deadlines 2013-2014 http://ba.uoregon.edu/staff/year-end-close OUS Financial Statements http://www.ous.edu/dept/cont-div/accounting-reporting/annualfinreport

31

Closing Remarks

Similar presentations