Download presentation

Presentation is loading. Please wait.

1

Capital Consumption Don Mango American Re-Insurance 2003 CAS Ratemaking Seminar

2

Goals for Today Get you to admit this is a valid alternative framework (albeit orthogonal) to capital allocation / release / IRR Given it’s a possibility, demonstrate how it can be practically implemented as a means of pricing reinsurance

to capital allocation / release / IRR Given it’s a possibility, demonstrate how it can be practically implemented as a means of pricing reinsurance")

3

Two Bets Bet #1 You pay me $10 now I might pay you $50 later Bet #2 I pay you $10 now You might have to pay me $50 later

4

Payoff Diagrams

5

Bet #1 Spend then Maybe Receive You spend now, hope to receive later You spend NOW, voluntarily With the odds I give you, you can compute an expected value and decide if you want to make the bet

6

Bet #2 Receive then Maybe Spend You receive now, hope you don’t have to spend later You MAY spend LATER, involuntarily With the odds I give you, you can compute an expected value and decide if you want to make the bet

7

Capital? Bet #1 = $10 You spend $10 capital NOW no matter what The capital investment is current and certain – i.e., not contingent Allocated = spent

8

Capital? Bet #2 = $??? I should be sure you have $40 available LATER, but you don’t spend anything NOW If Bet #2 hits, you spend $40 capital LATER Capital expenditure (= allocation) is contingent and in the future

is contingent and in the future.")

9

Allocation vs Consumption Two different but equally valid frameworks for Treating capital Evaluating insurance business segments Developing indicated prices for reinsurance Nearly orthogonal

10

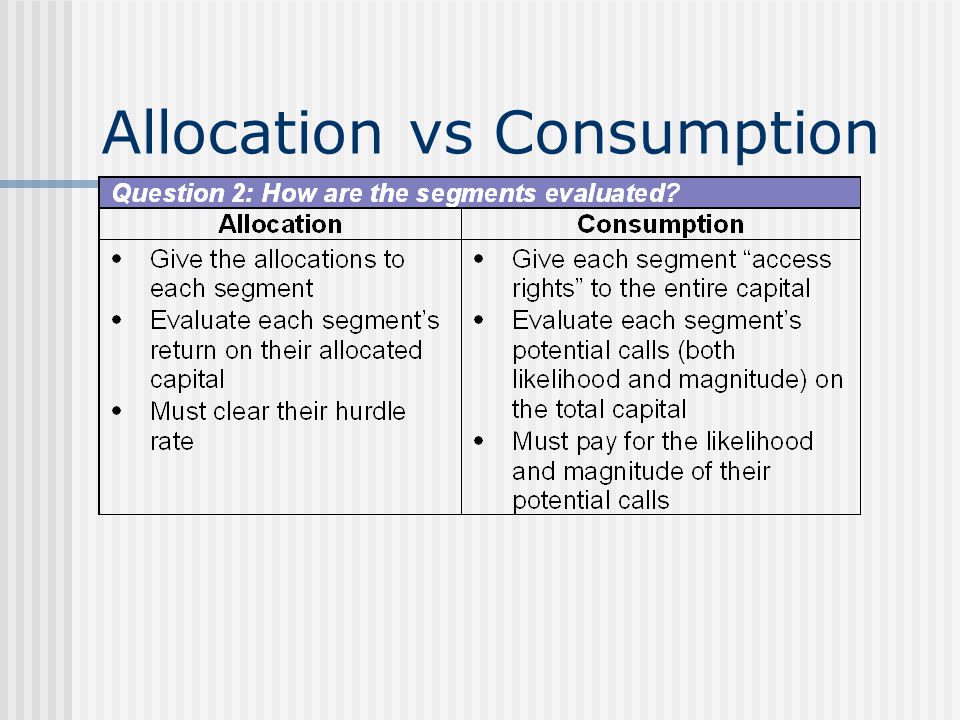

Allocation vs Consumption Four questions: 1. What do you do with the total capital? 2. How do you evaluate business segments? 3. What does it mean to be in a portfolio? 4. How is relative risk contribution reflected?

11

Allocation vs Consumption

13

This is THE CRITICAL SLIDE!

14

Allocation vs Consumption

15

Details of the Framework Scenario analysis Default-free discounting Scenario-level capital consumption Evaluation of capital consumption using a “quasi~utility” approach

16

Default-Free Discounting Conditional on its occurrence, a given scenario’s outcome is certain discount at the default-free rate Risk-adjusted discounting is too clumsy Overloaded operator Try splitting out default probability from price of risk in risky debt spreads Reflect uncertainty between scenarios, not within What is uncertainty within a scenario anyway? Do you believe the scenario is possible or not?

17

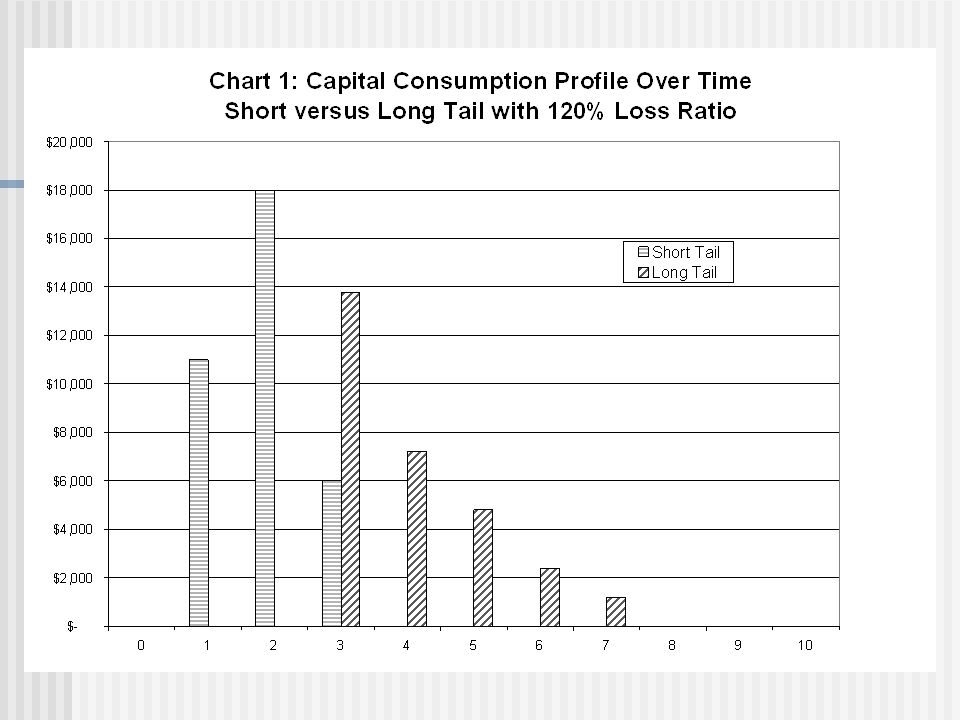

Scenario Capital Consumption Experience fund From Finite Reinsurance Fund into which goes all revenue, from which comes all payments Bakes in investment income When it drops below zero, and further payments need to be made, gotta “call the parents” for some capital That capital is spent CONSUMED

18

Experience Fund Long-Tailed LOB

19

Experience Fund Short-Tailed LOB

21

Capital Calls (Philbrick/Painter) The entire surplus is available to every policy to pay losses in excess of the aggregate loss component. We can envision an insurance company instituting a charge for the access to the surplus. This charge should depend, not just on the likelihood that surplus might be needed, but on the amount of such a surplus call.

22

Capital Calls (Philbrick/Painter) We can think of a capital allocation method as determining a charge to each line of business that is dependant on the need to access the surplus account. Conceptually, we might want to allocate a specific cost to each line for the right to access the surplus account. In practice though, we tend to express it by allocating a portion of surplus to the line, and then requiring that the line earn (on average) an adequate return on surplus.

an adequate return on surplus..")

23

Capital Call Cost Function Risk-based overhead expense loading Pricing decision variable Application of utility theory Borch (1961): To introduce a utility function which the company seeks to maximize, means only that such consistency requirements (in the various subjective judgements made by an insurance company) are put into mathematical form.

: To introduce a utility function which the company seeks to maximize, means only that such consistency requirements (in the various subjective judgements made by an insurance company) are put into mathematical form.")

24

Capital Call Cost Function Make the implicit explicit Express your preferences explicitly, in mathematical form, and apply them via a utility function The mythical Risk Appetite Enforce consistency in the many judgments being made

25

Implicit Preferences Preferences buried in Kreps’ “Marginal Standard Deviation” risk load approach: The marginal impact on the portfolio standard deviation is our chosen functional form for transforming a given distribution of outcomes to a single risk measure. Risk is completely reflected, properly measured and valued by this transform. Upward deviations are treated the same as downward deviations.

26

Property Cat Example

27

How would you do this with capital allocation? Allocate a percentage of the limit – say 5% -- based on marginal portfolio capital requirements? What does that mean? What happens if the event occurs? Where does the money to pay the claim come from? Does the sum of the marginals add up to the company’s total capital? If not, what does it mean?

28

Building Bridges Pricing via probability measure change – from voluminous capital markets literature Utility theory in pricing – from Halliwell, Heyer and Schnapp The Wang Transform – from Wang The market cost of risk – from Van Slyke Additive Co-Measures – from Kreps

29

Final Thought: This actually IS capital allocation for insurance, done right

30

And now… FIRE AWAY !

Similar presentations

Seminar on Ratemaking Nashville, TNRuss Bingham March 11-12, 1999Hartford Financial Services.>")

wage rate,>")