Download presentation

Presentation is loading. Please wait.

1

Monetary Policy Econ 102 2015

2

Key player in the financial markets: CENTRAL BANKS: Every sovereign nation has a bank which is the ‘lender of the last resort’. The Central Banks is a financial institution owned by the government, which is in charge of ‘managing the currency’ Money market equilibrium

3

Turkey: Türkiye Cumhuriyeti Merkez Bankası (TCMB) United Kingdom: Bank of England (BoE) United States: Federal Reserve System (FED) Board of Governors European Union: European Central Bank (ECB) Central Banks

United Kingdom: Bank of England (BoE) United States: Federal Reserve System (FED) Board of Governors European Union: European Central Bank (ECB) Central Banks")

4

1.Issuance of currency: Prints or mints notes and coins for the gov’t (usually backed by the gov’t bonds). 2.Reserve management: manages the foreign exchange reserves, buys and sells to influence the domestic currency value/ 3.Banker to the government: 4.Banker to the commercial banks: provides payment system for the transactions between banks, provides liquidity to the banks. Functions of the Central Bank

5

5.Maintains financial stability: lender of the last resort, emergency liquidity to solvent financial institutions, otherwise they may collapse. 6.Banking supervision: (BDDK) 7.Monetary Policy Function: prevent inflation. Functions of the Central Bank

7.Monetary Policy Function: prevent inflation. Functions of the Central Bank.")

6

1.Open Market Operations: CB buys and sells gov’t bonds in private financial markets. 2.Reserve Requirement Ratio: Minimum reserves that the commercial banks have to hold as reserves for a given deposits 3.Discount rate: Lending rate of the Central Bank to commercial banks Monetary Policy Tools

7

Assets Foreign government bonds (official international reserves) Gold (official international reserves) Domestic government bonds Loans to domestic banks (called discount loans in US) Liabilities Deposits of domestic banks Currency in circulation (previously central banks had to give up gold when citizens brought currency to exchange) Balance Sheet of the Central Bank

Gold (official international reserves) Domestic government bonds Loans to domestic banks (called discount loans in US) Liabilities Deposits of domestic banks Currency in circulation (previously central banks had to give up gold when citizens brought currency to exchange) Balance Sheet of the Central Bank")

8

Central Bank

9

Central Bank (TCMB) Balance Sheet

Balance Sheet")

10

1.One tool is the open market operations: CB can sell bonds and create shortages of liquid funds, this will decrease the price of bonds and increase the interest rates because the funds are scarce. 2. CB can change in the interest rate (discount rate) that they charge to the commercial banks that borrow from the CB in case of liquidity shortages. If the discount rate changes the market determined interest rates also change in the same direction. Money Market Operations and Control of Money Supply and interest rates

that they charge to the commercial banks that borrow from the CB in case of liquidity shortages. If the discount rate changes the market determined interest rates also change in the same direction. Money Market Operations and Control of Money Supply and interest rates.")

11

3.CB Bank can change the reserve requirement ratios. This determines the amount of loans that commercial banks can give for a given amount of deposits, hence the money multiplier. This tool is seldom used. Money Market Operations and Control of Money Supply and interest rates

12

Does the CB control MS or the Interest rate? Or both??? Money market i Can they use both at the same time? MS is the quantity and interest is “price” of money. Either the MS or the interest rate (Either the quantity or the price)

.")

13

Which one is easier to control? - Your can control the narrowest money supply (which is the liquidity – bank notes and coins) - It is more difficult to control broad money supply (liquidity plus demand deposits (M1)) Does CB control MS or the interest rate?

- It is more difficult to control broad money supply (liquidity plus demand deposits (M1)) Does CB control MS or the interest rate .")

14

Inflation targeting Monetary targeting Exchange rate targeting Discretionary monetary policy. Alternative Central Bank Policies

15

Transmission mechanism of the monetary policy. Example: MS increase (interest rate declines), Desired Investment expenditures increase, Aggregate expenditures increase, (Aggregate Demand increase) Hence, OUTPUT increases. BUT, there will be an effect on PRICE and/or EXCHANGE RATES Simple Monetary Policy

, Desired Investment expenditures increase, Aggregate expenditures increase, (Aggregate Demand increase) Hence, OUTPUT increases. BUT, there will be an effect on PRICE and/or EXCHANGE RATES Simple Monetary Policy.")

16

Consumer and Producers do not have static views, they look into the future and form ‘expectations’. They form expectations about future prices, or the rate of change of prices. In all their consumption, production and labor supply decisions they take the expected inflation rate into consideration. What is your expected rate of inflation today for the next year in Turkey? Expectations

17

Turkey’s disinflation policy

18

Policy change Fiscal Deficit Monetization of fiscal deficit Weak banking system INFLATION Tight fiscal policy Central Bank independence Banking reforms DISINFLATION

19

Governments make a CB law which says that CB is independent and has the objective of controlling inflation and growth. Central Bank Independence

20

To achieve price stability they set an inflation target rate of x percent for the CPI increase in the following 12 months. Then makes monthly forecasts of inflation looking two years ahead. Then decides whether the interest rates should be changed to avoid a deviation from the target. Inflation targeting

21

If credible everybody will adjust their expected inflation to the one announced by CB. If they are not credible, because for example if they believe that with coming elections that will resort to expansionary policy, hence they will not be able to control the inflation rate... Central Bank

22

Inflation experience

23

Disinflation experience

24

Inflation realized and expected CBRT “inflation is expected to be between 8.2 and 9.4 % (with a mid- point of 8.17 percent) at the end of 2014.” Inflation report 2013.

at the end of Inflation report 2013.")

25

Inflation report of 2014

26

TCMB Policies

27

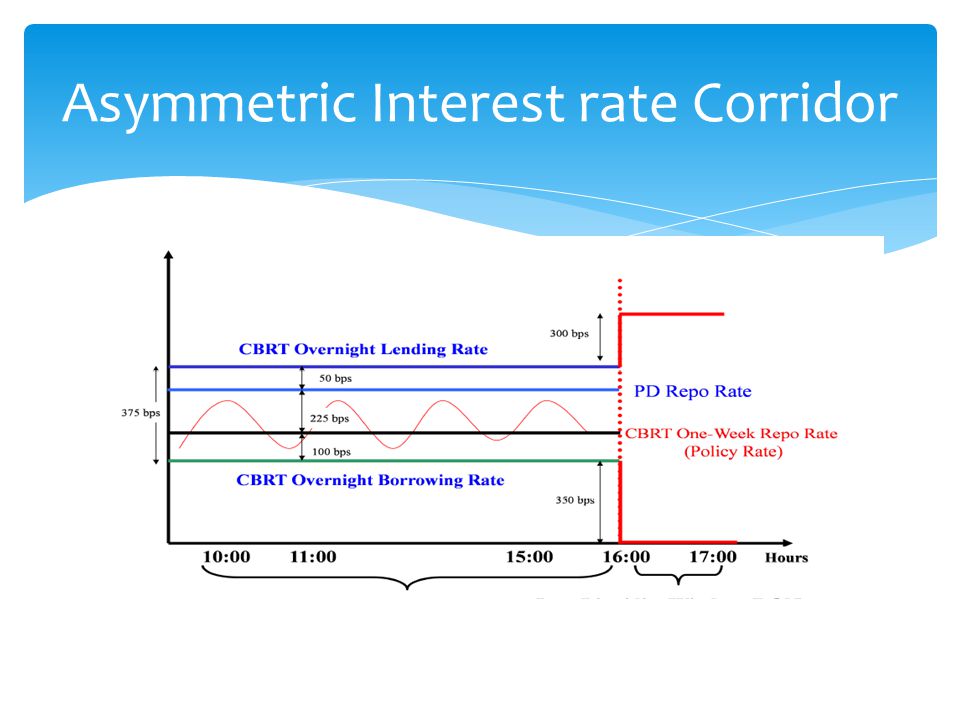

Asymmetric Interest rate Corridor

29

Since 2010

30

Commercial banks voluntarily hold part of their reserve requirements in terms of foreign exchange and gold. Weaken the effect of capital flows to exchange rates and bank lending Reserve Option Mechanism

31

What are the other factors that affect the rate of inflation rate other than money supply growth rate? Fiscal policy, Developments affecting business and trade in the country, Developments affecting households Developments affecting labor markets, unemployment Wages and input prices Foreign exchange and stock prices Why the CB can not target one level of inflation rate?

32

Lags –delays between the start of the problem, and the effect of the policy. Recognize the problem, decide on the action and implementing, then the effect will be observed.... Delays Others... Other difficulties of monetary policy

Similar presentations

M1 – money, narrow money (cash + demand deposits) M2 –>")

Lecturer: Mr S. Puran Topic: Central Banking and the Monetary System.>")