Download presentation

Presentation is loading. Please wait.

1

Managerial Economics Professor Geoffrey Heal 616 Uris Hall

Phone: (212) (note - gmh “one” not “L”)

(note - gmh one not L )")

2

Course Outline: (I) Analyzing the structure of a market

Part A: Demand & Supply Part B: Costs (II) Pricing (most important part of course) (III) e-con.com (application and review) (IV) Foundations of Strategy

Pricing (most important part of course) (III) e-con.com (application and review) (IV) Foundations of Strategy.")

3

Analyzing the Structure of a Market

Aim: to understand key aspects of markets: nature of demands for the products closeness or otherwise of competitors structure of costs dependence of profits on the level of output

4

Material to be covered:

Analysis of demand demand curves, price, income & cross elasticities of demand use of demand parameters in forecasting Structure of costs: fixed & variable costs break-even analysis opportunity costs and sunk costs learning curves & economies of scale.

5

Pricing How much product should you produce and what price should you charge for it? How can you best segment your market if there are different types of buyers with different demand characteristics (e.g., business travelers vs. vacation travelers, home PC buyers vs. corporate buyers)? What are the types of pricing schemes available (e.g., bundling, promotional offers, loyalty bonuses, volume discounts)?

What are the types of pricing schemes available (e.g., bundling, promotional offers, loyalty bonuses, volume discounts)")

6

e-con.com e-commerce business strategies.

Applications of market analysis to electronic commerce How does the internet affect demand, pricing, and other aspects of running a business. e-commerce business strategies. Auctions and the internet.

7

Foundations of Strategy

Interacting with competitors Anticipating their reactions Forecasting the final outcome when everyone has reacted.

8

Aim of Course To teach you to use basic economic ideas in making business decisions. Decisions about opening and closing businesses. Decisions about pricing and other policies.

9

Level of Course Emphasis on understanding concepts and where and how they can be used. Don’t aim to make you an economist, but an intelligent consumer of economics. Evaluate and understand works of consultants, staff. Ask the right questions. Recognize BS when you see it!

11

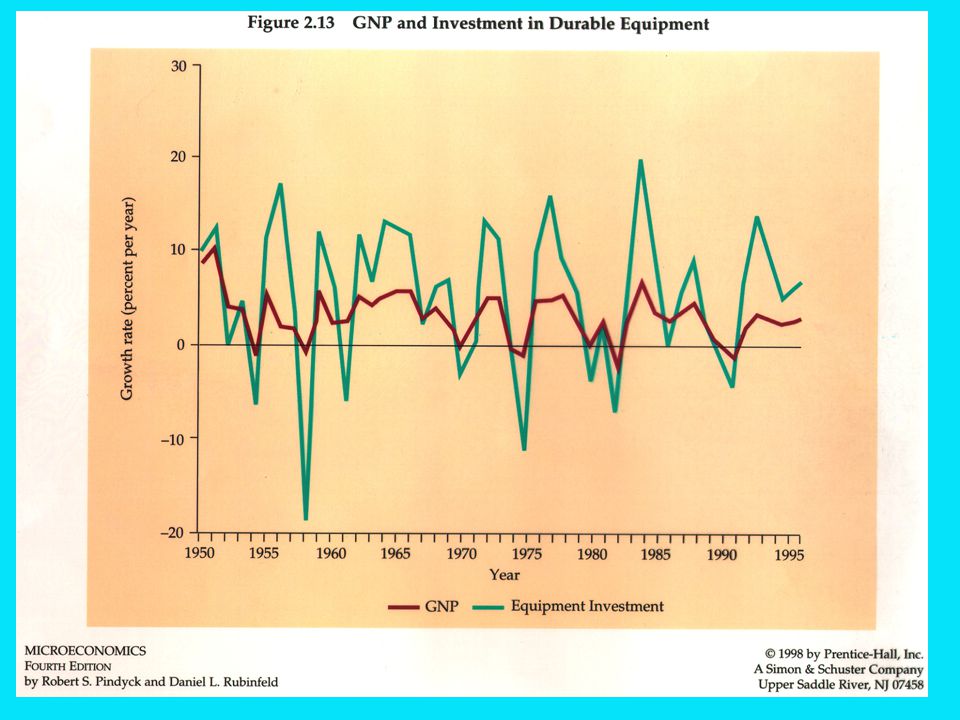

Consumption & Price of Copper 1880-1998

14

Compare Internet companies

eBay AOL Yahoo Amazon.com

15

Demand and Supply

16

Demand Curve Shows amount purchased as a function of price Depends on:

- income - tastes - prices of competitive products - prices of complementary products

17

Supply Curve Amount offered for sale as a function of price

Depends on costs of production, which in turn depend on - costs of inputs - technology

18

The Market Mechanism S P0 D Q0 Price ($ per unit)

The curves intersect at equilibrium, or market- clearing, price. At P0 the quantity supplied is equal to the quantity demanded at Q0 . P0 Q0 Quantity 12

19

The Market Mechanism Characteristics of the equilibrium or market clearing price: QD = QS No shortage No excess supply No pressure on the price to change 13

20

Demand Curve -Income Rises

21

Demand Shifts

22

Supply shifts

23

D & S shift

24

The Market Mechanism Surplus S D Q1 P1 Q2 P2 Q3 Price ($ per unit)

Quantity Price ($ per unit) S D Q1 Assume the price is P1 , then: 1) Qs : Q1 > Qd : Q2 2) Excess supply is Q1:Q2. 3) Producers lower price. 4) Quantity supplied decreases and quantity demanded increases. 5) Equilibrium at P2Q3 P1 Surplus Q2 P2 Q3 17

S. D. Q1. Assume the price is P1 , then: 1) Qs : Q1 > Qd : Q2. 2) Excess supply is Q1:Q2. 3) Producers lower price. 4) Quantity supplied decreases and quantity demanded increases. 5) Equilibrium at P2Q3. P1. Surplus. Q2. P2. Q")

25

The Market Mechanism The market price is above equilibrium A Surplus

There is excess supply Producers lower prices Quantity demanded increases and quantity supplied decreases The market continues to adjust until the equilibrium price is reached. 19

26

The Market Mechanism S Shortage D Q3 P3 Q1 Q2 P2 Price ($ per unit)

Quantity Price ($ per unit) S D Assume the price is P2 , then: 1) Qd : Q2 > Qs : Q1 2) Shortage is Q1:Q2. 3) Producers raise price. 4) Quantity supplied increases and quantity demanded decreases. 5) Equilibrium at P3, Q3 Q3 P3 Q1 Q2 P2 Shortage 22

S. D. Assume the price is P2 , then: 1) Qd : Q2 > Qs : Q1. 2) Shortage is Q1:Q2. 3) Producers raise price. 4) Quantity supplied increases and quantity demanded decreases. 5) Equilibrium at P3, Q3. Q3. P3. Q1. Q2. P2. Shortage. 22.")

27

The Market Mechanism The market price is below equilibrium: Shortage

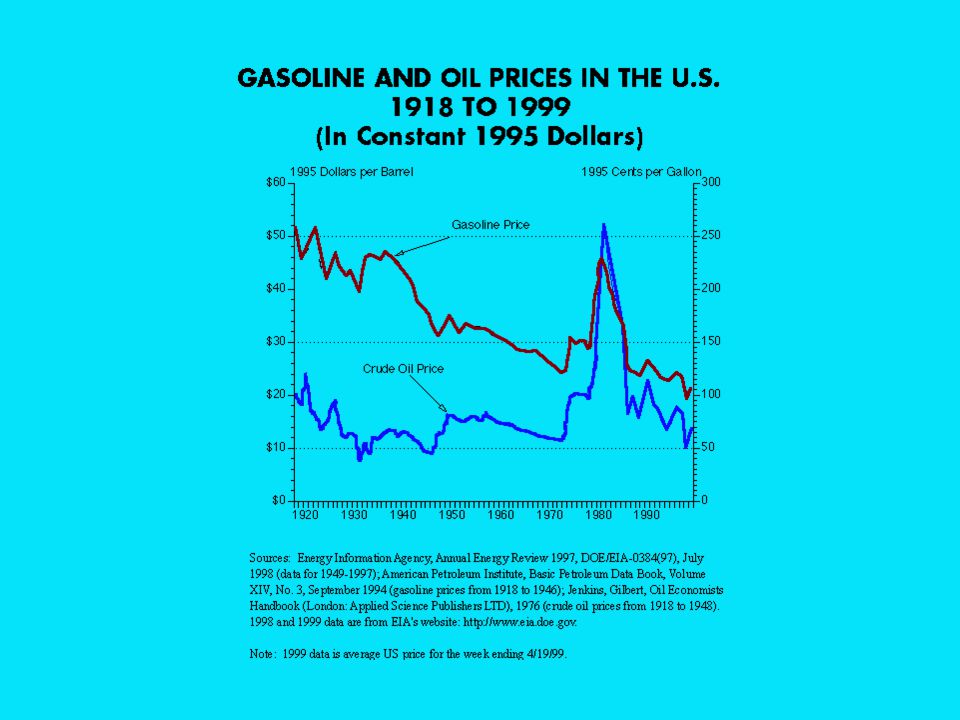

There is a shortage Producers raise prices Quantity demanded decreases and quantity supplied increases The market continues to adjust until the new equilibrium price is reached. 24

28

The Market Mechanism Market Mechanism - Summary:

1) Supply and demand interact to determine the market-clearing price. 2) When not in equilibrium, the market will adjust to alleviate a shortage or surplus and return the market to equilibrium. 3) Markets must be competitive for the mechanism to be efficient. 25

Supply and demand interact to determine the market-clearing price. 2) When not in equilibrium, the market will adjust to alleviate a shortage or surplus and return the market to equilibrium. 3) Markets must be competitive for the mechanism to be efficient. 25.")

31

Consumption & Price of Copper 1880-1998

32

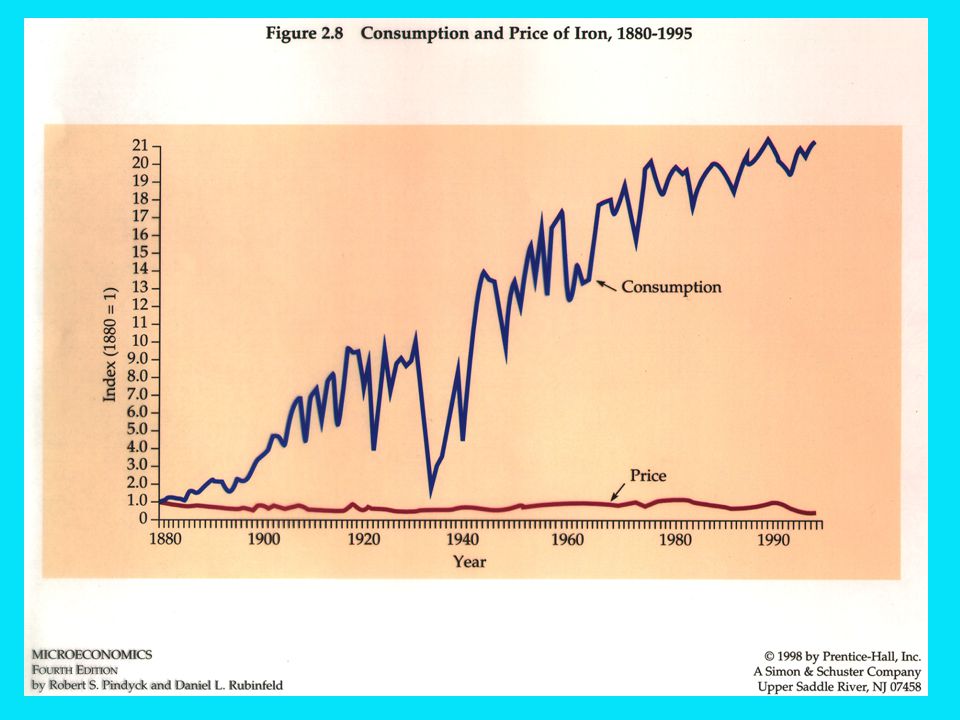

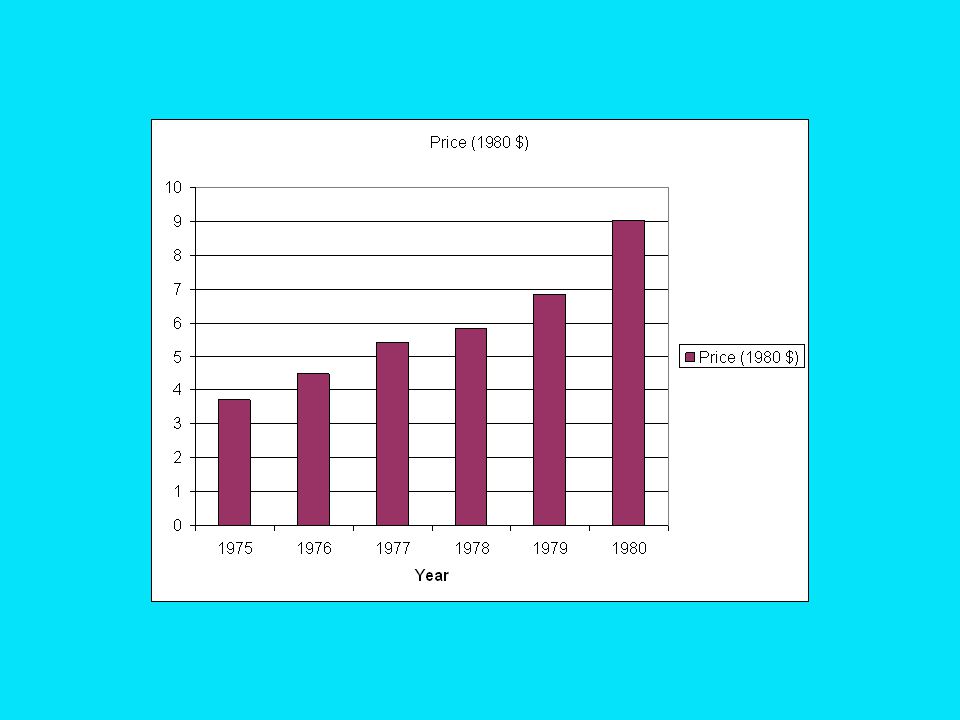

The Long-Run Behavior of Natural Resource Prices

Observations Consumption of copper has increased about a hundred fold from 1880 through 1998 indicating a large increase in demand. The real price for copper has remained relatively constant. 59

33

Changes In Market Equilibrium

D1998 S1950 D1950 Quantity Price S1900 D1900 Long-Run Path of Price and Consumption 63

34

Changes In Market Equilibrium

Conclusion Decreases in the costs of production have increased the supply by more than enough to offset the increase in demand. 64

35

Changes In Market Equilibrium

Wage Inequality in the United States Real after-tax income from 1977 to 1999: Rose 40+% for the top 20% of the income distribution Fell 10+% for the bottom 20% 26

36

Changes In Market Equilibrium

Question Why did the income distribution become more unequal for 1977 to 1999? 26

37

Price elasticity of demand:

Measures responsiveness of demand to price. Defined as E = (DQ/Q)/(DP/P) = (DQ/DP)*(P/Q) Why is it defined in proportional terms? - Unit free. - Scale sensitive. A negative number.

/(DP/P) = (DQ/DP)*(P/Q) Why is it defined in proportional terms - Unit free. - Scale sensitive. A negative number.")

39

Elasticity = (DQ/Q)/(DP/P) = (DQ/DP)*(P/Q) = -2*(P/Q)

Q = 8 - 2P or P = Q Elasticity = (DQ/Q)/(DP/P) = (DQ/DP)*(P/Q) = -2*(P/Q)

/(DP/P) = (DQ/DP)*(P/Q) = -2*(P/Q)")

40

Elasticity and Pricing

If elasticity is between 0 and -1 then raising price will raise profits - it will raise revenues and lower costs. If elasticity is lower than -1 then raising price will lower revenues and also costs, so the effect on profits is not clear. Moral - never operate where the elasticity is between 0 and -1.

41

Relationship between demand, quantity and revenue:

Q = 8 - 2P or P = Q so as revenue R is price times quantity R = 4Q - 0.5Q2

42

Revenue rises as price rises

Revenue falls as price rises PED = -1 PED = 0

43

This is a quadratic pointing up.

The slope is: DR DQ which is zero at Q = 4. Slope is positive for Q<4 and vice versa. Maximum revenue comes when Q = 4, therefore P = 2, and max revenue is 8 = 4 - Q

44

PED when revenue is maximum

Revenue is max when Q = 4, P = 2. E = (DQ/Q)/(DP/P) = (DQ/DP)*(P/Q) So E = (DQ/DP)*(1/2) and DQ/DP = -2 so E = -2 * 1/2 = -1 when R is at a maximum.

/(DP/P) = (DQ/DP)*(P/Q) So E = (DQ/DP)*(1/2) and. DQ/DP = -2 so E = -2 * 1/2 = -1 when R is at a maximum.")

45

Cross price elasticity of demand:

The responsiveness of demand for good A to change in price of good B: DQA/QA = DQA * PB DPB/PB DPB PA Example: responsiveness of demand for Dell computers to prices of Gateway computers

46

Goods are Complements:

Cross PED is negative (autos and gasoline) Goods are substitutes-competitors: Cross PED is positive (Dell vs. Gateway)

Goods are substitutes-competitors: Cross PED is positive (Dell vs. Gateway)")

47

Demand elasticities in the home PC market.

Jerome Foncel and Marc Ivaldi, Ecole des Hautes Etudes en Science Sociales, Toulouse.

48

Supply Elasticity The responsiveness of supply to price changes.

(DS/S)/(DP/P), proportional change in supply divided by proportional change in price. Usually positive.

/(DP/P), proportional change in supply divided by proportional change in price. Usually positive.")

49

Elasticities of Supply and Demand

The Market for Wheat 1981 Supply Curve for Wheat QS = 1, P 1981 Demand Curve for Wheat QD = 3, P

50

Elasticities of Supply and Demand

The Market for Wheat Equilibrium: Q S = Q D

51

Elasticities of Supply and Demand

The Market for Wheat ED=(P/Q) (DQD/DP) = (3.46/2630)(-266)= -0.35 ES=(P/Q) (DQS/DP) = (3.46/2630)(+240)= 0.32

(DQD/DP) = (3.46/2630)(-266)= ES=(P/Q) (DQS/DP) = (3.46/2630)(+240)=")

52

Changes in the Market: 1981-1998

The Market for Wheat Supply (Qs) Demand (QD) Equilibrium Price (Qs = QD) P P P = P P = P1981 = $3.46/bushel 1998 1, P 3, P 1, P = 3, P P1998 = $2.65/bushel 66

Demand (QD) Equilibrium Price (Qs = QD) P P P = P 506P = 1750 P1981 = $3.46/bushel , P 3, P 1, P = 3, P P1998 = $2.65/bushel. 66.")

53

Marginal Revenue Increase in revenue from one extra sale

Rate of change of revenue with respect to sales Typically less than price as demand curve slopes down Depends on PED

54

Relationship between demand, quantity and revenue:

Q = 8 - 2P or P = Q so as revenue R is price times quantity R = 4Q - 0.5Q2

55

This is a quadratic pointing up. Slope is MR, which is DR/DQ

This is a quadratic pointing up. Slope is MR, which is DR/DQ. As R = 4Q Q2, slope is Q, which is zero at Q = 4. Slope is positive for Q < 4 and vice versa. So MR is > 0 for Q < 4 and MR < 0 for Q > 4. Maximum revenue comes when Q = 4, therefore P = 2, and max revenue is 8

56

PED when revenue is maximum

Revenue is max when Q = 4, P = 2. E = (DQ/Q)/(DP/P) = (DQ/DP)*(P/Q) So E = (DQ/DP)*(1/2) and DQ/DP = -2 so E = -2 * 1/2 = -1 when R is at a maximum.

/(DP/P) = (DQ/DP)*(P/Q) So E = (DQ/DP)*(1/2) and. DQ/DP = -2 so E = -2 * 1/2 = -1 when R is at a maximum.")

58

Marginal Revenue & PED MR = P{1 + 1/PED}

Remember PED < 0 so MR < P. The larger PED as a number the nearer MR is to P If PED = - 1, then MR = 0. (Top of revenue curve) ………………………………………… Derivation - dR/dQ = d{P(Q).Q}/dQ = P + Q*dP/dQ = P{1 + (Q/P)*dP/dQ}

………………………………………… Derivation - dR/dQ = d{P(Q).Q}/dQ. = P + Q*dP/dQ. = P{1 + (Q/P)*dP/dQ}")

59

Income Elasticity of Demand:

Responsiveness of demand to changes in income IED = (DQ/Q)/DI/I) = (DQ/DI)*(I/Q) Use to define necessities and luxuries

/DI/I) = (DQ/DI)*(I/Q) Use to define necessities and luxuries.")

60

Necessities - IED < 1 Luxuries - IED > 1 Cyclical vs. defensive sectors Cyclical - high IED - foreign travel, consumer durables Defensive - low IED - food, utilities

63

Short-run vs. long-run elasticities

Critical in understanding oil market, energy markets, metal markets Responding to a price movement takes time - possibly many years Long-run elasticity measures total response Short-run elasticity measures immediate response

64

Short-run demand P1 Po Long-run demand Short-run drop in demand Long-run drop in demand

65

Short-Run Versus Long-Run Elasticities

The Demand for Gasoline Years Following Price or Income Change Elasticity Price Income 93

66

Short-Run Versus Long-Run Elasticities

The Demand for Automobiles Years Following Price or Income Change Elasticity Price Income 93

67

Short-Run Versus Long-Run Elasticities

The Demand for Gasoline and Automobiles Data Explains: 1) Why the price of oil did not continue to rise above $30/barrel even though it rose very rapidly in the early 1970s. 2) Why automobile sales are so sensitive to the business cycle. 95

Why the price of oil did not continue to rise above $30/barrel even though it rose very rapidly in the early 1970s. 2) Why automobile sales are so sensitive to the business cycle. 95.")

68

The World Oil Market In 1995: P* = $18/barrel

World demand and total supply = 23 bb/yr (= 63 mbd) OPEC supply = 10 bb/yr (= 27 mbd) Non-OPEC supply = 13 bb/yr (= 35 mbd) US consumption about 17 mbd = 5.5 bb/yr 129

OPEC supply = 10 bb/yr (= 27 mbd) Non-OPEC supply = 13 bb/yr (= 35 mbd) US consumption about 17 mbd = 5.5 bb/yr")

69

Price of Crude Oil

71

Price Elasticity Estimates

Short-Run Long-Run World Demand: Competitive Supply (non-OPEC) 130

130.")

72

Upheaval in the World Oil Market

Short-Run Impact of a stoppage of Saudi Production equal to 3 bb/yr (= 8 mbd). Short-run Demand D = P Short-run Competitive Supply SC = P 131

. Short-run Demand. D = P. Short-run Competitive Supply. SC = P")

73

Upheaval in the World Oil Market

Short-Run Impact of a stoppage of Saudi Production equal to 3 bb/yr. Short-run Total Supply--before supply reduction (includes OPEC, 10bb/yr) ST = P Short-run Total Supply--after supply reduction ST = P 132

ST = P. Short-run Total Supply--after supply reduction. ST = P")

74

Upheaval in the World Oil Market

New Price After Reduction Demand = Supply P = P P = 41.08 133

75

Impact of Saudi Production Cut

18 ST S’T SC D Price ($ per barrel) 45 Short-Run Effect 40 35 30 25 20 15 10 5 Quantity (billions barrels/yr) 5 10 15 20 23 25 30 35 134

45. Short-Run. Effect Quantity. (billions barrels/yr)")

76

Upheaval in the World Oil Market

Long-Run Impact of a stoppage Saudi Production equal to 3 bb/yr.. Long-run Demand D = P Long-run Total Supply S = P 136

77

Upheaval in the World Oil Market

New Price is found setting long-run supply equal to long-run demand: P = P P = 21.75 137

78

Impact of Saudi Production Cut

SC ST Due to the elasticity of the long-run supply and demand curves, the long-run effect of a cut in production is much less. S’T Long-run Effect Price ($ per barrel) 45 D 40 35 30 25 20 18 15 10 5 Quantity (billions barrels/yr) 5 10 15 20 23 25 30 35 139

45. D Quantity. (billions barrels/yr)")

79

- market research and pricing policy - forecasting

Uses of elasticities - market research and pricing policy - forecasting

80

Examples: 1. Spring 1990 - sales of BMWs in the US fell sharply

Possible explanations: (a) rising D mark pushed US prices up “too high” (b) entry of Lexus and Infiniti at lower prices had drawn away sales (c ) recession lowered incomes of target market

rising D mark pushed US prices up too high (b) entry of Lexus and Infiniti at lower prices had drawn away sales. (c ) recession lowered incomes of target market.")

81

(a) depends on own price elasticity of demand

(b) depends on cross PED between BMW and Lexus-Infiniti (c ) depends on IED for BMW

depends on cross PED between BMW and Lexus-Infiniti. (c ) depends on IED for BMW.")

82

The price of oil in 2020 Project user income growth by 2020: call this G% Multiply G by IED for oil: G*IED gives growth in demand for oil by 2020 at constant prices Estimate possible % growth in supply by 2020 (at constant prices). Call this S. Suppose S < G*IED

. Call this S. Suppose S < G*IED.")

83

Then if prices were to stay constant demand would rise more than supply. So price must rise to keep the two equal How much? Enough to reduce demand by (G*IED-S)%. Call this R: R = (G*IED - S) A 1% rise in price reduces demand by PED%: hence to reduce demand by R = (G*IED - S)% we need a price rise of R/PED

%. Call this R: R = (G*IED - S) A 1% rise in price reduces demand by PED%: hence to reduce demand by R = (G*IED - S)% we need a price rise of R/PED.")

84

Example: Let growth of user incomes to 2020 be 3% p.a. = 1.03 = 86% in total Let IED be 1.1 The demand growth by 2020 = G*IED = 86*1.1 = 95%

85

Let supply growth S be 30% Then demand growth exceeds supply growth by = 65% Assume PED in the long run is Then price growth must be 50% This may raise S: rework with a bigger S

86

Lessons on Demand and Supply

Formalism of demand and supply curves provides tools for analyzing how various shocks (input costs, customers’ income, competitors’ prices, etc.) affect own sales and prices.

affect own sales and prices.")

87

Elasticities provide useful summary numbers that feed into these analyses

Short Run Long Run. Use numbers appropriate to the time scale of the decision

88

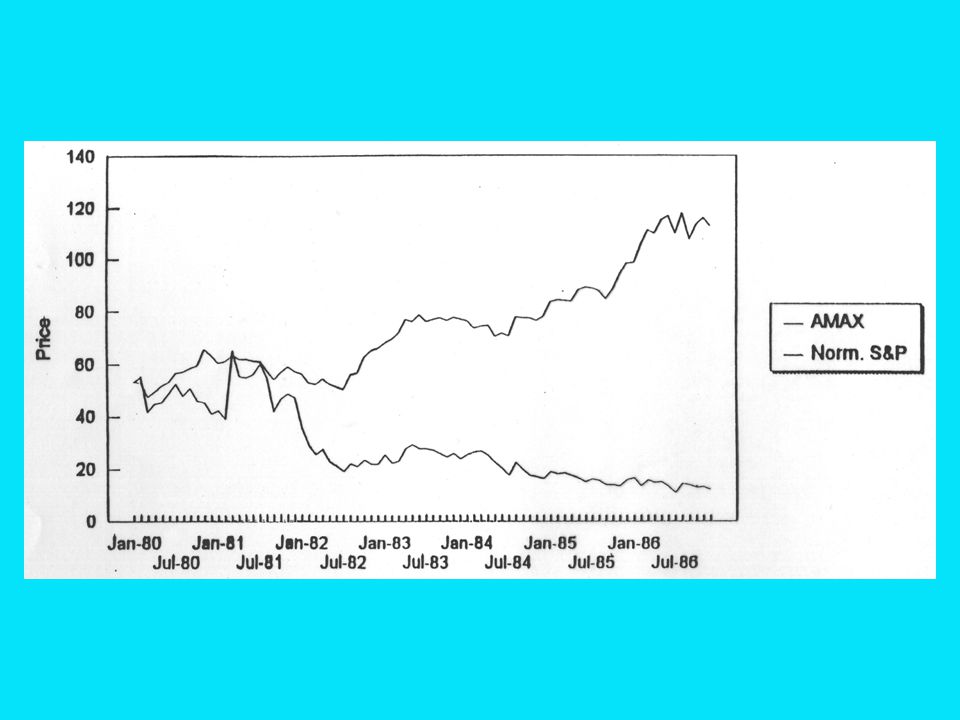

AMAX Case

91

Marginal Costs

Similar presentations

![Demand and Elasticity A high cross elasticity of demand [between two goods indicates that they] compete in the same market. [This can prevent a supplier.](/16/4932269/big_thumb.jpg "Demand and Elasticity A high cross elasticity of demand [between two goods indicates that they] compete in the same market. [This can prevent a supplier.>")